Author: BEWATER GIGA-BRAIN Source: X,@BewaterOffical

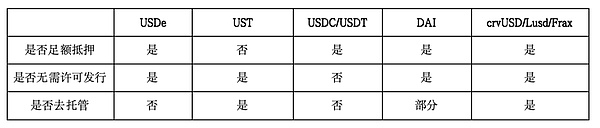

1. USDE Definition: The half -center center of the mortgage is stable coin

There are many classification methods for stable currency, such as:

(1) Toply mortgage and non -enough mortgage

(2) Centralized hosting and non -central custody

(3) Issuing and centralized institutions on the chain

(4) Licensing and no permits need

There are also some overlapping and changes. For example, in the past, we believe that the supply and circulation of algorithms such as AMPL and UST are completely stable coins of the algorithm section.According to this definition, most stablecoins are non -foot mortgage stablecoins, but there are exceptions, such as LUMITERRA’s LUAUSD. Although the price of casting and destruction is adjusted by the algorithm, the agreement vault provides mortgage of not less than luausd anchor value.The objects (USDT & amp; USDC), Luausd also has the dual attributes of algorithm stable coins and sufficient mortgage stable coins.

Another example is DAI. When the DAI mortgage is 100%chain asset, DAI belongs to non -central custody stable coins, but after the introduction of RWA, some mortgagers are actually controlled by reality. DAI transformed into the center of the center to the centerHua and non -centralized hybrid custody.

Based on this, we can peel off too complicated classifications, abstract whether there are three core indicators: whether there are sufficient mortgages, no license issuance, and whether to host.In contrast, the three attributes of USDE and other common stablecoin are partially different.If we think【Decentralization】Need to be satisfied at the same time[No need to license issuance]and【Go to host】Two conditions, then the USDE is not in line, so it is classified as【The half -central center of the mortgage stable currency】It is suitable.

>

2. Analysis of mortgage value analysis

The first question is whether the USDE has sufficient mortgage, and the answer is obviously positive.As described in the project document, the USDE mortgage is a synthetic asset of encrypted assets and corresponding short futures positions as mortgages.

Synthetic asset value = spot value+short futures head inch value

In the initial state, the spot value = x, the futures of futures = 0, assuming that the base difference is y

Mortgage value = x+0

假设一定时间后现货价格上涨a美元,而期货头寸价值上涨了b美元(a、b可以为负)头寸价值=X+a-b=X+(a-b),基差变为Y+ΔY,其中ΔY =(A-B) can be seen that if Δy is unchanged, the inherent value of the position will not change. If Δmber is a positive number, the internal value of the position will rise, otherwise it will fall.In addition, for the delivery contract, the initial state of the basis is generally negative, and the basis difference will gradually become 0 when the delivery day (no consider trading friction), which means that AY must be positive, so if synthesis is synthesized, if it is synthesized,The basis is Y, and the composite port value will be higher than the initial state during the delivery day.

The asset portfolio of holding the spot and short futures is also called “current arbitrage”. This arbitrage structure itself is not risky (but there is external risk). According to the current data, the constructing investment portfolio can get about 18%of about 18%.Low -risk annualized income.

>

We returned to Ethena, and I did not find accurate definition on the official website on the use of delivery contracts (considering the depth of transaction, the probability of perpetual contracts is relatively high), but the address and CEX distribution of the mortgage chain and CEX distribution of the mortgage objects and CEX distributionEssence

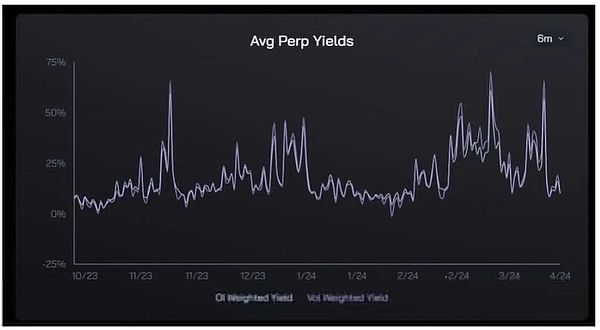

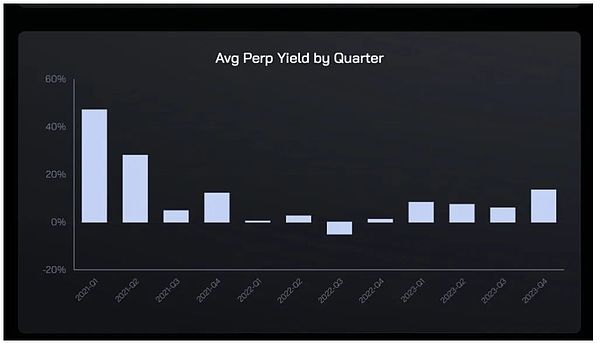

In the short term, there will be some differences in these two methods. The delivery contract will provide a more “stable and predictable” yield, and the expiration income is always positive.The perpetual contract is a product of a fluctuation rate, and the daily interest rate may be negative under certain circumstances.However, from experience, the arbitrage history of sustainable contracts will be slightly higher than the delivery contract, and both are positive:

1) Delta’s neutral futures airdrop is the essential borrowing funds. It is impossible to maintain 0 interest rates or negative interest rates for borrowing funds for a long time, and this position has piled up the risk of USDT risks and centralized exchanges.So the necessary yield & gt; the dollar no risk yield.

2) Sustainable contracts need to withstand variable due yields and pay additional risk premiums.

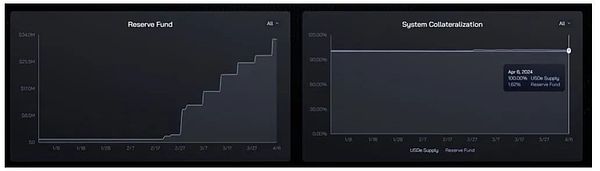

Based on this, it is completely wrong to worry about “USDE” assets or USDE.According to the mortgage risk assessment framework introduced according to the article, the current core/narrow mortgage coefficient of USDE is 101.62%. After incorporating the market value of ENA 1.57 billion US dollars into consideration, the generalized mortgage coefficient can reach 178%.

>

[Potential negative rates will cause USDE mortgage to shrink]It is not a big problem.According to the large number of theorems, as long as the time is long, the frequency will inevitably converge to the probability, and the USDE mortgage will maintain a growth rate of the average funding rate for a long time.

>

Change the more popular saying: You can draw a piece from the poker unlimited times. If you draw the size of the size, you will lose $ 1, and you can earn $ 1 in the other 52 other.In the case of $ 100 in principal, do you need to worry that because the king is bankrupt too much? It is more intuitive to see the data directly. The average contract rate in the past 6 months is only at 0%.The historical winning percentage is much higher than that of pumping cards.

>

Where is the real risk?

1. Market capacity risk

Now we have made it clear that the risk of mortgage is not worth worrying.But this does not mean that there are no other risks.The most noteworthy is the potential restrictions on Ethena in the contract market.

The first risk is liquidity risk.At present, the circulation of USDE is about 2.04 billion U.S. dollars, of which ETH and LST have a total of about 1.24 billion US dollars, which means that it needs to be set up with a short position of $ 1.24 billion under the case.

>

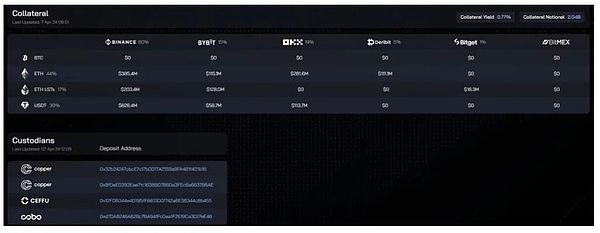

The current Binance ETH perpetual contract is about $ 3 billion, and 78%of the Ethena USDT reserve reserve is stored in Binance. Assume that the use of funds is uniform, which means that Ethena needs to open 2.04 billion*61%*78.%= 970 million short positions of nominal value have accounted for 32.3%of the position.

The proportion of Ethena’s positioning on the Binance or other derivatives exchanges will have a lot of negative effects, including:

1) It may cause transaction friction to become larger

2) Unable to cope with large -scale redemption in a short time

3) The supply of USDE pushing up the short position leads to a decline in rates and affects the rate of return

Although some mechanical design may be able to slow down the risk, such as setting time -based cast/destruction upper limit and dynamic rate (LUNA introduced this mechanism), a better way is not to danger.

According to these data, the combination of Binance+ETH transactions can be very close to the limit.But you can also break through this limit by introducing multi -currency categories and more exchanges.According to the tokenInSight data, Binance occupies a 50.1%share of the derivatives trading market. According to Coinglass data, in addition to ETH, the total positioning of the TOP10 currency in Binance is about three times that of ETH. According to these two data, the estimate is estimated:

The upper limit of the USDE market capacity theory = 20.4 (628/800)*60%/4/50.1%= $ 12.8 billion

The bad news is that the USDE has a capacity limit, and the good news is that there is still 500%of the growth space from the upper limit.

Based on these two upper limits, we can divide the size of the USDE into three stages:

(1) 0-20 billion: This scale is reached through the market on the Binance

(2) 2 billion to 12.8 billion: You need to expand the mortgage to the mainstream currency of the market deeply+make full use of the market capacity of other exchanges

(3) More than 12.8 billion: need to rely on the growth of the Crypto market itself+introduce additional mortgage management methods (such as RWA, lending market position)

It should be noted that if the USDE hopes that the real FLIP is truly centralized, at least it needs to exceed USDC to become the second largest stablecoin., Will be a relatively big challenge.

>

2. Host risk

Another controversy of Ethena is that the funds of the agreement are custody by a third -party agency.This is a compromise based on the current market environment.CoingLASS data shows that the total amount of BTC contracts in DYDX is 1.19 million US dollars of 1.48%of Binance and 2.4%of Bybit.Therefore, through the centralized exchanges, the management position of the centralized exchange is unavoidable for Ethena.

>

But it should be pointed out that Ethena uses the “Off-EXCHANGESETETLEMENT” hosting method.Simply put, the funds managed through this method will not really enter the exchange, but are transferred to a special address for management. Usually the client (that is, Ethena), the custodian (third -party custodian agency), and the exchange of the exchanges.At the same time, the exchanges generate the corresponding amount in the exchange based on the scale of the custody funds. These funds can only be used for trading and cannot be transferred; afterwards, settlement is settled according to the profit or loss.

The biggest benefit of this mechanism is exactly it is exactly[Eliminate the single -point risk of a centralized exchange]Because the exchanges have never really controlled the funds, at least the two -party signature of the three parties can be transferred to transfer.On the premise of the custodian institution, this mechanism can effectively avoid the exchange Rug (such as FTX) and the project party Rug.In addition to the Copper, CEFFU, COBO listed by Ethena, Sinohope and FireBlocks also provide similar services.

Of course, the custodian agency also has theoretical possibility of evil, but based on the current CEX still occupies absolute dominance+frequent security incidents on the chain, this half -center center is a local optimal solution, not the final form, not the final form, not the final form, not the final form, not the final form, not the final form.But after all, APY is not free. The key is whether to bear these risks for the improvement of income and efficiency.

3. Interest rate sustainable risk

USDE requires pledge to obtain income. Since the pledge rate will not be 100%, the yield of Susde will be higher than the derivative rate. At present, the USDE pledged in the contract is about 470 million US dollars, and the pledge rate is only about 23%.The underlying asset APY corresponding to 37.1%of APY is about 8.5%.

The current ETH pledge yield is about 3%, and the average capital rate of the past three years is about 6-7%.Whether there are enough applications to carry USDE to reduce the pledge rate and bring higher returns.

>

4. Other risks

Including contract risks, liquidation and ADL risk, operating risk, exchange risk, etc.