author:Chaos Labs Source: X,@Chaos_Labs Translation: Shan Ouba, Bitchain Vision

In traditional finance, the currency market provides short -term lending opportunities. It is usually for assets with strong liquidity and low risk. The goal is to provide as high returns as possible under the premise of security.In decentralized finance (DEFI), this concept has evolved, mainly refers to various digital assets without licenses and decentralized borrowing, and there is no specific time limit.These platforms allow users to deposit cryptocurrencies into the agreement and earn benefits through interest paid by the borrower. At the same time, borrowers need to provide sufficient mortgage as guarantees.

The currency market uses a dynamic interest rate model to automatically adjust the borrowing interest rate according to the liquidity utilization rate in specific markets or capital pools.These models ensure that the capital is efficiently deployed, and at the same time, the borrower is encouraged to return assets as soon as possible when the liquidity is scarce.One key feature of interest rate curve is “inflection point”, that is, when the utilization rate reaches a certain threshold, interest rates begin to rise significantly to control the leverage in the control system: as the utilization rate increases, interest rates may gradually rise, but it will surge sharply after the inflection point exceeds the inflection point., Greatly increase the cost of lending.

It should be noted that the currency market is different from unsecured loans: the currency market requires borrowers to provide mortgage to ensure the ability to pay for the loan; and the traditional sense of loans are usually unsecuredLending loan.

Why the currency market is the key DEFI “Lego” module

By releasing liquidity by allowing users to earn income on idle assets and without selling assets, the currency market has played a vital role in DEFI’s capital efficiency.In the industry, the ability to borrow a loan based on specific tokens is a high -demand function, which often determines whether a certain encrypted asset is considered “blue chip” asset.

The currency market allows users to conduct low -cost leverage operations on their assets, and high net worth individuals integrate them into tax planning. At the same time, teams with rich funds but insufficient liquidity use their assets as mortgage borrowings to provide fund support for the project. At the same timeIt can also earn interest from the mortgage position (Curve and Maker have been typical cases of this model in the past few years).

In addition, the currency market is the foundation of other DEFI tools, such as mortgage debt positions (CDPS), income agricultural strategies (supporting multiple pseudo -market neutral strategies), and chain margin transactions.

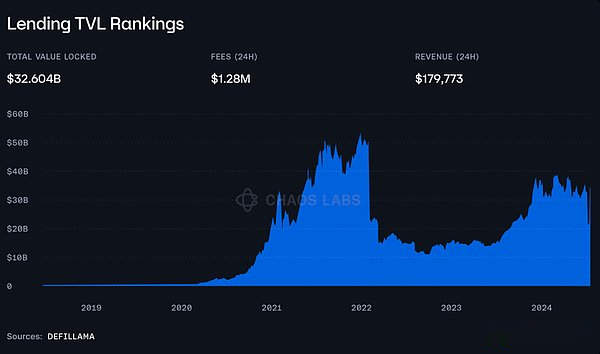

Therefore, the currency market is considered to be one of the most important construction modules in DEFI, that is, “Financial Legao”.In terms of scale, the total lock value (TVL) of the encrypted borrowing agreement has exceeded 32.6 billion US dollars, as shown in the figure below.

>

Design selection in the cryptocurrency market: sharing and independent liquidity pool

Although the basic goals of the cryptocurrency market are the same, their design choices may be significantly different, especially in terms of liquidity structure.The biggest distinction is that the currency market (such as AAVE) that shared the liquidity pool and the market for the implementation of the independent liquidity pool (such as Compound V3).Each model has its advantages and disadvantages, and influencing factors include depth of liquidity, asset flexibility and risk management.

Independent liquidity pool: flexibility and risk isolation

In the independent liquidity pool model, each market or assets run in their respective liquidity isolation areas.This method is adopted by Compound V3 and some more extreme platforms (such as Rari Capital) (although the latter has failed).

The main advantage of the independent liquidity pool is its flexibility and can tailor the market for specific asset categories or user needs.For example, the independent pool can support a specific asset group (such as the moldy coin) or tokens that include only some unique risk characteristics or demand.This customization enables the independent liquidity system to meet the needs of specific communities or fields, and these needs may not be realized in a wider shared liquid pool framework.

In addition, the independent liquidity pool also provides better risk isolation.Each market is partitioned and risks related to specific assets are limited to its market.If the value of a certain alternation decreases sharply or is too large, its potential impact is limited to the market and avoids affecting the entire agreement.

However, these benefits are also accompanied by the price: independent liquidity means fragmentation.For independent markets, the problem of cold start needs to be resolved repeatedly when each new market is created, because each market can only rely on its own participants, and the liquidity may not be enough to support significant loan activities.

>

As mentioned earlier, some agreements have pushed the concept of the independent loan market to the extreme, allowing users to create such a market without license.

In these cases, such asRARIorSolendprotocol, Users can create their own license market, determine their own asset list, risk parameters (such as loan value ratio LTV and mortgage ratio CR), and manage the corresponding incentive mechanism.

Sharing liquidity pool: Since the first day, have deep liquidity

On the other hand, a single shared liquidity pool has provided sufficient liquidity support since the first day.By integrating all assets into a unified pool, the shared liquidity system can support large -scale borrowing activities. Even newly added assets can be limited by liquidity.

For users who provide liquidity, shared pools are also beneficial: a larger liquidity foundation attracts more borrowers, thereby generating higher and more stable returns, because these benefits are supported by diverse borrowing demand.

This is the main advantage of sharing liquidity models. Although its core advantages are only one, its importance cannot be underestimated.In all markets, liquidity is the most important, especially in the field of cryptocurrencies.

However, the main disadvantage of sharing liquidity pools is systemic risk.Because all assets are connected to the same -class activity pool, the problem of a certain asset (such as sudden depreciation) may cause a liquidation chain reaction, especially when it generates bad debts, it may affect the entire system.

Therefore, compared with the highly flowing and established tokens, these pools are not suitable for niche or experimental assets.

Finally, the governance and risk monitoring of shared liquidity systems are usually more complicated, because the impact of any agreement change may be very significant.

The mixed trend of models?

The balance between independence and sharing liquidity pools is very significant, and there is no single method to be perfect.This is why with the maturity of the market, the currency market is becoming more and more tended to adopt a hybrid model (or at least the introduction of hybrid function) to balance the liquidity advantage of the shared pool and the customized and risk isolation function of the independent market.

AaveThe method is the perfect example of this trend.LidofinanceandEther_fiWhen the platform cooperates, a carefully designed independent market is introduced.The AAVE system usually works with a single liquidity pool to provide deep liquidity for major assets.However, AAVE recognizes that assets that support different risk characteristics or use scenarios require greater flexibility, so the market for specific token or cooperative projects has been created.

Another key feature that conforms to this trend is AAVEemode, Designed for high -related assets to optimize capital efficiency.EMODE allows users to unlock higher leverage and borrowing capabilities for closely related assets (thereby clearly low liquidation risks), thereby significantly improve capital efficiency by isolation.

Similarly, likeBenqifinanceandVenusprotocolSuch an agreement, although traditionally belongs to the shared liquidity category, has also introduced the needs of a specific sub -field by introducing the independent pool.For example, these independent markets can focus on niche areas, such asGamefi, Real World Assets (RWA) or “Ecosystem tokens” without affecting the operation of the main pool.

At the same time, the currency market in the independent market (such asCompoundorSolend) Usually there is a “main pool” as a shared liquidity pool.Taking Compound as an example, it recently started adding more assets to its most liquid pool, which effectively moves closer to the mixed model.

The business model of the currency market

The core business model of the cryptocurrency market is revenue around a variety of mechanisms related to borrowing and mortgage debt (CDP).

1. Poor interest rate

•mechanism:The main source of income of the currency market is the difference between loans and borrowing interest rates.

•process:Users can earn assets into the agreement to earn interest, and borrowers need to pay interest to obtain liquidity.The difference between the difference between the interest rate charged to the borrower and the interest rate paid to the deposit interest rate.

•Example:On AAVE V3 Ethereum, the current $ ETH deposit interest rate is 1.99%, while the borrowing interest rate is 2.67%, which generates 0.68%of the interest rate difference.Although the difference is small, the income will gradually accumulate as the number of users increases.

2. Clear cost

•mechanism:When the borrower’s mortgage is lower than the required threshold, the agreement will start the liquidation process to maintain the system’s solvency.The liquidator obtains some of the borrower’s mortgage as a exchange price as a exchange, and settled some of its debt.

•Income source:Generally, the parliament is divided into part of the cost from the liquidation rewards.Sometimes the agreement also runs its own clearing robot to ensure timely liquidation and obtain additional income.

3. CDP -related costs

•Toll method:The agreement may charge for its CDP products. These costs may be charged at one time, accumulated by time, or both.

4. Lightning loan cost

•mechanism:Most protocols allow users to perform lightning loans and charge a small amount of but very considerable fees.

•Function:Lightning loan is a loan that must be repaid in the same transaction, allowing users to obtain the required capital immediately to perform certain operations (such as liquidation).

5. Treasury income

•operate:The agreement usually uses its national treasury funds to find a source of safety income, thereby further increasing income.

These mechanisms make the lending market one of the most profitable agreements in the encryption field.

>

These costs are sometimes shared with tokens to incentive form recycling or only for payment of operating costs.

Risk & lt; & gt; currency market

As it is said, the business of operating the cryptocurrency currency market may be one of the most profitable businesses, but it is undoubtedly one of the most risky businesses.

The first obstacle facing the new currency market is the problem of cold start.This refers to the difficulty of guiding liquidity in the new agreement or market.Due to low liquidity, reduced borrowing opportunities, and potential security vulnerabilities, early users were reluctant to deposit funds into the capital pool that had not reached the critical scale.Without sufficient initial deposits, interest rates may be too low and cannot attract the loan, and borrowers may find that they cannot obtain a loan they seek, or they face over -fluctuating interest rates due to changes in liquidity.Agreement is usually solved by liquidity mining incentives to solve the problem of cold start. Users can obtain native currencies as rewards by providing liquidity or borrowing liquidity (the incentives of one party will indirectly reflected in the other side, especially when the cycle is available).However, if you do not manage it carefully, the dependence on such incentives may produce unsustainable emissions. This is the trade -off that is considered to be considered when designing its launching strategy.

Timely liquidation is another key factor in maintaining the solvency of the agreement.When the borrower’s mortgage value is lower than a certain threshold, the protocol must clear the position to prevent further loss.This brings two main problems: First of all, the success of this process depends to a large extent on the existence of liquidants. Whether it is running by the agreement or being managed by a third party, they monitor the agreement and quickly implement the liquidation.

>

In order to achieve these goals, they need to be fully inspired by liquidation bonuses. These bonuses need to be balanced with the income of the agreement.Secondly, the liquidation program must be triggered when the position is still safely liquidated: if the granted mortgage value is too close or the same as the unburresed debt of the liquidation, the risk of the head inch to the bad debt is higher.In this regard, define security and the latest risk parameters (LTV, CR, establish a liquidation buffer between these parameters and liquidation thresholds) and apply strict selection processes to include the assets available on the platform on the white list to play a fundamental role.Essence

In addition, in order to ensure the smooth operation of the agreement, timely liquidation, and users will not abuse their functions. The currency market is seriously dependent on functional prophecy, providing real -time valuations for mortgages, and indirectly providing the health status and liquidity of loan positions.

The manipulation of prophet machine is an important issue worthy of attention. Especially for the protocol for low liquid assets or relying on a single source prophet machine, attackers can distort prices to trigger liquidation or borrow from the wrong mortgage level.This situation has happened many times in the past, and the most famous is the Mango Markets vulnerability of Eisenberg.Delay and waiting time are also critical; during market fluctuations or network congestion, the delayed price update may cause the mortgage’s valuation to be inaccurate, resulting in liquidation delay or pricing errors and bad debts.In order to make up for this, the agreement usually uses multiple prophecy machine strategies to summarize data from multiple sources to improve accuracy or establish a reserve prophecy to prevent the main source of the main source.The value of assets suddenly changed.

Finally, we have security risks: the currency market is the main victim of the vulnerability after the bridge.

The code for handling the currency market is extremely complicated. Only a few protocols can proudly have perfect courses. We see many agreements, especially the fork of complex borrowing products. Multiple loopholes will be generated when editing or error processing the original code.Agreement to reduce these risks through measures such as vulnerability bounty, regular code audit, and changes to the agreement to change the agreement through complex process approval.However, there is no one -loss security measure. The possibility of vulnerability is still a continuous risk factor that the team needs to be careful.

How to deal with losses?

When the agreement suffers losses, whether it is a bad debt caused by liquidation failure or accidents such as hackers, there is usually a standard terms to allocate losses.AAVE’s method can be used as an example again.AAVE’s security module acts as a reserve mechanism to make up for the shortage of potential agreement.Users can pledge AAVE tokens in the security module and get rewards, but if necessary, their pledged token may be reduced by up to 30% to make up for the deficit.This has served as a insurance layer, and has recently been further strengthened by introducing Stkgho.These mechanisms have essentially introduced the “higher risk, higher return” position for users, and maintained their interests with the benefits of the entire agreement.

Chaos labs & lt; & gt; currency market

Chaos Labs provides overall methods for the currency market customers: comprehensive solutions to optimize and protect their protocols.The most innovative is the edge risk prophet (EDGE RISK ORACLES) invented by Chaos Labs, which can automatically optimize the parameter update process of the protocol, thereby narrowing the user experience (UX) and capital between decentralized and centralized financial platforms.Efficiency gap.With the launch of EDGE, Chaos has expanded to the field of prediction machines, using the professional knowledge of the team in the field of risk monitoring, providing accurate and safe price data feeds, and real -time abnormal detection to ensure accuracy and reliability.CHAOS LABS also conducts mechanism design review, asset admission management and parameter recommendations for new assets and existing asset mechanisms to ensure that only after a thorough risk assessment will it integrate the appropriate assets and provide a safe optimization of the loan value ratio of variables; Chaos’s’s’s of CHAOSThe unique method is to monitor real -time risk monitoring through a detailed instrument board and design liquidity incentives to promote sustainable growth and user participation to solve the problem of cold startup and market competition.