Author: Michael Nadeau, The DeFi Report; Compilation: Tao Zhu, Bitchain Vision

Ethereum is executing its roadmap.The network is being expanded through Layer 2.Sometime this summer, we should have ETF trading.Larry Fink won’t stop talking about tokenization.We are on the verge of a Fed rate cut.

Now is a good time to be optimistic about Ethereum.

Should you have ETH?Or own a basket of L2?Or both?

In this week’s report, we provide a data-driven portfolio building framework.

L2 Data and Ethereum

We will start the analysis with some advanced data to compare the top L2 and ETH among multiple KPIs.

We also looked at the best among L2 in each indicator.

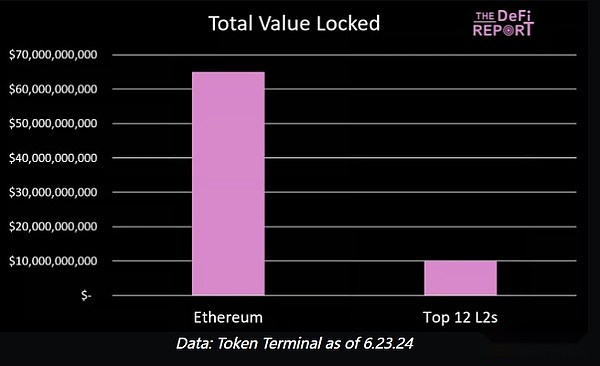

Lock the total value:

Data: Token Terminal as of June 23, 2024

The top 12 L2s account for 15% of Ethereum’s daily lock-in value.

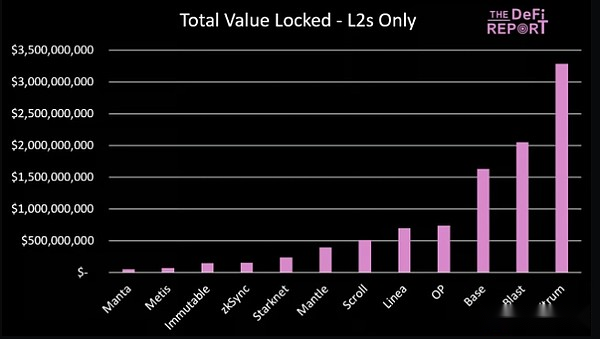

Here are the TVL rankings in L2:

Data: Token Terminal as of June 23, 2024

Arbitrum ranked first, with the top 5 drivers as follows:

-

Aave – $790 million;

-

Pendle – $659 million;

-

GMX – $612 million;

-

Renzo – $371 million;

-

Uniswap – $306 million.

It is worth noting that Blast ranked second by providing revenue in Ethereum (through staking) and stablecoins (through MakerDAO, Treasury bills).We will keep an eye on this to see how sticky it is after the token drops.

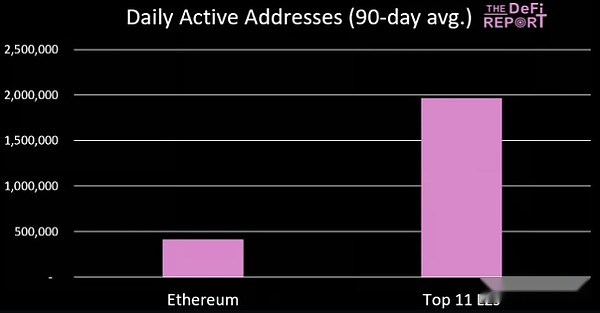

Daily active address:

Data: Token Terminal as of June 23, 2024

at present,The number of daily active addresses for top L2 is 4.7 times that of Ethereum.Here are the rankings for L2:

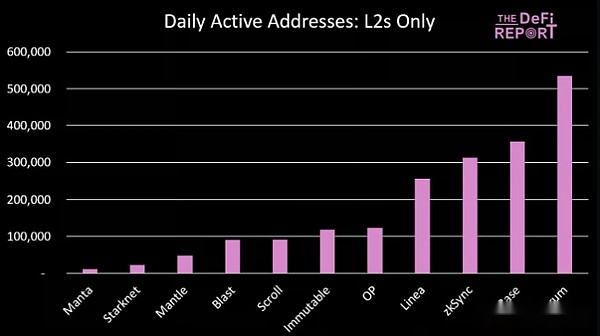

Data: Token Terminal as of June 23, 2024

Arbitrum once again occupies the first place and is the first L2 to surpass Ethereum L1 daily users.

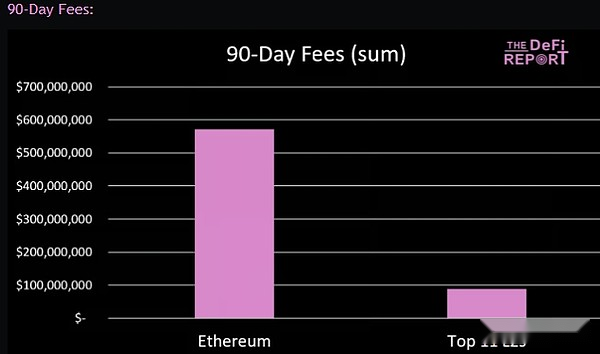

Data: Token Terminal as of June 23, 2024

The first 11 L2 fees account for 15% of Ethereum’s fees charged in the past 90 days.

Let’s take a quick look at the L2 rankings:

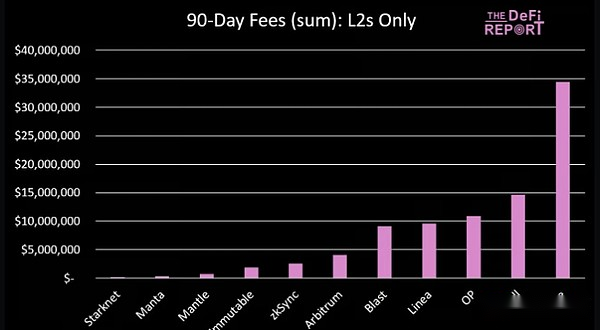

Data: Token Terminal as of June 23, 2024

In the past 90 days, Base’s fees have been more than twice the second-ranked Scroll, accounting for 6% of Ethereum’s total expenses.

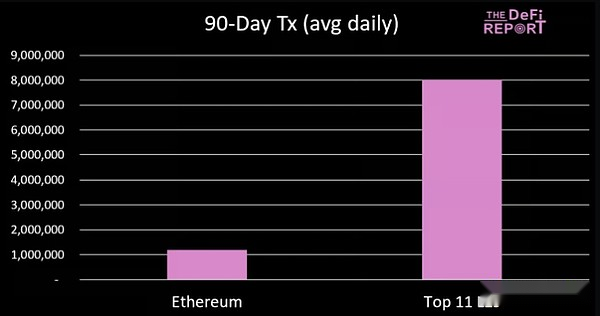

90-day trading volume:

Data: Token Terminal as of June 23, 2024

On average,Compared with Ethereum L1, the top L2 now processes 6.7 times the number of transactions per day.

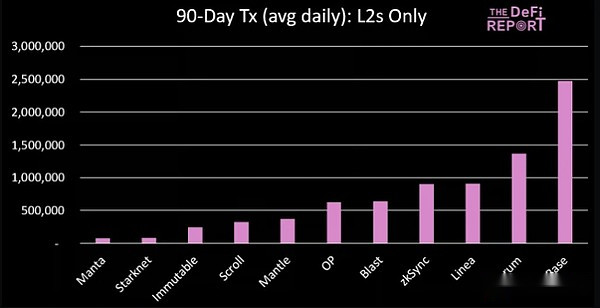

Here is a breakdown of L2:

Data: Token Terminal as of June 23, 2024

Base’s average daily user base is about 66% of Arbitrum.However, Base users trade 6.9 times on Arbitrum every day, compared to just 2.5 times on Arbitrum.

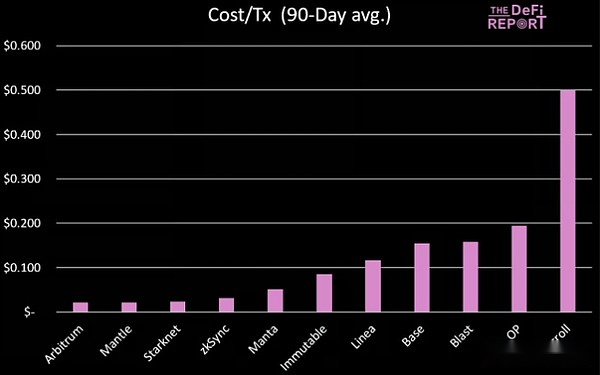

Cost/Transaction:

Data: Token Terminal as of June 23, 2024

Average Cost/Trading reveals why Arbitrum, despite being ranked second in terms of trading, is in the middle: the transaction cost on Arbitrum is $0.02, while the transaction cost on Base is $0.15.For reference, the average transaction fee for Ethereum during the same period was $5.30.

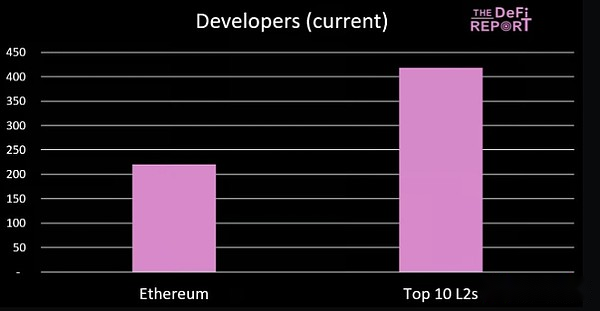

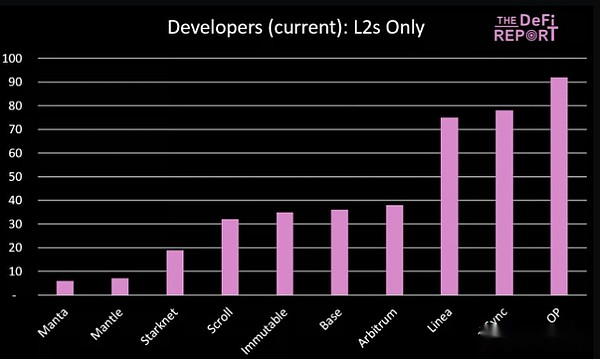

Developer:

Data: Token Terminal as of June 23, 2024

Currently, the number of active core developers at the top L2 is about twice as high as it is now.*Token Terminal defines core developers as the number of different Github users who have made 1+ commits to the project’s public repository in the past 30 days.These numbers do not include ecosystem/application developers.

Let’s see how the L2 compares:

Data: Token Terminal as of June 23, 2024

Here, Optimism first appeared in the No. 1 spot, and today there are more than twice as many active developers on Arbitrum.It’s worth noting that Base is in the middle – which shows that they get more money from developers than their competitors considering the app, users and on-chain fees.

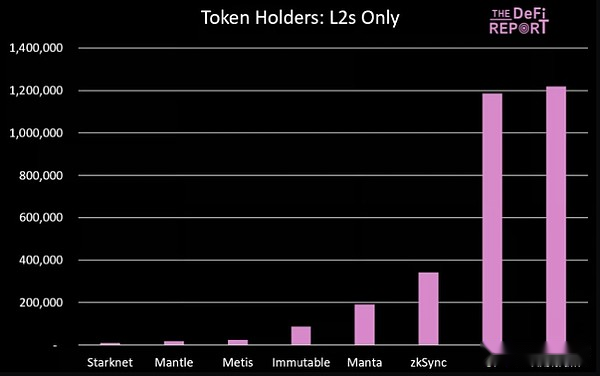

But what do market participants hold?ETH 还是 L2 代币?

数据:Token Terminal 截至2024年6月23日

The L2 portfolio accounts for only 2% of Ethereum’s current token holders (note that the 4 top projects do not have tokens yet: Base, Blast, Linea and Scroll).

Here are the details of the 8 leaders in the market who own tokens:

Data: Token Terminal as of June 23, 2024

In terms of the psychological share of L2 token holders/investors, Optimism and Arbitrum have 80% of the market share, but only 1% of Ethereum L1.

最后,让我们总结一下估值:

数据:Token Terminal 截至2024年6月23日

如上所述,顶级 L2 具有:

-

以太坊 TVL 的 15%;

-

以太坊费用的 15%;

-

活动地址数量的 4.7 倍;

-

6.7 times the number of daily transactions;

-

2 times the number of developers.

only……

-

2.4% token holders;

-

9% of Ethereum’s fully diluted market value;

-

and 2.7% of Ethereum’s market value.

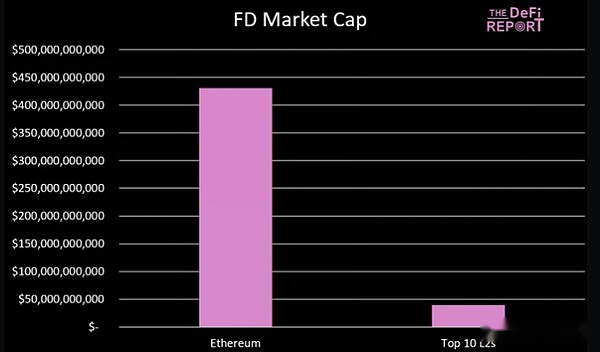

Here is the full dilution market value of the top L2:

Data: Token Terminal

On a complete dilution basis, Arbitrum and Optimism account for 40% of the top 10, accounting for 3.7% of Ethereum’s market value (1.06% of the market value of circulation).

L2 Token Utility/Demand and ETH

Now that we have some data in mind, let’s check the utility and requirements of ETH tokens and L2 tokens.

ETH

Today, ETH has the following purposes:

-

Pay Gas fees (including L2!) on the Ethereum network.If you want to transfer stablecoins, trade on DEX, mint NFTs, play games on chains, get loans, etc., you need some ETH.

-

Collateral to obtain proceeds.Want to get the benefits of the Ethereum network?You need some ETH to do this.

-

Collateral for the loan.Currently, more than 1% (2.3 million) of ETH circulation is locked in MakerDAO smart contracts as collateral for on-chain loans.

-

Transaction medium.Want to buy your favorite NFT on OpenSea?You need some ETH.

-

Real-world assets.Want tokenize assets so they can trade freely around the world?You need some ETH.

-

Deploy smart contracts.Want to build something on Ethereum?You need some ETH.

-

Re-pled.ETH can be used as collateral to get fees directly from Ethereum or from applications and protocols within the Ethereum ecosystem.This is done by “re-staking” ETH.To get this benefit, you need some ETH.

As we have seen, ETH has a rich utility in the Ethereum ecosystem.This utility drives the demand for assets in a way similar to that of petroleum utility driving asset/commodity demand.

For these reasons, we believe ETH is more practical than any other asset in today’s cryptocurrency.

Layer 2 Tokens

Today, Layer 2 tokens are used for…governance.

That’s true.Some networks allow users to pay for Gas fees using L2 tokens, but in most cases, these fees are paid with ETH.

In addition, L2 must pay for block space on Ethereum in ETH (where transactions are settled).

Important: L2 has no utilities or incentive structures to drive demand for today’s tokens.This is true with Ethereum.

L2 Token Value Accumulation and ETH

How does the value of ETH accumulate?Actual income generated through pledge (and re-pled).

How do L2 tokens add value?There is no such value accumulation mechanism today, because user fees are paid to the L2 sorter, not the distributed validator network.

Execution (L2) and Settlement (ETH)

What is more valuable?implement?Or settlement?

First, let’s set the difference between the two horizontally:

-

Execution: A useful analogy might be to consider execution as ordering in a restaurant.你选择你想要的。Communicate with the waiter.The waiter then confirms your order.

-

Settlement: Settlement can be considered as paying bills, receiving receipts, and accounting for transactions.

Today, the relationship between L1 and L2 is like this: the user executes the transaction on L2, and L2 settles the transaction on L1 (for which the fee is paid).

So, what is more valuable?

Some thoughts from the “L2/Execution” camp:

-

In traditional finance, the vast majority of value is attributed to the execution layer of the technology stack—brokers, market makers and high-frequency traders.Settlement produces less value – it can be considered as liquidation/accounting (DTCC).

-

Transaction fees for all blockchains may eventually drop to zero (or close to zero).If that is the case, then MEV will be the way these networks will be monetized in the future.Now.If all executions happen on L2, then this is where we expect MEV to come from—because executions include batching and sorting of transactions.

Some ideas from the Ethereum L1/Close Camp:

-

As far as the Ethereum ecosystem is concerned, there is only 1 settlement layer.Everything at the top end will eventually fall on Ethereum and pay for ETH for it.

-

L2 inherits the security and decentralization of Ethereum.

-

The utility of tokens (and subsequent network effects) may ultimately be the only thing that matters.For example, Ethereum may lose most of its expenses at the L1 level, but can still get cash flow from other applications and protocols that “leased” Ethereum security, including L2 without tokens like Base.

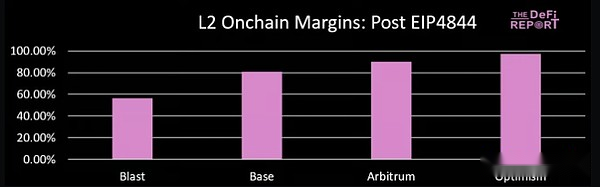

L2 Margin vs ETH

Ethereum’s margin is basically 100%, and it will not change in the future.

Here are the current L2 margins that have increased significantly since EIP4844:

Data: Token Terminal

-

Base has a lower margin as it pays 15% of its total revenue to Optimism.

-

Blast balance is low due to delays in upgrading the network to support EIP4844-related upgrades.Blast margin has increased to 91% since its May 27 upgrade.

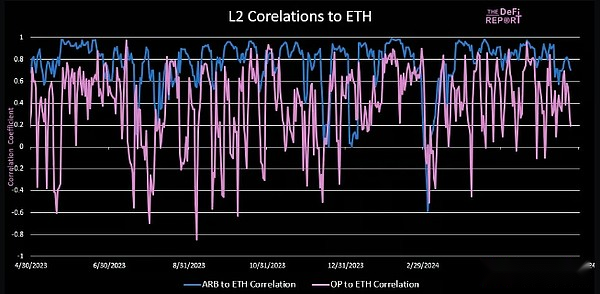

L2 correlation with ETH

ARB & OP Price Exchange ETH

Data: Token Terminal

The historical price correlation coefficient of ARB and ETH is 0.71 (highly correlated).

Similarly, optimism was less correlated with ETH with a historical correlation coefficient of 0.61 (moderate correlation with periods that were completely unrelated to ETH).

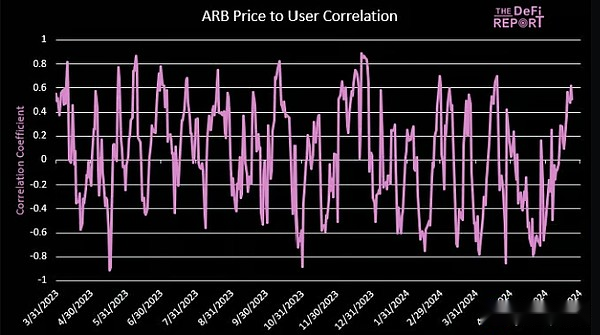

ARB price for users

Data: Token Terminal

The historical correlation coefficient of Arbitrum is -0.009 (negative correlation).This is not a typo.

How to compare the negative correlation between user activities and price?

Token unlock.This is largely due to the lack of regulation in the SEC and Congress.

Please stay tuned and we will cover unlocking in the next section.

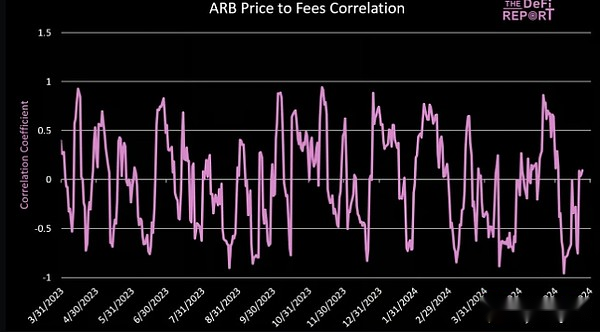

ARB Prices and Fees

Data: Token Terminal

Not surprisingly, the price is also negatively correlated with the expense (historical correlation coefficient is -0.004).You can’t make up for it.

L2 Catalyst and ETH

Ethereum Catalyst

The biggest catalyst for ETH next year is the ETF – it should be traded sometime this summer.Other catalysts include restaking (additional income for ETH holders), tokenization of real-world assets, enterprise adoption, and maturity of DeFi and NFT use cases.

With the approval of the ETF, we expect Wall Street to start doing some real due diligence on networks and assets.We ultimately believe Ethereum has a larger potential market than Bitcoin, so it will be interesting to see if large institutions will eventually come to the same conclusion.

L2 Catalyst

We think there are two potential catalysts for L2 next year.

-

Ethereum price.If ETH outperforms ETFs after ETF approval, we may see some investors jump directly to L2 – seeking to allocate to projects with smaller market caps.

-

L2 is re-rated relative to ETH.Currently, top L2 accounts for only 2.7% of Ethereum’s market value (9% after complete dilution).If the market believes that the ratio should be close to 10%, then L2 may outperform the market.

Token unlock

This is probably the most important part of this report.

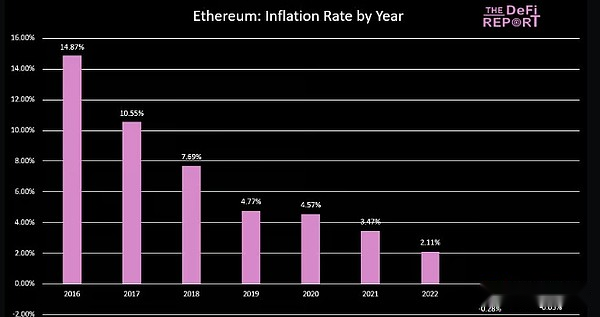

Ethereum does not have any “token unlock” because the supply is fully circulated.Additionally, Ethereum whales, which have obtained large allocations through initial ICOs, have now experienced two bull markets and can sell/recycle their tokens back to the market/newbies.

That being said, Ethereum’s supply may increase during a slowdown in on-chain activity and “fee consumption” is not enough to offset the new issuance/consensus rewards paid for services to incentivize validators.

For reference, Ethereum was deflationary in 2023 (-.28%) and has been deflationary so far in 2024 (-.02%).Here is the inflation rate of Ethereum since its inception:

Data: Etherscan

It is worth noting that as EIP4844 (network upgrade) causes L2 fees to decline, we observe that the “cost burn” speed is slowing down.

In fact, Ethereum’s ETH issuance has increased by 75,951 since March 13, which means approximately 767 new ETHs per day (EIP 4844 implementation).This year, the network’s supply still decreased by 23.3k ETH.But if we don’t see an increase in on-chain activity in the second half of this year, there may be a slight inflation on the Internet this year.

L2 differs in the following factors:

L2 distributes tokens to investors, advisers and contributors, and is usually granted for more than 4 years.

Today, the vast majority of L2 tokens (especially major tokens) do not have a “buyback” or “destroy” mechanism.

The utility of the L2 token is almost zero, so there is no structured purchase support.

As mentioned earlier, we predict a slight deflation on Ethereum this year.

We can compare it with known information related to L2 token unlocking.For example, Arbitrum will unlock 1.15 billion tokens next year (36% inflation of existing supply).

Arbitrum will unlock 3.2 billion tokens in the next three years.Most of these tokens are allocated to investors and contributors who hold a large number of unrealized returns.

We should expect them to be sold at the end of the vesting period – increasing the supply of tokens on the market.

We can see the impact of token unlocking in the figure below.For example, Arbitrum’s unlocking starts in March, and we can see the impact on the price below.This offsets the stunning growth in Arbitrum’s fundamentals (pink represents active user growth).

Data: Token Terminal

Given that Arbitrum will unlock 1.15 billion tokens next year, nearly $1 billion of new funds must enter the asset before it can stay at $0.82 – the same conditions (the price of ARB at the time of writing).

Predicted price

Remember, no matter how much data, vision or luck we have, no one can predict the price.In this section, we are just sharing some high-level forecasts so that we can get back to a reasonable price target.

Data: Token Terminal

*The above prediction assumes that the supply of ETH’s circulating tokens remains unchanged.The supply of BTC is known.So use the actual value and add the inflation for one year.In addition, “BTC dominance” and “ETH as a percentage of BTC MC” are taken from the periodic peaks.

We use our predictions for ETH to return to the potential valuations of the first 2 Layer 2: Arbitrum and Optimism.

Data: Token Terminal

The above data table assumes the following:

In its base case and bear market situation, Arbitrum accounts for 0.62% of ETH’s estimated market capitalization (as it is today).

In a bull market situation, Arbitrum accounts for 1.24% of ETH’s market capitalization (2 times the current one).

In the base case and bear market situation, Optimism accounts for 0.46% of ETH’s estimated market capitalization (as it is today).

In a bull market situation, Optimism accounts for 0.92% of ETH’s estimated market value (2 times the current one).

One year of token unlocking is included in the price/token of each asset.

Betting on Ethereum L2 is essentially a bet on ETH.This is why our predictions first make advanced predictions for ETH.

in conclusion

If you are optimistic about the Ethereum ecosystem, we think you need to emphasize ETH as part of your portfolio.Why?Because too much investment in any L2 can produce negative returns—even if the argument on Ethereum is correct.For this reason, we believe that at least 50% of the Ethereum investment in the liquidity portfolio should be ETH.Please note that this number depends on risk tolerance, goals, investment schedule, etc.

Token unlocking is real.They obviously affect the predicted returns.For example, Arbitrum’s base case is expected to grow its market cap by 315% next year, but the price per token only increases by 210%.It is precisely for this reason, ETH performed better than L2 in basic scenarios and bear market scenarios.

In order for top L2s to outperform ETH, the market needs to reprice based on their percentage of Ethereum’s market capitalization.We saw this last year on Solana – in December 2022, it had a market capitalization of only 2.5% of Ethereum’s market capitalization.This is obviously wrong.Since then, the market has re-tuned Solana’s rating to 15% of Ethereum.

On a complete dilution basis, ARB and OP account for 3.7% of Ethereum’s market value.If you think the top L2 should account for nearly 10% of Ethereum’s market capitalization, this may change your portfolio allocation.Given the lack of practicality, unlocking and competition for the tokens, we don’t think this will happen next year, but it may be re-rated in the long run.