Author: Chris Powers, founder of DOES of Defi, translation: Bitchain Vision Xiaozou

The core base layer has shown a good degree of unblocking. Ethereum once had a single solution to achieve execution, settlement and data availability, but now it has been switched to a more modular method to be the core elements of the blockchain.Provide special solutions.

The same model is also staged in the field of DEFI lending.First of all, those products that succeed are all products that can be self -sufficient.Although there are many excellent places for the first three Defi lending platforms -MakerDao, AAVE, and Compound, they all run in the predefined structure set by their core teams.However, the growth of Defi loan business today comes from a number of new projects that further split the core function of the loan agreement.

These projects are creating an independent market, focusing on minimizing governance, separation risk management, liberating Oracle’s responsibility, and removing other single dependencies.Other companies are developing easy -to -use bundling products to combine multiple DEFI “Lego” to provide more comprehensive borrowing products.

This new measure that unbinds DEFI borrowing is called “modular loan”.In Dose of Defi, we are loyal fans of Meme, but we also see some new projects (and their investors) trying to speculate on the market for new narratives, more for their purse, not because they really have some potential potentialInnovation.

We believe that the hype is real.DeFi借贷将经历与核心基础层类似的蜕变——新的模块化协议出现(如Celestia),而既有老牌公司则改变了他们原来的路线图,朝着更加模块化的方向前进——就像What Ethereum does when he continues to unblocked himself.

In the short term, the main competitors are opening different tracks.Morpho, Euler, Ajna, Credit Guild, and other companies put successful expectations on new modular borrowing projects, while MakerDao turned to less centralized SubDao models.The recently announced AAVE V4 is also developing in the direction of modularity, which reflects that Ethereum’s structure is changing.At present, these development paths are likely to decide where the value accumulation of DEFI borrowing has taken place in the long run.

1. Why is it modularized?

There are usually two methods to build complex systems.One method is to pay attention to the end user experience and ensure that the complexity does not affect the availability.This means to control the entire stack (just like Apple does in hardware and software integration).

Another method focuses on enabling some parties to build some components of the system.In this way, the designer of the complex system focuses on creating the core standards of interoperability and relying on the market to innovate.The core Internet agreement has not changed, and applications and businesses based on TCP/IP have promoted the innovation of the Internet.

This type of ratio is also applicable to economic development. Among them, the government is regarded as the basic layer of TCP/IP. Through the rule of law and social cohesion to ensure interoperability, economic development has subsequently appeared in the private sector based on management.Neither of these methods will always be effective. Many companies, agreements, and economies are weighed these two methods.

2. Key components

Supporters of modular borrowing theory believe that DEFI’s innovation will be driven by the professionalization of each lending component, not just focusing on the end user experience.

One key reason for this idea is to eliminate single dependencies.The borrowing agreement requires close monitoring risks. A small problem may lead to disaster loss, so the establishment of a redundant mechanism is the key.The single lending agreement introduces multiple Oracle to prevent problems in a certain Oracle, but the modular lending method uses this hedging method and applies it to every layer in the lending structure.

For each DEFI loan, we can determine that five key components are required -but can be modified:

-

Loan asset

-

Mortgage asset

-

Oracle

-

Maximum loan value ratio (LTV)

-

Interest rate model

These components must be closely monitored in order to ensure the platform’s solvency and prevent bad debt due to rapid fluctuations in prices (we can also add a clearing system to the above five components).

For AAVE, Maker, and Compound, token governance makes decisions for all assets and users.Initially, all assets were concentrated together to bear the risk of the entire system.However, even the single lending agreement has quickly changed to create an independent market for each asset to distinguish risks.

3. The main modular competitors

The independent market is not the only way to make the lending agreement more modular.Real innovation is taking place in the new agreement, and these agreements redefine the necessary conditions for borrowing.

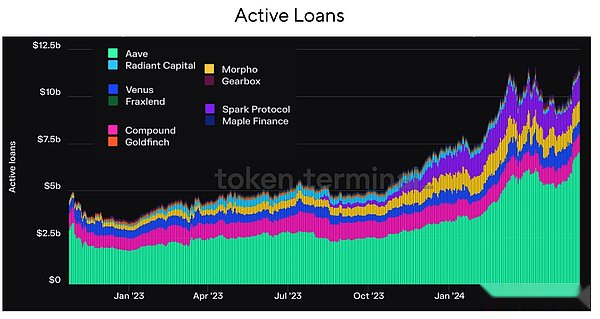

The largest competitors in the field of modularity are Morpho, Euler and Gearbox.

-

Morpho

At present, Morpho is obviously the leader in the field of modular lending. Although Morpho has recently seems not very used to this cause, trying to transform into “neither modular nor monomer, but aggregation.”With a $ 1.8 billion TVL, it can be said that Morpho is at the forefront of the entire DEFI lending industry, but its goal is to become the biggest giant.Morpho Blue is its main borrowing stack. On this basis, it can create a vault without a license and adjust to any parameters it wants.Governance only supports modified parts -currently there are five different components -not to say that these components should be like this.This is configured by the owner of the vault (usually DEFI risk manager).Another main layer of Morpho is Metamorpho, which tries to become a polymerization layer of passive lender.Metamorpho pays special attention to the end user experience.This is similar to UNISWAP with DEX on Ethereum, or Uniswap X for high -efficiency trading paths.

-

Euler

Euler launched the V1 version in 2022. Before the hacking attack consumed almost all the agreement funds (later returned), it had produced an unbounded contract of more than 200 million US dollars.Now, it is preparing to launch its V2 version and re -enter the mature modular borrowing ecosystem as the main competitors.Euler V2 has two key components.One is the EULER VAULT KIT (EVK), which is a framework for creating an ERC4626 compatible vault with additional borrowing functions, enabling these vaults to play the role of passive borrowing pools. The other is Ethereum Vault Connector (EVC). This is a.EVM primitives mainly support multi -vault guarantees, that is, multiple vaults can use a mortgage provided by one vault.V2 is planned to be released in the second or third quarter of this year.

-

Gearbox

Gearbox provides a more user -centric framework, that is, users can easily set their own position without needing too much supervision, no matter how their skills/knowledge level can be set.The main innovation of Gearbox is a “credit account”. As a list of non -prohibited behavior and whitelist assets, the borrowing asset is priced.It is basically an independent lending pool, similar to the EULER vault, but Gearbox’s credit account holds user mortgage and borrowing funds at the same time.Like Metamorpho, Gearbox also proves that the modular world can have a special packaging layer for end users.

4. Unblock, and then bundle it

The professionalization of some lending components provides opportunities to establish an alternative system. These systems may be targeted at specific small -scale markets or bet on future growth.The following are some of the main promoters of this method:

-

Credit guild

Credit Guild wants to catch up with the existing aggregate loan market with a trusted governance model.Existing competitors (such as AAVE) have very strict governance specifications, which often leads to small -scale tokens who lose interest because their voting seems to be influenced.Therefore, a few people who control most tokens are responsible for most changes.Credit Guild reverse this dynamic by introducing a veto -based Optimistic governance framework. This framework specifies the delay of different legal number thresholds and different parameters, and at the same time integrates a risk pursuit method to handle unpredictable consequences.

-

Starport

Starport’s ambition is a bet on cross -chain theory.It implements a very basic framework to combine different types of EVM compatible borrowing agreements.It is designed to implement the terms of data availability and protocols through two core components:

Component 1: Starport contract.The Starport contract is responsible for loan issuance (definition of time limit) and re -financing (term update).It stores these data for protocols based on the Starport kernel and provides these data when needed.

Component 2: Trusted contract.The custody contract mainly holds the mortgage of the original protocol borrower on the Starport, and ensures that the debt settlement and settlement are carried out in accordance with the terms defined by the original protocol, and are stored in the Starport contract.

-

Ajna

AJNA has a non -Oracle aggregation loan model that does not require permission, and has no level of governance.The funding pool has a unique quotation/mortgage asset transaction provided by the lender/borrower, allowing users to evaluate the demand for any kind of assets and allocate funds accordingly.AJNA’s no Oracle design originated from the price of the lender that can designate their willingness to loan, and achieved it by specifying the number of mortgages that borrowers should be mortgaged for each offer token (vice versa).It is particularly attractive to asset long tails (just like Uniswap V2 to small tokens).

5. If you can’t defeat them, join them

The field of lending has attracted a large number of newcomers, which also revives the largest DEFI protocols. These agreements have launched new lending products:

-

AAVE V4

The AAVE V4 released last month is very similar to Euler V2.Earlier, AAVE fanatic supporter Marc “Chainsaw” Zeller said that due to the modular characteristics of AAVE V3, it will become the ultimate state of AAVE.Its soft and clearing mechanism is first created by Llammalend, and its unified liquidity layer is similar to the EVC of Eule V2.Most of the upcoming upgrades are not novel, and they have not performed a large -scale test in a high liquidity protocol (AAVE has been done).We can successfully win market share in each chain, which is too crazy.Its moat may be very shallow, but it is very wide and has a very powerful smooth wind.

-

CURVE

CURVE (also an informal name is Llammalend) is a series of independent one -way one -way (non -loan mortgage) borrowing market. In these markets, CURVE’s native stablecoin CRVUSD (cast) is used as mortgage orDebt assets.This enables it to combine CURVE’s expertise in AMM design to provide unique borrowing market opportunities.In the field of DEFI, Curve’s approach is always unique, but it is feasible for them.Therefore, in addition to Uniswap’s giant, CURVE has opened up an important niche market in the DEX market, and with the success of the VECRV model, everyone will no longer determine their questioning of token economics.LLAMALEND seems to be another chapter of the Curve story:

*The most interesting feature is its risk management and liquidation logic. This logic is based on the Curve Llamma system and supports “soft liquidation”.

*LLAMMA is deployed as a city contract, encouraging arbitrage between isolated borrowing market assets and external markets.

*Just like a concentrated liquidity automatic as a market merchant (CLAMM, Uniswap V3), LLAMMA uniformly distributed the borrower’s mortgage in a series of users designated.Oracle has a big deviation to ensure incentive arbitrage behavior.

*In this way, when the price of mortgage assets falls below the historical band, the system can automatically sell some mortgage assets (soft liquidation) to CRVUSD.This reduces the overall health of the loan, but it is definitely better than the complete liquidation, especially the clear support of long -tail assets.

Since 2019, Michael Egorov, the founder of CURVE, does not agree with the external criticism of their excessive designed remarks.

Both Curve and AAVE are very concerned about the growth of their respective stablecoins.This is a good long -term charging strategy.Both follow the footsteps of MakerDao. MakerDao did not give up DEFI borrowing and split Spark as an independent brand. Even without any native token incentive measures, Spark has achieved considerable success in the past year.But in the long run, stable currency and crazy money printing (credit make people addiction) is a huge opportunity.However, unlike lending, stable coins really require a certain type of chain governance or centralized entity.For CURVE and AAVE, they have the oldest and most active token governance (of course later than MakerDao). This road is good.

The question we can’t answer is what is compound doing?It can be said that it was once a member of the DEFI royal family. It started the summer of Defi and truly established the profit farming Meme.Obviously, regulatory concerns have limited the activity of its core teams and investors, which is why its market share has declined.However, like AAVE’s wide and shallow moat, Compound still has US $ 1 billion of unpaid loans and extensive governance distribution.Just recently, some people outside the Compound Labs team picked up a command stick for developing Compound.We don’t know which market it should pay attention to -maybe it is a large blue -chip market, especially if it can bring some supervision advantages.

6. Value acquisition

The first three Defi lending companies (MAKER, AAVE, and Compound) were adjusting their development strategies to cope with the transformation of modular lending structure.The encrypted mortgage loan business used to be a good business, but when your mortgage is on the chain, as the market becomes more efficient, your profit margin will be compressed.

This does not mean that there is no chance in an efficient market structure, but no one can monopolize their positions and rent.

The new modular market structure provides more ways to acquisition without permission for risk management agencies and risk capitalists.This provides a method that is more capable of sharing risk management, and directly brings better opportunities for end users, because economic losses will cause great damage to the reputation of the treasury managers.

A good example is the GAUNLET-Morpho farce that recently performed in the EZETH decourse incident.

Gauntlet is a mature risk management company, and its running Ezeth vault suffered losses during the decoupling.However, because the risk is highly targeted and an isolated incident, most of the other Metamorpho vault users are not affected, and Gauntlet must provide post -afterwards evaluation and bear responsibility.

The reason for Gauntlet’s initial launch of the vault was that they felt that Morpho’s future prospects were more bright. It can be charged directly on Morpho, better than providing risk management consulting services for AAVE governance (the latter often pays more attention to political factors rather than risk analysis).

Just this week, Paul Frambot, the founder of Morpho, revealed that a smaller risk management company Re7Capital, as the management company of Morpho vault, has an annualized chain of $ 500,000.It is worth noting that Re7Capital also has a great research briefing.Although the scale is not large, it shows how to create financial companies based on DEFI (not just Degen’s farming).This does trigger some long -term regulatory problems, but this is not surprising today’s encryption industry.In addition, this will not prevent risk management companies among the best in the “biggest winner” list of future modular lending tracks in the future.