Author: Charles Shen @ inWeb3.com

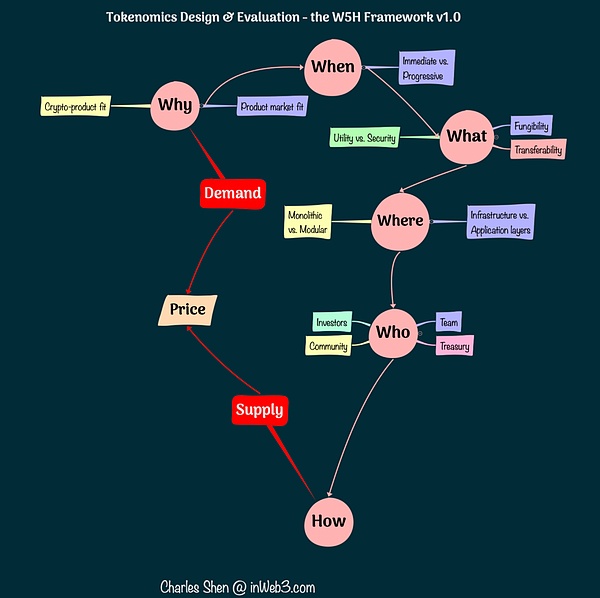

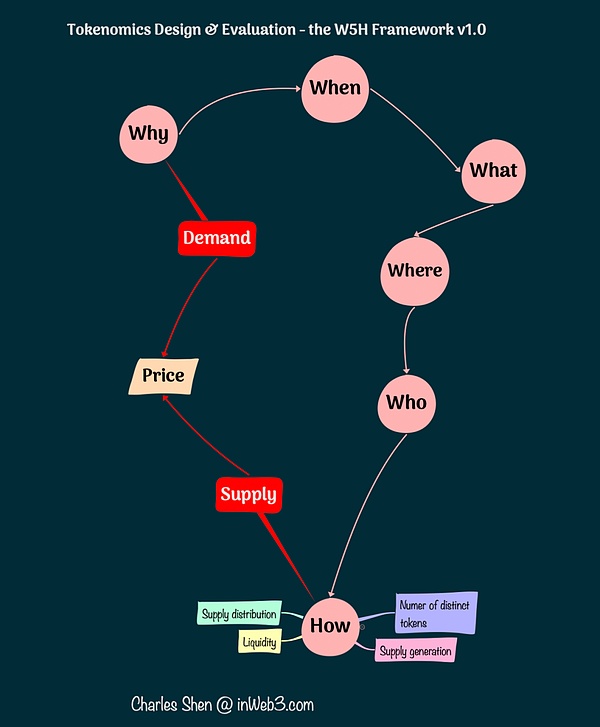

In the first two articles, we have discussed the five “Ws” of the W5H framework: namely “Why, When, What, Where, Who”.Among them, “Why” explores the rationality of tokens and the sustainable value creation of crypto economies behind them; “When” discusses the best time to issue tokens; “What” studies the types of tokens suitable for specific purposes; “Where” focuses on which blockchain network tokens should be created; “Who” examines which participants in the ecosystem are suitable for owning tokens.

In this article, we will continue to explore “How to design tokens”.Admittedly,The discussion on “how to design tokens” can be very broad.This article will discuss several of these key issues, including how many different tokens are needed, how to generate and allocate token supply, how to distribute tokens, and how to build liquidity for tokens.

Determine how many different tokens are needed for the project

When analyzing “why tokens are needed”, we often find that modern coins can play multiple roles in projects to help achieve system goals.In other words, tokens can have various functions and can also have governance rights.Naturally, we think about a question:How many different tokens are needed in the project?Or, should we integrate all the features into a single token?

Before answering this question, we first need to clarify the definition of “different tokens” in the project.Typically, when referring to project tokens, we refer to native tokens specially created for a specific project.However, even native tokens have different types.Take Sushi, the DeFi trading platform, as an example, which has the native token SUSHI.After a user pledges SUSHI, he will receive xSUSHI tokens, which can accumulate transaction fees from Sushi exchanges and bring benefits to holders.Users can redeem xSUSHI at any time to retrieve the original pledged SUSHI and the benefits generated.Therefore, xSUSHI is just a profit-generating variant of SUSHI, which is just a packaging or derivative form of the base token.We do not regard these tokens as truly “different tokens” in the project.

How to decide how to use several different tokens based on the determined token goal is not an easy task.Each target can use a separate token. The advantage of this is that it has clearer design and more direct analysis of token systems.But using multiple different tokens in a project, the disadvantage of this approach is that the value of each token is dispersed and the liquidity of each token is reduced, which may ultimately affect the overall development of the project.In addition, tokens that are completely independent cannot take advantage of synergies that may be generated by strategic integration.

The “dual token model” is a widely used model in which governance and non-governance functions are carried by two different tokens.Axie Infinity game is a typical example, where AXS tokens assume the governance role and SLP tokens act as in-game currency.However,The dual token model is not a common solution to the problem, because the utility of tokens is much more than governance and currency.

To address this problem, we can take the following general approach:

-

List all the goals we want to achieve (such as specific product features or incentive goals).This information should be obtained from the “Why tokens” step in the first part of this series.

-

Suppose that each target is assigned an independent token.

-

Discuss whether certain tokens can be integrated based on the consistency of interests of potential holders.

-

Iterative technology solutions ensure that both the required business logic is realized while making token integration possible.

-

In this process, other attributes of each candidate token, such as substitutability, applications and infrastructure, should also be considered.

There are several important things to remember when making decisions:

The final decision results depend heavily on the implementation of actual solutions, and even for similar products, the results may vary greatly.

The level of consistency in stakeholders is key to determining whether multiple goals can be merged into the same token.

Combining goals at different levels of the network stack presents additional risks, which requires special attention.

The decision about choosing different tokens is only part of the design, and it does not guarantee whether the basic structure of the project is sound.

In the appendix to this article, we show how the above steps are applied through several case studies of decentralized stablecoin projects and reflect the manifestation of these considerations in the actual process.

Generate and allocate token supply

Once we have identified the tokens we want to create, the next step is to consider how to generate and supply these tokens.

Maximum supply:When formulating a token generation plan, we first need to determine whether the total supply of tokens is limited or unlimited.This decision itself does not determine the health of token design, because what really matters is the continuous balance between supply and demand.For example, among the major cryptocurrencies, the maximum supply of Bitcoin (BTC) is fixed at 21 million, while the supply of Ethereum (ETH) is unlimited.Some projects set a maximum supply based on the estimated number of holders to avoid decimal amounts of tokens. For example, Ankr sets a maximum supply of 10 billion.

Coin minting timetable:Although all tokens can be minted in one go, it is more common to gradually increase the maximum supply over time, as this is more conducive to regulating supply.There are two main ways to achieve it: casting on demand or emissions as planned.For example, MakerDAO’s stablecoin DAI can be minted at any time by providing corresponding collateral, without a fixed minting schedule or supply cap.The Bitcoin blockchain generates a block every 10 minutes and creates new Bitcoins in each new block, a process that will continue until the maximum number of Bitcoins is reached.

Allocation table:Projects usually develop an allocation table to clarify how different key stakeholders will allocate the token supply.It is worth noting that we do not want to hold tokens too concentrated, because excessive concentration may lead to the token price being easily operated by a few large investors.For example, a report by Coopahtroopa and Lstephanian summarizes data from 60 projects and proposes some allocation examples such as team 17.5%, investors 17.5%, early community (airdrop) 5%, ecological incentives 10%, and fiscal 50%.Liquifi’s follow-up report, although using different classification definitions, came to similar conclusions.There is also the so-called “fair issuance” exception, where tokens are offered to all participants in a fair and transparent manner, so no distribution will be made to the team, investors or any specific stakeholders in the initial stage.Yearn Finance adopts this fair issuance method, with its YFI tokens not pre-allocated, and anyone can obtain their initial token supply by participating in its initial liquidity pool.

Distribute tokens to key stakeholders

A portion of the token supply will usuallyThis is done in a variety of ways, including raising funds or for community incentives, through pre-sales or rewards.

For tokens that are not pre-allocated for initial issuance, such as tokens located in the ecosystem incentive pool and finance department, they can be continuously allocated to relevant stakeholders based on the project’s governance process.

If tokens are distributed in large quantities at extremely low or no costs, especially in token issuance plans accompanied by inflation expectations, adverse selling pressure may arise and interfere with the supply and demand relationship of the token.To address this problem, strategies derived from game theory and economic mechanism design theory have been adopted, and we will further explore these strategies in Part IV of this series.

Distribute tokens to investors

Distribution of tokens to private investors is usually done through discounted sales in exchange for their high-risk investments in the early stages of the project.Distribution of tokens to public investors faces greater challenges because of legal uncertainty.Initial token offerings (ICOs) were once a widely adopted method of crypto crowdfunding, but this method has been restricted due to strict regulatory scrutiny.In 2022, people usually refer to the initial token issuance as a token generation event (TGE).TGE usually makes tokens open to the public and may take many forms, such as initial DEX offering (IDO) and initial exchange offering (IEO).Some teams come up with some very creative naming to attract public participation in raising initial funds.For example, the JPEG’d project allows those who have valued NFTs, such as Cryptopunk holders, to use their NFTs as collateral to obtain loans.Before the project was launched in late April 2022, the team held an event in February called “Token Donation Event.”They invite the public to donate Ethereum (ETH) to the project, and in return, these donors will share 30% of the project’s native token, JPEG, in proportion.

Distribute tokens to communities and teams

Many crypto projects will distribute tokens for free to relevant community members and core teams in the early stages, aiming to launch the community or reward core teams.

Airdrop is a common way to distribute tokens for free.Before successfully performing airdrops, the project needs to first determine the qualified recipient address.While obtaining the address of the core team is relatively simple, determining the address of a qualified community member can be more difficult.This decision is usually made by project governance agencies, whether it is a centralized team or a decentralized governance agency.

In the early stages of the project, many projects use the time when community members begin to interact with the product as the primary basis for identifying loyal users.For example, Uniswap airdrops the token to a wallet that has had at least one interaction just before the token release date.

A simple time-based qualification mechanism has the disadvantage that it may attract people to satisfy the empty investment space by creating multiple wallets and conducting simple bot transactions, who are not actually real users, but more like Sybil attacks.the person.Therefore, subsequent airdrops raise the threshold for participation and require more meaningful interactions with the protocol, such as duplication and more real usage patterns, thus achieving overall improvements.

The airdrop of the Ethereum Name Service (ENS) is assigned to people who have registered the “.ETH” domain name before a specific date.Since domain name registration is a unique process involving multiple steps and cost, this reduces the possibility of manipulating qualification procedures.

Rarible is an NFT trading platform that initially allocates weekly airdrops based on buyers and sellers’ trading activities. This seemingly reasonable approach was quickly used by a large number of order brushers to increase their trading volume and gain more.award.This behavior ultimately leads to the voting decision of protocol governance to terminate this reward distribution mechanism.

Optimism’s latest airdrop further refined the qualification mechanism, covering multiple rounds of airdrops, and emphasized the behavioral advantages of target users.Its first airdrop covers active early adopters of the Optimism system.Since Optimism is Ethereum’s second layer protocol, its airdrops are also targeting active Ethereum participants who are highly consistent with the project’s goals, such as DAO voters, multisigners, Gitcoin donors, and users who are still active in Ethereum.

Accurately defining the target stakeholder group is one way to identify the expected airdrop population; another is to screen out unwanted members from existing groups, which are usually fake accounts created by Sybil attackers.For example, HopDAO provides rewards to the user community that reports Sybil attackers and allows Sybil attackers to report their misconduct on their own so that these attackers can still receive the allocated rewards.If they do not surrender but are reported by others, they will find nothing.

Token allocation standards can also consider the actual performance of users providing services to the network.The Covalent protocol is a distributed blockchain data access network that uses tokens to pay fees to nodes that provide network services.Additionally, the best performing nodes may receive additional bonus multiples in terms of latency and reliability.

The effectiveness of airdrops has been questioned.In addition to airdrops, another way to achieve token allocation is to lock the position and airdrop.Unlike airdrops, locking airdrops require the receiver to lock some crypto assets for a period of time to receive token rewards, thus bringing opportunity costs to the token recipients.This approach is often beneficial to the project.For example, the decentralized exchange lock-up airdrop of Astroport requires community members to lock LP tokens to receive ASTRO token rewards.This process helps the protocol accumulate liquidity and simultaneously implements initial token allocation.The recipient of the locked airdrop is actually “earning” the tokens, a variant of the “staking and participation” value allocation model we will discuss in Part 5 of this series.The difference is that the locked assets are usually not the reward token itself (if the reward token has not been distributed), and if there are no other activity requirements, no penalty is involved.

Handle initial token liquidity

Liquidity is a key factor that determines the difficulty of users buying and selling specific tokens.The liquidity of a Web3 project can be compared to the bandwidth of a Web2 project.If the token economy is compared to a real-world city, available liquidity is like a highway connecting the city with the outside world.It is basically an entrance to the token economic world.Inadequate liquidity may result in a “liquidity premium” that causes the token to trade below its intrinsic value.Methods to improve liquidity include leveraging professional market makers in centralized exchanges and establishing deep liquidity pools in decentralized exchanges.But for the newly launched tokens, launching initial liquidity is a major challenge.

Determine liquidity pairing

Before the token is listed, we need to decide which existing token should be paired with.A common practice is to choose the infrastructure tokens of the blockchain as the pairing object.For example, if the project is on Ethereum, ETH is usually chosen as the pairing.The reason for this choice is that infrastructure tokens are usually the most widely used in the blockchain ecosystem, and paired with them can maximize the effect of initial liquidity.Another popular option is to pair with stablecoins, such as USDC, which is more convenient for coin holders who want to reduce volatility.While creating multiple liquidity pairs can make new tokens easier to obtain, this will also spread the overall liquidity of the new tokens into different pools.If the start-up capital of the project is limited, it would be wiser to concentrate on a few major pairings.

Choose a liquidity exchange

Tokens can be listed on multiple exchanges.Binance, FTX and Coinbase are among the largest centralized exchanges.Each blockchain ecosystem also has its main decentralized exchanges. For example, Uniswap is the largest on Ethereum, while PancakeSwap is the largest on Binance Smart Chain.Centralized exchanges usually have stricter standards for token listing than decentralized exchanges.Many projects also hire professional market makers to reduce trading slippage and provide deeper order books to further improve liquidity.

Initial price discovery

When the token is sold publicly on the exchange, we need to set an initial price.Liquidity Guide Pool (LBP) is a method of determining the initial price.The way LBP works is to start with a higher price, and without a buyer, the price will drop to what people think is suitable for purchase.In addition to providing a license-free price discovery mechanism, this approach also helps raise funds in the process, similar to public pre-sales.The funds obtained through the LBP process can be used to supplement the liquidity required for the token to be listed on the exchange later.Balancer provides popular LBP services, while Copper provides a user-friendly interface to participate in Balancer’s LBP.Delphi Labs also designed Lockdrop + Liquidity Bootstrap and applied it to projects such as Astroport and Mars.

Without a suitable public price discovery mechanism, the project needs to directly estimate the value of the token, and at the same time, it needs to balance multiple factors, such as the number of tokens initially issued, the initial liquidity funds and the preset inflation rate.

Increase initial liquidity

When tokens are released, teams often want to build liquidity beyond their own financial resources.Therefore, many projects encourage external liquidity providers to supply the required liquidity trading pairs and pay with newly issued tokens from the project.These new tokens for liquidity providers play a rent-like role, usually derived from the ecological incentive portion of the token allocation table.A major drawback of this model is that the liquidity of these leases is similar to mercenary capital, and the providers are often not loyal to the project itself and may quickly sell their tokens in search of other opportunities for higher returns.This practice is called profit farming.According to Nansen 2021 data, 42% of earning farmers quit the day the project started, about 16% left within 48 hours, and by the third day, 70% of users had withdrawn.This cycle of farming and selling has caused token prices to plummet, further reducing farmers’ earnings and accelerating their pace of leaving the liquidity pool.therefore,This liquidity strategy is only effective in the short term, usually just after the token is issued.

Long-term liquidity holding

A more sustainable long-term liquidity solution is that the project itself holds enough token liquidity, which is called the liquidity owned by the protocol.Rather than using tokens for lending liquidity, sell tokens at a discount and use these tokens to buy liquidity from third parties.OlympusDAO promotes this concept and helps other protocols implement the process through its Olympus Pro service.The liquidity owned by the protocol is the core theme of DeFi 2.0.

Summarize

This article continues our discussion of the tokens in Parts 1 and 2 “Why, when, what, where, who”.We delve into several key aspects of “how to design tokens”, including determining the number of different tokens required, the generation and configuration of token supply, distribution of tokens to key stakeholders, and building the flow of tokenssex.In the upcoming fourth part, we will focus on supply and demand dynamics to complete the final link of the W5H framework.The dynamic balance of supply and demand relationships is a key factor in ensuring the sustainability of token projects.

appendix:

Case Study: How to determine how many different tokens a project requires

We apply the steps mentioned in the previous chapter to evaluate several decentralized stablecoin design projects and demonstrate this process.

The core goal of a stablecoin is that its value can be pegged to fiat currencies such as the US dollar.We can clarify the following specific goals (O1 to O4), which can be achieved by using tokens in a decentralized stablecoin system:

O1: Provide stablecoins as payment method

O2: Regulates the price fluctuations of stablecoins and keeps them pegged to the US dollar

O3: Governance protocol, determines system changes, such as adjusting adjustment mechanisms and parameters

O4: Ensure the security of the blockchain infrastructure that deploys stablecoins

Following these steps, we start designing a separate token for each target.Specifically, we call them T1 tokens for O1, T2 tokens for O2, T3 tokens for O3, and T4 tokens for O4.How can we combine them?

Method A: Suppose we want to build on Ethereum so that stablecoins can be directly interoperable with the Ethereum ecosystem.This means that the T4 token is ETH.So what should I do with tokens from T1 to T3?At least one token representing stablecoin products is needed, so T1 tokens are needed.In addition, the link between T2 and T3 token stakeholders was noted.Users involved in the linkage adjustment process may also be concerned about adjustment and optimization of the adjustment mechanism.This shows that the interests of T2 and T3 token stakeholders are highly consistent.Therefore, it may be possible to merge them into one.Is there a solution?MakerDAO gave the answer.MakerDAO has two separate tokens, one is the stablecoin DAI (T1) and the other is the MKR token (T2 and T3) used to regulate DAI pegs and governance.

Method B: Again, our target list.Obviously, the T1 token is required because it directly represents the product itself.If we choose to build on Ethereum, then T4 will be held by ETH.In Method A, we have merged T2 and T3 into one token.However, the interests of stakeholders of T1 and T2 are also aligned, because maintaining the stability of stablecoins is exactly what stakeholders of T2 are pursuing.So, is it possible to use a token to satisfy the functions of T1 and T2 at the same time?The AMPL protocol provides an example.In this protocol, the AMPL token is both a stablecoin (T1) and is also used directly to regulate its anchoring (T2).In addition, it uses a separate governance token, FORTH (T3).

Method C: What would happen if the team wanted to create their own blockchain instead of deploying stablecoins on existing blockchains?T1 tokens are still required.Both T2 stakeholders responsible for regulation and T3 stakeholders responsible for governance are committed to maintaining stablecoin pegs.At the same time, T4 stakeholders responsible for ensuring blockchain security also hope that the stablecoin application will succeed.So, can we consider combining T2, T3 and T4 into one token?This is exactly the way the TerraUSD (UST) project takes.UST, as a stablecoin (T1), its underlying blockchain, Terra, is a PoS chain supported by infrastructure token LUNA (T4).At the same time, LUNA is also used for USD pegging regulation (T2) and governance (T3) of UST.

Through these examples, we can see that achieving the same set of goals can take multiple different token combinations.

How to reflect the “principle of consistency in the interests of important stakeholders” in the above design?In these three cases, none of the design combines the stablecoin itself (T1) with its governance (T3).This may be because stablecoins, as trading tools, are usually frequently circulated.The number of tokens people hold more reflects their demand for transaction volume than their willingness to participate in governance.This means that the interests of users of stablecoins (stakeholders of T1) and governors of stablecoins (stakeholders of T3) are not exactly aligned (although if stablecoins fail, they will all be damaged, so they do havesome common bottom line interests).In contrast, there is a more obvious consistency of interest between regulators of stablecoins (stakeholders of T2) and governors (stakeholders of T3).

We can also see the consequences of merging tokens at different levels of the network hierarchy, such as the difference between infrastructure tokens and application tokens.For example, when an application token acts as an infrastructure token that protects the blockchain, if there is a problem with the application token, it may cause damage to the entire infrastructure.This is exactly what happened in the Terra UST/LUNA crash event.LUNA tokens are used to protect the Terra blockchain (as an infrastructure token) and to maintain the US dollar peg of UST stablecoins (as an application token).When UST decoupling results in the LUNA value being almost zero, the network’s incentive verification system cannot continue to operate.The team had to pause the network several times and take measures to prevent the opponent from taking over the network.If the blockchain verification token is separated from the application token, or the application is deployed on an existing blockchain that has been tested, the protocol may reduce at least one attack factor in this turmoil.

Finally, decisions about the number of project tokens do not guarantee the basic soundness of tokens or projects.The success of the token depends on the effective integration of all components of the system.Take UST/LUNA as an example. Even if the LUNA token is only used as an application token, the project is still unsuccessful due to the flaws of the basic design.