This article has been slightly deleted and modified based on the original text. Please refer to the original text:https://www.coinbase.com/en-gb/institutional/research-insights/research/monthly-outlook/monthly-outlook-may-2024

The U.S. approval of Bitcoin spot ETF strengthens BTC’s image as a storage value asset and consolidates its macro asset status.In contrast, Ethereum’s basic positioning in the field of crypto is still unclear.Competitive public chains like Solana have influenced Ethereum’s position as the preferred deployment platform for DApps.The growth of Ethereum Layer2 and the reduction in ETH destruction also seem to affect the way its value accumulates.

However, we believe that the long-term prospects of Ethereum are still optimistic, and it has unique advantages in smart contract platforms, including Solidity’s strong developer ecosystem, the widespread use of EVM platforms, the importance of ETH as a DeFi collateral, and the mainnet’s departureCentralization and security.Moreover, with the accelerated development of the trend of converting real-world assets into digital assets on blockchain, ETH may gain a more positive and positive driving role in the short term compared to other L1s.

Historical transaction data shows that ETH reflects both the characteristics of storage value and technological innovation.It is highly linked with BTC and is in line with the characteristics of storage value, but it can perform independently during the long-term rise of BTC, and follows technology-oriented market laws like other crypto assets.ETH is expected to continue to integrate these two characteristics and is likely to reverse its current poor performance in the second half of 2024 to achieve beyond expectations.

ETH’s narrative

ETH has a diverse role, both known as Ultrasound money that controls supply through production cuts and as an internet bond that provides non-inflation pledge proceeds.With the rise of Layer2 expansion and re-staking technology, new concepts such as “settlement layer assets” and “general labor certification assets” have also emerged.

Translator’s note: Under the PoS mechanism, users can participate in network maintenance and receive rewards by pledging ETH, which is similar to obtaining interest by purchasing bonds, but is more decentralized.Since pledge rewards come from online transaction fees and newly issued ETH, and the total control strategy limits excessive issuance, this pledge return model of ETH is regarded as a more anti-inflation Internet bond compared to traditional inflation.

But at the end of the day, we don’t think that none of these separate statements fully demonstrate the vitality of ETH.In fact, the increasing use of ETH makes the way to evaluate its value more complex, and a single measure is difficult to define.Moreover, the interweaving of these multiple concepts can sometimes lead to confusion, and the contradictions between them can distract market participants and obscure the real driving force that drives the rise in ETH value.

Spot ETF

Spot ETFs are extremely critical for Bitcoin, which not only clarifies the regulatory framework, but also attracts new capital injections.This type of ETF fundamentally reshapes the industry landscape, and we believe it subverts the cyclical model of previous capital shifting from Bitcoin to Ethereum and then investing in higher-risk alternative assets.

There are barriers between funds investing in ETFs and funds on centralized exchanges, which can delve into a wider range of crypto assets.Once the spot Ethereum ETF is approved, this barrier will be removed and Ethereum will also be able to access the capital source that is now open to Bitcoin only.

In fact, the logic of approving Bitcoin spot ETFs also applies to Ethereum spot ETFs, because the futures prices on the Chicago Commodity Exchange (CME) are closely related to spot prices and can effectively monitor and prevent market misconduct.

The relevance research period for Bitcoin Spot ETF approval reference starts exactly one month after the launch of Ethereum Futures on the Chicago Commodity Exchange (CME), that is, in March 2021. We speculate that this is intentional so that the same logic can be applied in the future.in the Ethereum market.Previous data analyses by Coinbase and Grayscale also show that Ethereum’s spot and futures price correlation is similar to BTC.

Other Layer1 challenges

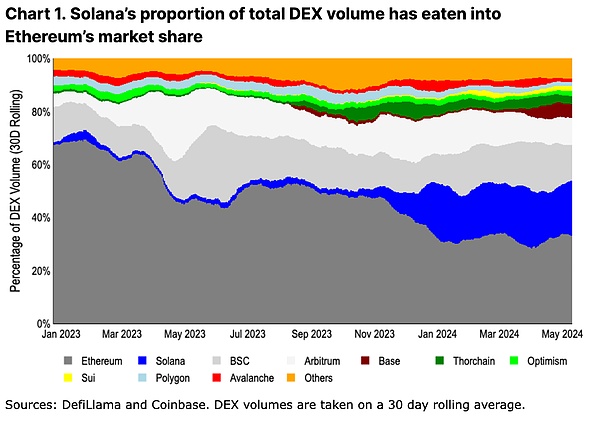

Some high-performance integration chains, especially Solana, are gradually eroding Ethereum’s market share.These chains provide high-speed and low-cost transactions, allowing transaction activity to increasingly move from the Ethereum main network.For example, last year alone, the share of DEX transactions in the Solana ecosystem soared from 2% to 21%.

We observe that the differences between these L1s and Ethereum are now more obvious than the previous bull cycle.They no longer rely on Ethereum virtual machines, and DApps have also been completely redesigned from scratch, creating their own unique user experiences.In addition, the integrated/integrated strategy adopted by these chains enhances the collaboration capabilities between different applications, solving problems such as poor user experience and diversified capital liquidity during the bridging process.

Although these unique value propositions are critical, we believe it is too early to judge success based on motivation-driven activity indicators.For example, some Ethereum Layer2 user transaction volume decreased by more than 80% after the peak airdrop period.Meanwhile, Solana’s share of DEX volume grew from 6% at the time of the release of the Jupiter airdrop announcement on November 16, 2023 to 17% on the first pickup date on January 31, 2024 (Jupiter is the main one on SolanaDEX aggregator).

With Jupiter still three more airdrops unfinished, Solana’s DEX activity is expected to remain high.However, during this period, the assumption of the retention ratio of long-term activity still belongs to the speculation stage.

On the other hand, the leading Ethereum Layer2 (Arbitrum, Optimism and Base) currently account for 17% of the total DEX transaction volume, plus 33% of Ethereum itself.This is especially important when comparing ETH demand growth with other Layer1 solutions, because among these three Layer2s, ETH is the base fuel asset.In addition, additional demand drivers for ETH in these networks, such as MEV, have not been fully developed, leaving room for future demand growth.Therefore, from the perspective of DEX activity, this provides a more proportional comparison between the integrated and modular expansion methods.

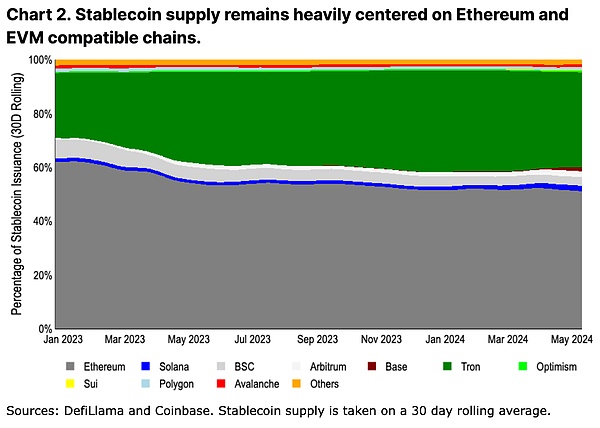

In addition, another more lasting metric for measuring the adoption of the network by users is the supply of stablecoins.The circulation and issuance/redemption of stablecoins is restricted by bridging, so their movements are slower.

Measured by the volume of stablecoin issuance, the activity is still concentrated on Ethereum.We believe that many emerging chains are not enough to support large-scale capital in terms of trust and reliability, especially capital locked by smart contracts.Large capital holders tend to be less sensitive to Ethereum’s higher transaction fees (relative to transaction size), and they tend to reduce risk by reducing liquidity interruption times and minimizing bridge trust.

In fact, the stablecoin supply has grown faster than Solana on Ethereum Layer2.Since the beginning of 2024, Arbitrum has surpassed Solana (currently $3.6 billion and $3.2 billion in stablecoins, respectively), and Base has grown its stablecoin supply from $160 million to $2.4 billion so far this year.

Although the final conclusion is far from clear in the expansion debate, early signs of stablecoin growth may actually be more favorable to Ethereum Layer2 than other Layer1 chains.

The booming development of Layer2 technology has sparked discussion: Layer2 reduces Layer1 block space requirements (and thus reduces ETH destruction as transaction fees) and may also support non-ETH gas fees in its ecosystem (more reducing ETH destruction).

However, in-depth analysis shows that the impact of this situation on ETH is not negative.

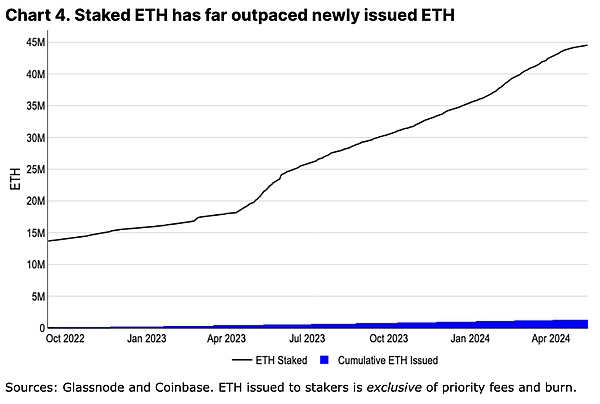

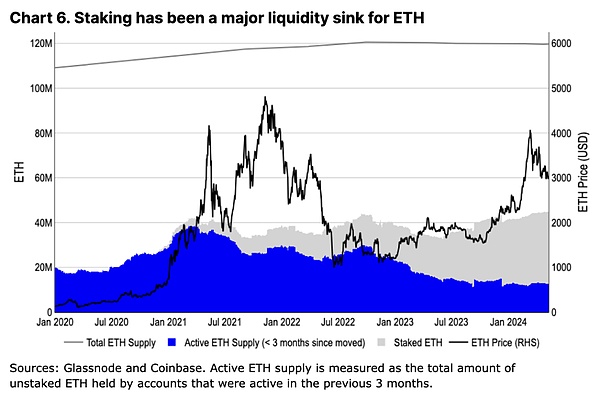

ETH has reached its highest annualized inflation rate since Ethereum switched to PoS in 2022.Although inflation is often considered a structurally important component of BTC supply, we don’t think this applies to ETH.In essence, all newly issued ETH is directly allocated to the stakers, and the ETH holdings of these stakers are growing at an astonishing rate, far exceeding the issuance rate.Unlike miners who need to frequently sell BTC to maintain operations in the Bitcoin mining economy, ETH has a low pledge cost, allowing pledgees to accumulate ETH for a long time without selling it.

At the same time, pledge has become a sucking stone for ETH liquidity, and the growth rate of pledged ETH is more than 20 times that of ETH issuance.

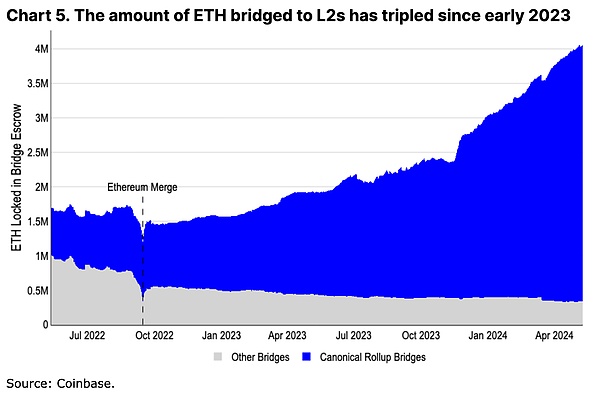

The rise of Layer2 further aggravated the liquidity tightening of ETH. More than 3.5 million ETHs were moved to Layer2, which not only directly transferred ETH, but also prompted users to prepare ETH for Layer2 transactions as reserves, which is equivalent to locking ETH in disguise.

Although the Layer2 ecosystem is growing, core financial services and governance activities such as EigenLayer’s re-staking, Aave, Maker, Uniswap, etc. are still carried out based on Layer1, ensuring the fundamental demand for ETH.Especially those large-scale fund holders who value security the most tend to stay in Layer1 until Layer2 is fully decentralized and license-free fraud proof, which also supports the market demand for ETH.

In summary, Layer2’s development not only did not weaken ETH, but instead promoted the value-added ETH in a complex way.It is not only a driving force for the growth of ETH demand, but also strengthens the core value of ETH by increasing the application scenarios of ETH and its role as the basic unit of Layer1 fee and Layer2 pricing.

Advantages of Ethereum

In addition to common data-driven narratives, we think Ethereum has some other difficult but still very important advantages.These may not be short-term trading narratives, but represent a core set of advantages that can maintain their dominance over the long term.

High-quality mortgage assets and pricing benchmarks

ETH plays a central role in the DeFi field, it is widely used in L1 and L2, and assumes the role of low-risk collateral in lending platforms such as Maker and Aave, and is also the basic trading pair in many DEXs.With the expansion of DeFi applications on L1 and L2, the demand and liquidity of ETH also increase.

Although BTC is recognized as the primary stored value asset, WBTC used in encapsulated form on Ethereum involves additional trust bridging issues.At present, it seems unlikely that WBTC will replace ETH’s position in Ethereum DeFi – the supply of WBTC has been stable for a long time, exceeding 40% lower than its previous peak.On the contrary, ETH’s value and role are constantly highlighting due to its wide applicability in diverse secondary ecosystems.

Continuous innovation and decentralization of the Ethereum community

What is unique about Ethereum is that it continues to promote decentralization while still maintaining strong innovation capabilities.The outside world sometimes criticizes Ethereum’s upgrade plan for delays, but does not fully realize the difficulty of coordinating developers from different backgrounds to achieve technological progress.

It should be noted that in order to ensure the network is running uninterrupted, teams involving more than five execution clients and four consensus clients must work closely together to promote updates.

For example, since Bitcoin’s major upgrade in November 2021 (Taproot) to date, Ethereum has implemented a series of changes: including the introduction of dynamic transaction fee destruction (August 2021), the successful shift to PoS (September 2022),Opening the mortgage withdrawal function (March 2023), and adding blob storage for L2 (March 2024), are accompanied by numerous other technical improvement proposals (EIPs).In contrast, some other blockchain platforms that are rapidly developing, although iterating quickly, their systems appear more concentrated and fragile due to their dependence on a single client.

Although decentralization will lead to more cumbersome decision-making process and even to some extent rigid, it is also a necessary price to ensure safety and fairness.For other ecological systems that may embark on a similar path to decentralization in the future, whether it can establish an development model that is both efficient and inclusive of opinions from all parties is still a challenge to solve.

The rapid advancement of L2 innovation

This is not to say that innovation on Ethereum is slower than other ecosystems.Instead, we believe that innovations around execution environments and developer tools actually outweigh the competitors.Ethereum benefits from the rapid centralized development of L2, all of which pays settlement fees to L1 in the form of ETH.The ability to create diverse platforms with different execution environments (such as WebAssembly, Move, or Solana virtual machines) or other features, such as privacy protection or enhanced staking rewards, means that L1’s slower development schedule does not hinder ETH from being more comprehensive in technologyUse cases are adopted.

At the same time, when defining concepts such as side chains, Validium, and Rollup, the Ethereum community has clarified its work on various trust premises and definitions, which has enhanced the transparency of the industry.By contrast, for example, within Bitcoin’s L2 ecosystem, similar levels of efforts (such as the L2 Beat project) are not significant yet, and the trust model on which L2 relies on is diverse and often not clearly recognized or fully communicated by the outside world.

The widespread dissemination of EVM

Innovations around the new execution environment do not mean that the Solidity language and EVM will be outdated in the near term.Instead, EVM has been widely spread to other blockchains.For example, the research results of Ethereum L2 are being adopted by many Bitcoin L2.Some of Solidity’s shortcomings (such as the ease of inclusion of reentrant vulnerabilities) are now available with static tool checkers to prevent basic attacks.Furthermore, the popularity of the language has spawned a mature auditing industry, a wealth of open source code examples and detailed best practice guides that are essential to fostering a large developer talent pool.

Although the direct use of EVM does not necessarily increase the demand for ETH, the improvements to EVM originate from the development of Ethereum, and other chains will also follow the updates in order to maintain compatibility with EVM.We believe that fundamental innovations in EVM will continue to be centered on Ethereum or will soon be absorbed by some L2, thereby consolidating the position of the Ethereum ecosystem in the hearts of developers.

Tokenization trend and cumulative advantages

We believe that promoting tokenization projects and increasingly clear global regulatory policies will benefit Ethereum (in public chains) in the first place.Financial products usually focus more on technical security than extreme optimization, and Ethereum, as the most mature smart contract platform, has natural advantages.For many large tokenization projects, relatively high transaction costs (a few dollars instead of cents) and longer confirmation times (a few seconds instead of milliseconds) are not the main obstacles.

For traditional enterprises who want to enter the blockchain field, having a sufficient number of skilled developers becomes crucial.At this time, Solidity, as the most widely used smart contract language, became the first choice, which further strengthened the popularization advantages of EVM.Blackstone’s Ethereum BUIDL Fund and JPMorgan’s proposed ODA-FACT standard that is compatible with ERC-20 are early signals that attach importance to this developer community.

Ethereum supply dynamics are very different from Bitcoin

The circulation and supply changes of ETH are fundamentally different from those of BTC.Even though prices have risen sharply since Q4 2023, ETH’s three-month liquid supply has not expanded significantly, while the active supply of BTC increased by about 75% during the same period.Unlike previous Ethereum mining period (2021/2022) where long-term holders increased market supply, more and more ETH is now being used for staking, which shows that staking is an important way for ETH to reduce selling pressure.

Evolution of trading patterns

Historical data shows that ETH has a closer relationship with BTC than any other crypto asset.However, during peak bull markets or specific Ethereum ecosystem events, ETH will be temporarily decoupled from BTC, a model that is also reflected in other crypto assets, with a smaller amplitude.This reflects that the market conducts relative evaluation based on the stored value attributes of ETH and the practical value of technological innovation.

In 2023, there was a special phenomenon in the correlation between ETH and BTC: when the price of BTC rises, the trend correlation between ETH and BTC weakens; when the price of BTC falls, the correlation between the two increases.

This implies that the fluctuations in BTC prices are like a leading signal, heralding the subsequent changes in market correlations in ETH.The market’s enthusiasm for the high BTC price seems to drive independent markets for other crypto assets (including ETH), especially during the market’s rise, where asset types perform diversely; and when the market falls, they tend to be consistent with BTC’s performance.

But this model has changed after the United States approved Bitcoin spot ETF.The newly approved ETFs attract different groups of investors such as investment advisors, wealth management agencies, etc., who handle BTC differently than traditional investors in the crypto space.

In pure crypto asset portfolios, BTC is valued because of its small volatility, but in traditional investment portfolios, it is more of a diversified allocation for a small part.This change in capital flows and market structure caused by changes in BTC’s role has affected the trading interaction between BTC and ETH.In the future, if Ethereum spot ETFs are listed, it is expected that ETH will also face similar market structure changes, and its trading model may be adjusted again.

Summarize

We believe ETH still has potential upside surprise space in the coming months.ETH does not appear to have a major supply-side oversupply source such as asset unlocking or miner selling pressure.On the contrary, staking and L2 growth have proven to be meaningful and sustained absorption points for ETH liquidity.Given the widespread use of EVM and its L2 innovation, ETH’s position as a DeFi center is unlikely to be replaced.At the same time, the importance of US spot ETH ETFs cannot be underestimated.

We believe that the structural demand drivers for ETH, along with technological innovations within its ecosystem, will enable ETH to span multiple narratives and continue to maintain its unique position.