Author: Alex Thorn, Gabe Parker, Galaxy; Compilation: Wuzhu, Bitchain Vision

Preface

2024 was a brilliant year for the cryptocurrency market, with the spot Bitcoin ETP launched in January and the election of the president and Congress, the most supportive cryptocurrency in U.S. history, in November.Overall, the liquidity cryptocurrency market increased its market cap by $1.6 trillion in 2024, up 88% year-on-year to $3.4 trillion.Bitcoin alone adds $1 trillion in market capitalization, close to $2 trillion for the whole year.The cryptocurrency narrative in 2024 was driven by the rapid rise in Bitcoin (62% of total market earnings) on the one hand, and by meme and AI on the other hand.Meme is a popular cryptocurrency for most of the year, with most on-chain activity happening on Solana.In the second half of the year, tokens operated by AI agents became the focus in the former Bitcoin cryptocurrency space.

Crypto venture capital in 2024 remains difficult.These major Bitcoin, meme, and AI agents are not particularly suitable for venture capital.Memecoin is launched with just a few buttons, and Memecoin and AI proxy coins are almost exclusively on-chain, leveraging existing infrastructure primitives.Hot industries in the last market cycle, such as DeFi, gaming, metaverse and NFT, either failed to attract market attention or were built and needed less capital, making new entrepreneurship more competitive.The crypto market infrastructure and games are mostly built and are now in a late stage, with the next administration’s expectations of U.S. regulation changing, these industries could face competition from deeply rooted traditional financial services intermediaries.There are signs that new dollar currencies may become an important driver of new capital inflows, but these dollar currencies range from immature to very new:Among them, the standout are stablecoins, tokenization, the integration of DeFi and TradFi, and the overlap between encryption and artificial intelligence.

Macro and wider market forces also continue to bring resistance.The high interest rate environment continues to put pressure on the venture capital industry, and allocators are less willing to take further risks on the risk curve.This phenomenon squeezes the entire venture capital industry, but given its risks, the crypto venture capital industry may be particularly affected.Meanwhile, large comprehensive venture capital firms still mostly avoid this space, perhaps they remain cautious after several well-known venture capital firms went bankrupt in 2022.

So, despite significant opportunities in the future, whether through the recovery of existing primitives and narratives or through the emergence of new primitives and narratives, crypto ventures are still competitive and downturn compared to the 2021 and 2022 fanaticism.Both trading and invested capital increased, but the number of new funds stagnated, and the capital allocated to venture capital funds decreased, creating a particularly competitive environment that facilitates the founders’ valuation negotiations.Broadly speaking, venture capital is still much lower than the level of previous market cycles.

But the growing institutionalization of Bitcoin and digital assets, as well as the growth of stablecoins, and the new regulatory environment may ultimately herald the possibility of some convergence between DeFi and TradFi, and also bring new opportunities for innovation.A meaningful recovery is expected in 2025 for venture capital activities and interests.

summary

-

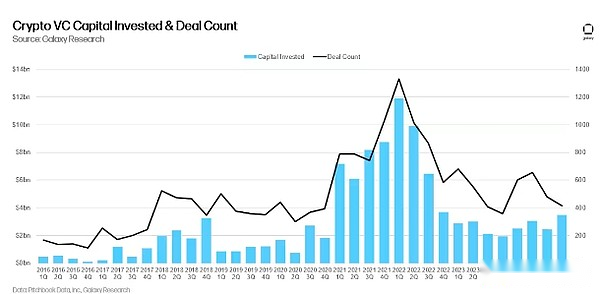

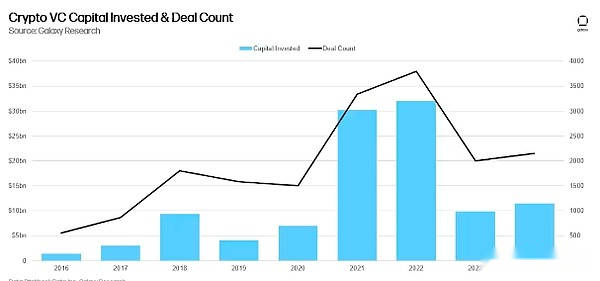

In the fourth quarter of 2024, venture capital investment in cryptocurrency startups was $3.5 billion (46% month-on-month increase), involving 416 transactions (13% month-on-month decrease).

-

Throughout 2024, venture capitalists invested $11.5 billion in 2153 transactions in startups focused on cryptocurrencies and blockchain.

-

Early transactions received the most capital investments (60%), while late transactions accounted for 40% of invested capital, a significant increase from 15% in the third quarter.

-

The median valuation of venture capital transactions rose in the second and third quarters, with cryptocurrency-specific transactions growing faster than the entire venture capital industry, but remained unchanged in the fourth quarter on a quarter-on-month basis.

-

Stablecoin companies raised the most, with Tether raising $600 million from Cantor Fitzgerald taking the brunt, followed by infrastructure and Web3 startups.Web3, DeFi and infrastructure companies account for the largest number of transactions.

-

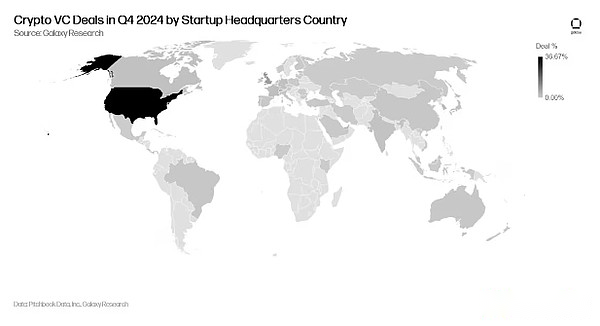

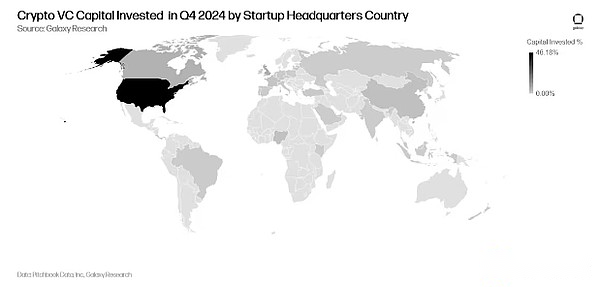

In the fourth quarter, most investments went to U.S.-based startups (46%), while Hong Kong companies accounted for 17% of all investment capital.In terms of deal count, the U.S. leads with 36%, followed by Singapore (9%) and the United Kingdom (8%).

-

In terms of financing, investors’ interest in crypto-focused venture capital funds fell to $1 billion in the 20 new funds.

-

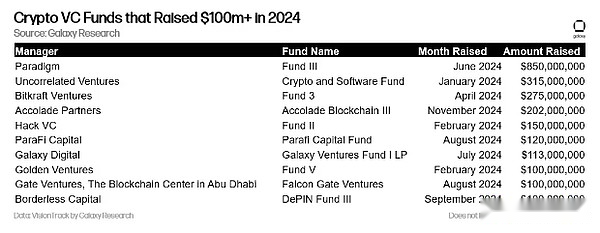

In 2024, at least 10 cryptocurrency venture capital funds raised over $100 million.

Venture Capital

Number of transactions and investment capital

In the fourth quarter of 2024, venture capitalists invested $3.5 billion (46% sequentially) in cryptocurrency and blockchain-focused startups, totaling 416 transactions (13% sequentially).

As of 2024, venture capitalists have invested $11.5 billion in cryptocurrency and blockchain startups through 2153 transactions.

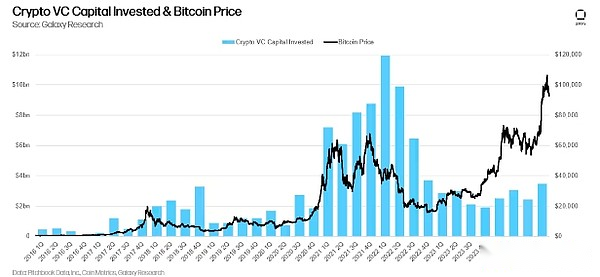

Investment capital and Bitcoin price

There was a years of correlation between Bitcoin prices and capital invested in crypto startups in previous cycles, but this correlation has been working to recover last year.Bitcoin has risen sharply since January 2023, while venture capital activity has struggled to keep pace.Configurators’ weak interest in crypto venture capital and broad venture capital, coupled with the crypto market narrative’s preference for Bitcoin and ignoring many of the hot narratives of 2021, can partly explain the difference.

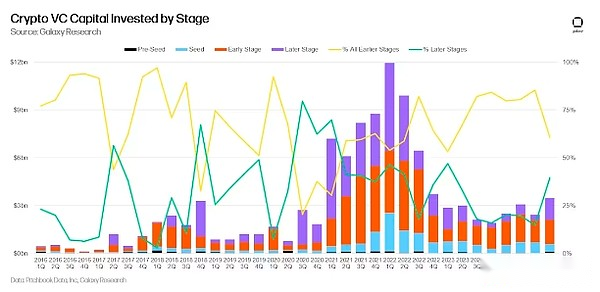

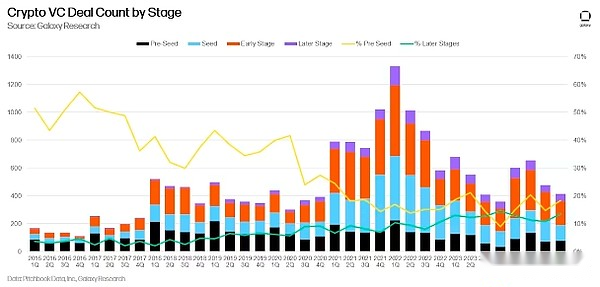

Phase investment

In the fourth quarter of 2024, 60% of venture capital was invested in early-stage companies, while 40% were invested in late-stage companies.Venture capital firms raised new funds in 2024, and crypto-native funds may still be able to get funding from large-scale financing a few years ago.Starting from the third quarter, more and more capital flows to late-stage companies, which can be partly explained that Tether raised $600 million from Cantor Fitzgerald.

In terms of trading, the proportion of pre-seed trading has increased slightly, and remains healthy compared to the previous cycles.We track the proportion of pre-seed transactions to measure the robustness of entrepreneurial behavior.

Valuation and transaction size

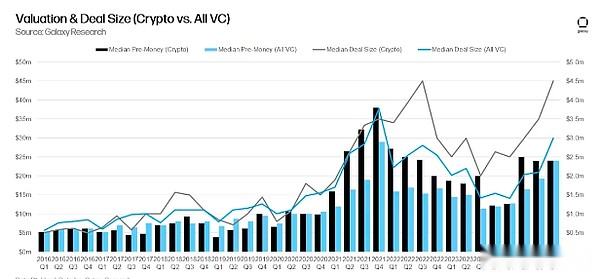

In 2023, VC-backed cryptocurrency companies saw a sharp decline in valuations, reaching their lowest level since the fourth quarter of 2020.However, as Bitcoin hit an all-time high, valuation and transaction size began to rebound in the second quarter of 2024.In the second and third quarters of 2024, valuations reached their highest levels since 2022.The growth in cryptocurrency transaction size and valuation in 2024 is consistent with similar growth across the venture capital sector, although the cryptocurrency rebounds are stronger.The median pre-investment valuation for the fourth quarter of 2024 transactions was $24 million, with an average transaction size of $4.5 million.

Investment Category

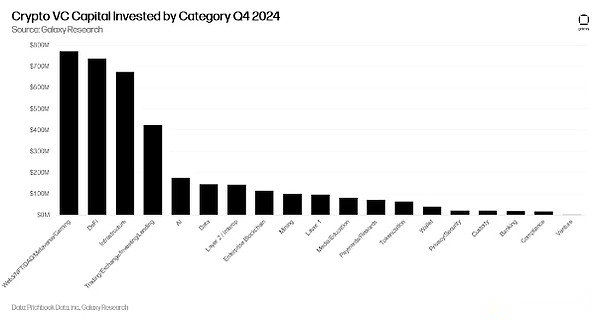

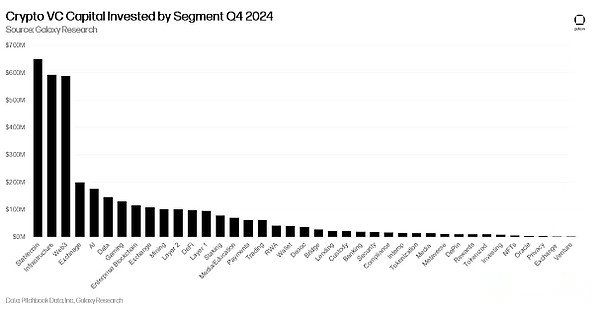

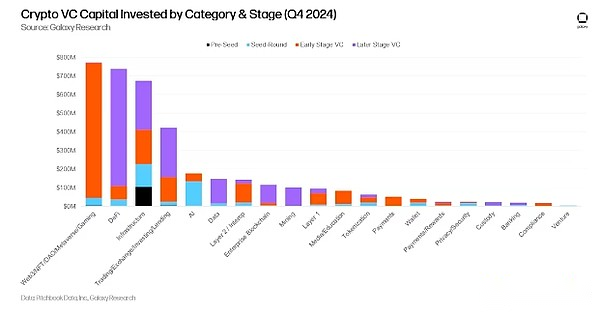

Companies and projects in the “Web3/NFT/DAO/Metaverse/Gaming” category accounted for the largest share of crypto venture capital (20.75%), with a total of US$771.3 million.In this categoryThe three largest deals are Praxis, Azra Games and Lens,$525 million, $42.7 million and $31 million were raised, respectively.DeFi’s dominance of total crypto venture capital is attributed to a $600 million deal with Tether and Cantor Fitzgerald, which owns a 5% stake in the company (stablecoin issuer falls under our premium DeFi category).While this deal is not a traditional venture capital structured deal, we incorporated it into our dataset.If Tether’s transaction is removed, the DeFi category will be ranked 7th in the fourth quarter.

In the fourth quarter of 2024, crypto startups that build Web3/NFT/DAO/Metaverse and infrastructure products accounted for 44.3% and 33.5% of the total quarterly crypto venture capital, respectively.The increase in capital allocation as a percentage of total capital deployment is mainly attributed to the sharp decline in capital allocation to Layer 1 and crypto AI startups by crypto venture capital, down 85% and 55% respectively since the third quarter of 2024.

If we break down the big categories in the chart above into more granular parts, the crypto project that builds stablecoins raised the largest share of crypto venture capital (17.5%) in the fourth quarter of 2024, totaling in 9 tracking transactions$649 million.However, Tether’s $600 million transaction represents much of the total capital invested in stablecoin companies in the fourth quarter of 2024.Crypto startups that develop infrastructure raised the second most venture capital out of 53 tracking transactions in the fourth quarter of 2024, at $592 million (16%).The three major crypto infrastructure transactions are Blockstream, Hengfeng Group and Cassava Network, raising $210 million, $100 million and $90 million respectively.Following crypto infrastructure, Web3 startups and exchanges ranked third and fourth in funding from crypto venture capital firms, totaling $587.6 million and $200 million, respectively.It is worth noting that Praxis is the largest Web3 deal and second largest in the fourth quarter of 2024, raising up to $525 million to build an “Internet native city.”

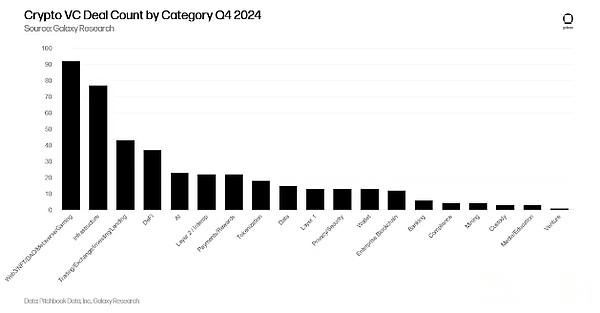

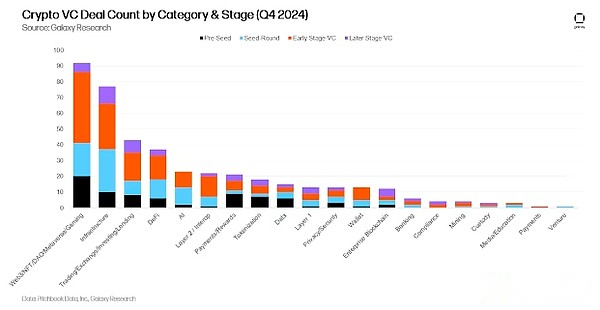

In terms of transaction count, Web3/NFT/DAO/Metaverse/games accounted for 22% of transactions (92), with 37 game transactions and 31 Web3 transactions being the driving factors.The biggest gaming deal in the fourth quarter of 2024 was Azra Games, which raised $42.7 million in Series A financing.Followed closely by infrastructure and trading/exchange/investment/lending, with 77 and 43 transactions respectively in the fourth quarter of 2024.

Projects and companies that provide crypto infrastructure ranked second in the number of transactions, accounting for 18.3% of the total transaction volume (77 transactions), an increase of 11 percentage points month-on-month.Following the crypto infrastructure, projects and companies that build transaction/exchange/investment/lending products rank third in terms of transactions, accounting for 10.2% of the total transaction volume (43 transactions).It is worth noting that crypto companies that build wallets and payment/reward products have seen the largest month-on-month increase in transaction volume, at 111% and 78% respectively.While these quarter-on-month increase is a significant percentage, wallet and payment/reward startups accounted for only 22 and 13 transactions in the fourth quarter of 2024, respectively.

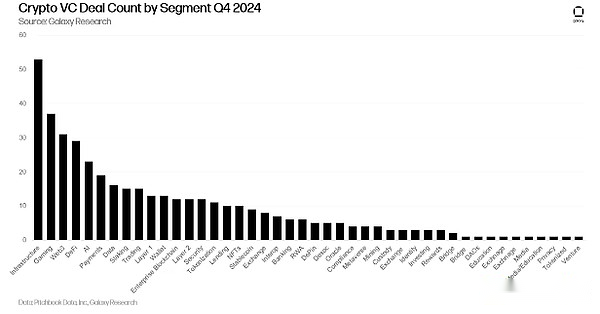

Break down the large categories in the figure above into more granular parts, with projects and companies building crypto infrastructure the largest number of transactions in all industries (53).Following closely behind are gaming and Web3-related crypto companies, which completed 37 and 31 transactions in the fourth quarter of 2024, almost the same order as in the third quarter of 2024.

Investments by stage and category

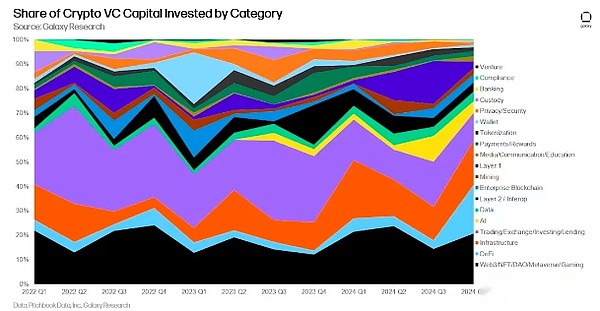

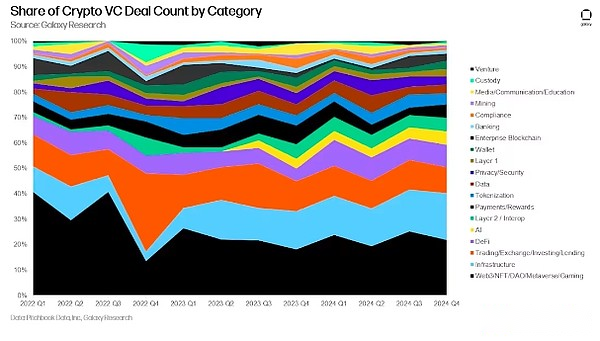

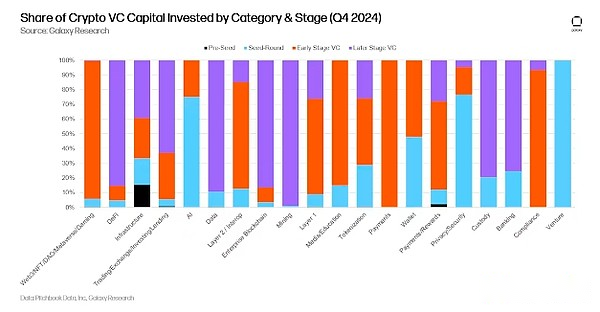

Segmenting the number of invested capital and transactions by category and stage gives a clearer understanding of which types of companies in each category are raising funds.In the fourth quarter of 2024, the vast majority of capital in Web3/DAO/NFT/Metaverse, Layer 2s, and Layer 1s flowed to early stage companies and projects.In contrast, a large portion of crypto venture capital funds invested in DeFi, trading/exchange/investment/lending and mining flows to late-stage companies.This is expected considering the relative maturity of the latter relative to the former.

Analyzing the distribution of investment capital at different stages in each category can reveal the relative maturity of various investment opportunities.

Like crypto venture capital invested in Q3 2024, a large portion of transactions completed in Q4 2024 involve early-stage companies.Crypto venture investment transactions tracked in the fourth quarter of 2024 include 171 early transactions and 58 late transactions.

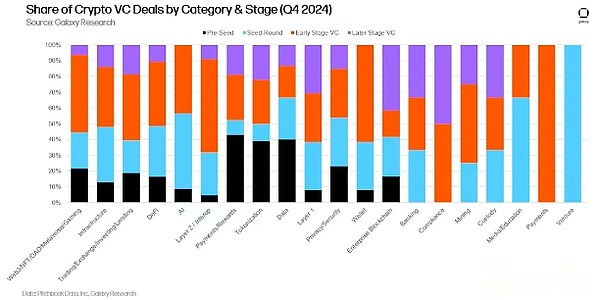

Examining the transaction share completed by stage in each category provides an in-depth understanding of the stages of each investable category.

Investments by geographical location

In the fourth quarter of 2024, 36.7% of transactions involved U.S.-based companies.Following closely behind are Singapore (9%), the United Kingdom (8.1%), Switzerland (5.5%) and the United Arab Emirates (3.6%).

The U.S.-based company absorbed 46.2% of all venture capital, down 17 percentage points from the previous quarter.As a result, venture capital allocation for Hong Kong-based startups increased significantly, reaching 17.4%.The UK is 6.8%, Canada is 6%, and Singapore is 5.4%.

Group investment

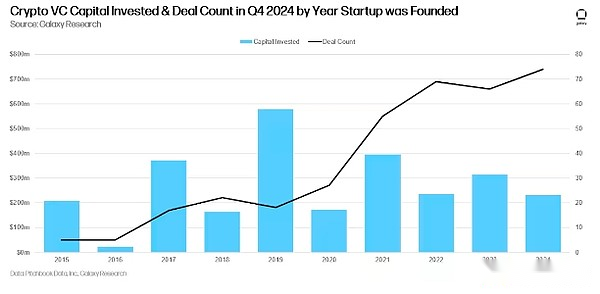

Companies and projects established in 2019 account for the largest share of capital, while companies and projects established in 2024 have the largest number of transactions.

Venture Capital Financing

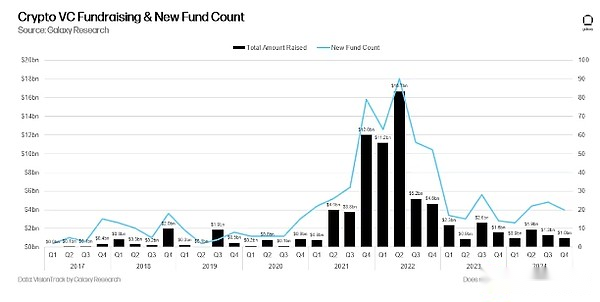

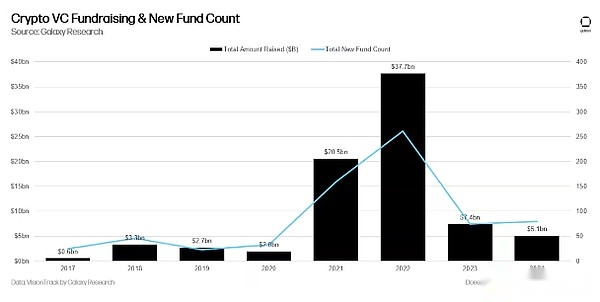

Financing of crypto-risk funds remains challenging.The macro environment and turmoil in 2022 and 2023 have made some allocators reluctant to make the same level of commitment to crypto venture investors as they did in 2021 and early 2022.In early 2024, investors generally believed that interest rates would drop sharply in 2024, although rate cuts did not begin to be realized until the second half of the year.Since the third quarter of 2023, the total capital allocated to venture funds has continued to decline month-on-month, although the number of new funds increased throughout 2024.

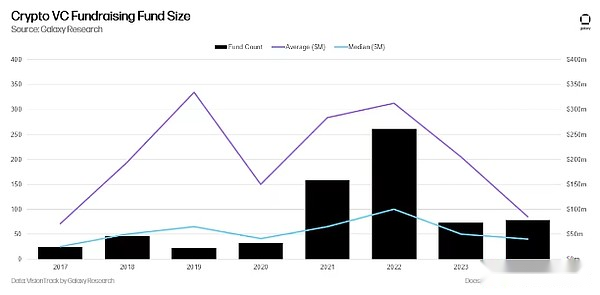

On an annualized basis, 2024 was the weakest year for crypto venture fundraising since 2020, with 79 new funds raising $5.1 billion, well below the 2021-2022 craze.

While the number of new funds does increase slightly year-on-year, the decline in allocation interest also leads to smaller funds raised by venture capital firms, with median and average fund sizes reaching the lowest level since 2017.

At least 10 cryptocurrency venture funds that actively invest in cryptocurrencies and blockchain startups raised more than $100 million for new funds in 2024.

Summarize

-

Emotion is improving and activity is increasing, although both are still well below previous highs.While the liquidity crypto asset market has recovered significantly from the end of 2022 and early 2023, venture capital activity is still far below the previous bull market.The bull markets in 2017 and 2021 were reflected in a high correlation between venture capital activity and liquid crypto asset prices, but activity has been sluggish over the past two years while cryptocurrencies have rebounded.The stagnation of venture capital is due to a variety of factors, including the “barbell market” that puts Bitcoin (and its new ETFs) at the center, and marginal net new activities from Meme, which is difficult to finance and has doubts in life.Passion for the intersection of AI and cryptocurrency projects is rising, and expected regulatory changes may open the door to opportunities for stablecoins, DeFi and tokenization.

-

Early trading continues to lead the trend.Despite resistance to venture capital, interest in early trading still heralds the long-term health of the broader cryptocurrency ecosystem.The late trading group made progress in the fourth quarter, but mainly due to Cantor Fitzgerald’s $600 million investment in Tether.Nevertheless, entrepreneurs continue to find investors willing to invest in new innovative ideas.We believe thatProjects and companies that build stablecoins, artificial intelligence, DeFi, tokenization, L2 and Bitcoin related products performed well in 2025.

-

Spot ETP may put pressure on funds and startups.Several high-profile investments by U.S. allocators in spot Bitcoin ETP suggest that some large investors (pensions, endowments, hedge funds, etc.) may be reaching the industry through large liquidity tools rather than turning to early-stage venture capital.Interest in spot Ethereum ETP has begun to increase, and if this continues, or even if new ETPs are launched, covering other alternative tier 1 blockchains, demand for segments such as DeFi or Web3 may also flow toETP, not venture capital complex.

-

Fund managers are still facing a difficult environment.Although the number of new funds increased slightly year-on-year in 2024, the total capital allocated to crypto venture capital funds was slightly lower than in 2023.The macroeconomic continues to bring resistance to allocators, but significant changes in the regulatory environment may rekindle interest in the field.

-

The United States continues to dominate the crypto startup ecosystem.Although regulatory regimes are very tricky and often hostile, U.S.-based companies and projects still account for the majority of transactions completed and the majority of invested capital.The new presidential administration and Congress will become the most supportive government and Congress in history.We expect U.S. dominance will increase, especially if certain regulatory matters are consolidated as expected, such as stablecoin frameworks and market structure legislation, which will allow traditional U.S. financial services firms to seriously consider entering the field.