Text: GrayScale Research, Translation: Bit Chain Vision Xiaozou

summary

· In the field of encryption in the smart contract platform, value accumulation is a flywheel that connects fees and network usage with the security and decentralized characteristics of the network.

· The network in the field of encryption in the intelligent contract platform takes various methods to compete for expenses: some platforms seek expenses with relatively high transaction costs, while others are trying to obtain from relatively low transaction costs to obtain to obtain relatively low transaction costs.More transaction volume.

· Grayscale Research believes that costs can be regarded as the main driving factor for the accumulation of token value in this market segment, but other basic factors are also important because they will affect expenses over time.

· Although the industry leader Ethereum has accumulated a few years of network expenses (more than 2 billion US dollars in 2023), other smart contract platforms (such as Solana) have also revealed mature development (the cost of expenses so far from 2024 is approximately about the approximately approximate$ 200 million).

One general misunderstanding is that people think that crypto assets have no basic value and cannot be analyzed like traditional investment.GrayScale ResearchThink of this.For example, smart contract platforms like Ethereum and Solana generate costs and benefits from their own economic activities.GrayScale Research believes that a way for investors to conduct asset valuations in the field of smart contract platforms is to analyze their revenue capabilities by analyzing their costs over time.

1, Basic aspects of smart contract platforms

Smart contract platforms like Ethereum and Solana are the networks that support developers to build decentralized applications, involving various applications from games to finance to NFT.The role of the intelligent contract chain is to handle the transactions of the application it served in a safe and anti -examination manner.

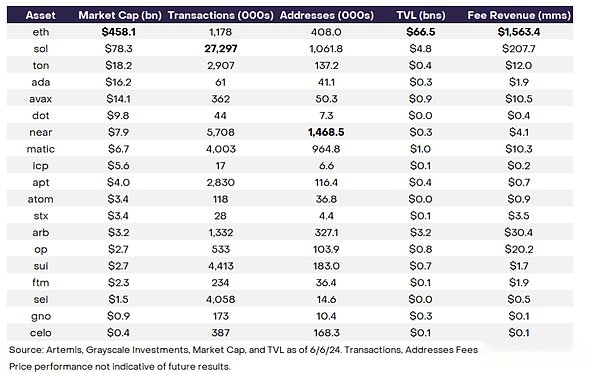

Therefore, the value of the smart contract platform is essentially related to its activities on the Internet.The key indicators of network activities include the number of transactions that can be processed by the network, the number of supportable users (usually measured by the daily active address), the supportable asset value -that is, the total lock value (TVL), and the currency of the block space of the network.The ability, or online costs -will be introduced in detail later.

Each indicator tells a story.For example, Ethereum’s leading position on TVL indicators (66 billion US dollars, more than 7 times larger than TVL’s second largest competitors) reflects its liquidity advantage and value proposition in financial applications.In addition, its advantages in the total number of ecosystem applications have created network effects and constantly attract new developers, applications and users.At the same time, the number of daily transactions of Solana -reflecting its throughput advantages and low cost -make the chain more suitable for high transaction volume like DEPIN, as well as retail -friendly use cases such as NFT and MEME coins.

In addition to comparing these basic indicators between various assets, investors can also put these data in the background of the market value, or the market’s current valuation of specific assets.For example, as shown in the figure below, although Solana’s TVL (US $ 4.7 billion) is currently higher than Arbitrum (US $ 3.2 billion), the market value of Arbitrum is far lower than that of Solana (16 times).These indicators not only allow investors to understand the relative advantages and disadvantages of different assets, but also help them discover value.

Figure 1: Fundamentals of smart contract platforms

(Rough body indicates the largest fundamental indicator of the same kind)

>

2The core role of cost

Although there are many different ways to measure network activities, the most important basic variables of the most important valuation of the smart contract platform are theoretically network expense income (see the figure below).This indicator can be considered as the total cost paid by users to use the network.The smart contract platform has many different benefits models, but in the end it will incur expenses to provide value to token holders.

Similar to the centralized entity in traditional industries, decentralized networks also use different ways to compete for expenses.For example, some smart contract platforms seek expenses for relatively high transaction costs, while other platforms try to obtain more transaction volume at a relatively low transaction cost.These two methods are effective methods.Let’s assume that there are two blockchains as follows:

chain1: The number of users and transactions is small, and the cost of each transaction is higher

5User,10Pen transaction, each transaction fee10Dollar

Network expenses= 100Dollar

chain2: The number of users and transactions is large, and the cost of each transaction is low

100User,100Pen transaction, each transaction1Dollar

Network expenses= 100Dollar

The above example shows that although Chain 2 has more users and transactions, the network costs generated by the two chains are the same.Although indicators such as users and transactions are also important, they need to be considered comprehensive with transaction costs because these will determine the cost.

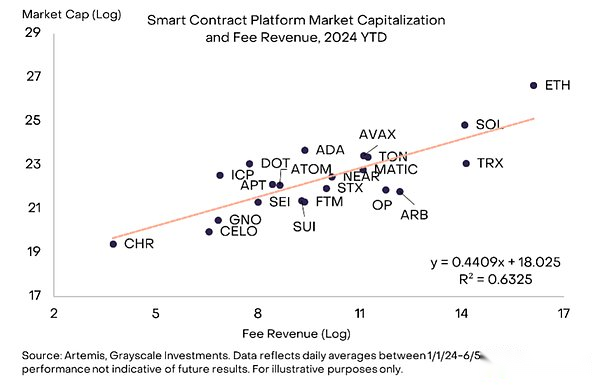

The importance of expenses and income is theoretically established in terms of experience and theoretically.For example, the figure below shows the relationship between the costs and market value of our smart contract platform encryption.Despite the increasingly developing encryption market, investors have distinguished different projects according to their fundamentals.The analysis of GrayScale Research shows that over time, the relationship between cost returns and market value is relatively stable. Compared with other indicators of the smart contract platform, the correlation between cost returns and market value is greater.

Figure 2: The most closely correlated with the market value of the network fee is the most closely related to the market value

>

GrayScale Research believes that a part of the close relationship between the cost and the market value is that the accumulation of network expenses is crucial because of the accumulation of tokens.Value accumulation means that the agreement builds its tokens in a way that connects the network activity with the long -term sustainable value of the token.You can see the accumulation of value at different stages through the following three examples: Ethereum, Solana, and Near.

(1) Ethereum: Value accumulated“Premium chain“

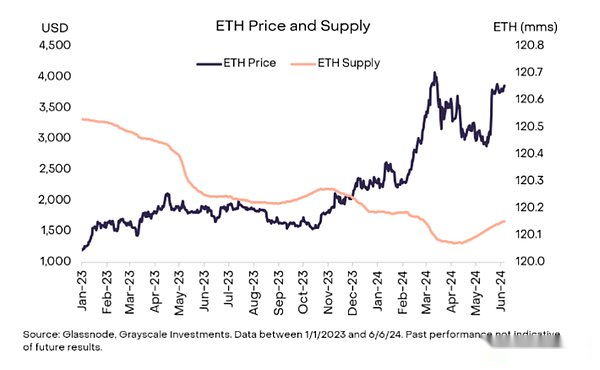

Based on the market value, the first and the largest smart contract blockchain Ethereum has faced serious expansion problems since 2022.The increase in usage has led to network congestion, which makes users’ transactions expensive: its average daily network cost reached a high point of $ 200 per transaction on May 1, 2022.

However, the increase in usage and high average transaction costs have also been converted into significant value accumulation. Ethereum generated a total network cost of more than 2 billion US dollars in 2023.Ethereum network’s network cost income consists of two parts: basic and tip.Whenever the user pays the transaction fee, the basic fee will be burned (burned, destroyed), thereby removing ETH supply from the network.At the same time, the tips paid for the transaction will be distributed as a reward to the verificationrs and pledges who help protect the network security.

Therefore, in 2023, a large number of Ethereum network revenue caused about 2 million ETH to be burned (accounting for 1.7%of the supply), which accumulated value for ETH holders and provided a reward of 390 million US dollars for verificationrs and pledges.This inspires higher levels of network security.

Ethereum has reached a mature stage, and it has proven its ability to create value accumulation.On the Ethereum main network, users pay a premium for high -quality products -in this case, block space is supported by smart contract platforms with the largest network security.This is particularly important for applications involving a large amount of transaction value and priority considering network security, such as stable currency or token -based financial assets.Its user monetization ability is quite mature. This is reflected in its valuation of $ 458 billion (as of June 6, 2024), which is almost six times that of other smart contract platforms.

Figure 3: The increase in network usage (reflected in the period when the supply consumption is large) is often corresponding to higher valuation

>

(2.Solana: Value accumulation“High -performance chain“

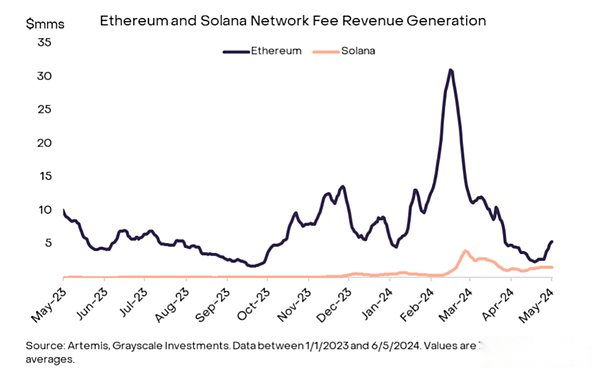

Although Ethereum has a cost -benefit acquisition model, Solana has adopted another method that has recently narrowed the gap with market leaders and made significant progress.Solana is the second largest smart contract platform in market value. It has been considered to be a faster and cheaper alternative solution for Ethereum for a long time. It has an impressive transaction processing speed (335 transactions per second) and low cost (averageEach transaction fee is $ 0.04).However, in the past few years, Solana could not transform these into expenses.In 2023, although Solana’s transaction volume is obviously more transaction volume, it only generates1300Ten thousand dollars of network expenses, and Ethereum’s network expense income is20$ 100 million (less than 154 times).

In the past, the lack of value accumulation mechanism was the relative disadvantage of Solana. However, in 2024, this situation changed.So far this year, Solana’s costs have been 6 times the whole year of 2023, which reduces the cost gap between Ethereum and Solana from 154 times in 2023 to 16 times (shown in the figure below).This shows that the Solana model -low transaction cost and high throughput -also help create economic value.

Figure 4: Solana has begun to accumulate value by calculating the value

>

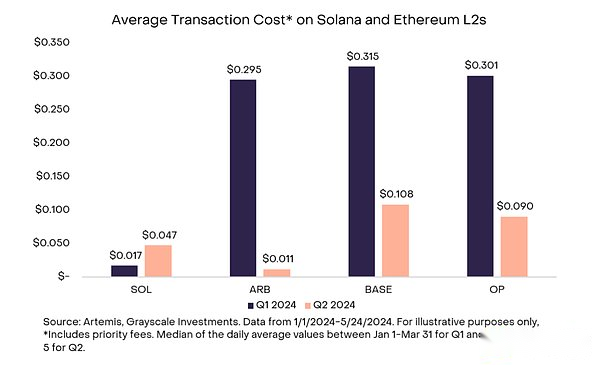

It is worth noting that the significant growth of this cost and profit is consistent with the significant growth of the market value.The significant growth of network expenses is mainly due to the significant increase in the average transaction costs (an increase of 37 times compared to last year), rather than the overall growth of the transaction (only 33%compared with last year).Ironically, the average cost of blockchain, which is traditionally known as the “cheap options”, has increased, which coincides with the Ethereum L2 transaction fee decreased due to the upgrade of Dencun (see the figure below).Since April 1, the average transaction fee ($ 0.04) of Solana users is still lower than that of Ethereum ($ 4.80), but it is higher than Arbitrum (US $ 0.01).

Figure 5: ETH’s Dencun upgrade makes Layer 2 cheaper; increased costs help solana achieve value accumulation

>

Because each transaction fee of Solana is more expensive for its users than Ethereum L2 Arbitrum, it may endanger its positioning as a cheap and high throughput chain.Nevertheless, GrayScale Research believes that in general, this cost growth is good and harmless, because it reflects both high -level user activities, but also shows the value of the pledgee and token holders.

(3.Near: Getting startedCryptoIt has been practically adopted, but it is still in the early stage in terms of network monetization

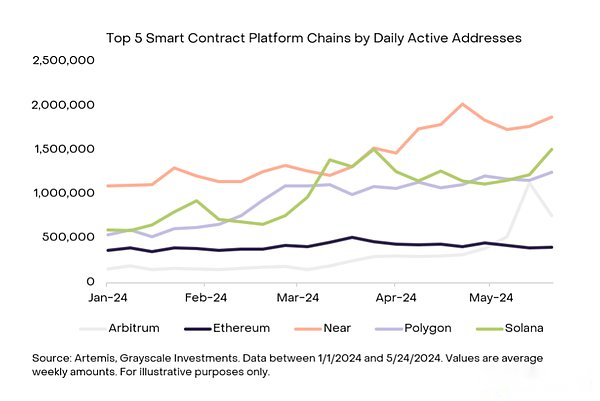

The above two examples are in sharp contrast to the smart contract platform Near. The platform has recently obtained a large number of adoption through non -commissioning cases, but it has not yet shown its value accumulation capacity.Near is the underlying platform of Kaikai and Hot Protocol. Kaikai and Hot Protocol are the two largest decentralized applications (DAPPs) for all users in the encryption field.NEAR leads all smart contract platforms with 1.4 million daily active users, and in terms of throughput, the fastest chain in industries such as Solana can be higher (see the figure below).

Figure 6: Near leads all smart contract platforms in daily active users

>

Although the number of users is in a leading position, Near is still far behind competitors in terms of monetization. The cost and return so far this year is only $ 4.1 million.This shows that it is currently in a relatively mature stage of development, which is also reflected in its valuation relative to competitors (the market value is US $ 7.9 billion, Ethereum is $ 458 billion, and Solana is US $ 78 billion).Although the Near network has shown high -speed processing capabilities, it has not currently provided cumulative value to token holders or pledges.

Although Near’s profitability has been relatively weak so far, it is an important starting point.If the network can continue to expand the network or increase the average transaction fee (similar to the recent progress of Solana) without reducing network activities, it can achieve meaningful value accumulation.

Each of these three smart contract platforms -Ethereum, Solana and Near — each of each of them represents different maturity stages of decentralized networks to create network expenses.Ethereum has many years of revenue and growth.Solana has a powerful user base, but has just begun to generate considerable returns.In the end, Near’s products have shown attractiveness, partly because of their low cost, but they have not obtained considerable returns.

3Precautions and minor understanding of expenses and valuations

To be sure, there are many precautions and minor differences in the costs and valuations in the encryption field of smart contract platforms.First, each protocol involves different forms of value accumulation and different token distribution rates (inflation rates) and tokens (shrinkage rates).For tokens with higher inflation rates, the impact of cost accumulation may be greatly diluted by the distribution of tokens.Each agreement has its own charging structure.On Ethereum, the transaction fee promotes the tokens to benefit all tokens, and the priority fee is assigned to the verificationrs and pledges.On Solana, the distribution method is different: 50%of the transaction fee is burned, and the remaining 50%of the pledgers are owned.Recently, a governance vote decision, all the priority fees of Solana will be paid directly to the verifications.These measures reflect Solana’s greater verification hardware demand.In addition, the high -level MEV activity on Solana provides additional rewards for verificationrs and pledges, but for token holders, it constitutes a “indirect” cost.Therefore, ordinary token holders will get more value in the cost structure of Ethereum, andSolanaThe verifications and pledges will passSolanaGet more value.

Similar to the valuation of traditional assets involving future cash flow, the valuation of encrypted assets may also involve the reflection of future expected network costs.This variable reflects the potential growth of the future of specific networks in the use, use, or monetization in a way that is different from the current total cost.For example, people can reasonably believe that Ethereum’s $ 458 billion valuation not only reflects its current costs, but also reflects the potential of its network effects, as well as the growth of the use rate, usage rate and cost income of the future L2potential.

Finally, the valuation of certain encrypted assets may include “currency premium”.In other words, users may be willing to hold a certain asset because it is the function of currency medium -medium as exchange and/or storage value -surpassing the ability of network cost income.Especially for Ethereum, the concept of currency premium may be very important for its valuation (especially when the tokens are widely used in the mortgage assets of the entire industry).

4,in conclusion

If the accumulation of value is correctly implemented in the agreement, the increase in network usage will not only inspire users to hold tokens, and make them exit and circulate.Network security.In addition to network security, transaction fees will also inspire more authenticists to join, thereby promoting a greater degree of decentralization and anti -examination.Therefore, the accumulation of value is a flywheel that connects the cost and network usage with the token valuation and the security and decentralization characteristics of the network.

But it is important to recognize that although the cost can be used as an indicator of the maturity of the network, there are many other factors in this flywheel that can affect the growth of the network and its valuation.For example, if a specific application is widely used, it may bring more users and attract more developers to develop and build in the same ecosystem.Therefore, we should consider network costs in a comprehensive consideration in the context of other basic indicators and specific ecosystems.

Looking forward to the future, paying attention to some of these growth narratives will be very important.Although the average transaction cost of users is relatively high ($ 4.80), can Ethereum continue to maintain cost growth through high -value trading cases such as token financial assets?Can Ethereum increase its transaction costs with the increase of L2 activities?How will Solana be balanced between profit and maintaining their low enough transaction costs, so as not to lose users to other cheap, high throughput chains?NEAR will try to make a profit, or will it give up the meaningful cost of expenses as before, and give priority to user growth?

These dynamics emphasize the importance of the basic indicators (including fees, transactions, active users and TVL).GrayScale Research believes that with the continuous maturity of crypto assets and more and more adoption, the importance of these basic indicators will continue to increase.These indicators will provide more in -depth insights for the relative advantages and opportunities in the encryption field of smart contracts, and finally help guide wise investment decisions by promoting a more subtle understanding of network value.