Author: @Elias201179 Instructor | @Cryptoscott_eth

>

-

AAVE is a multi -chain lending agreement. Its core business is to achieve P2C (point -to -point) borrowing through dynamic interest rate models and liquidity capital pools.At present, its total lock value (tvl) ranks third in the DEFI project,Especially in the lending category, occupy a leader.AAVE’s parent company Avara is gradually expanding its business into new areas, including cross -chain lending, stabilizing coins, open social agreements, and institutional lending platforms.

-

The total supply of AAVE tokens is16 million,in13 million piecesIt is assigned to token holders, the remaining ones3 millionInjected into the reserve of the AAVE ecosystem.The total AAVE tokens circulating in the market currently14.8 million piecesEssence

-

With the continuous expansion and maturity of the AAVE business, in the context of the market recovery in 2024,AAVE’s TVL and prices have improved.Avara announced the upgrade plan of the AAVE V4 version in May,The focus is on further improving the liquidity and asset utilization of AAVE.

-

The AAVE V3 version has basically replaced the V2 version. The gradual stability of the business model and the user group also makes AAVE ahead of other borrowing agreements in TVL, transaction volume, and support chain.

-

Avara encountered some challenges in expanding business.At present, its main income still depends on the traditional lending business.Stable currency GHO has recently beenThe anchor was restored.The TVL of AAVE ARC, the institutional lending platform, has been at a low level for a long time after the experience plummeted.

-

For the future development of AAVE, it is recommended to further optimize its cross -chain lending plan, strengthen its stablecoin business, and deeply couple with the AAVE platform. Integrate AAVE’s DEFI capabilities in emerging businesses such as social platforms.Integrate into oneComprehensive ecosystem.

>

In the first quarter of 2024, the DEFI market showed significant growth and vitality, of which the charges and income reached the annual high.The DEFI market charged more than 1.6 billion US dollars in the last quarter, with a total revenue of more than 467 million US dollars. Especially in March, a single monthly revenue reached US $ 230 million, a new high of the year.

As one of the core functions of the cryptocurrency ecosystem, lending uses intelligent contracts to achieve the functions of matching, asset locks, interest calculations, and repayment execution.According to DEFILLAMA data, as of mid -May 2024, the total value of TVL in the field of lending reached $ 29.586B, accounting for 36%of TVL in the entire DEFI field.

In this context, AAVE, as an important participant in the DEFI borrowing market, is particularly worthy of attention.AAVE’s total borrowing in the first quarter of 2024 reached 6.1 billion US dollars, an increase of 79% month -on -month. This growth rate far exceeded the average market.

In addition, AAVE’s loan revenue in this quarter also increased by 40%to $ 34.9 million, and continued to maintain a leading position in the DEFI lending market.Despite the fierce competition from competitors, AAVE still dominates the total locking value (TVL) and income.

Studying AAVE’s performance in the DEFI market is also of great significance to understand the development trend and future potential of the entire DEFI market.AAVE’s successful cases and operating models also have a reference and revelation effect on other DEFI projects.

>

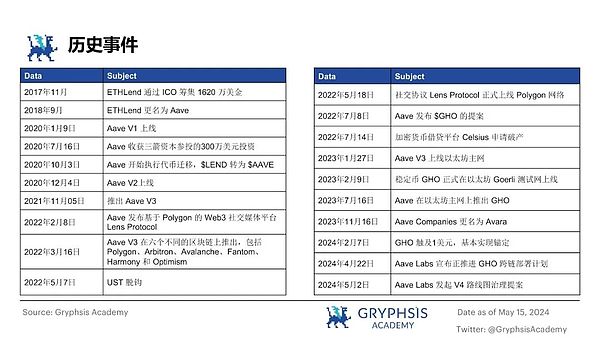

In May 2017, Stani Kulechov founded the ETHLEND project.At first, ETHLEND encountered serious liquidity challenges during the operation.By the end of 2018, ETHLEND conducted a strategic transformation, transformed from the P2P (point -to -point) mode to the P2C (point -to -contract) mode, introduced the liquidity fund pool model, and officially renamed AAVE.This transition marks the official launch of AAVE in 2020.

In November 2023, Aave Companies announced that the brand was renamed Avara.AVARA has gradually launched new businesses including stabilized currency GHO, social network protocol Lens, and AAVE ARC, an institutional lending platform, and began to conduct strategic layout in many areas such as wallets and games.

The current AAVE V3 version has been put into use stably, and its services have expanded to 12 different blockchains.At the same time, AAVE Labs further tried to upgrade the loan platform, and announced the V4 version upgrade proposal in May 2024.

According to the data provided by Defillama, as of May 15, 2024, AAVE ranked third in the field of Defi (decentralized finance), reaching US $ 1.069.4 billion.

>

>

AAVE’s parent company Avara is headquartered in London, England. At first, it was composed of an innovative team of 18 people. At present, the leading Britain shows a total of 96 employees.

-

The founder and CEO (CEO): Stani Kulechov obtains a master’s degree in law in the University of Helsinki. The theme of its master’s dissertation uses the efficiency of business agreements with technology. It is also a web 3 practitioner with continuous entrepreneurial experience.

-

Chief Operating Officer (COO): Jordan Lazaro Gustave is more than ten years old and has a master’s degree in the Department of Risk Management of University Paris X NANTERRE.

-

Chief Financial Officer (CFO): Peter Kerr graduated from Massey University and University of Oxford. He has served as HSBC, Deutsche Bank, Sonali Bank, etc., and joined Avara as CFO in 2021.

-

Institutional person in charge: Ajit Tripathi graduated from IMD Business School and Indian Institute of Technology, and has served in Binance, Consensys, and PWC.

>

-

In 2017, ETHLEND raised $ 16.2 million through ICO. During this period, Aave Companies sold 1 billion units of Lend tokens.

-

In 2018, the project brand was upgraded to AAVE.

-

In July 2020, AAVE received a $ 3 million round A investment led by Sanjian Capital.

-

In October 2020, AAVE harvested $ 25 million in Series B investment and launched the governance token $ AAVE.

-

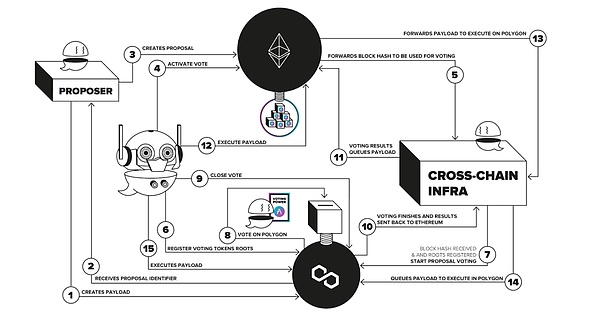

In May 2021, the AAVE agreement was deployed on Polygon and will be awarded the MATIC lending mining award worth 200 million US dollars in one year.

>

>

Figure 1: AAVE history event

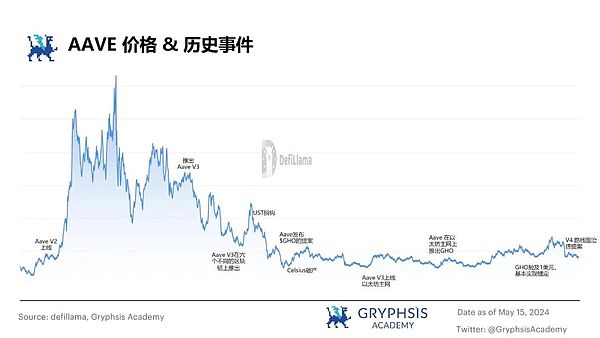

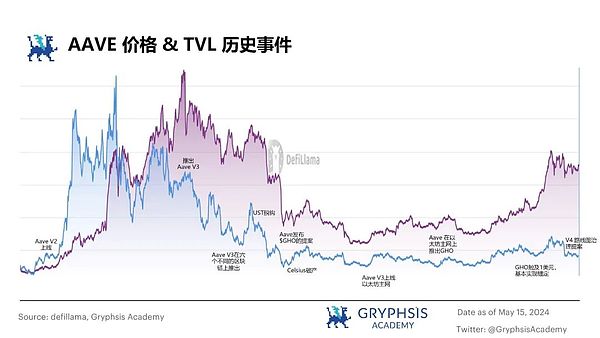

Major events and announcements often have a significant impact on the price and total lock value (TVL) of the decentralized lending agreement.For example, after the AAVE V2 was launched at the end of 2020, the price of AAVE and TVL have risen significantly.This trend continued during the Defi Summer in 2021,At that time, the mortgage and borrowing scale of the lending agreement continued to expand, thereby maintaining the high price level of AAVE.By March 2022, the launch of AAVE V3 once again promoted the significant growth of AAVE prices and TVL.However, the subsequent UST decourse and the following bear markets led to AAVE’s TVL overall shrinkage and price decline.

Although on November 5, 2023, AAVE received a short -term decline in AAVE prices and TVL after receiving a report on AAVE protocol function issues and temporarily suspending AAVE V2 market transactions.However, as the overall market is better and GHO has gradually resumed anchor, the price of AAVE and TVL have recently emerged as a significant upward trend.

>

Figure 2: AAVE price & amp; historical event map

>

Figure 3: aave tvl & amp; historical event map

>

>

>

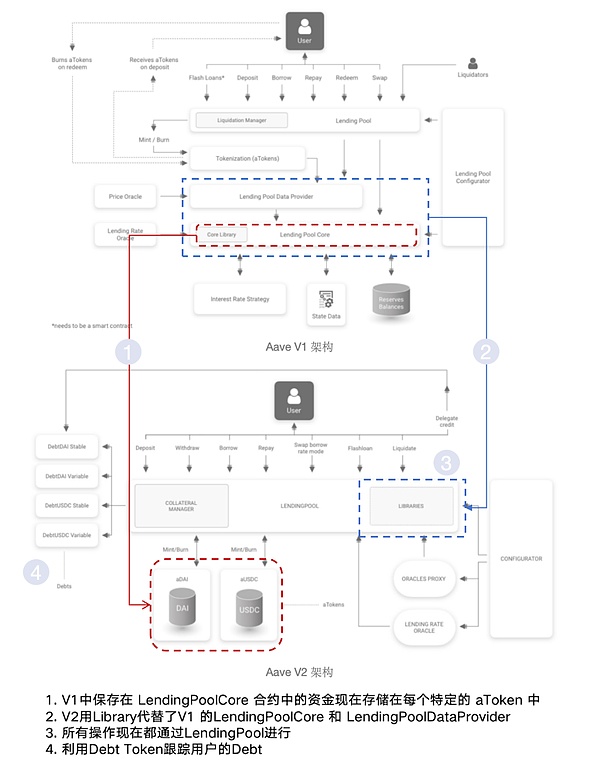

Since the first appearance of AAVE in January 2020, it has established its important position in the field of decentralized finance (ATOKEN model, innovative interest rate mechanism, and Lightning loan functions.As AAVE evolved from V1 to V3, its loan business model showed a continuous and stable development trend.

In December 2020, AAVE released V2 version, which simplified and optimized its architecture and introduced debt tokensization and Lightning Loan V2, which significantly improved the user experience.According to the official white paper, the optimization of the architecture of V2 is expected to reduce the cost of about 15% to 20%.In January 2023, AAVE launched the V3 version, which further enhanced the efficiency of funds on the basis of V2, and the overall structure was not changed much.The V3 version introduces three innovative functions: E-Mode, ISOLATION MODE, and Portal.

In May 2024, AAVE proposed the V4 version proposal, and it is planned to adopt a new structure in the new version of the design and introduce itUniformly liquidity layer, blurring control interest rates, GHO native integration, AAVE Network and other designs, etc.The specific details of the relevant mechanism of the V4 version will be explained in detail in the subsequent section 4.1.6.

>

Figure 4: AAVE protocol V2 and V3 architecture changes

>

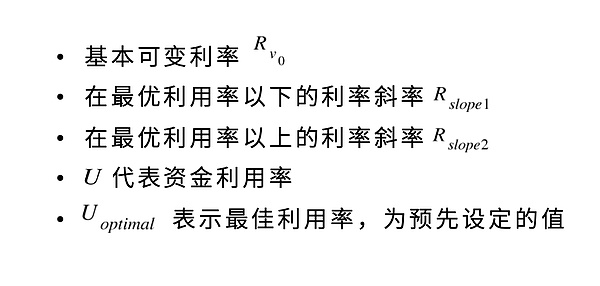

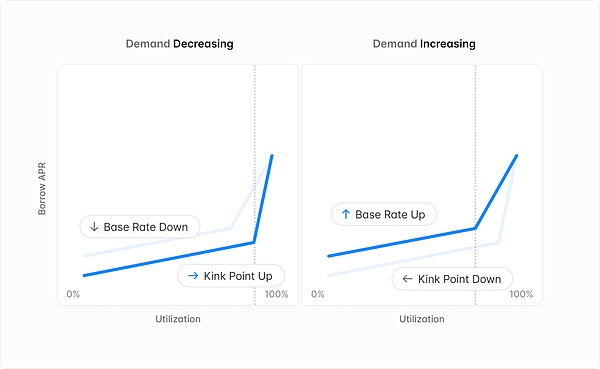

Borrowing interest rate

AAVE has a specific interest rate strategy contract for each reserve.Specifically, the following content is defined in the basic strategic contract:

>

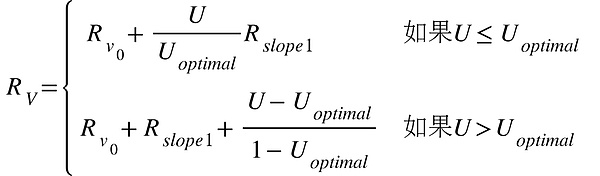

The formula for variable interest rate calculation is:

>

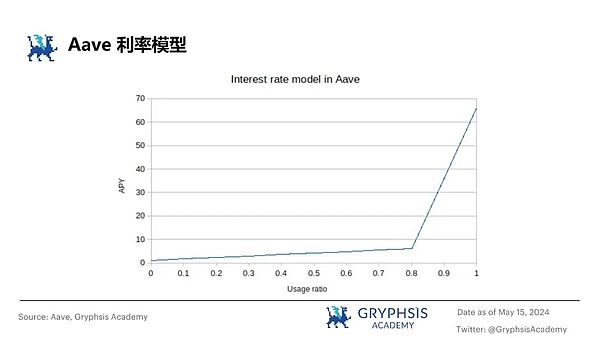

By analyzing the interest rate model, we can find that when the current utilization rate is lower than the optimal utilization rate of the given market, the borrowing interest rate has risen slowly.However, when the current utilization rate exceeds the optimal utilization rate, the borrowing interest rate will increase sharply with the improvement rate.That is, when the liquidity in the trading pool is high, low interest rates encourage loans; when the liquidity is low, high interest rates maintain liquidity.

>

Figure 5: AAVE deposit interest rate change map

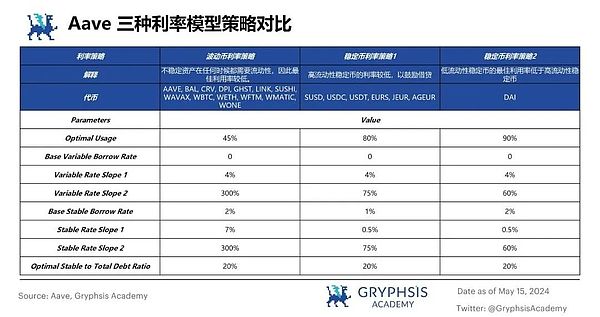

Each asset has a predetermined optimal utilization rate.Based on the above interest rate model, the AAVE V3 divides three interest rate model strategies according to the risk status of different assets::

>

Figure 6: AAVE V3 Three interest rate model strategies comparison

>

In the interactive process of AAVE, the lending process is as follows:

-

The deposit party can get the corresponding Atoken by depositing the tokens into AAVE’s asset pool.These Atoken, as a deposit certificate, not only proves the deposit behavior, but also freely trade and transfer in the secondary market.

-

For borrowers, they can borrow cryptocurrencies by excess mortgage or lightning loan.When the borrower prepares the debt, in addition to the need to return the principal, it also needs to pay interest calculated based on the asset utilization and market supply and demand status.Once the debt is settled, the borrower can not only redeem its mortgaged assets, but also the ATOKEN linked to its mortgage assets will also be destroyed accordingly.

The clearing mechanism of AAVE is as follows:

When the market value of mortgage asset declines or the value of borrowing assets rises, and the mortgage value of the borrower’s mortgage falls below the established clearing threshold, the AAVE liquidation mechanism will be triggered.Different token will have different loan value ratio (LTV) and liquidation thresholds according to their risk characteristics.When liquidation occurs, in addition to paying principal and interest, the borrower also needs to pay a certain percentage of liquidation bonus to a third -party payment of the liquidation.

Related parameters:

-

Loan value ratio (LTV):Determine the maximum asset quota that the borrower can borrow.For example, 70% of the LTV said that for the mortgage worth 100 USDT, the borrower’s upper borrowing is up to 70 USDT.

-

Health factor:Reflecting the safety level of the borrowing position, the higher the health factor, the stronger the debt repayment capacity of the borrower; otherwise, the lower the health factor, the weaker the debt repayment capacity.Once the health factor drops below 1, it indicates that the mortgage may face liquidation.

>

-

Clearing thresholdTheThe lowest proportion between the value of mortgage assets and the value of borrowing assets is set.When the borrower’s position touches this threshold, its mortgage is risk of liquidation.

>

In the AAVE protocol, Flash Loans is a breakthrough financial innovation. It relies on the atomic characteristics of Ethereum trading: all operations in the transaction are either fully executed or completely not executed.This mechanism enables participants to borrow large assets without providing mortgages.The borrower is borrowed from AAVE from AAVE in the time frame of a block (about 13 seconds) and repaid it in the same block, so as to achieve a rapid closed loop of the lending process.

Lightning loan greatly simplifies the process of implementing price arbitrage, automation trading strategy, and other decentralized finance (DEFI) operations, while effectively avoiding liquidity risks.In the AAVE V3 protocol, the fee for each Lightning loan transaction is 0.05%, which is significantly lower than 0.3%of the Uniswap V2, which brings users more economical borrowing options.

>

>

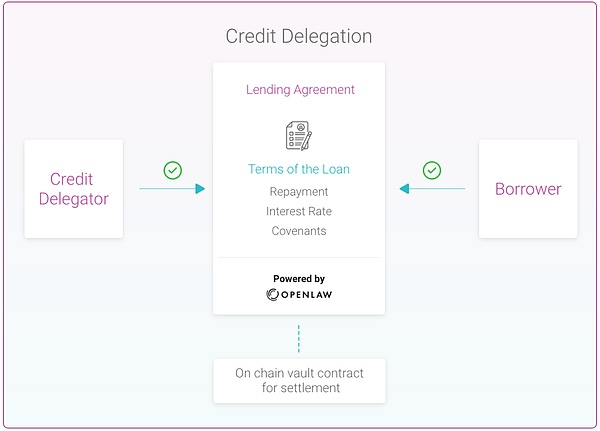

Figure 7: Credit entrustment mechanism diagram

AAVE launched the Credit Delegation in August 2020,Through the credit commission, the depositee can entrust its unsatisfactory credit quota to other users, and the borrower can obtain additional borrowing capabilities.

In addition, OPIUM in September 2020Credit Default Swaps (CDS) was launched for AAVE’s credit commission mechanism.As a risk management tool, CDS allows investors to transfer the risk of breach of specific borrowers, thereby adding an additional protection to the credit commission mechanism.The following cases and details of the credit commission mechanism are explained through the case provided by AAVE:

>

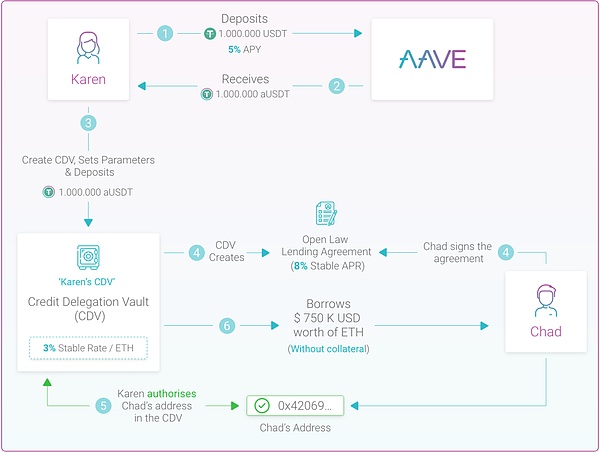

Figure 8: Case of AAVE Credit Entrustment

-

As a depositor, Karen deposits a USDT USDT into AAVE. According to the setting of AAVE, her annualized return (APY) is 5%.As a deposit voucher Karen, it received AUSDT worth $ 1 million.

-

In order to further participate in the credit commission mechanism, Karen needs to create a CDV (Credit Delegation Vault) smart contract.The contract will allow Karen to deposit AUSDT worth $ 1 million and set various parameters including credit lines.To this end, Karen needs to pay a 3% ETH stability fee.

-

According to the parameters she set, Karen and Chad reached a consensus on the borrowing terms through the Openlaw platform and agreed to borrow with an annualized interest rate (APR) of 8%.The two parties agreed to the agreement and officially signed.

-

Subsequently, Karen added CHAD’s receipt address to the white list of CDV, so that CHAD can borrow $ 750,000 from the CDV based on the credit limit without providing any mortgage assets.

-

In this case, Karen’s actual annualized yield (APY) calculation method is to minus 3% stable fee of 5% plus 8% borrowing interest rate, that is, 5% -3% + 8% = 10%EssenceThis rate of return is higher than her interest rate that she originally passed AAVE directly.CHAD successfully borrowed $ 750,000 without mortgage, and agreed to pay 8% of the annualized interest rate.

-

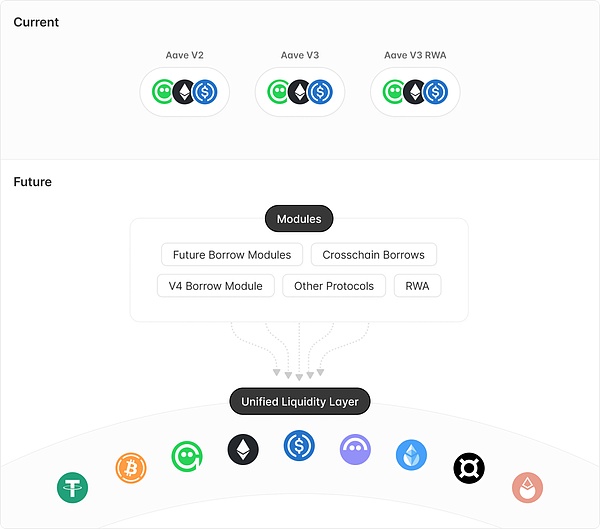

Unified liplation layer

The liquidity layer is designed on the Portal concept of the AAVE V3 version.Taking the overall AAVE as an example, the current AAVE V2 and AAVE V3 are decentralized due to the version update, and the overall liquidity is spent for a long time to complete the migration from V2 to V3.The liquidity layer proposed by V4 aims to uniformly manage the upper limit, interest rates, assets, and incentive measures borrowed from the supply and borrowing, allowing other modules to extract liquidity from it.In short, when AAVE DAO plans to join or remove a new functional module (such as isolation pool, RWA module, and CDP), no migration liquidity is required, and all kinds of modules only need to uniformly extract from the liquidity layer to extract from the liquidity layer.Llericality is sufficient.

-

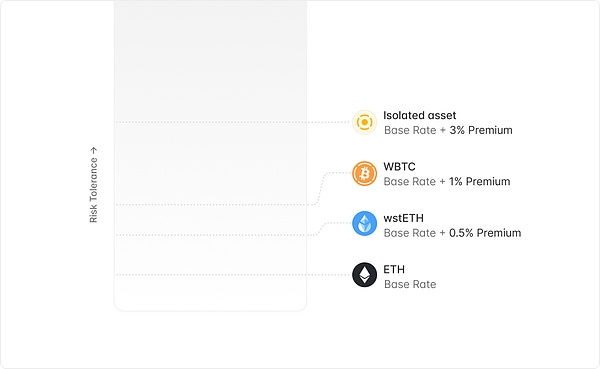

Liquidity premium

The AAVE V4 version introduces the liquidity premium function, which is a adjustment interest rate to adjust the borrowing rate according to the risk of the mortgage.The risk factor for each asset is dynamically adjusted according to the market and external risk factors.Assets (such as Ethereum) with lower risks will enjoy lower borrowing interest rates, and assets (such as cottage coins) will be relatively increased by borrowing costs.

-

The design of smart accounts and vault has greatly enhanced the user experience. Smart account allows users to manage multiple positions through a single wallet.And the vault function implemented by smart accountsAllow users to borrow without providing mortgages directly to the liquidity layer,The mortgage will be locked when the loan active or liquidation incident occurs, increasing the convenience and security of user interaction.

-

V4 version is also proposedDynamic risk configuration, Adjust the risk parameters when market conditions change.When borrowing, users will be associated with the current allocation of assets, while the new asset allocation is provided to new users, which avoids affecting existing borrowers.In addition, V4 is introducedAutomatic delisting mechanism, Simplified the process of getting off the assets.

-

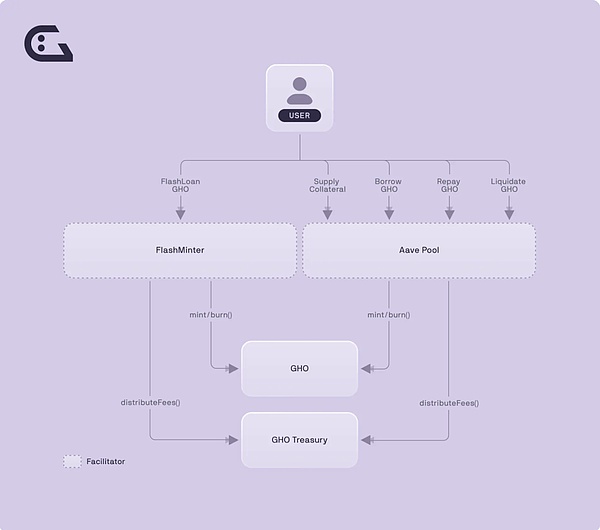

Native GHO casting: V4 version proposes that GHO’s native casting will be performed efficiently in the liquidity layer;

-

GHO “soft” liquidation: Drawing on CRVUSD’s liquidation model, V4 introduces a lending -liquidation automatic market as a market business (LLAMM) to simplify the clearing process.Users can choose to convert to GHO when the market is sluggish, or repurchase the collateral when the market rises;

-

Stable currency interest is paid with GHO: V4 will support the depositors to receive interest payment with GHO.When stable currency deposits choose this, interest payment will be converted to V4’s PCV (Protocol Controlled Value), and the interest payment process of interest will also enhance the stability of GHO and improve capital efficiency.

-

Emergency redemption mechanism: The emergency redemption mechanism proposed by V4 is used to cope with extreme anchor situations.When this mechanism is triggered, the lowest health of the position corresponding to the low level will be redeemed as GHO and is used to repay its debt.

-

Promotioner (Facilitator):The protocol, entity or project of controlling GHO’s casting and destruction mechanism, AAVE is the first promoter of GHO

-

BUCKET:The upper limit of the GHO holdings determined by community governance through voting is to maintain the stability and liquidity of the price of GHO.

-

Discount mode:The lending rate will adjust the discount mode according to the holdings of Stkaave.

-

Isolation mode:GHO uses the isolation mode to allow users to generate various assets supported by the AAVE protocol, reducing the impact of market volatility on system stability.

-

High -efficiency mode:High -efficiency model supports users can use non -volatile mortgage assets to borrow more GHOs to balance their positions, thereby increasing the supply of GHO in the market and reducing the pressure of demand.

-

Cross -chain portal:The portal function provides ideal ways for GHO’s expansion in the multi -chain ecosystem, thereby reducing the risk of cross -chain interaction.

-

Profile NFT (Personal Information NFT):That is, the user’s identity in the Lens ecosystem can be obtained by casting or buying.It contains the historical records of all users, mirror, comments, etc., and gives users the complete control of these contents.

-

Collect NFT (Favorite NFT):That is, the creator’s content profit model in Lens ecology, followers can buy the content created by the creator.

-

Follow NFT (Follow NFT):That is, the user’s attention in the Lens ecosystem. When the user pays attention to a personal data on Lens Protocol, they will get a Follow NFT.

-

Publication (Posted):Divided into three types: posts, comments and reposts.Publication is directly published on the user’s Profile NFT, ensuring that everything created by users is owned by the user.

-

Comments (comment):Allows users to comment on other people’s Publication, and the comments also exist in the user’s NFT, so they are completely belonging to the user.

-

Mirror (mirror):Equivalent to the forwarding function in traditional social media.Because they quoted other Publication, they were subject to conditional constraints of the reference module of the original Publication and could not be collected.

-

Borrowing income (that is, agreement income):The handling fee charged by providing a loan to the borrower

-

Lightning loan fee:For the handling fees collected by users who use Lightning Loan, the AAVE V3 protocol is charged 0.05% of each Lightning loan transaction

-

Other functional costs:Other fees obtained by AAVE through liquidation, portal bridge, AAVE ARC, etc.

-

GHO coinage fee

>

According to the description of the AAVE V4 protocol development proposal, the AAVE V4 will be constructed with a new architecture, with high -efficiency and modular design, and at the same time to minimize the impact on third parties and provide more convenient conditions for the expansion of third parties.

Liquidity layer

>

Figure 9: Uniform lilation layer signal

>

Figure 10: Diagram of liquidity premium

Fuzzy control interest rate

At present, AAVE’s interest rate setting not only increases the complexity of governance, but also affects capital efficiency.The AAVE V4 version of the proposal introduces a fully automatic interest rate mechanism, using fuzzy interest rates to dynamically adjust the slope and inflection point of interest rate curves.This innovative interest rate management method will allow AAVE to flexibly increase or reduce basic interest rates according to the real -time market demand, thereby providing more optimized interest rates for deposits and borrowers.

>

Figure 11: Vague control interest rate schematic diagram

AAVE V4 lending module

The AAVE V4 version optimizes the security and user experience of borrowing and lending by introducing a series of innovative functions and simplifies the governance process:

Excess debt protection mechanism

Due to the risk of bad debt diffusion in shared liquidity, the AAVE V4 introduced a new mechanism to track the positions of non -debt and automatically handle its cumulative excess debt.This mechanism can automatically lose the borrowing capacity by setting the debt threshold. Once the threshold corresponds to the asset, it will automatically lose the loan capacity to prevent its adverse debt transmission, thereby protecting the shared liquidity model to receive infection.

GHO Native Integrated Plan

AAVE V4 proposes a plan to strengthen integration with GHO, which aims to improve the user experience and improve the income of stable currency suppliers.

Aave network

At the same time, the Aave team also proposed the concept of Aave Network.The AAVE team is expected to develop an AAVE network that can be used as the main hub of AAVE and GHO.The network will be paid with AAVE V4 as the core, and uses GHO for payment, and is managed by the community voting through Aave Governance V3, and inherited network security from Ethereum.At present, the concept is still in the design stage, and the AAVE team said that they will closely pay close attention to L1 and L2 related technologies and select the corresponding implementation plan.

>

The borrowing interest rate of GHO stabilized currency is determined by AAVEDAO and can be dynamically adjusted according to market conditions to adapt to the changes in the fluctuations of the economic cycle and the change of fund supply and demand.

The innovation characteristics of GHO stablecoin are mainly reflected in the following key aspects:

The update of the AAVE V3 version has a positive impact on the operation of the GHO stablecoin, which is specifically reflected in:

>

Figure 12: GHO mechanism

>

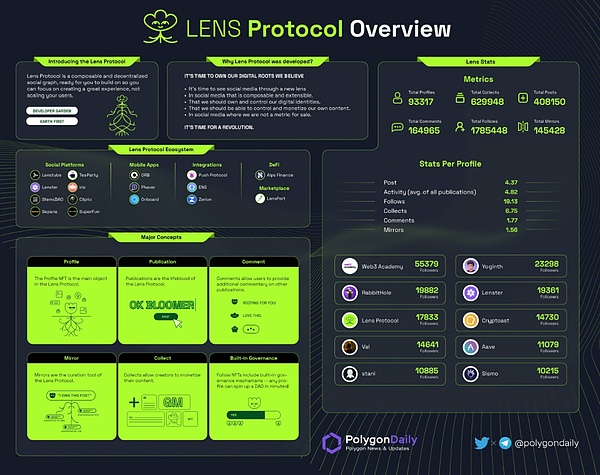

Lens Protocol is an innovative social network agreement launched on the Polygon blockchain. Its design concept is a modular underlying protocol to promote the expansion and continuous development of the community.This agreement encourages developers to build a variety of social applications on their basis, while ensuring that users can fully control their content and social relationships.

>

The core innovation of Lens Protocol is to convert social media behavior to NFT (non -homogeneous tokens), which is mainly reflected in the following aspects:

>

The functional module of Lens Protocol includes:

>

At present, Lens Protocol has developed a variety of social related applications, such as decentralized Twitter substitute Lenster.xyz, video content platform Lenstube.xyz, and decentralized resume platform orb.ac.These applications reflect the potential of Lens Protocol in reshaping social media interaction.

>

Figure 13: Lens Protocol Ecological panorama

>

With the increasing importance and influence of decentralized finance (DEFI) in the global financial market, traditional fintech companies, hedge funds, family offices, and asset management companies’ demand for DEFI solutions continued to increase.In order to respond to this market demand,AAVE launched AAVE ARC -a private liquidity pool solution designed by institutional investors designed to meet strict supervision requirements.

AAVE ARC’s private pool and existing public liquidity pools on AAVEMutual independenceIt ensures that participants can safely participate in the market safely under the environment of compliance with regulatory standards.

In the AAVE ARC ecosystem, USDC, as the only stablecoin provided, is the reason why USDC is strictly regulated and is widely considered to be a stablecoin suitable for institutional investors.In addition to USDC, AAVE ARC also supports other three mainstream assets:Bitcoin (BTC), Eto (ETH) and AAVE.

In order to meet the attention of institutional investors to regulatory risks, AAVE ARC has implemented strictlyCustomer identification (KYC) program and “whitelist” mechanismIt not only further strengthened the security and compliance of the platform, but also provided higher trust and reliability for institutional -level users.

>

Figure 14: AAVE ARC

According to DEFILLAMA data, AAVE ARC TVL continued to maintain its low point after the plunge in November 2022, and there was no relevant progress information in the near future.

>

Figure 15: AAVE ARC TVL

>

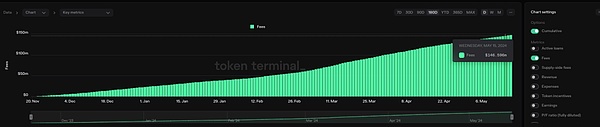

According to the data of Tokenterminal, as of 2024, on May 15th, the AAVE V3 protocol cumulative borrowing fee (Fees) was as high as $ 146.6 Millions.In this cumulative cost, the borrowing costs on the Ethereum network occupy most of the dollar, reaching 45.6 Millions dollar.

>

Figure 15: AAVE Fees

From 2023 to 2024, the total revenue of the annual agreement between AAVE V2 and V3 was US $ 20,646,600, a decrease from 209.262 million US dollars from 2022 to 2023, a decrease of 3.2%.Although the income is slightly reduced,Since December 2022, the revenue of the AAVE protocol has been enough to cover its token inspiration and achieve surplus.This marks AAVE’s stability in financial management.

The main income of the AAVE protocol can be divided into the following four categories:

>

Figure 16: Aave annual income analysis

>

>

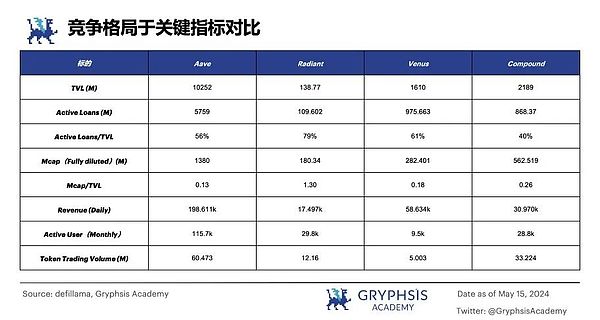

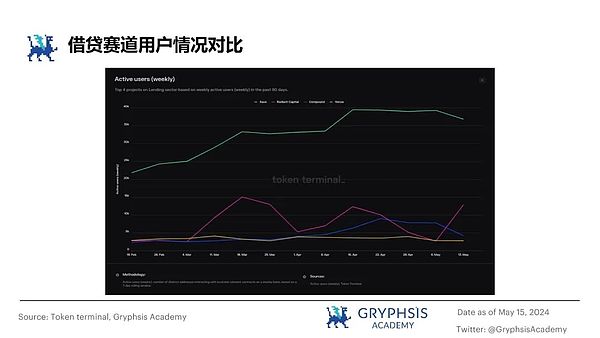

The lending industry plays a pivotal role in the field of decentralized finance (DEFI), and its total value lock (TVL) ranks second in various DEFI sectors, second only to the Liquid Staking industry.According to the data provided by Defillama, there are currently 379 borrowing agreements on the market.In these agreements, the top lending agreement includes AAVE, Justlend, Spark, Compound, Venus, and Morpho.

AAVE stands out in the field of DEFI with its significant leading advantage, and its current TVL has reached $ 1.025 billion.Among the top five lending agreements, AAVE has successfully logged in to 12 different blockchain networks, while the number of compounds with the largest number of login chains in other agreements is only 4.

Specific to each chain, AAVE (V2/V3) is the largest borrowing protocol on Ethereum, Arbitrum, Avalanche, Polygon, and Optimism, and it is ranked fifth on BSC.

>

Figure 17: Defi borrowing track comparison

>

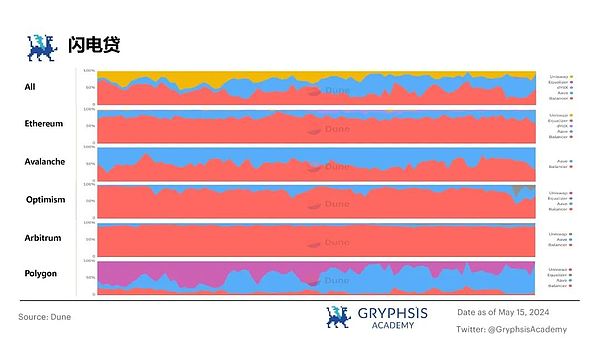

As a key innovation in the DEFI ecosystem, Lightning Loan has played a vital role in the development of the entire decentralized financial system.According to Dune’s data, the total transaction volume of Lightning Loan has reached about $ 248,596 in the past month.Among the many lightning loan tools, BALANCER, AAVE and Uniswap ranks in the top three, becoming the leading force in the market.

From the perspective of market share, the performance of Balance and AAVE has been particularly prominent in the past three months.Their market share is about 40%, which is higher than Uniswap.

Specific to the situation on different blockchain networks, AAVE’s market share on Ethereum, Avalanche, Optimism, and Arbitrum is slightly lower than Balancer.However, on the Polygon network, AAVE’s market share is significantly ahead of other lightning loan tools, showing its strong competitiveness and user base on the chain.

>

Figure 18: Lightning Loan Circuit Comparison

>

As mentioned earlier, the AAVE V3 version is introduced by the Portals function. The AAVE V4 further designed the concept of liquidity layer based on Portals. It aims to enhance the cross -chain liquidity and utilization rate of assets. This is an important innovation in the DEFI ecosystem.EssenceSimilar products or functions in the market also include Radiant Capital, Cedro Finance, Flux V3, Prime Protocol, Paribus, etc.Although some cross -chain lending solutions have appeared in the DEFI ecosystem, this field is still in the development stage.

Radiant Capital V2 is the first to build a full -chain interoperability by using Layerzero’s Omnichain technology (although Radiant Capital has suspended its borrowing market on Arbitrum in January 2024).

Overall, cross -chain lending is a field that is gradually maturing and rapidly.Radiant Capital has a certain leading position in market maturity and user participation with its first advantage.At the same time, AAVE has shown huge potential in the field of cross -chain lending as its TVL that far exceeds other competitors.

>

Figure 19: Cross -chain lending track comparison

>

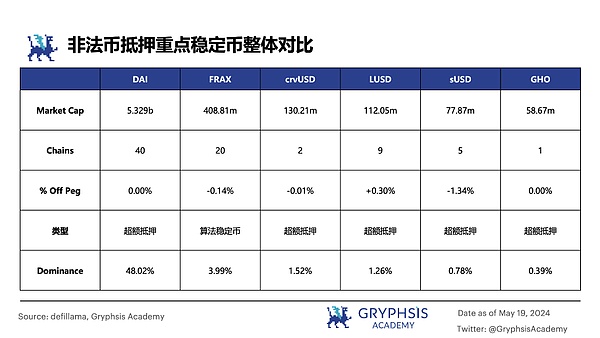

Since AAVE launched its stablecoin GHO in July 2023, the price of GHO has been below $ 1 for a long time.In November 2023, AAVE announced a series of measures to restore the anchor value of GHO. These efforts were finally confirmed by Aave founder Stani Kulechov on February 7, 2024, announcing that GHO had successfully resumed the anchor.

At present, GHO accounts for about 0.504%in the illegal currency mortgage stable currency market.Compared with other mature illegal currency mortgage stablecoins on the market, GHO, as an emerging stablecoin, has a relatively small market value. The main use scenarios include pledge on the AAVE platform for benefits, or after exchange with other stablecoins.

Generally speaking, the development of GHO is still in the early stage. AAVE is taking various measures to enhance the stability of the GHO anchor, and has increased the upper limit of the coin to 50 million pieces.Through these measures,You can observe that AAVE is committed to deepening the integration of GHO and AAVE platform to promote the use of stable coins in a wider range of application scenarios.

>

Figure 20: Comparison of stable currency track

>

>

As the native governance tokens of the AAVE platform, AAVE tokens not only play a core role in platform governance, but also a key component of the pledge reward mechanism.The predecessor of the AAVE tokens was the Lend token issued by the ETHLEND project in 2017.Initially, the total supply of LEND tokens was set to 1.3 billion pieces.

With the continuous evolution of the AAVE ecosystem, by 2020, AAVE released its V1 version, accompanied by the brand to reshape, the Lend tokens converted to the AAVE token with a redemption ratio of 1: 100.In the process, in order to further support and promote the development of the AAVE ecosystem, an additional 3 million AAVE tokens were issued.The total supply of AAVE token was therefore set to 16 million pieces.

According to the latest data of CoinMarketcap, the number of AAVE tokens circulating on the market is about 14.7 million pieces.This shows that the circulation of AAVE tokens has occupied most of its total supply, reflecting the active participation of the AAVE community and the importance of governing tokens in the DEFI ecosystem.

>

Figure 21: AAVE token economics signal

>

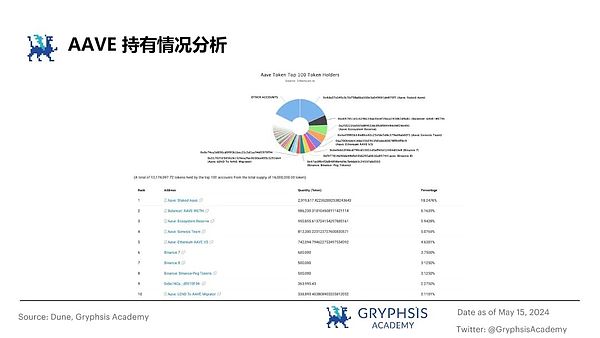

Among the top ten holdings of AAVE, only the ninth place is the big coin, accounting for about 2.275

Figure 22: Analysis of AAVE holding situation

>

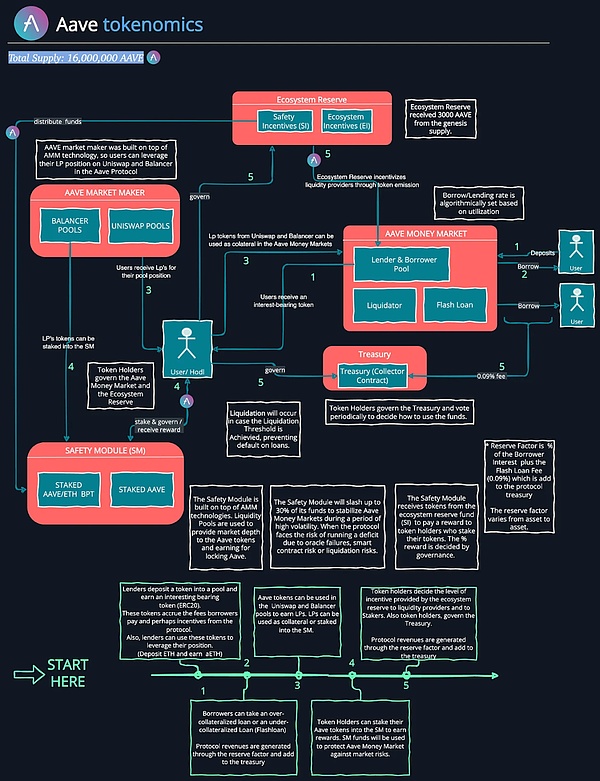

In the AAVE ecosystem, the AAVE tokens plays a vital dual role: the first is to participate in the governance of the AAVE protocol, and the second is to pledge in the security module to obtain the profit dividend of the agreement.

>

Figure 23: AAVE token use

>

The governance of the AAVE protocol is managed and managed by the governance token holders holding AAVE, Stkaave and AAAVE in the form of decentralized autonomous organization (DAO).The governance token holders obtained the weight of governance based on the sum of the balance of AAVE, Stkaave and AAAVE they held, and obtained the corresponding proposal rights and voting rights.In AAVE GOVERNANCE V3, each proposal specifies a voting network, and all votes are performed on the network.

>

Figure 24: AAVE governance process

>

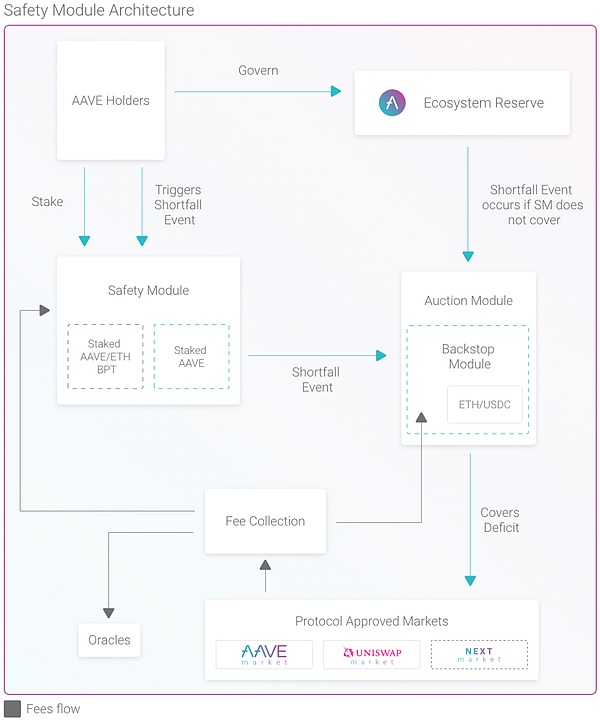

The AAVE protocol provides two pledge methods for the AAVE token holders: pure AAVE pledge and AAVE BALANCER POOL Token (ABPT) pledge pool, which consists of 80% of AAVE and 20% ETH.

Users can choose to pledge the AAVE tokens directly in the AAVE security module, or provide AAVE and ETH liquidity through the Balance Lili liquidity pool to obtain ABPT and pledge it in the AAVE security module.This method can not only earn pledge income, but also have the opportunity to get additional BAL rewards and trading fees.

>

Figure 25: Security module mechanism

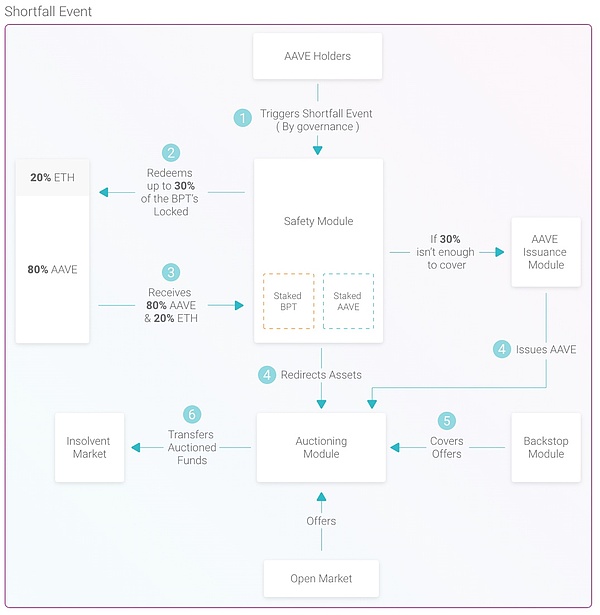

AAVE’s pledge mechanism is a way to balance risk and return.Users are willing to bear certain risks in exchange for security incentives by pledged AAVE tokens.The security module aaVE protocol provides financial support when encountering financial problems.If the funds are not enough to cover the loss, the agreement will start the “restoration of issuance” mechanism to supplement the funds by adding AAVE tokens.

The AAVE protocol’s auction module adopts Dutch auction and is responsible for managing the market issuance of pledged funds.When necessary, funds are raised by auction AAVE and ETH to ensure market stability.

Users participating in the pledge will get Stkaave tokens, which is an ERC-20 standard tokens as proof of pledge.Users holding Stkaave can exercise the right to vote and enjoy discounts when pledged GHO.

>

Figure 26: pledge mechanism

>

>

As of May 15, the AAVE protocol on Ethereum showed a strong TVL, reaching $ 10.252 B.In the ranking of the DEFI borrowing agreement, AAVE tops the list, followed by Compound, Venus, and Radiant. The total value of the four major protocols has a total of $ 15.408 billion.

>

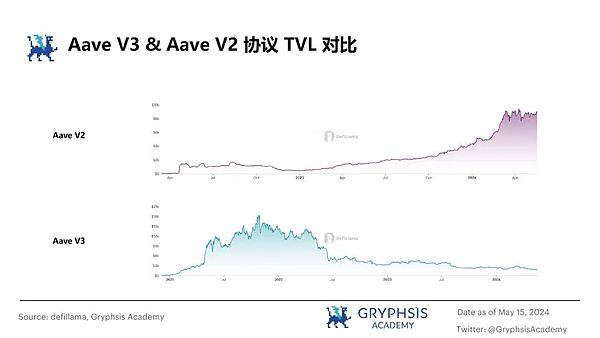

Figure 27: Aave v3 & amp; v2 tvl comparison

Since the launch of AAVE V3, AAVE V2’s TVL (total locking value) has gone through a gradual decline.After about half a year of volatility, AAVE V3’s TVL entered a stable growth stage and successfully surpassed V2’s TVL in September 2023.

The overall market value of the AAVE protocol to TVL (MCAP/TVL) has maintained a lower level, which is usually regarded as a positive signal.The lower MCAP/TVL ratio indicates that the market value of the agreement is more reasonable than the value lock on its platform, suggesting that there are fewer market bubbles and high internal value.

>

>

>

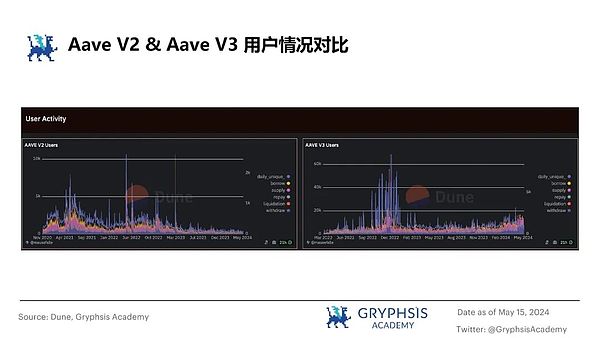

Figure 28: Comparison of users of the borrowing market

Since 2021, the user foundation of the AAVE platform has experienced two significant growth, which is mainly launched by the AAVE V3 version and the market heating at the end of 2023 and the launch of its native stablecoin GHO.As of May 15, 2024, Aave V2 recorded 186 users, and AAVE V3 had as high as 14,752 users. This data clearly shows that the V3 version is popular among users.

Among the current AAVE V3 user group, users who provide liquidity and access to access operations occupy a large proportion, which may be related to the enhanced capital efficiency and diversified function of the V3 version.In contrast, among the users of AAVE V2, the proportion of extraction operations and users who only complete a single transaction may reflect the use of this version to use this version for one -time or simpler borrowing activities.

>

>

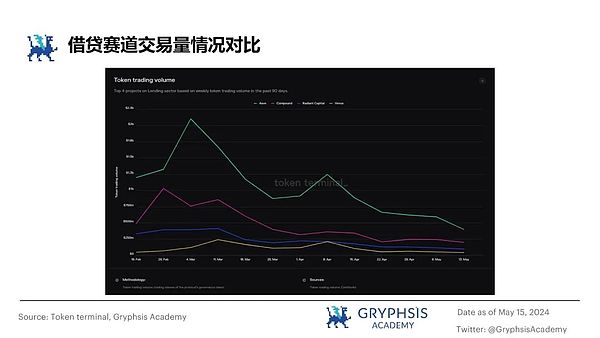

Figure 29: Comparison of transaction volume in the lending market

AAVE’s transaction volume in April 2024 reached $ 26.588 B. This number increased by 16.9%from March, showing that AAVE not only has the highest transaction volume in the DEFI lending field, but also has the fastest growth rate in the near future.This significant growth trend reflects the high trust and preferences of investors in the AAVE platform during market heating.

>

>

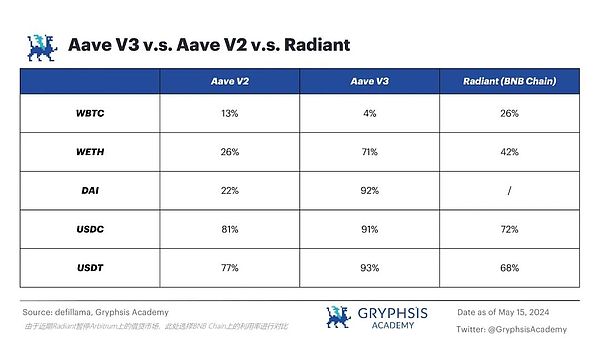

Figure 30: Comparison of utilization rate of borrowing market

AAVE V3 has significantly improved the utilization of assets through its high-efficiency model. This feature makes AAVE V3 dominant in the overall asset utilization rate in similar DEFI borrowing agreements.Specific to the utilization rate of individual assets, on the RADiant platform, the utilization rate of WBTC and WETH is particularly high.AAVE V2’s performance in stable currency is similar to Radiant, but AAVE V3 significantly exceeds other protocols in terms of utilization.

>

>

The current cross -chain lending market is already the first to lay out the protocol such as Radiant.Although product stability is still further strengthened, its potential market space is huge.AAVE V3’s launch speed is slightly slower than competitors, which may affect its competitiveness in this field.

>

AAVE has always maintained a leading position in the lending market, but in the face of many agreements to provide innovative lending plans, such as Lightning Loan and cross -chain lending, competition has become increasingly fierce.These innovative measures may challenge AAVE’s user growth and market share.Therefore, AAVE needs to provide unique value claims to attract and retain users and maintain its market leadership.

>

The stablecoin Gho in the AAVE ecosystem has been slightly decoupled since its launch, although it has recently achieved stability.However, the integration of GHO and AAVE loan function is currently not close, and its role in the AAVE ecosystem has not been fully played.

>

As a leader in the field of decentralized finance (DEFI) lending,AAVE has significantly ahead of competitors in terms of asset utilization, market share and transaction volume, playing key rolesEssenceHowever, AAVE’s leading position is not impossible.Protocols such as Radiant and Compound have shown strong growth potential and launched a new version with growth potential.In order to consolidate its market position,AAVE can adopt the following strategies: strengthen its core lending business, promote the further development of GHO and fully integrate it at AAVE, establish the AAVE Network designed by V4 version, and expand its non -loan business ecosystem.