Author: Gryphsis Academy

summary

-

The Ethena protocol’s revenue source is the spot pledge income+short position capital rate income. The introduction of the btc mortgage is introduced to the diluted pledge yield.

-

Increasing mortgage varieties are the only way for Ethena to develop for a long time, but it means that long -term interest rates may be low.

-

At present, the insurance funds of the agreement are not sufficient enough, and there are high risks.

-

Ethena has a natural advantage in the squeeze that occurs when facing negative funds.

-

The total amount of Open Interest on the market is an important indicator to limit USDE issuance.

-

The user’s confidence in the project is insufficient. If the high yield starts to decline, the project TVL will gradually decrease.

-

High TVL, low insurance fund, the project party must increase the extraction rate of insurance funds (at least 30% or higher) to supplement insurance funds as quickly as possible, but under the current decline in the income of funds, usersThe yield is even worse, which may exacerbate the first consequences.

>

Ethena is a stabilized currency protocol built on the Ethereum blockchain. It provides a “synthetic US dollar” USDE through Delta neutral strategy.

The working principle is: the user stores STETH into the protocol to cast an equivalent USDE.Ethena uses OES settlement (OES) solution to map STETH balance to CEX as a margin and short -term ETH perpetual contract.This investment portfolio realizes Delta neutrality, that is, the value of the combination does not change with the price fluctuations of ETH.So theoretically USDE achieved stability of value.

Users can pledge the USDE to the protocol and cast Susde, holding SUSDE to obtain the income generated by the funding rate.This income once is as high as 30%, which is one of the main means for Ethena to take over.

As of 2024/9, the yield of holding SUSDE was 15.3%, and the total circulation of USDE reached 2.29 billion US dollars, accounting for about 1.43% of the total market value of stable coins, ranking fifth.

>

In the Ethena protocol, both the short position of the STETH mortgage and the ETH perpetual contract will generate income (derived from the funding rate). If the comprehensive yield of the two positions is negative, the insurance fund in the Ethena protocol will make up for the loss.

What is funding rate?

In the traditional commodity futures contract, the two parties agreed to a delivery day, that is, the term of a physical exchange, so when the futures contract is about to reach the daily date, the futures price will be equal to the spot price.However, in digital currency transactions, in order to reduce the cost of delivery, the form of sustainable contracts is widely used: compared with traditional contracts, the delivery link has been canceled, resulting in the relationship between futures and spot.

In order to solve this problem, the funding rate was introduced, that is, when the price of perpetual contracts is higher than the spot price (the base difference is positive), the amount of funds pays the short -term payment from the short -to -short payment (the funding rate is proportional to the absolute value of the basis);When the price of permanent contract is lower than the spot price (the base difference is negative), the short -term payment rate is paid to the bulls.

Therefore, when the price of permanent contract is deviated from the spot price (the greater the absolute value of the base difference), the greater the capital rate, and the stronger the suppression of the price deviation.The funding rate has become a connection between the medium -term and spot prices of perpetual contracts.

Ethena holds ETH airdrops and STETH. The income comes from the capital rate and pledge income. When the comprehensive return rate is positive, the insurance fund will be stored in part of the income to compensate users when the comprehensive income is negative.

In the current bull market, more emotions are significantly higher than short, and the demand for multiple orders in the market is greater than the demand for empty orders.The Delta risk of the spot mortgage in the Ethena protocol is hedged by short positions, and the short position held can obtain a large amount of capital rate income. This is why the Ethena protocol generates high -risk high returns.

>

>

Before the appearance of USDE, the stablecoin project on the Solana chain UXD also used the same way to stabilize the currency, but the UXD used hedge on the DEX contract exchange, which also laid the foreshadowing for UXD’s failure.

From the perspective of liquidity, the centralized exchange accounts for more than 95% of the unsuitable contracts. In order to expand the size of the USDE to a billion level, Ethena is the best choice: the large -scale issuance of the USDE issuance is issued at USDE issuance.During the growth, or when the crowding occurs, the price of Ethena’s short position will not cause much disturbance to the market.

>

Because Ethena uses the centralized exchange setting period, it will inevitably generate new centralized risks, so Ethena introduces a new mechanism OES to hand over mortgage to third -party custody (Copper, Fireblocks).Any mortgage is similar to saving the user’s mortgage into one more wallet, maximizing the centralized risk.

>

Insurance funds are an important part of the Ethena protocol. It transferred some income of STETH and ETH short positions to the timing of the time to be released when the comprehensive income rate of the timing was released to maintain the stability of the currency.

>

Figure 1: USDE floating yield simulation

In 2021, the high USDE yield in the bull market reflects the strong bullish demand. The multi -header pays 40% of the capital rate of funds per year.With the beginning of 2022, the funding rates often fall below zero, but it does not continue to be negative, and the average value can still be maintained above 0.

In the second quarter of 2022, the failure of Luna and 3AC on the impact on funding rates was surprisingly small. The short -term downturn made the capital rate hovering around 0 for a while, but it quickly returned to the positive value.

In September 2022, Ethereum changed from POW to POS, causing the largest black swan incident ever in history. The funding rate once fell to 300%. The reason was that in this conversion, users only need to hold ETH spot in stockYou can get short rewards, which has led to a large number of users to obtain a stable airdrop return. Not only does it hold ETH spot bulls, but also hold ETH short positions to maintain a large number of ETH spot suits.

A large number of short pouring led to ETH sustainable contract funding rates plummeted in a short time, but after the end of the short release, the capital rate rate quickly returned to the level.

The closure of the FTX in November 2022 also led to the level of funding rates to -30%, but it did not continue, and the funding rate quickly returned to the positive value.

Through historical data calculations, the average income of USDE has been maintained above 0, which demonstrates the long -term feasibility of the USDE project.The short -term normal market shock or black swan incident has caused comprehensive income to be less than 0, and sufficient insurance funds can transition the agreement smoothly.

>

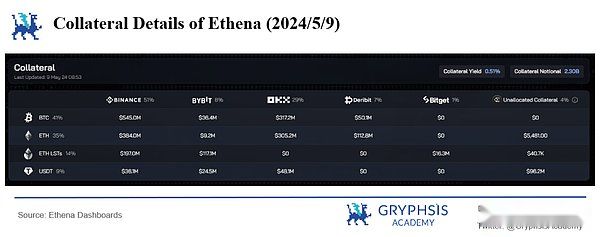

Starting from 20244, users can mortgage BTCs in the Ethena protocol to cast USDE stablecoins. As of 2024/5/9, the current BTC mortgage has accounted for 41% of the total mortgage.

>

Figure 2: 2024/5/9 Ethena collateral details

>

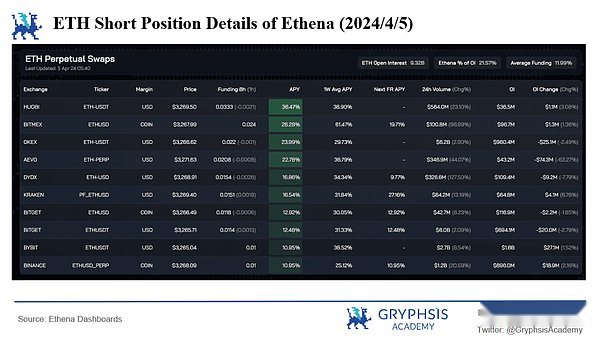

Figure 3: 2024/4/5 Ethena protocol details of ETH short position

On the eve of Ethena accepting BTC as a mortgage, Ethena’s total empty position has accounted for 21.57% of the total unsupering contract.Although the centralized exchange is strong and Ethena holds ETH short positions on multiple exchanges, the rapid growth of USDE issuance has caused the centralized exchange to provide sufficient ETH perpetual contract liquidity. Ethena is urgentNeed a new growth point.

Compared with liquid pledges, BTC does not have native pledge income. If BTC is introduced as a collateral, the pledge yield contributed by STETH will be diluted.However, the BTC permanent contract in the centralized exchange exceeds $ 20 billion. After the introduction of the BTC mortgage, the USDE’s short -term expansion capacity will increase rapidly, but in the long runThe growth rate of quantity is the main factor to limit USDE growth.

>

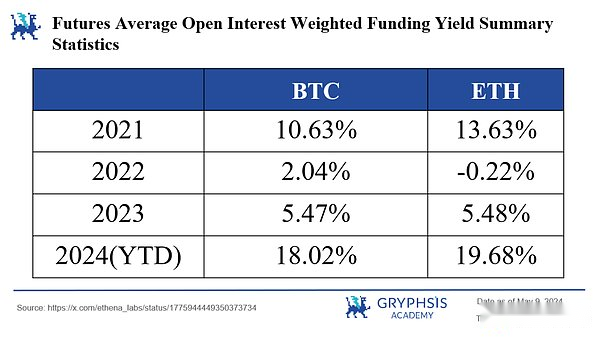

Figure 4: Average capital rates of each year

Although the BTC mortgage dilutes the pledge income of STETH, through historical data calculations, the average funding rate of BTC perpetual contracts is lower than ETH and higher than ETH in the bear market., Increased the degree of diversion of investment portfolios, and lower the risk of USDE from anchoring in the bear market.

>

>

At present, the yield of SUSDE has rapidly fell from 30%+ to about 10%+. It was not only affected by the overall emotions of the market, but also the impact of a large number of short positions brought by the rapid expansion of USDE on the market.

As we all know, the growth rate of USDE horror comes from the funding rate of the high -end funding rate in the bull market, but the USDE, as a stable currency, still lacks application scenarios, and existing transactions are only related to some other stablecoins.Therefore, most of the USDE holders hold USDE only to harvest high APY and airdrop activities.

Although the mechanism of the insurance fund is to enter the comprehensive negative interest rate, users who provide STETH will be redeemed when the comprehensive income is lower than the STETH pledge yield; users who provide BTC will be more cautious. As the foundation difference gradually decreases, the funding fee will be gradually reduced, and the funding fee will be gradually reduced.The rate of income continues to be sluggish. When there is no high APY, a large amount of redemption may be generated after the second round of airdrop activity. For reasons, you can refer to the dilemma that the Bitcoin L2 is also facingIt is regarded as the target of value storage, which is extremely harsh on funding security.

Therefore, the author believes that if Ethena’s second quarter airdrop activity is over, if the USDE’s stable currency application scenarios have not achieved breakthrough development, the capital rate will gradually reduce the capital rate, and the USDE is likely to be sluggish.

>

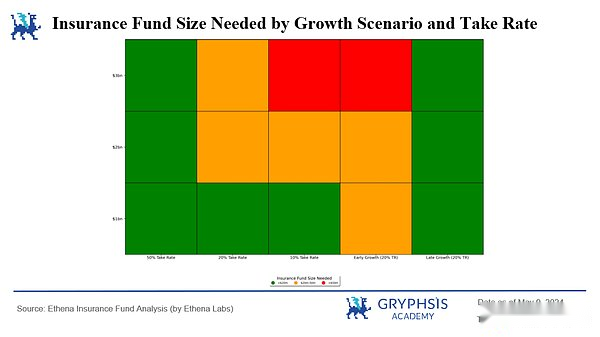

Ethena officially concluded that the following conclusions of insurance funds were obtained through analog calculation:

>

Figure 5: The scale of the insurance amount of the initial required insurance amount based on the growth scenario and insurance fund extraction rate

In Figure 5, green, yellow, and red represent the size of the initial insurance funds less than 20 million US dollars, between 20 million to 50 million US dollars, and greater than 50 million US dollars to ensure the security of funds.

The longitudinal coordinates indicate that the amount of USDE issuance is expected to be finalized within two and a half years (2021/4 ~ 2023/10).In the first three horizontal coordinates, when the amount of USDE issuance is linearly increased, the extraction rate of insurance funds is set to 50%, 20%, and 10%.The fourth of the horizontal coordinates indicates that when the amount of USDE issuance remains unchanged after the exponential growth in the first year, the extraction rate of the insurance fund is set to 20%.The fifth indicator of the horizontal coordinate indicates that when the amount of USDE has always maintained an index type growth, the extraction rate of the insurance fund is set to 20%.

From Figure 5: For a starting insurance fund of $ 20 million, 50% of the extraction rate is very safe, and almost all cases and growth can make insurance fund capital sufficient.If a black swan incident occurs before the insurance fund has the opportunity to undergo capitalization, the premature index growth may be dangerous to the solvency of the insurance fund.At the same time, the late index growth is safer because it provides more time for the growth of insurance funds.

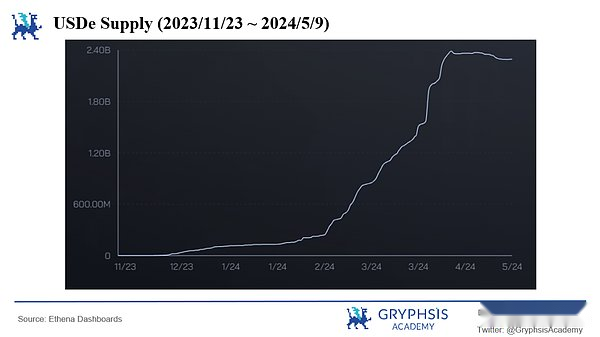

But the actual situation is that the starting insurance fund is only $ 1 million. The supply of USDE is much faster than the early index type in the case of Early Growth in the model.At present, 38.2 million US dollars (only 1.66%of USDE issuance) are increased in the past month.It can be seen that the problem brought about by the rapid distribution of USDE is that the early insurance funds of the Ethena project are serious compared to the official model calculation.

Insufficient insurance foundations have two consequences:

>

Figure 6: 2023/11/23 ~ 2024/5/9 USDE Issuance

>

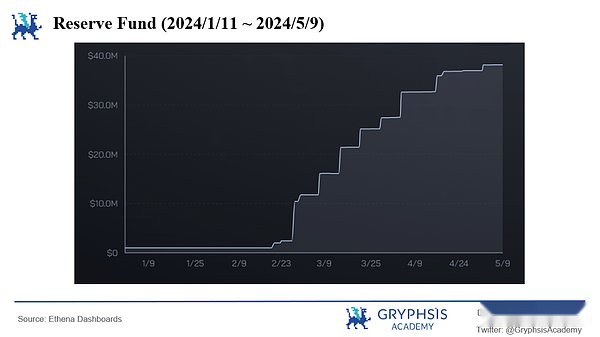

Figure 7: 2024/1/11 ~ 2024/5/9 Insurance fund quota

>

With reference to the ETH POW Arbitrage incident in the third quarter of 2022, the capital rates fell hugely in a short period of time, and the annualization exceeded 300%.In such black swan incidents, it is basically inevitable that the USDE is running, but the unique mechanism of USDE seems to have a natural response advantage.

At the beginning of the sharp decline in funding rates, the crowding may have occurred. Due to the emergence of the crowding, the Ethena protocol needs to return a large amount of spot mortgage to the airdrop bonus. Due to the reduction of the airdrop bonus, the expenditure of insurance funds has also decreased.The insurance fund can maintain longer.

From the perspective of liquidity, when extrusion occurs, Ethena needs to liquid short positions, and in a market with negative funding rates, it means that the bulls are abundant.Passion.

At the same time, the 7 -day cooling period of SUSDE in the Ethena protocol (the mortgage cannot be liquidated within a week of mortgage) can also be used as a buffer when market mutations.

But the premise of all this is the sufficient insurance fund.

>

The total amount of unclean contracts in the market (OI, Open Interest) is always a key factor that restricts the issuance of USDE. It is also the potential risk of USDE in the future. As of 2024/5/9, ETH OI in the Ethena protocol accounts for 13.77% of the total OI., BTC OI accounts for 4.71% of the total OI.The huge short position generated by the Ethena protocol has brought some disturbance to the contract market. The subsequent expansion of the USDE scale will have a certain liquidity problem.

The best way to solve this problem is to increase as much high mortgage as much as possible (the funding rate is greater than 0 for a long time), which can not only increase the upper limit of the USDE supply, but also increase the degree of dispersing the combination and reduce risks.

>

In summary, the Ethena protocol shows its unique stable currency mechanism and sensitive response to market dynamics.Although it is facing challenges such as long -term downturn, insurance funds insufficient and potential extrusion risks, Ethena maintains market competitiveness through innovative off -site settlement mechanisms and diversified mortgage varieties.

With the continuous changes in the market environment and technological innovation in the industry, Ethena must continue to optimize its strategy and enhance its risk management capabilities to ensure the sufficientness of insurance funds and the stability of liquidity.For investors and users, it is crucial to understand the operating mechanism, source of income and its potential risks of the agreement.