Source: Coinbase; Compilation: White Water, Bitchain Vision Realm

Different classifications of ETH characters have triggered some of their positions in the investment portfolio.We have clarified some narratives and the potential promotion factors of the assets in the next few months.

summary

-

Although Ethereum has not performed well at the beginning of the year, we believe that its long -term positioning is still strong.We believe that it may rise in a surprising increase in the later period.

-

We also believe that Ethereum has some most powerful continuous demand -driven factors in the field of encryption, and has retained unique advantages on its expansion road map.

-

ETH’s historical trading model indicates that it benefits from the combination of “value storage” and “technical tokens”.

The approval of the US spot Bitcoin ETF has strengthened the value storage narrative of Bitcoin and its position as a macro asset.On the other hand, the problem of the unreasonable problem of ETH’s basic positioning in the field of cryptocurrencies still exists.Competitive Layer 1 like Solana weakened Ethereum as a “preferred” network positioning as a decentralized application (DAPP).The growth of Ethereum Layer 2 and the reduction of ETH burning seem to greatly affect the value accumulation mechanism of assets.

despite this,We still believe that the long -term positioning of Ethereum is still strongAnd it has an important advantage that is significantly different from other smart contract networks.These include the maturity of the Solidity developer ecosystem, the surge in the EVM platform, the practicality of ETH as the DEFI mortgage, and the decentralization and security of its main network.also,We believe that the advancement of autumnization in the short term may have a more positive impact on ETH on other L1.

We found that ETH’s ability to capture value storage and technology tokens was proven through its historical trading model.The correlation between ETH’s transaction and BTC is very high, showing behaviors that meet the BTC value storage model.At the same time, like other cottage coins, it is decoupled with BTC during the long -term appreciation of BTC prices, and trades like technical -oriented cryptocurrencies.We believe that although the performance is not good at the beginning of the year,ETH will continue to play these roles, and there is still room for winning the market in the second half of 2024.

Solve counter -narrative

ETH’s classification methods have a variety of ways, from being classified as “ultrasonic currencies” because of its supply and destruction mechanism, to the “Internet bonds” due to its non -inflation pledge yield.With the expansion and re -pledge of L2, narratives such as “settlement layer assets” or more esoteric “general target work currency” have also surfaced.But in the end, we believe that these characteristics themselves cannot fully capture ETH’s vitality.In fact, we believe that the increasing complexity of ETH uses makes it difficult to define a single indicator of value capture.On the contrary, the integration of these narratives may even appear negative because they may be scattered -decentralized market participants’ attention to the active driving of the tokens.

Spot ETH ETF

The spot ETF provides a channel for regulatory transparency and new capital inflows, which is essential for BTC.TheseETF has changed the industry from structural, and in our opinion, we challenged the previous cycle model, that is, capital shifted from Bitcoin to Ethereum, and then turned to higher Beta’s cottage.There is an obstacle between capital assigned to ETF and the capital assigned to the centralized exchange (CEX), and only the latter can expose more extensive encrypted assets.The potential approval of the spot ETH ETF has eliminated this obstacle of ETH and opened ETH to the same capital pool that is currently only enjoyed by BTC.We believe that this may be ETH’s biggest suspense recently, especially considering the current challenging regulatory environment.

Although the SEC has remained silent to the publisher and approved uncertainty in a timely manner, we believe that the existence of ETH ETF in the United States is still a question of when it exists, not a question of whether it exists.In fact,The main reason for approved the spot BTC ETF is also applicable to the spot ETH ETF.In other words, the correlation between CME futures products and the periodic exchange rate is high enough, so that “it can be reasonably expected that CME’s monitoring will find … [spot market] inappropriate behavior.”The relevant research period in the spot BTC approval notice began in March 2021, that is, CME ETH futures were launched one month after launching.We believe that this assessment period is intentionally selected so that similar reasoning can be applied to the ETH market.In fact, the correlation analysis proposed by Coinbase and Grayscale shows thatThe spot and futures correlation of the ETH market are similar to BTC.

Assume that correlation analysis is established, we believe that the remaining possible opposition is likely to originate from the differences between the nature of Ethereum and Bitcoin.In the past, we have discussed some differences between the size and depth of the ETH and the BTC futures market, which may be a factor in SEC decision -making.butAmong other fundamental differences between ETH and BTC, we believe that the most related to approval issues is the Ethereum’s equity certificate (POS) mechanism.

Since there is no clear supervision and guidance for the treatment of asset pledge,We believe that the spot ETH ETF that supports pledges is unlikely to be approved in the short term.The complexity of the reduction of conditions, the differences between the client of the verification, the possible vague cost structure of the third -party pledged provider, and the cancellation of the risk of pledge liquidity (and exit the queue congestion) are very different from Bitcoin.(It is worth noting that some ETH ETFs in Europe contain pledge function, but in general, European exchange products are different from the products provided by the United States.) In other words, we think this will not affect the state of unpacking ETH.Essence

The challenge to replace L1

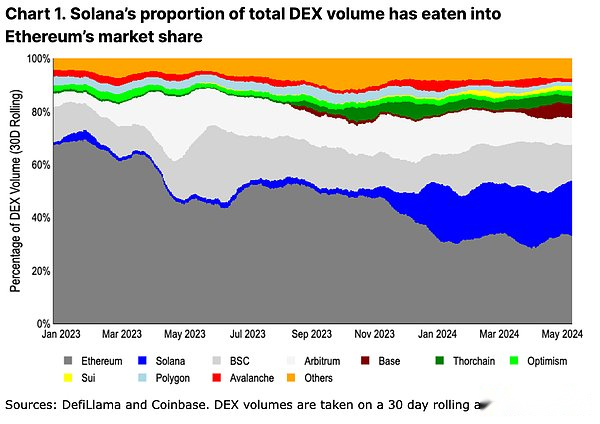

At the level of adoption,The rise of highly scalable integrated chains (especially Solana) seems to be eaten in the market share of Ethereum.High throughput and low -cost transactions have moved the center of the transaction activity away from the main network of Ethereum.It is worth noting that in the past year, Solana’s ecosystem has increased from 2% of the transaction volume of only decentralized exchanges (DEX) to 21%.

We believe that compared with the previous bull market cycle, alternative L1 is now more meaningful to Ethereum.Far away from the Ethereum virtual machine (EVM) and forced to redesign DAPP from scratch has brought a unique user experience (UX) in different ecosystems.In addition, integrated/single expansion methods can achieve more cross -application combination, and prevent the problem of bridging user experience and liquidity fragmentation.

Although these value claims are important, we believe that it is too early to infer the incentive activity index as a confirmation of success.For example, the number of trading users of some Ethereum L2 decreased by more than 80% compared with the peak of air investment mining.At the same time, from Jupiter on November 16, 2023, it was announced that the air investment was between January 31, 2024, and the percentage of Solana’s total DEX increased from 6% to 17%.(Jupiter is the leading DEX polymer on Solana.) Jupiter still has 3 4 rounds of air investment has not yet been completed, so we expect that the increase in the Solana Dex event will last for a period of time.During this period, the hypothetical hypothesis of long -term activities is still speculative.

That is,The proportion of transaction activities on leading Ethereum L2, which is leading Ethereum L2, currently accounts for 17%of the total DEX transaction volume (Ethereum accounted for 33%).This may provide more suitable comparisons for ETH demand driving factors and alternative L1 solutions, because ETH is used as native GAS tokens on all three L2.In these networks, ETH’s MEV and other additional demand drivers have not yet been developed, which also provides space for future demand catalysts.We believe that this is a more equivalent comparison for DEX activities and modular expansion methods.

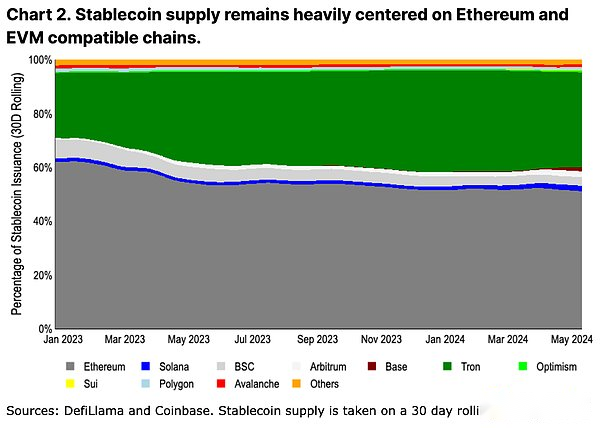

Another more “viscous” measurement indicator is the stable coin supply.Due to bridges and issuance/redemption frictions, the changes in stable currency issuance are slow.(See Figure 2, the color scheme and sorting are the same as FIG. 1, Thorchain is replaced by TRON.) Based on the amount of stable currency issuance, the activity is still mainly elements.We believe that this is because many new chain trust assumptions and reliability are still not enough to support a large amount of capital, especially the capital locked in smart contracts.Large capital holders usually do not care about the high transaction costs (proportion of scale) of Ethereum, and tend to reduce risks by reducing the time of liquidity shutdown and maximum reduction of bridges.

even so,In a high -throughput chain, the supply growth rate of stable currency on Ethereum L2 is still faster than solana.Arbitrum’s stable currency supply in early 2024 surpassed Solana (the current stable currency supply was US $ 3.6 billion and US $ 3.2 billion, respectively), and Base’s stable currency supply has increased from $ 160 million to US $ 2.4 billion from the beginning of the year to the present day to the present.EssenceAlthough the final conclusion of expansion controversy is far from clear, butEarly signs of stable currency growth may actually help Ethereum L2, not replace L1.

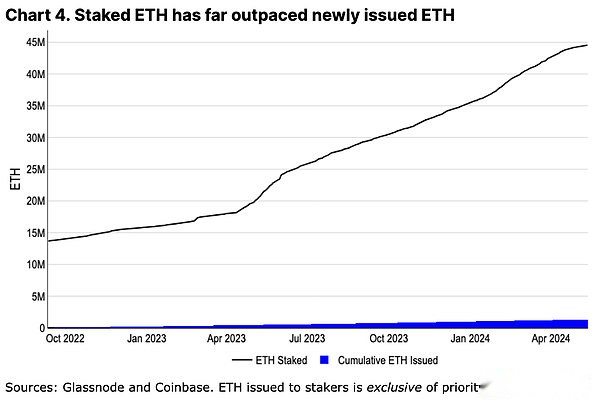

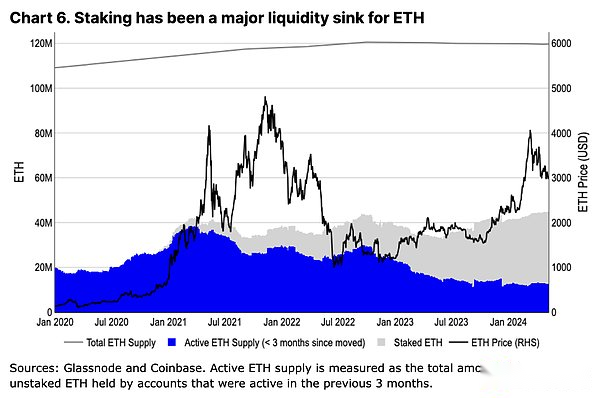

The increasing popularity of L2 has caused people’s concerns, that is, they are actually eating similar to ETH -they reduce the demand for L1 block space (thereby reducing the consumption of transaction costs), and may also support its ecosystem in their ecosystemsNon -ETH GAS tokens (further reduce ETH consumption).In fact, ETH’s annualized inflation rate is at the highest level since the transition to the equity certificate (POS) in 2022.Although inflation is usually considered to be an important part of BTC’s structurally component, we think this is not suitable for ETH.All ETH circulation is owned by the pledgers. Since the merger, the total balance of the pledgers has far exceeded the cumulative circulation of ETH (see Figure 4).This is in sharp contrast to the Economics of Bitcoin’s workload (POW). In Bitcoin, the competitive computing power environment means that miners need to sell most of the new BTCs for operations.Although the Miner’s BTC holding will be tracked by cyclical to prevent its inevitable selling,The minimum operating cost of pledged ETH means that the pledgers can continue to accumulate their position permanently.In fact, pledge has become the growth rate of ETH liquidity -the growth rate of pledge ETH than 20 times higher than the ETH issuance rate (even includes destruction).

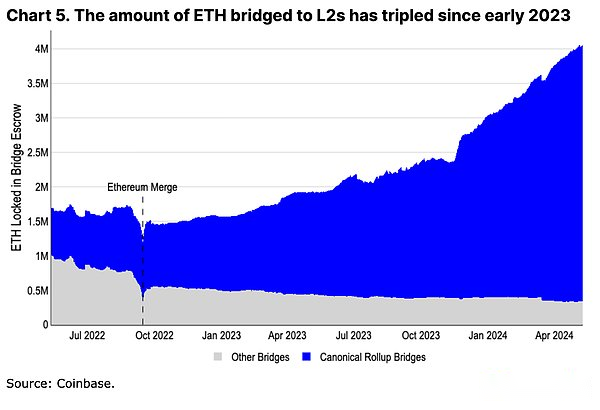

L2 itself is also a meaningful demand driving force for ETH.More than 3.5 million ETH has access to the L2 ecosystem, which is another liquidity slot of ETH.In addition, even if the ETH of the bridge receiving L2 is not directly destroyed, the remaining native token is trying to pay the transaction fee through the new wallet, and its reserve balance constitutes a soft lock in more and more ETH tokens.

In addition, we believe that even if the L2 layer expands, a set of core activities will always be retained on the main network of Ethereum.The governance actions of eigenlayer et al. Or AAVE, MAKER, and Uniswap and other major protocols were still rooted in L1.Users with the highest security concerns (usually the maximum capital) may also keep the funds on L1 until the deployment and testing of completely decentralized sorters and proof of fraud without permission -this process may take several years.Even if L2 is innovative in different directions, ETH will always be part of its vault (for paying L1 “rent”) and local account units.We firmly believe,The growth of L2 is not only beneficial to the Ethereum ecosystem, but also for ETH assets.

Ethereum

In addition to the description of the indicators usually covered, we believe that Ethereum also has other difficulty in quantifying advantages., But still important.These may not be a short -term trading narrative, but represent a set of core long -term advantages that can maintain its current dominant position.

Primitive mortgage and account units

One of the most important cases of ETH is its role in DEFI.ETH can play a leverage in Ethereum and its L2 ecosystem and minimize the risk of transaction opponents.It acts as a mortgage form for monetary markets such as Maker and AAVE, and is also the basic trading unit of the DEX pair on many chains.The expansion of the Ethereum and its L2 DEFI leads to additional liquidity absorption of ETH.

Although BTC is still a wider range of dominant value storage assets, the use of packaging BTC has introduced bridges and trust assumptions on Ethereum.We believe that WBTC will not replace ETH’s use in the DEFI based on Ethereum -WBTC supply has remained stable for more than a year, which is more than 40% lower than the previous high.Instead, ETH can benefit from the practicality of its L2 ecosystem diversity.

Continuous innovation in decentralization

One of the components that Ethereum community is often ignored is that even if it is decentralized, it can continue to innovate.Ethereum has been criticized for its long release time and delayed development. However, few people recognize the goals and purposes of weighing relevant stakeholders to achieve the complexity of technological progress.Developers with more than five executions and four consensus clients need to coordinate design, testing and deployment changes, and will not cause any shutdown in the main network.

Since Bitcoin’s last Taproot upgrade in November 2021, Ethereum launched a dynamic transaction destruction (August 2021), transitioned to POS (September 2022), and enabled pledge (March 2023), and and and and and also, and also enabled.Create BLOB storage (March 2024) for L2 expansion -these upgrades include many other Ethereum improvement proposals (EIP).Although many alternative L1 seems to be able to develop faster, their single customers make them more vulnerable and concentrated.The decentralized road inevitably leads to a certain degree of rigidity. It is unclear whether other ecosystems have the ability to create a similar development process, if they start this process.

Quickly perform L2 innovation

This is not to say that Ethereum’s innovation is slower than other ecosystems.On the contrary, we believe that innovation around the execution environment and development staff tools actually exceed competitors.Ethereum has benefited from the rapid centralization of L2, and all these are paid to L1 with ETH.Different platforms or privacy or other functions such as Web Assembly, Move, or Solana virtual machines (such as Web Assembly, MOVE, or Solana virtual machines) mean other functions, which meansL1 slower development schedule will not hinder ETH obtaining more comprehensive use cases.

At the same time, the Ethereum community defines different trust assumptions and definition efforts to define different trust assumptions and definitions around the side chain, verification, and rollup.Similar efforts (such as L2Beat) have not been obvious in the Bitcoin L2 ecosystem. For example, its L2 trust assumptions are very different, and they are usually not well communicated or understood by a wider range of communities.

EVM surge

Innovation around the new execution environment does not mean that Solidity and EVM will be outdated in the near future.Instead, EVM has spread widely to other chains.For example, many Bitcoin L2 is using Ethereum L2 research.Most of the disadvantages of Solidity (for example, it is easy to contain reload vulnerabilities) now has a static tool checker to prevent basic vulnerabilities.In addition, the language of this language has also created a comprehensive audit department, a large number of open source code examples, and the best detailed guide for the best practice.All these are important for the establishment of a huge developer talent pool.

Although the use of EVM does not directly lead to ETH demand, the change of EVM is rooted in the development process of Ethereum.These changes are subsequently adopted by other chains to maintain EVM compatibility.We believe,EVM’s core innovation is likely to still be rooted in Ethereum, or it is quickly adopted by L2, which will focus on the attention of developers, thereby focusing on the new protocol in the Ethereum ecosystem.

Vigatization and Lindy effect

We believe that the promotion of tokens and the increase in global regulatory transparency in this field may also be most conducive to Ethereum (in public blockchain).Financial products usually focus on technological risk relief rather than optimization and functions, but the advantage of Ethereum is the longest operating smart contract platform.We believe,Moderate transaction costs (USD instead of US dollars) and longer confirmation time (seconds instead of milliseconds) are secondary issues of many large tokenized projects.

In addition, for traditional companies that want to expand the business on the chain,Employing sufficient number of development talents has become a key factor.Here, Solidity has become an obvious choice because it constitutes the largest subset of smart contract developers, which echoes the early view of EVM diffusion.The BUIDL fund and JPM proposed on Ethereum and JPM proposed on ERC-20 are compatible with ERC-20 digital assets alternative to the ODA-FACT tokens.

Structural supply mechanism

The changes in active ETH supply are very different from the changes in BTC.Although prices have risen since the fourth quarter of 2023, ETH’s 3 -month circulation supply has not increased significantly.In contrast, we observed that the active BTC supply in the same time increased by nearly 75%.Different from the increase in contributing to the long -term ETH holders (as Ethereum is still seen under POW in the 2021/22 cycle), more and more ETH supply is pledged.This once again confirms our point, that is, pledge is the key liquidity exchange of ETH, and minimizes the structural seller of the asset.

Continuous development trading system

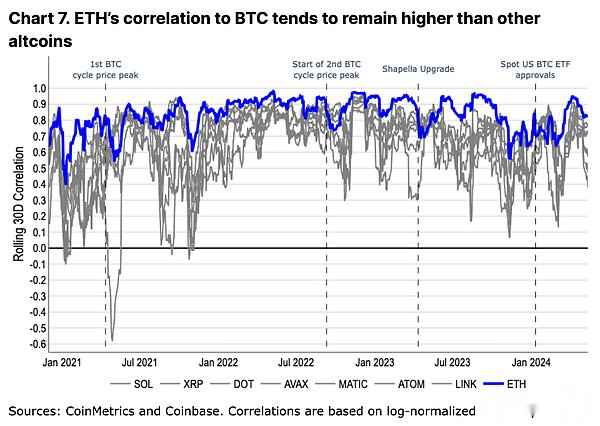

Historically,Compared with any other cottage coins, ETH’s transactions are more consistent with the trend of BTC.At the same time, during the bull market peak or special ecosystem incident, it is also decoupled with BTC -similar models are also observed in other alcohol currencies, although the degree is small (see Figure 7).We believe that this trading behavior reflects the relative valuation of the market as a value storage token and a technical practical tokens in the market.

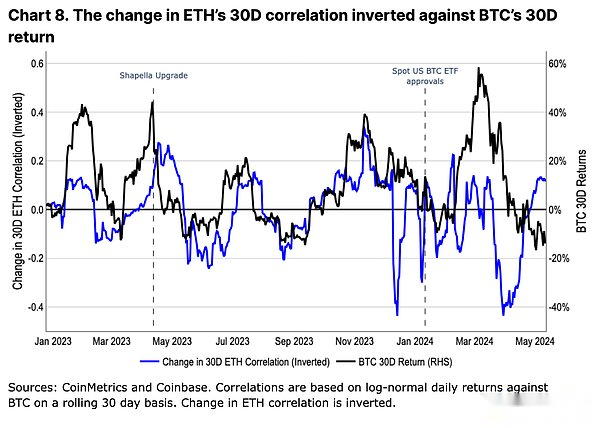

Throughout 2023, the changes in correlation between ETH and BTC have a inverse relationship with the changes in the price of BTC(See Figure 8).That is,With the appreciation of the value of BTC, ETH has a lower correlation, and vice versa.In fact, changes in BTC prices seem to be the advance indicators of ETH correlation changes.We believe that this is a indicator of the prosperity of the Congzhan currency market in BTC prices, which in turn has improved their speculative performance (that is, the transaction methods of the cottage in the bull market are different, but the performance of the BTC in the bear market corresponds to the performance.To.

However, this trend has stopped after the spot US BTC ETF was approved.We believe that this highlights the structural impact of ETF -based capital inflows, and the new capital foundation can only be used by BTC.Compared to many cryptocurrency holders or retail traders, the new markets of registered investment consultants (RIA), wealth management institutions and brokerage companies may have a very different view of BTC in the investment portfolio.Although Bitcoin is the smallest asset in the pure cryptocurrency investment portfolio, in more traditional fixed income and stock investment portfolios, it is usually regarded as small diversified assets.We believe that this transformation of BTC effect has an impact on its transaction model relative to ETH, and in the spot trading of ETH ETF in the United States, ETH may have similar changes (and re -adjustment of transaction models).

Summarize

We believe that ETH may still have an unexpected increase in the next few months.ETH does not seem to have problems with excess supply, such as token unlocking or miners’ selling pressure.On the contrary, it turns out that the growth of pledge and L2 is meaningful, and the absorption of ETH liquidity has continued to increase.We believe,Because EVM and its L2 innovation are widely used, ETH’s status as a DEFI center is unlikely to be replaced.

In other words, the importance of potential US Ethereum ETF spot cannot be underestimated.We believe that the market may underestimate the timing and possibility of potential approval, which leaves an unexpected space for the rise.During this period, we believe that ETH’s structural demand driving factors and technological innovation in their ecosystems will enable it to continue to span multiple narratives.