Source: LD Capital

summary

-

The Chinese market was most worthy of attention last week, with a series of policies/rumors supporting the Chinese stock market and commodity prices, and the RMB also appreciated significantly.This seems to change people’s negative sentiment towards Chinese assets.

-

Global equity funds and emerging market funds had a sharp net inflow last week, with the scale of Chinese equity funds reaching a record high.However, institutions’ positions in Chinese stocks are still relatively low.

-

The fourth quarter GDP data of the United States, manufacturing PMI data, and personal consumption expenditure data were better than expected.But both S&P 500 and U.S. Treasury yields rose slightly, indicating that the market valued economic growth rather than interest rates.

-

Intel’s performance figures exceeded expectations, but the stock suffered a sharp drop, reflecting investors’ picky attitude towards high-valuation stocks.

-

China’s increase in U.S. bond holdings in November may be due to the settlement of Sino-US relations and the rising U.S. bond prices.

-

This week, the financial reports of many US technology giants may increase.In addition, we pay attention to the policy trends of central banks in various countries and the impact of the US government bond issuance plan in the first quarter.

Chinese market

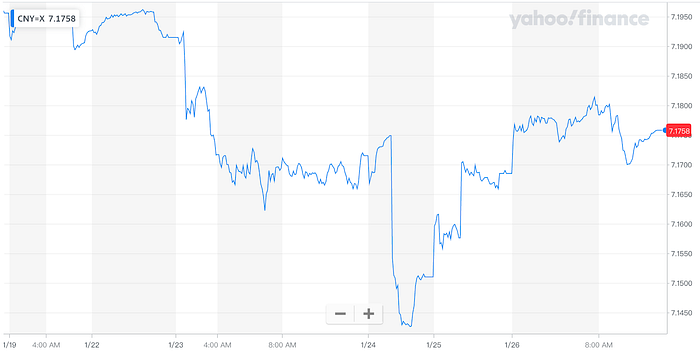

The most noteworthy thing last week was the Chinese market. A series of policies/rumors supported the Chinese stock market and commodity prices. The RMB also appreciated sharply against the US dollar by 500 points in the first half of the week (7.19–7.14 was also the first time it closed higher after three weeks).The sentiment of a bottoming out and rebounding in China is heating up, and the market that has emerged from three consecutive positive trends after a rapid sell-off on the K-line is also a popular bottom pattern for technical analysts.

background:

-

Rumors about a potential 2 trillion stock market bailout plan on Tuesday, if the plan comes true, could change sentiment in the sluggish yuan assets.This fund may use cash deposited by state-owned enterprises overseas, which is equivalent to about 8% of the free-circulating market value of the mainland Chinese stock market.

-

Chinese People’s Bank of China Governor Pan Gongsheng unexpectedly announced on Wednesday that the deposit reserve ratio was cut by 0.5 percentage points on February 5 = RMB 1 trillion in long-term liquidity to the market, and a “targeted interest rate cut” of 25bp.The Governor of the People’s Bank of China suddenly announced major news such as reserve requirement cuts and interest rate cuts at the press conference, and it was released before the closing. It is very rare in China’s financial history, highlighting the continuous sharp drop in China’s assets, and Chinese regulation boosts global investment.Those who are very confident are very urgent.(Since the market has always expected the central bank to cut interest rates, the previous short-term failure caused a “stock stock market crash” and the regulatory pressure is huge,)

-

On Wednesday, the State-owned Assets Supervision and Administration Commission of the State Council stated that it will further study the inclusion of market value management in the performance appraisal of the heads of central enterprises, and guide the heads of central enterprises to pay more attention to the market performance of the listed companies they control.This means that central enterprises’ increased market-oriented operations such as increasing real money and silver, such as repurchase, and dividends, will become a political task, and it is estimated that it will also be transmitted to local listed companies in the future. Against this background, the “Chinese-headed” stocks were launched on Thursday.With the surge in daily limit, companies with high dividends and low valuations have become hot spots for buying.

As the economy and stock markets are in trouble, policy makers have taken a series of actions, but none of them are considered sufficient.Investors who bet on bazooka-style stimulus — as seen during the global financial crisis — have been left out.Measures such as state funds purchasing ETFs, reducing stamp duty on stock transactions, and restricting the listing of new stocks only provide a brief rebound at most.

But authorities have stepped up support recently, and people hope this time may be different.The stock market has risen rarely for three consecutive days this week.This is not the first time that the Chinese government has made a big rescue when the stock market plummeted.In 2015, China also used various state-owned holding funds to invest huge amounts in the stock market, and recently bought Chinese stock ETFs.

Strategy

Regarding investment strategies, in addition to the concept of state-owned enterprises and index concepts, investors in the first category believe that they should stick to sectors such as electric vehicles and semiconductors, because regardless of whether the government introduces large-scale stimulus policies, these industries already have sufficient development potential.

There is also a view that we should go to Hong Kong stocks to get cheaper, where there are more targets that are wrongly killed by emotions. For example, Li Ka-shing’s investment company CK Hutchison is a good example: about half of the company’s revenue comes from Europe, involvingPorts and telecommunications industries.Sales from mainland China and Hong Kong account for only 14% of the company’s total sales, so the downturn in mainland China and Hong Kong’s economy has little impact on the company, and the dividend yield is 7.2%, but Cheung Kong shares are currentlyThe price-to-earnings ratio is only five times.

Continuity

Given that the valuation of China’s stock market is relatively low, the short-term rebound is very reasonable.But whether this rebound can continue ultimately depends on whether the government is willing to boost the real economy through more fiscal and monetary easing policies. Compared with Europe and the United States, we are not just a problem with the tools themselves, but also a problem with the ZZ environment, such as last yearThe central bank is assigned to the Central Financial Commission, weakening the power of government agencies such as the People’s Bank of China and the China Securities Regulatory Commission.So even if you know that only these few moves are available, if your confidence in whether it can be implemented cannot be maintained, the rebound will be very poor.

Now the government has relaxed housing purchase restrictions in some cities and slightly lowered interest rates, but this still disappoints most market participants. A considerable number of people believe that China’s rapid economic slowdown requires strong medicine, just as governments in the pastDo that.But the reasons why senior executives do not want to make strong stimulus are understandable. Although such measures will boost growth, they will also push up debt, promote long-term instability, uneven distribution, slow industrial transformation, sharp depreciation of exchange rates, etc..

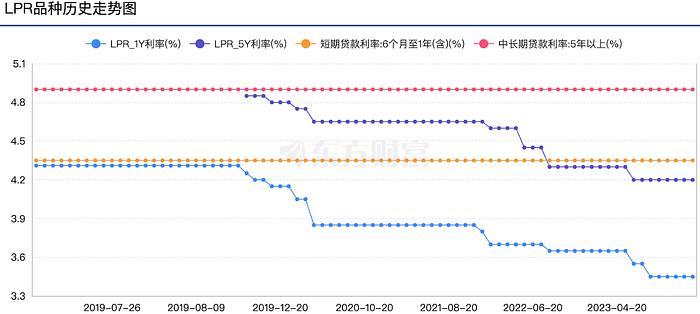

As shown in the figure below, China’s benchmark interest rate LPR has remained unchanged for the fifth consecutive month since September last year, with LPRs of 1-year and 5-year or above respectively at 3.45% and 4.2%, respectively, but China’s CPI is close to 0 or negative, This makes such interest rates very “restrictive”, which is unreasonable for the economic downturn. Compared with countries such as Britain and the United States, interest rates have only been higher than the rise in recent months.

But while the yuan strengthened when it announced a lower RRR (and comments supporting foreign exchange stability), its failure to maintain these gains may be due to increased expectations of further easing in subsequent trading.In general, this is a very interesting game. If a loose monetary policy can lead RMB assets out of the negative cycle, it may not lead to a weakening of the exchange rate:

In the future, my personal view is optimistic, because developed countries have generally ended the interest rate hike cycle. If the interest rate cut cycle is started as early as March, it will leave room for China to implement more easing measures.

US Market

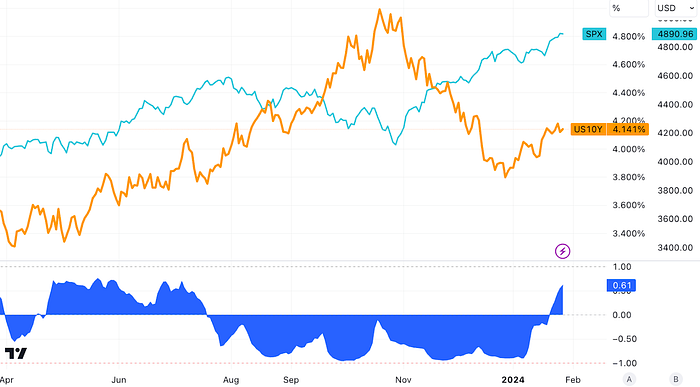

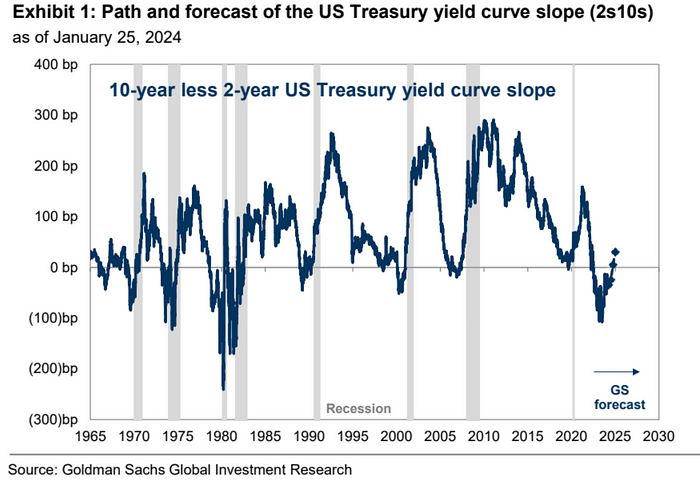

Last week, there was a much stronger-than-expected fourth-quarter GDP figure (3.3%), while personal consumption expenditure (PCE) weakened (core 3M 2%, overall 3M 1.7%), the number of initial jobless claims rose more than expected, and durable goods data was lower thanIt is expected that the manufacturing PMI will return to above 50 (the weakest link has also resumed expansion), and the result is that the US dollar has strengthened slightly, with the yield on 10 US Treasury first falling and then rising basically flat, with the short-term yield dropping even more, 2–10 The interest rate spread inversion has narrowed from the highest 1% last year to 0.21%, and the “normalization” of the yield curve has become a hot topic in the market.

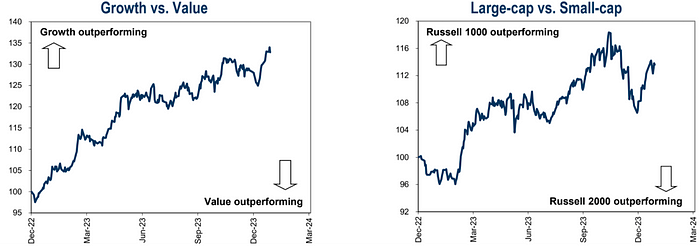

The S&P 500 continued to hit record highs last week, with 10-year U.S. Treasury yields almost sideways around 4.14.10Y opened at 3.87% this year and SPX also rose 2.4% this year, despite higher yields.The reversal of interest rates and stocks is the first time in half a year. This situation shows that the market is now focusing more on growth than interest rates:

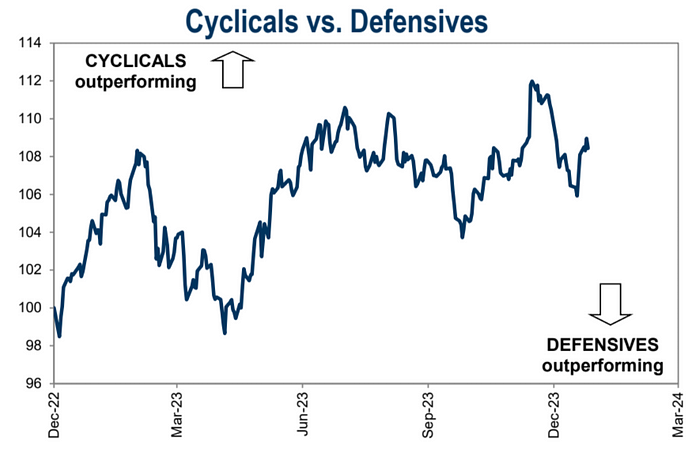

The US stock market has been positive in the past two weeks, and is trending towards cyclical, growth, and market:

There are some voices in the market recently discussing how the normalization of the yield curve affects stocks, especially given the recent negative correlation between stocks and bond yields.However, the impact of economic growth on stock returns is more important than the movement of the earnings curve.In times of strong economic growth, stocks usually get the maximum returns regardless of whether the earnings curve is steep or flat.As long as the U.S. economy avoids recession, even the normalized return curve will bring positive returns.

Goldman Sachs currently expects the Federal Reserve to implement 25 basis points interest rate cuts five times this year, with the 2-year yield dropping to 3.7% by the end of the year, and the 10-year term will remain at the current level of 4.0% by the end of 2024. If it comes true, the interest rate curve will beIt will resume normalization, and on this basis, if bond longs are more certain in short-term bond categories.

Bank of America strategy says any decline in U.S. bonds is a buying opportunity, and recommends increasing duration when the 10-year Treasury yield exceeds 4.1–4.15%, while reducing holdings when the interest rate is around 3.85–3.9%..

In terms of celebrity companies, Intel’s performance figures exceeded expectations, but its first-quarter performance guidance was far inferior to analysts’ expectations, especially the highly-watched data center business, which showed that Intel was unable to defend its position as the top leader in the industry.Poor financial forecasts led to Intel’s fall of more than 10% after the market on Thursday, which also indirectly reflects investors’ picky attitude in front of high-valuation companies:

Specifically:

Earnings per share was $0.63, higher than expected $0.45

Revenues of $15.41 billion, exceeding expectations of $15.17 billion

Adjusted operating income was $2.58 billion, higher than expected $2.1 billion

Adjusted operating margin was 16.7%, exceeding expectations of 13.9%

Adjusted gross profit margin is 48.8%, which is also exceeding expectations by 46.5%.

However, Intel expects revenue range of $12.2 billion to $13.2 billion in the first quarter, far less than analysts’ average forecast of $14.25 billion.Adjusted earnings per share are expected to be 13 cents in the first quarter, less than analysts’ estimates of 34 cents.

Intel expects gross margin to be 44.5% in the first quarter, slightly below analysts’ expectations of 45.5%, showing inefficient efficiency at Intel’s chip factory.By comparison, before 2019, Intel’s gross profit margin often exceeded 60%.

China increases its holdings of U.S. bonds

The US Treasury Department released the International Capital Flows Report (TIC) for November 2023, showing that as of the end of November 2023, China’s holdings of US dollars reached US$782 billion, an increase of US$12.4 billion from October.This means that China has ended its seven consecutive months of selling U.S. bonds, bringing the total holdings of U.S. bonds back from its lowest value since May 2009.

In the view of industry insiders, China’s increase in U.S. bond holdings may be affected by two major factors. First, the meeting between Chinese and US heads of state that month improved Sino-US relations, and second, the Federal Reserve issued a clear signal to end the interest rate hike cycle in November 2023.The yield on US Treasury fell sharply (US Treasury prices rose), attracting many countries to buy US Treasury bonds at the bottom to make profits.

It is worth noting that TIC data shows that among the top ten holding U.S. bonds, except for the Cayman Islands who reduced their holdings of U.S. bonds in November 2023, other countries and regions have chosen to increase their holdings of U.S. bonds.

The financial market generally believes that the end of the Federal Reserve’s interest rate hike cycle may become the most important driving force for many countries to increase their holdings of US bonds.

Fund flow

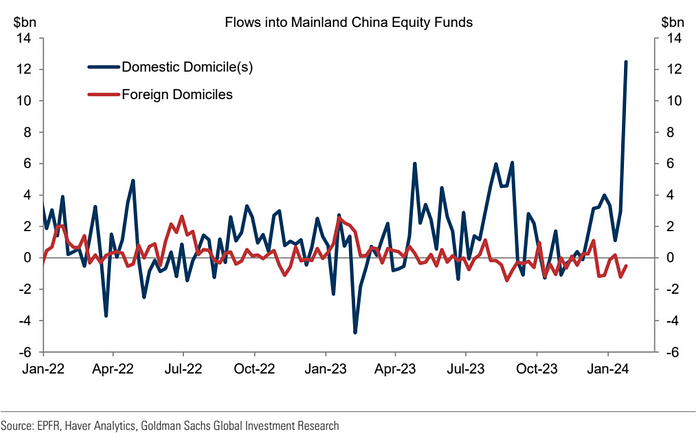

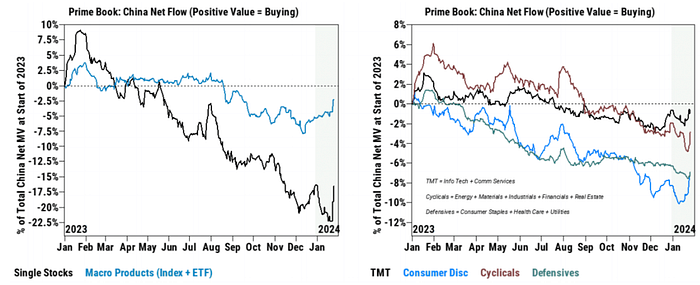

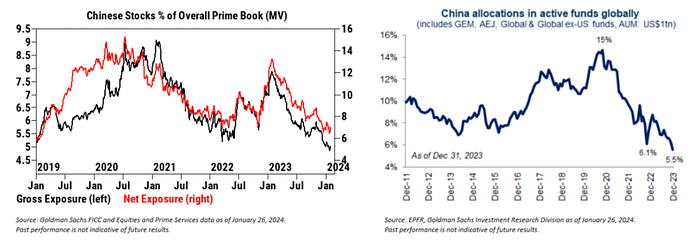

Net inflows from global equity funds have performed strongly in the week ending January 24 (up $18 billion compared to the previous week, compared to negative $900 million in the previous week), according to EPFR data.U.S. equity funds continue to drive net positive inflows to G10 equity funds.In emerging markets, capital inflows to mainland China have reached historical levels, with a total of approximately US$12 billion, the largest weekly capital inflow since 2015.It is worth noting that these inflows are almost entirely driven by domestic investors, suggesting support from the “national team”:

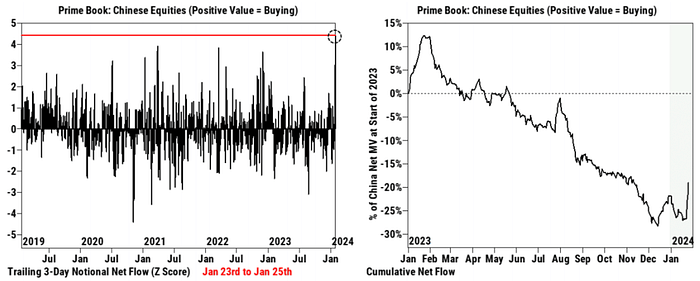

According to Goldman Sachs’ customer data, a large-scale net buy in Chinese stocks appeared on Tuesday, with net buys of Chinese stocks continuing to see on the Prime book on Wednesday and Thursday, despite buying at nominal value.The pace slowed down compared to Tuesday.From January 23 to January 25, the cumulative net purchases of Chinese stocks exceeded the value (+4.4 Z score) for any consecutive three-day period in the past five years, driven by multi-party purchases.

More than 70% of net buying activity recently was driven by individual stocks, which suggests that it may have sustainability.All 11 Chinese industries saw net buys Tuesday to Thursday, dominated by consumer durable goods, industry, communications services and finance.

Overall, both hedge funds and mutual funds, their overall positions in the Chinese stock market are still at very low levels.Despite recent net buying, the total and net allocation of Chinese stocks on Goldman Sachs Primebook are both at lows in nearly five years.Meanwhile, according to EPFR data, global mutual funds allocated 5.5% to China by the end of 2023, the lowest level in the past decade.

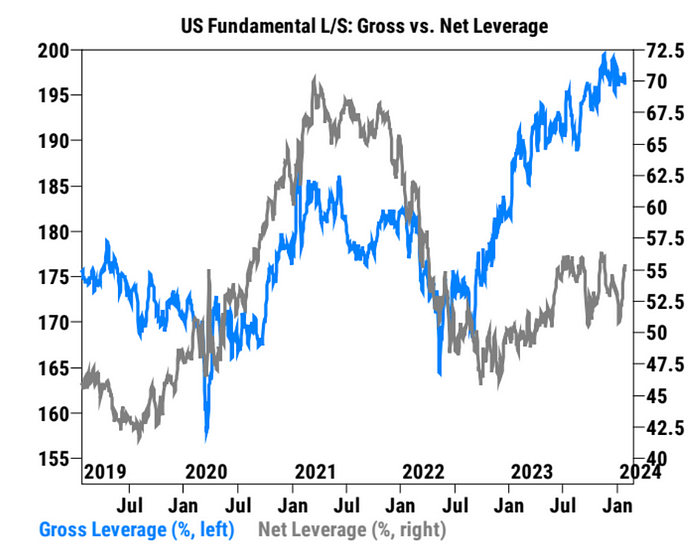

Goldman Sachs customers’ net leverage ratio has risen rapidly in the US stock market

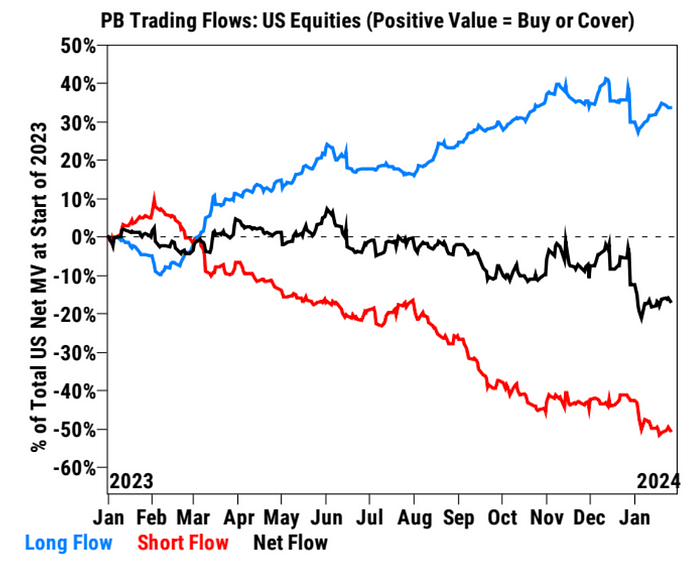

There is little change in capital flow:

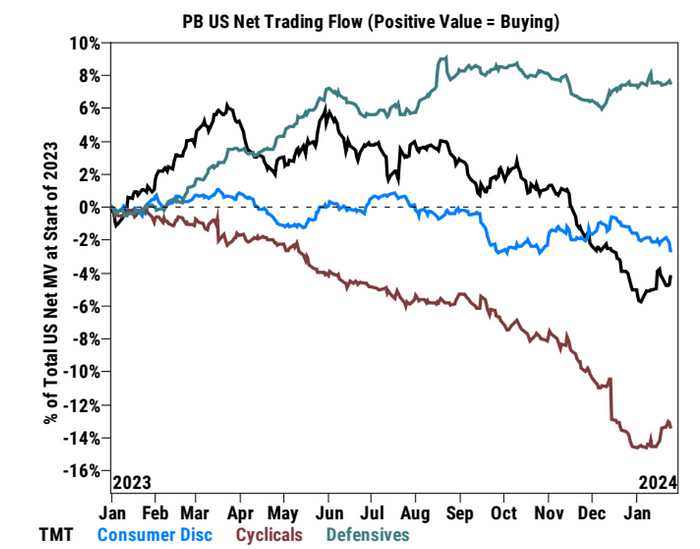

Disposable consumption flows out of funds by industry, inflows into TMT and cycles:

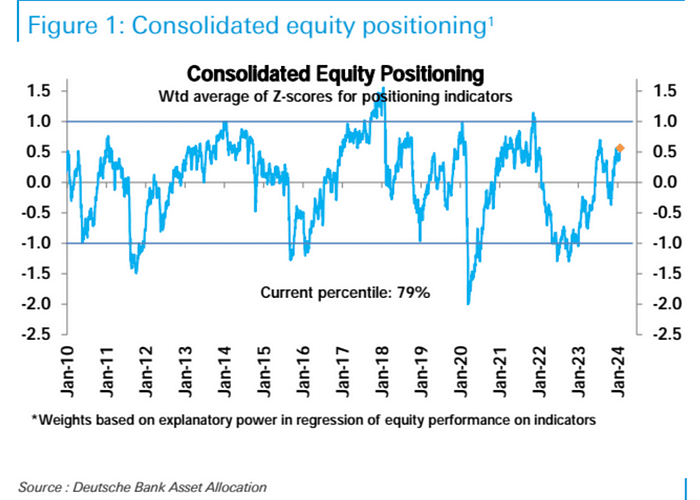

Under Deutsche Bank’s statistical caliber, the overall stock position level rose sharply last week to its highest level in six months (79 percentile), after it had been fluctuating in a narrow range since mid-December.Although the position is obviously high, it has not reached an extreme level.

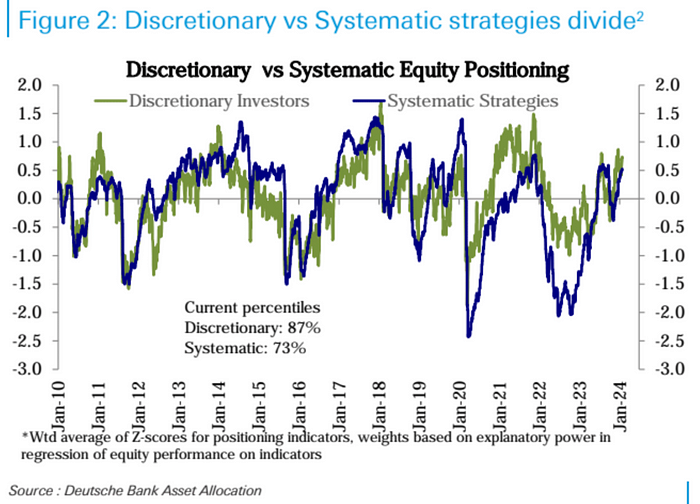

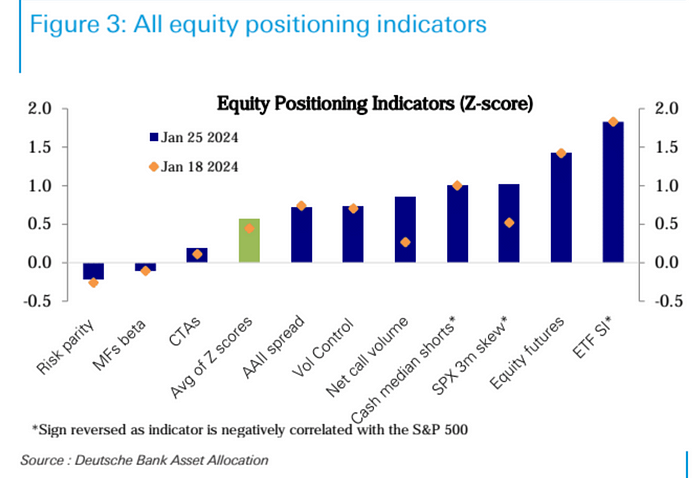

By investor type, subjective investor positions have risen significantly recently, and they have risen to the 87 percentile, while the position of systematic strategies continues to steadily climb to the 73 percentile.Among all industries, the position in the technology industry (ranked 73rd percentile) has risen further and is the only industry that significantly exceeds the historical average.

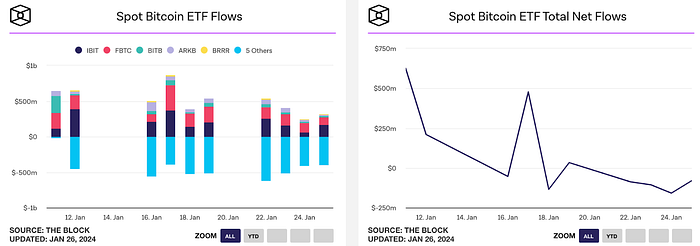

Bitcoin spot ETFs were in a net outflow every day last week, with funds such as BlackRock IBIT and Fidelity FBTC failing to keep up with the market exiting Grayscale GBTC, with a total net inflow of 8 in the two weeks since its listing.About US$17,000 to 20,000 BTC. Considering the selling pressure of GBTC, there is still an inflow of 800 million. This is a very positive signal. The price of BTC also rose by 5% last week:

Market sentiment

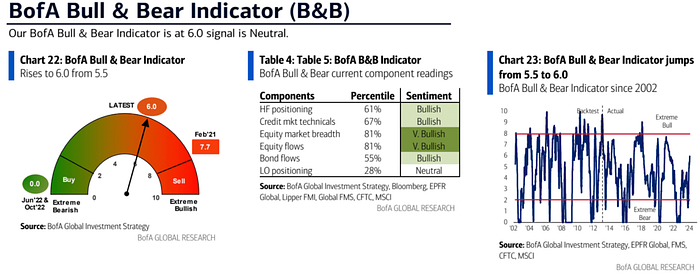

Bank of America Bull and Bear Index: Rised from 5.5 to 6.0, the highest since July 2021, due to large inflows of stocks, strong stock market breadth (7% to 44%) and strong credit markets.

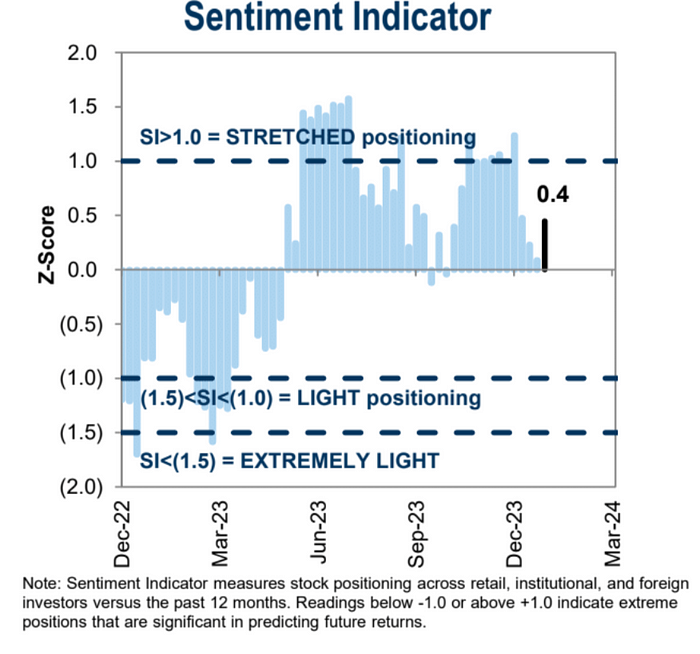

Goldman Sachs’ institutional sentiment rose again after falling back for three consecutive weeks:

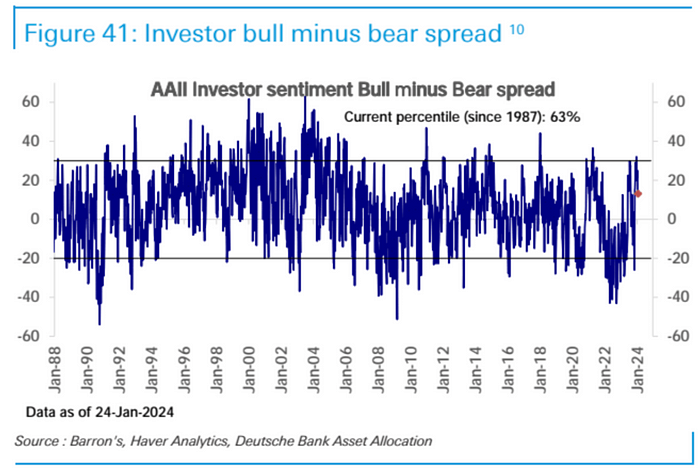

The AAII Bull and Bear Difference fell from the extreme value:

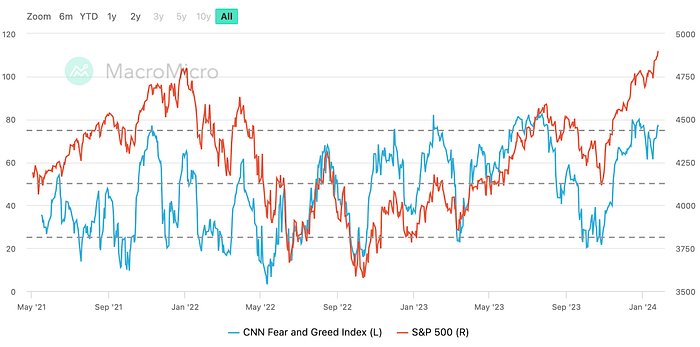

CNN Fear Greed Index returns to the “Extreme Greed” range:

Follow this week

Financial Report

32% of the S&P 500 companies will release financial reports this week, and investors will pay attention to which companies AI has brought actual benefits, including AMD, Alphabet, Microsoft (Tuesday), and Meta, Amazon and Apple (Tuesday).Volatility is bound to increase, and INTEL’s diving has shown us how picky investors are now.

Central Bank

This week, the Federal Reserve will announce its resolution on Wednesday, while the Bank of England and Sweden will announce its resolution on Thursday.On Tuesday, the Bank of Japan will also release a summary of its opinions for this week’s meeting.

Given that the 3- and 6-month annualized inflation is already below the 2% target, the central bank may also remove some dovish words (inflation is close to the target) by removing some hawkish words from the statement.Acknowledge this progress.

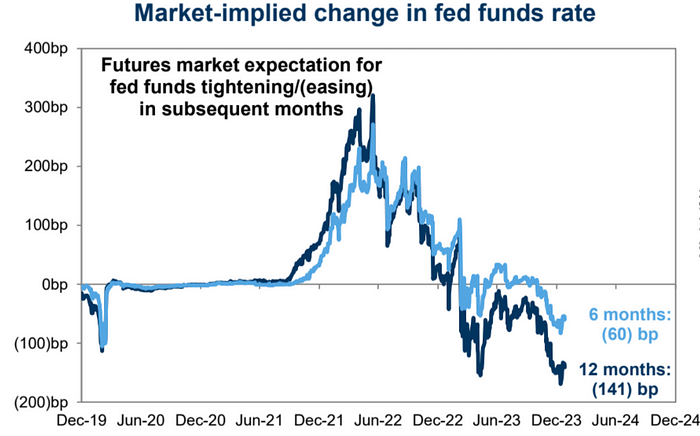

At the press conference, Powell is likely to be asked whether he will cut interest rates in March, and then see if he can answer this question clearly. If he flatly refuses (the probability of looking while walking is greater) it may suppress the market.Also, they may be asked about the substantial easing of financial conditions, the decline in inflation and changes in QT policies since the December meeting, paying particular attention to whether the expectations of QT cuts will be confirmed by Powell – that is, officials are not just “talking” butIn “making a plan”, it takes at least 2 meetings to be released based on history, and the balance of the RRP tool may be exhausted in March.

Overall, the current expectations for interest rate cuts are somewhat divided. Economists’ survey believes it is a rate cut in June and market pricing is March. FOMC may need to make some efforts to “only” hawks who cut interest rates “only” three times at the December meeting.The tendency changes to a situation that is more consistent with market expectations, otherwise the market may take this opportunity to expect it through a pullback.

Although foreign exchange and interest rate market prices have been adjusted in recent weeks except for the stock market, the risks are still biased towards overpricing:

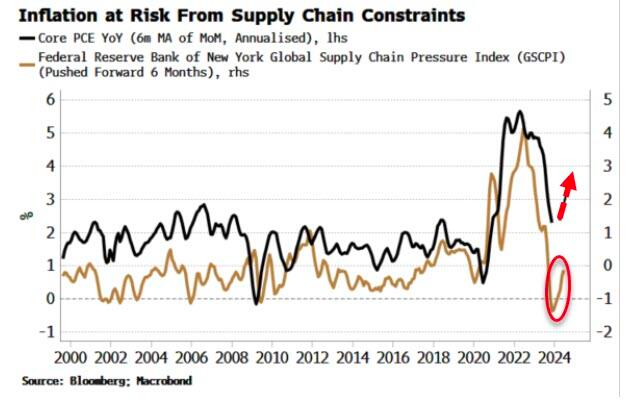

In addition, it is the leading indicator for rising prices – supply chain cost pressure has continued to rise, which is ahead of annualized core PCE for about six months. If China can also start to recover, the pressure on supply chain prices will only be greater, inflation will be carried out later this year.The shadow of the counterattack still exists, and Bloomberg strategist Simon White wrote that “PCE may justify the Fed’s rate cut in March, but it will be stupid.”

The strengthening of US dollar and US Treasury yields so far this year is mainly due to the overconfidence of the market in the last month of last year and the Fed finally confirmed its own turn, and some selling facts appeared in the market.This adjustment trend may still be possible this week, as it seems that the attitudes of FOMC officials have not yet progressed like market pricing.In addition, the US data continues to lead other developed countries, which means that the market is likely to be unable to infer a clearer tendency to easing like the ECB, and the US dollar still has no opponent that can stand out.

Non-agricultural

Friday’s US January non-farm employment report is not about the latest employment figures, and the impact of seasonal adjustments on the market may be greater, as past numbers have been significantly revised downwards.

Ministry of Finance’s bond issuance plan

The Treasury Department will release its financing estimates for the next two quarters on Monday and provide details on the auction scale on Wednesday.The Treasury Department’s own forecast for the last quarter was 816 billion yuan, Bank of America estimated the net borrowing scale of US$970 billion, and Deutsche Bank estimated the project to be 797 billion yuan.If the debt supply figure needs to exceed $1 trillion, it will have an impact on the rising momentum of U.S. Treasury bonds.The U.S. Treasury Department’s quarterly refinancing report has attracted much attention since the government announced higher-than-expected borrowing demand in the third quarter, triggering a sell-off in Treasury bonds.

However, the results of the US bond auction in the past two weeks were unexpectedly good. After the last over-issuance won widespread criticism, the Ministry of Finance also expressed its full understanding of the market’s concerns about the additional issuance and is willing to take action to appease the market. In this auction plan, the Ministry of Finance also expressed its full understanding of the market’s concerns about the additional issuance.There is little chance of any supply accident.Some analysts expect that the Ministry of Finance may announce the launch of a repurchase plan this time, involving the repurchase of debts with less liquidity and the issuance of current bonds with the strongest liquidity, aiming to improve market liquidity.In addition, we should pay attention to whether this additional issuance is more inclined to short-term treasury bond issuance rather than long-term, because the long-term treasury bond market currently performs relatively poorly.