Author: Sam Broner, investment partner of a16z crypto; compiled by: 0xjs@Bitchain Vision

Today’s payments are dominated by gatekeepers who charge high fees that undermine the profitability of every business they come into contact with and defend these expenses in the name of universality and convenience—while they stifle competition,Limits the creativity of builders.

Stablecoins can do better.

Stablecoins have lower fees, more competition for payment providers, and more accessibility.As stablecoins reduce transaction costs to almost zero, they can lift businesses out of friction from existing alternatives.People who use stablecoins will start with businesses that are most affected by current payment methods, this process will disrupt the payment industry.

Stablecoins have become the cheapest way to transfer US dollars.Last month, 28.5 million independent stablecoin users sent more than 600 million transactions.Stablecoin users are spread across almost every country, and they use stablecoins because they provide a safe, cheap and anti-inflation-resistant way to save and consume.In addition to cash and gold, stablecoins are the only widely adopted payment method that can be run without a gatekeeper such as a bank, payment network or a central bank.Meanwhile, stablecoins are programmable, scalable and integrated without permission – anyone can help build a stablecoin payment platform on the stablecoin payment track.

This disruption may take time, but may happen faster than many people expect.Businesses such as restaurants, retailers, businesses and payment processors will benefit the most from the stablecoin platform and profit margins will be significantly improved.This demand will drive adoption, and as stablecoin adoption continues to increase, the other benefits of stablecoin – licensing composability and improved programmability – will bring more benefits to on-chain users, businesses and products as they continue to increase.Many benefits.I will share more reasons and methods below, first introducing some backgrounds in the payment industry.

Payment track

• Payment channels: technology, rules and networks that process transactions

• Payment processor: operators on payment tracks that facilitate transactions

• Payment service provider: An entity that provides payment system access to end users or other systems

• Payment Solutions: Products provided by payment service providers

• Payment Platform: A set of related payment solutions covering providers, processors and tracks

Payment industry background

The scale of the payment industry cannot be underestimated.In 2023, the global payments industry processed 3.4 trillion transactions worth up to $1.8 trillion, generating $2.4 trillion in revenue.The credit card payments in the United States alone are as high as $5.6 trillion, while the debit card payments are as high as $4.4 trillion.

Despite the ubiquitous and large scale of the industry, payment solutions are still expensive and complex, and payment applications often block the consumer’s experience.For example, while the front end of the peer-to-peer payments app Venmo seems simple, in the back end, the product hides intricate bank integrations, debit card vulnerabilities and countless compliance obligations.Payment solutions are often interdependent, which adds complexity, and people still use various payment methods: cash, debit cards, credit cards, peer-to-peer payment applications, ACH (automatic clearing house), checks, and more.

The four main measurement indicators of payment products are timeliness, cost, reliability and convenience.

Consumers’ priorities include “How much do I have to pay?” Merchants will ask “Will I get paid?” But in fact, these four indicators are essential to both parties.

Since businesses have had to look for fraudulent credit cards in physical ledgers, the wave of innovation has continuously improved the payment experience.Each wave of innovation has brought faster, more reliable, more convenient and cheaper payment methods, which in turn has led to an increase in transaction volume and consumption.

But many customers still do not enjoy modern service or do not enjoy adequate service.For merchants, credit cards are expensive and directly erode their profits.Despite the increasing adoption of real-time payments (RTP), U.S. bank transfers are still too slow and take several days.And peer-to-peer applications are region- and network-specific, which makes transfers between ecosystems slow, cost-effective and complex.

While businesses and consumers have begun to expect payment platforms to provide more complex features, not all users can benefit from existing solutions.In fact, most users pay too much and do not use all bundled payment products.But they accepted the current situation.

Stable coins are included in this way

The key to stablecoins disrupting the industry is the failure of existing payment solutions (high cost, low availability or high friction), and the bundled products of payment solutions (including identity, lending, compliance, fraud protection and banking integration) are the least.necessary.

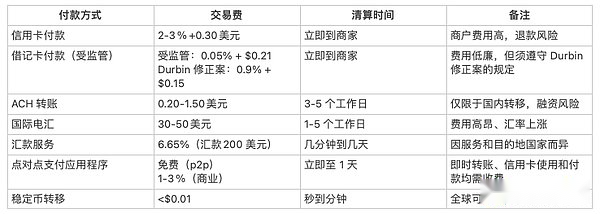

Taking remittances as an example, it was born in despair.Many remittance users have insufficient banking services and use highly fragmented banking services.Therefore, these users believe that the native integration between traditional payments and banking services is worthless.Stablecoin payments provide instant certainty, low cost and no intermediaries, which is a structural advantage for any payment user or builder.After all, with a stablecoin, sending $200 from the U.S. to Colombia costs less than $0.01, but on traditional channels it costs $12.13.(Remittance users will need to send money home regardless of transaction costs, but lower fees will greatly benefit.)

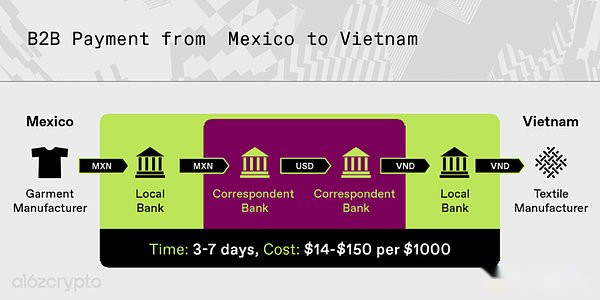

International commercial payments, especially small businesses in emerging markets, also face problems of high fees, slow processing times and low bank approval ratings.For example, payments between Mexican clothing manufacturers and Vietnamese textile manufacturers will involve four or more intermediaries – local banks, forex, agency banks, agency banks, forex, local banks.Each intermediary agency will charge a certain proportion of fees and there is a risk of middlemen going bankrupt.

Fortunately, these transactions occur between partners with regular relationships.With stablecoins, Mexican payers and Vietnamese payees can experiment and eliminate slow, bureaucratic and expensive intermediaries.They may need to work hard to find local channels and workflows, but ultimately they can enjoy faster, cheaper transactions and more control over the payment process.

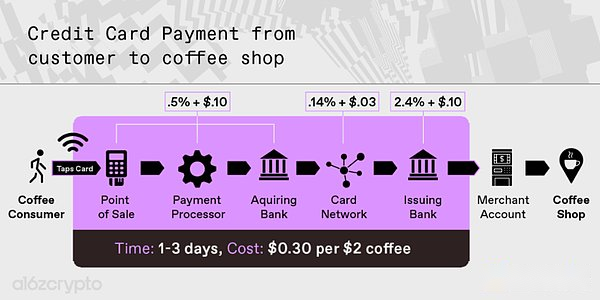

Small transactions (especially low-fraud face-to-face transactions, such as those conducted in restaurants, coffee shops or corner shops) are also a promising opportunity.Due to low profit margins, these businesses are cost-sensitive, so the 15-cent transaction fee charged by payment solutions has a big impact on their profitability.

For every $2 spent on coffee, only $1.70 to $1.80 went to coffee shops, and nearly 15% of the rest went to credit card companies—just to facilitate transactions.But credit cards are here just for convenience: no additional features are needed to justify the charges, either for consumers or for stores.Consumers don’t need fraud protection (they just got a cup of coffee) or loans (the coffee costs only $2).And the compliance and bank integration requirements of coffee shops are limited (coffee shops usually use integrated restaurant management software or do not use them at all).So if there are cheap, reliable alternatives, these businesses will take advantage of it.

Cheaper payments improve profitability

Current payment system transaction fees directly harm the profits of many businesses.Reducing these expenses will lead to huge profitability.The first boot has landed: Stripe announces that they will charge a 1.5% fee for stablecoin payments, 30% less than the credit card payments they charge.To support this effort, Stripe announced the acquisition of Bridge.xyz for approximately $1 billion.

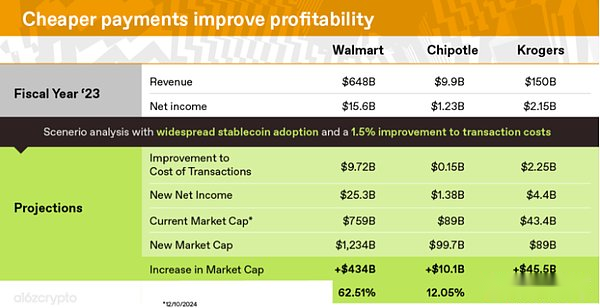

The wider adoption of stablecoins will significantly increase the profitability of many businesses—not just small businesses like coffee shops or restaurants.Let’s take a look at the financial situation of the three publicly listed companies for fiscal 2024 to get a rough idea of the impact of reducing payment processing rates to 0.1%.(For convenience, this evaluation assumes that the business pays 1.6% of the hybrid payment processor cost and the deposit and withdrawal costs are extremely low. See below for more information on this.)

-

Walmart earns $648 billion in annual revenue.Probably pay $10 billion in credit card fees and profit of $15.5 billion.Calculate it: considering the elimination of payment fees and Walmart’s profitability,Its valuation (controls all other factors) may increase by more than 60% with cheaper payment solutions alone.

-

Chipotle is a fast-growing fast food restaurant with annual revenue of $9.8 billion.Its annual profit is $1.2 billion, of which the credit card fees paid are $148 million.Chipotle’s profitability can be increased by 12% by reducing fees alone——This is an amazing number that is not available anywhere else in its profit and loss statement.

-

National grocery store Krogers has the lowest profit margins and therefore makes the most profits.Surprisingly, Krogers’ net income and payment costs are likely to be nearly equal.Like many grocery stores, its profit margin is below 2%, which is less than the fees paid by businesses to process credit cards.With stablecoin payments, Krogers’ profits could double.

How will Walmart, Chipotle and Krogers reduce transaction fees with stablecoins?First, consider an ideal situation: consumers won’t accept stablecoins all at once, and there will still be considerable fees until they get enough acceptance, especially when they start and stop using them.Second, retailers and payment processors are both opposed to high-cost payment solutions.Payment processors are also low-profit businesses, giving away most of their profits to credit card networks and issuing banks.When payment processors process transactions, most of their fees are passed on to payment networks.So when Stripe handles the online retail checkout process, they take 2.9% of the fees and $0.30 from the total transaction, but they pay Visa and the issuing bank more than 70%.As more payment processors, such as Block-formerly Square, Fiserv, Stripe and Toast, adopt stablecoins to increase profit margins, they will make it easier for more businesses to obtain stablecoins.

How will Walmart, Chipotle and Krogers reduce transaction fees with stablecoins?First, consider an ideal situation: consumers won’t accept stablecoins all at once, and there will still be considerable fees until they get enough acceptance, especially when they start and stop using them.Second, retailers and payment processors are both opposed to high-cost payment solutions.Payment processors are also low-profit businesses, giving away most of their profits to credit card networks and issuing banks.When payment processors process transactions, most of their fees are passed on to payment networks.So when Stripe handles the online retail checkout process, they take 2.9% of the fees and $0.30 from the total transaction, but they pay Visa and the issuing bank more than 70%.As more payment processors, such as Block-formerly Square, Fiserv, Stripe and Toast, adopt stablecoins to increase profit margins, they will make it easier for more businesses to obtain stablecoins.

The fee for stablecoins is low and there is no need to pay for the network gatekeeper.This means that payment processors earn much higher profit margins in stablecoin transactions.Higher profit margins may prompt payment processors to support and encourage more businesses and use cases to use stablecoins.But as payment processors start adopting stablecoins, stablecoin payment fees are expected to be compressed over time: Stripe’s 1.5% fee may drop.

Next step: Consumers adopt

Today, stablecoins are a new way to send and store currencies without permission.Entrepreneurs are already building solutions to transform the stablecoin track into a stablecoin platform.As with previous innovations, adoption will gradually take place, starting from the edge of consumer demand, then forward-looking businesses until the platform matures enough to meet the needs of daily users and cautious businesses.Three trends will drive more mainstream companies to adopt stablecoins.

1. Increase background integration through stablecoin aggregation

Stablecoin aggregation (the ability to monitor, guide and integrate stablecoins) will soon be integrated into payment processors such as Stripe.These aggregation products enable businesses to process payments at much lower costs than the current mechanism without major process or engineering changes.Consumers may end up with cheaper products without realizing it, as invoices, payrolls, and subscriptions have lower structural costs by default.

Many of these stablecoin aggregation businesses have begun to attract customers who want instant settlement, low-cost, and widely available business-to-business or business-to-consumer payments.By integrating stablecoins in the backend, businesses will benefit from the advantages of stablecoins—not interrupting or reducing the quality of service users expect from payment providers, while the adoption of stablecoins will also increase.

2. Improve the process of enterprise entry and increase sharing incentives

The stablecoin business is becoming increasingly mature in bringing end users into the chain through sharing incentives and improving entry solutions.

Entering is becoming cheaper, faster and more common, making it easier for users to start using cryptocurrencies.Meanwhile, more and more consumer applications support cryptocurrencies, enabling users to benefit from the expanded stablecoin ecosystem – without adopting new applications or user behavior.Popular apps like Venmo, ApplePay, Paypal, CashApp, Nubank, and Revolut all allow their customers to use stablecoins.

Moreover, companies are more motivated to use these channels to integrate stablecoins and deposit funds into stablecoins.Fiat-backed stablecoin issuers such as Circle, Paypal and Tether are sharing profits with average businesses, just as Visa shares profits from contracted credit card users with United and Chase.Such collaborations and integrations benefit stablecoin issuers because they can create larger pools of assets to earn profits.But they can also benefit businesses that successfully convert users from credit cards to stablecoins.These businesses can now earn some of the proceeds generated by their funds from their products, and this business model is often only applicable to banks, fintech companies and gift card issuers that make money through user floats.

3. Improve regulatory transparency and the availability of compliance solutions

When businesses are confident in the regulatory environment, they are more likely to adopt stablecoins.While we haven’t seen a comprehensive global regulation of stablecoins, many jurisdictions have issued rules and guidance on stablecoins that allow entrepreneurs to start hard work and build compliant, user-friendly businesses.

For example, the EU’s Crypto Asset Market Supervision Regulations (MiCA) sets rules for stablecoin issuers, including prudence and behavioral requirements.The regulation has greatly changed the European stablecoin market since the stablecoin clause came into effect earlier this year.

Although the United States currently lacks a stablecoin framework, policymakers from both parties are increasingly aware of the need to formulate effective stablecoin legislation.Such regulation requires ensuring that issuers fully support their tokens with high-quality assets, audit their reserves by third parties, and take comprehensive measures to combat illegal financial activities.At the same time, legislation needs to retain the ability of creators to create decentralized stablecoins, reduce user risks by eliminating intermediaries, and take advantage of decentralization.

These policy efforts will enable companies from all walks of life to consider moving from traditional payment methods to stablecoin infrastructure.While compliance solutions are not attractive, everyone who adopts stablecoins helps prove to existing businesses that stablecoins are a reliable, secure, regulated and improved solution to traditional payment problems.

With the popularity of stablecoins, the network effect of the platform will become stronger and stronger.While it may take several years for stablecoins to be used at the point of sale or as a replacement for bank accounts, as the number of stablecoin users grows, stablecoin-centric solutions will become more mainstream, for consumers,Businesses and entrepreneurs are also more attractive.

Trend: Why Stablecoins Continue to Improve

During the adoption process, the product itself will continue to improve.The web3 community is celebrating the adoption of stablecoins for good reason: Stablecoins are climbing the value innovation S curve due to years of investment in infrastructure and on-chain applications.With the improvement of infrastructure, the enrichment of on-chain applications and the growth of on-chain networks, stablecoins will become more attractive to users.This will be achieved in two ways.

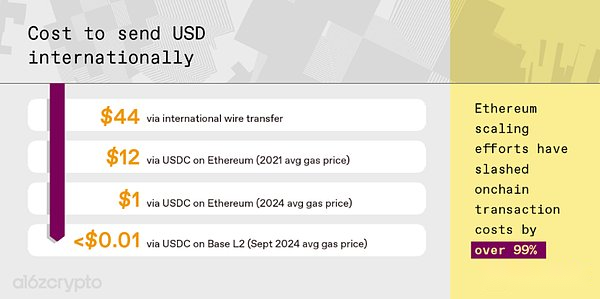

First, the hard work of crypto infrastructure makes it possible to pay for stablecoins under 1 cent.Future investments will continue to make transactions cheaper and faster.At the same time, stablecoin aggregation and improved entry experience are only possible through better wallets, bridges, deposits and withdrawals, developer experiences and AMMs.

This technology foundation provides entrepreneurs with increasing incentives to build stablecoins, providing a better developer experience, a rich ecosystem, a wide range of applications, and license-free composability of on-chain currencies.

Second, stablecoins unlock new user scenarios through the permissionless composability of on-chain currencies.Other payment platforms have gatekeepers that force entrepreneurs to work with withdrawal networks, such as expensive intermediaries in credit card transactions or international payments.But stablecoins are self-custodial and programmable, lowering the threshold for creating new payment experiences and integrating value-added services.Stablecoins are also comboable, allowing users to benefit from increasingly powerful on-chain applications and increasingly fierce competition.For example, stablecoin users have already benefited from DeFi, on-chain subscriptions, and social applications.

Conclusion

Stablecoins can lead us into a world of free, scalable, instant payments.As Stripe CEO Patrick Collison said, stablecoins are “a room temperature superconductor for financial services.”They will enable businesses to seek new opportunities that would otherwise not be able to bear the burden of existing payment channels or the friction of traditional gatekeepers.

In the short term, as payments become free and open, stablecoins will cause structural changes to financial products.Existing payment companies will seek new ways to make profits, either by charging a certain percentage of the revenue or by selling services that complement this new commoditized platform.As these traditional businesses recognize the changing situation, entrepreneurs will create new solutions to help these businesses leverage stablecoins.

In the long run, with the popularity of stablecoins and advancement of technology, startups will seize the opportunities brought by a world of free, frictionless and instant payments.These startups will be launched today, unlocking new and unexpected scenarios and further democratizing the opportunities offered by the global financial system.

Acknowledgements: Special thanks to Tim Sullivan, Aiden Slavin, Eddy Lazzarin, Robert Hackett, Jay Drain, Liz Harkavy, Miles Jennings and Scott Kominers for their thoughtful feedback and advice that have made this article complete.