Author: Patrick Bush, Matthew Sigel Source: Vaneck Research Translation: Shan Ouba, Bit Chain Vision Realm

summary:

-

Our conclusion is that the second layer of Ethereum is currently crowded, and there are almost no characteristics of winners.

-

Evaluate the second floor of the blockchain through the perspective of developer experience, user experience and technical capabilities.

-

Show the assumptions behind the valuation of Ethereum Layer-2 reaching a market value of $ 1 trillion in 2030.

Overview of blockchain in the second layer

Ethereum’s dominance in the field of intelligent contracts faces a key obstacle: scalability.Although the network provides unparalleled security and decentralization, the transaction costs and processing time will soar as the usage increases.In order to overcome this problem, the second-level solution came into being, and progress such as the nearest fork EIP-4844 is expected to unlock greater scalability for these Ethereum branches.Here, we analyzed a series of Layer 2 solutions from the perspective of transaction pricing, developer experience, user experience, trust assumptions and ecosystem size.

The second floor (L2) blockchain is a connection network running on the main blockchain (such as Ethereum) to improve its ability to deal with transactions.By processing the transaction on the main blockchain, and then reorganizing it to the main blockchain, the L2 solution helps expand the function of the blockchain without affecting its security or decentralization.

As we all know, Ethereum’s current ability is not enough to carry all financial transactions around the world.To be more accurate, the world’s financial system needs to deal with long -term restrictions of about 19.2 USDC or 6.8 UNISWAP transactions per second.However, this is a design limit, because the manager of Ethereum believes that it is best to achieve the resistance of the review system by allowing anyone to run the Ethereum node at a low cost.

As a result, Ethereum limited its chain capabilities to reduce the network needs, data storage requirements, and computer hardware requirements of their nodes.This is actually limited to the number of data bytes that Ethereum can process within a given time.Since the transaction on the blockchain is just a data fragment that the blockchain considers the correct data, the ability of the blockchain can simply process how much can it be processed through it.Useful data to measure.

>

Source: Vaneck Research as of March 15, 2024.

In order to solve these restrictions, Ethereum developers initially proposed a “shard” solution, which involved the division of the blockchain into 64 smaller, interconnected sub -blockchain, called “shard”.Each shard will deal with transactions in their respective containerized sub -blockchain, and then submit activities to prove to coordinate with the parent blockchain for the Taifang.Although this method looks very promising, and some of its components appeared for the first time on Polkadot since 2020, Ethereum developers finally abandoned the sharding plan called Ethereum 2.0.This is because they believe that this is not technically feasible and cannot expand to Ethereum to become the vision of blockchain for billions of users.

Instead, the route map of Ethereum is turned to the second floor (L2) blockchain.These L2 network processing most of the transactions other than the main blockchain of Ethereum only settled the highest value transaction directly on it.This method reduces the load of the main blockchain and enables it to effectively handle more transactions.In this dynamics, Ethereum has accumulated value, because the cost of these settlement must be paid based on ETH; this strategy also strengthens the value of ETH as the real “oil” and provides motivation for the entire interconnected ecosystem.

In essence, Ethereum’s main challenge is that its ability to process, store and calculate data in the form of financial transactions is limited.By transferring and calculating most of the data to the second floor blockchain, the bottleneck of data throughput can be solved.Therefore, the development of Ethereum is now focusing on enhancing its ability to compress trading data from these L2 blockchain.But how does these interconnected blockchain operate and what are their business models?

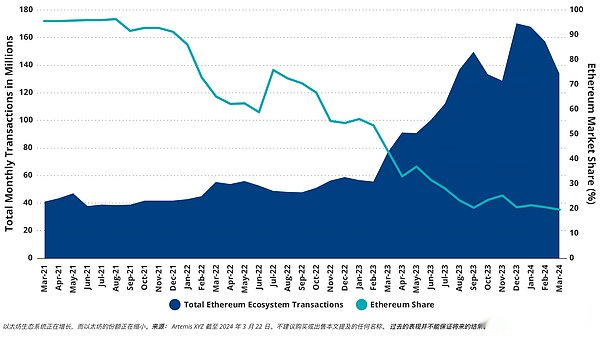

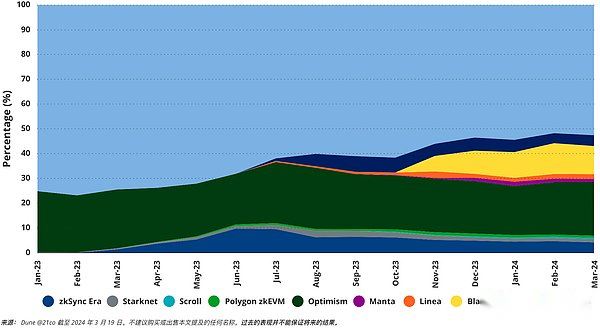

Ethereum ecosystem transaction and Ethereum main network market share

>

Layer-2 in expansion of Ethereum network

The second floor (L2) Blockchain enhances the function of Ethereum by aggregating multiple transactions into compressed packages (called “Summary”).These “trading beams” were published from different time intervals to Ethereum. These time interval was to balance trading needs, security and costs.Therefore, Ethereum is becoming becoming“Blockchain blockchain”.

Each L2 is usually composed of a series of smart contracts on Ethereum. These contracts track the history of L2 trading, promote data transmission between L2 and Ethereum, running fault proof or ZK verification device contract (see more content below), see more than content).And serve as the asset custody between Ethereum and L2.A very powerful computer called “sorter” can ingest and sort all transactions that occur on the L2 blockchain.This is more powerful and cheaper than Ethereum, because L2 runs a very powerful server computer, it only needs to receive transactions and sort it.This dynamic allows L2 to process more data throughout Ethereum.In contrast, the Ethereum transaction processing involves hundreds of thousands of global distribution verification device nodes to send, interpret, and agreed transaction data.Due to the consensus process of Ethereum, this requires more time and involves repeating a computer on each of hundreds of Ethereum nodes.Logically, the ratio of a single computer that handles transactions like a sequencer is scattered in global and poorly capable computer systems is much cheaper and faster.And use hundreds of thousands of CPUs to deal with blockchain transactions.

Types of Layer-2: Optimism Summary (Oru) and Zero-knowledge Summary (ZKU)

There are two main types of L2 connected to Ethereum: optimistic summary (oru) and zero -knowledge summary (ZKU).Both of them were originally settled in Ethereum to settle their ledger balance or “status” by sending a compressed version called “Merkle Root”.Oru also released a batch of compressed transaction data to verify and track the change of ledger over time.

The settlement in the second -layer blockchain (L2) can be compared to the score of the baseball game in a row, and the transaction data is used as a detailed game data.For optimism summary, they follow the principles of optimism, which means that they are considered accurate unless they have proofs.If an entity (such as a high -frequency trading company or a skilled researcher) identifies the incorrect or defective Merkle root, they can submit a fraud certificate to Ethereum (called a fault certificate).There is a 7 -day window (referred to as the “Challenge Period”) to monitor the entity of the ORU fraud.Once the deadline is over, the transaction in the oru will be considered a final transaction.If the failure proves the successful proof of fraud, the intelligent contract that supervises the status of the Oru will restore all transactions to the state before the fraud starts.The challenge period was extended for 7 days, and then each batch of transactions were finalized.

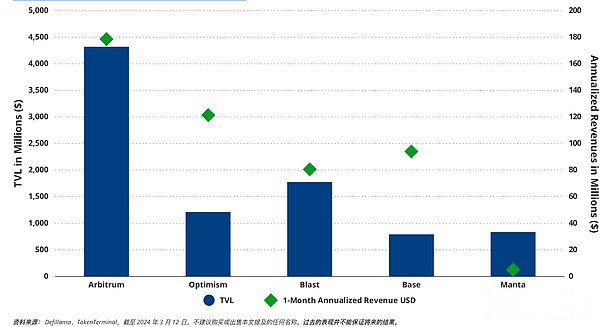

When writing this article, only 4 chains have real -time fraud proof of the 46 L2 tracked through L2Beat.The two of these four belong to Arbitrum’s protection range. Arbitrum has the highest locking total value (TVL) of all L2, which is $ 4.31B, and only allows fraud proof from the white list physical group.

The most popular Oru is Arbitrum, Blast, Optimism, Manta, MANTLE, and Base.

Locking total value (TVL) and annualized income optimism summary (oru)

>

The operation of zero -knowledge summary (ZKU) is similar to ORU, but there is a key difference.Oru submits transaction data Merkle root and status Merkle root to Ethereum, while ZKU only sends a zero -knowledge certificate for transaction data.This is because ZKU does not run under the correct assumption of the state of the submitted state.On the contrary, once the evidence is submitted to Ethereum, the smart contract will verify the authenticity of the ZKU trading package.

Therefore, ZKU has no failure proof, because each state update will generate proof.Unlike oru, once it is proved to be accepted in Ethereum, the ZKU transaction data is considered the final data, so as to ensure the immediately definitive and eliminate the needs of the challenge period.

The most important zku currently is Starkware, ZKSYNC, ZKSCroll, Linea and *C ZKEVM

The basic economics of ZKU and Oru is very similar to the L1 blockchain.When users create activities on their chain and pay Eth to Ethereum, these two types of summary will make money.At present, all L2 is priced at ETH, because this is to settle the transaction data to the tokens needed by Ethereum.

The second floor income model

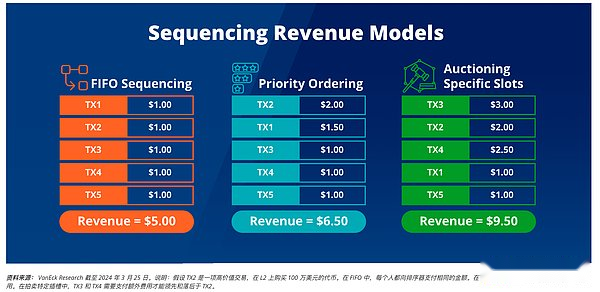

Regardless of the process,It is important to understand that the transaction sorting is valuable, and the blockchain can make money by selling the rights of transactions.The figure illustrates how three different transaction sorting models create different income flows.

>

Section 2 transaction sorting: priority, advanced first -out and auction

L2 charges users to each block contains the transaction fee.It consists of basic costs and priority expenses.Some L2 will charge priority fees, such as Optimism.The priority fee enables users to rank first on the top of the transaction block.In the past 6 months, the top 10 L2 ranked 10th in Ethereum has received $ 232 million in revenue from user transactions.This kind of ability to “cut off the line” by paying the priority fee is conducive to the time -sensitive activity (such as arbitrage transactions).

Arbitrum adopts an advanced FIFO sorting method when the transaction arrives.In some cases, users may prefer their transactions to follow specific other transactions on the block.A common strategy called “reverse operation” involves the transaction immediately after major transactions to obtain arbitrage opportunities with price differences between decentralized exchanges (DEX).More malicious trading ordering technologies, such as “sandwich attacks”, involved the strategic placement of buying orders before user plan transactions, and immediately place selling orders.This manipulation will push the price of the token required before the user transaction is executed, forcing them to buy them at an unfavorable and high price.

On Ethereum, the order is monetized by adding software in the Ethereum verification device software.The software is called Flashbots, which allows verifications to auction the right to order transactions (and insert its own transaction) from external entities.The auction generated a “maximum extraction value” (MEV), increasing the benefits of the verifications and pledges.Although L2 has the potential to monetize MEV through the right to order block order, there is no official L2 officially.However, the trading company may have positioned its server near the L2 server, similar to the practice of stocks and commodity exchanges.

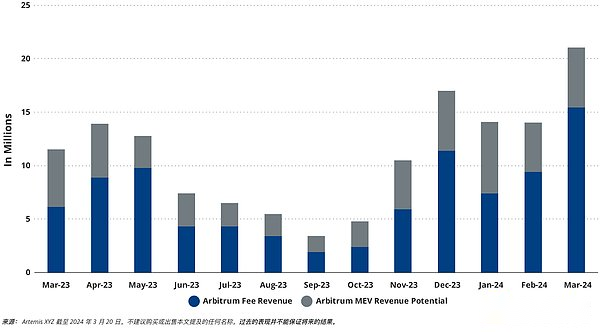

Looking forward to the future, many L2 plans to decentralize their sequencer set, which may involve mortgage tokens -eth may be from Eigenlayer DA or the tokens from each summary.The decentralization of the sequencer can release the new source of income from MEV.In terms of specific circumstances, the average adoption rate of Ethereum’s MEV’s DEX transaction volume is about 4 basis points (BPS), while the adoption rates of other blockchains such as Polygon and Solana are 0.4bps and 3.5bps, respectively.Due to the motivation of tracking and the motivation to conceal profits, these ratio may underestimate the entire range of MEV.By estimated the MEV usage rate based on DEX transaction volume, if Arbitrum’s MEV is captured at a rate of 3.0 basis points, the amount will reach 58.9 million US dollars -57%of Arbitrum’s pure charging income.

Arbitrum income realizes 3 basis points in DEX transaction volume

>

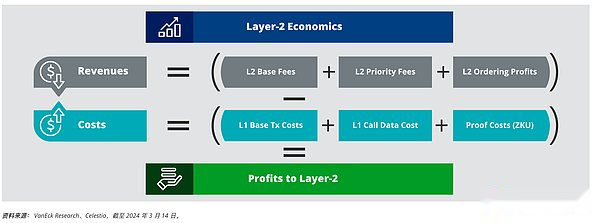

Layer-2 chain cost structure

The 2nd layer (L2) is mainly cost to generate costs through Ethereum GAS costs, because they regularly publish transaction data, settlement and proof to Ethereum.However, the cost structure of zero -knowledge summary (ZKU) and optimism summary (oru) is different.Although both are updated on L1, the Oru must pay the heavy data cost on the chain, and ZKU must spend money to prove the generation and verification.In any case, the consequences of relying on Ethereum are that the input cost of L2 will be affected by the fluctuation of the Ethereum block space.In most cases, this cost difference will be passed on to users.However, the profit earned by L2 is very unstable.

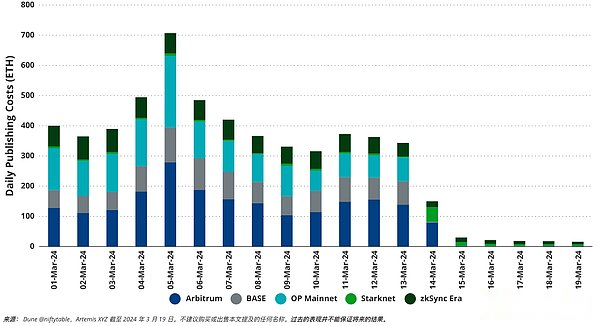

Before EIP-4844, L2 published settlement data and proves as a single transaction to Ethereum. The “message field” of each trading structure was called “call data”.This is a “hacker” behavior that uses an Ethereum standard transaction format to save compressed L2 data.Although this is novel, the price is very expensive.For example, in February, Optimism paid $ 5.7 million, Arbitrum paid $ 7.2 million, Scroll paid $ 6.7 million to publish call data to Ethereum.

>

Compared with ORU, the cost of ZKU is essentially higher, because ZKU submits zero -knowledge certification and calling data to Ethereum.Although Oru may also involve proof costs, these costs are usually outsourced to third parties to challenge the country when needed, so they will not seriously affect the basic costs of Oru.The cost of verifying ZKU’s zero -knowledge certificate on Ethereum may be extremely high.Although Ethereum has made optimization efforts, for example, using native operation code to simplify ZK-ProOF verification, the cost is still very high. For example, Scroll’s ZKU has a certificate of $ 1.1 million in the first 13 days of March.

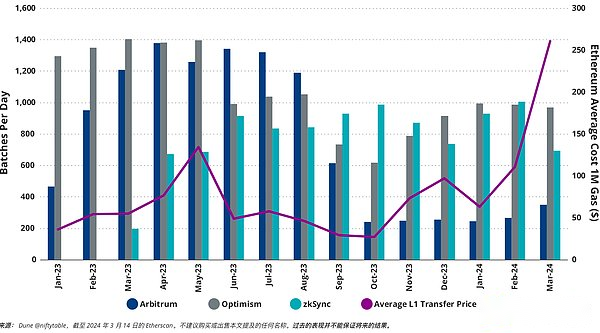

Due to the high cost, the average profit margin of ORU in the past six months was 26.7%, while the average profit margin of ZKU was 21%.Logically, the summary can be sent more transactions with fewer batches to reduce the cost of changing batches.However, the non -frequent batch releases may also be caused by less affairs on L2.In any case, the frequency of L2 batch to Ethereum is a profit leverage that L2 can be pulled, but it is at the cost of sacrificing the user experience.In practice, L2 decides that the batch accounts are based on the number of transactions in a block, Ethereum L1 natural gas price, and the transaction flow of each L2 for calculation.

The cost of settlement costs with Ethereum every day with Ethereum is daily

>

Technically, in addition to the simple “scoring card” solution, L2 can also publish a wider understanding of the situation on L2.The price competition conducted to provide users with the cheapest transactions between L2 has caused L2 to often choose the most economical data to release.Generally, this means that only the “state difference” of ZKU is released, and for the oru, it means publishing highly compressed transaction data.Strangely, although ZKU does not need to release complete transaction data in technology, some ZKUs still do so.StarkNet and ZKSYNC only released “status differences”, while Linea, Polygon, and Scroll released complete transaction data.This is because for browsers and wallets, tracking the blockchain without transaction data may be challenging.Another possibility is that publishing complete transaction data can increase transparency so that anyone can run nodes to track ZKU.

At present, many L2 reduces costs to improve compression efficiency.For example, on February 13, Linea deployed a new compression solution that increased the compression rate on the chain by 10 times, from about about 500 bytes of each transaction to about 50 bytes.By 2024, the average transaction size of other L2 (Oru and ZKU) on Ethereum was 300 bytes.Although compressing transactions may save L2 data costs, it reduces its potential due to the time required to compress the transaction.

L2 chain last monthly margin

>

EIP-4844 solution for L2 data cost: BLOB space

On March 13, 2024, Ethereum passed the Dencun upgrade. There were some important changes. The most important of which was the so -called “Blob Space”.Prior to the upgrade, Layer-2’s main challenge is the high cost related to the release of transaction data to Ethereum.With this point of view, Ethereum solution is a special data layer, commonly known as BLOB space, designed for L2 data release.

This newly established layer provides a targeted trading environment dedicated to receiving data from the L2 network.The innovation of Blob Space lies in its transient data processing -the data released here only retains four weeks before deleting, which significantly reduces the data overhead of Ethereum.Therefore, L2 can choose to bypass the Ethereum layer and directly publish them to the Blob Space.

The Blob Space layer of Ethereum has its own GAS price, following the same rule set as the routine execution layer of Ethereum.As a result, transactions that published data from L2 no longer need to compete for the competition block space with the routine Ethereum.The design of the dedicated transaction layer also makes data costs much cheaper than that of calling data to Ethereum.When writing this article, Data Blob has reduced the cost of using the GAS of L2 (-96%).

Ethereum (ETH) L2 data release cost

>

Layer-2 chain cost structure

The first part of the cost of the chain of the second layer (L2) is the sorter they use to sort transactions.This is basically just a high -end server located in the data center.For the cost of the basic or business entity payment sequencer behind most L2, L2.On the whole, the cost of running sequencer itself is very small. The cost of equipment is about 1,000 to 2,000 US dollars. It may need $ 3,000 to $ 5,000 per month.This cost is consistent for the optimistic summary (oru) and the zero -knowledge summary (ZKU).

ZKU’s less discussion but important cost elements involve the operation of the proof.Different from the sorter that generates the state root, the proofer is responsible for creating a ZK certificate that verified on the Ethereum network.This calculation process usually occurs on cloud computing platforms such as AWS.

According to the decentralized ZK proof project Gevulot, the cost proves will be between “10-20%of the cost of verification of Ethereum”.In addition, these costs change with the transaction volume generated by each L2.ZKU is facing a balance between cost and user experience. You can choose to reduce the frequency of certification publishing to Ethereum as potential cost savings measures.By called recursive process, ZKU proofers can merge multiple proofs into one submission, which can optimize economy by reducing the expensive certification verification on Ethereum on Ethereum while increasing the demand for computing outside the chain.

When writing this article, all ZKU runs his own proof and pays the cost generated directly.However, over time, many people intend to disperse the generation of proof.

Evaluation of 5 key areas of 5 key areas 2nd floor

In our analysis of the key 2 layer, we use five main variables to measure potential success or failure:

-

Transaction pricing -user transaction cost

-

Developer experience -Easily build products and applications

-

User experience -the simplicity of deposit, withdrawal and transaction

-

Trust assumption -activity and security assumptions

-

The size of the ecosystem -how many interesting things can be done

-

Transaction income (including transactions on the blockchain)

-

EstimatedUse the terminal market of the public blockchain to TAM

-

Calculate the actual situationUse the number of tams of the public chain

-

Forecast Ethereum ecosystem public blockchain’s market share

-

The income rate of the terminal market income for the use of the Ethereum ecosystem for settlement and transaction

-

Division of transaction value between Ethereum and L2

-

MEV (transaction sorting on the blockchain)

-

The value of assets (including currencies, securities and digital assets) protected by Ethereum ecosystem will be

-

By estimating the asset turnover rate to our prediction of the value of asset value of the Ethereum ecosystem, to predict the DEX transaction volume in the Ethereum ecosystem

-

Multiplying DEX transaction volume can be obtained by MEV occupation rate

-

Distribution value between Ethereum and its L2

1. Layer-2S transaction pricing

The root cause of transaction pricing is from data compression, data release efficiency, L2 scale, proof cost (for ZKU), and the most interesting combination of each L2.L2 can also arrange the time to post to Ethereum based on the GAS price, but in fact, we have not found experience evidence that supports this possibility.This may be due to predicting that the price of natural gas in Ethereum in the future is generally difficult.

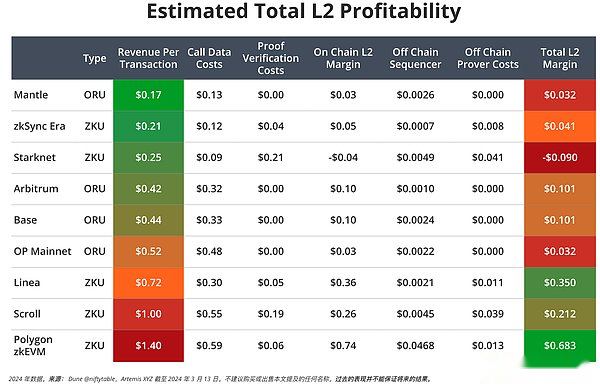

The main difference between pricing economics between ZKU and oru is that the fixed cost of ZKU is higher than Oru.This is because ZKU must pay the proof of Ethereum and the certification verification cost of Ethereum.Prove that generating/verification is a huge static cost. As each proof covers more transactions, the cost will not increase significantly.In contrast, Oru must publish complete transaction data to Ethereum.Although Oru uses different compression mechanisms to reduce data costs, the cost of publishing Ethereum is very expensive.Because the more transactions on the Oru, the more data is required to submit more data to Ethereum, the cost of issuing to Ethereum will increase.However, using EIP-4844, the cost of publishing data to Ethereum has been significantly reduced, and these savings that cause ORU transactions are cheaper.Similarly, Oru can also choose to place trading data on cheaper data availability blockchains, such as CELESTIA, EIGENDA, and Avail.Currently, Manta Pacific and AEVO published transaction data to Celestia.

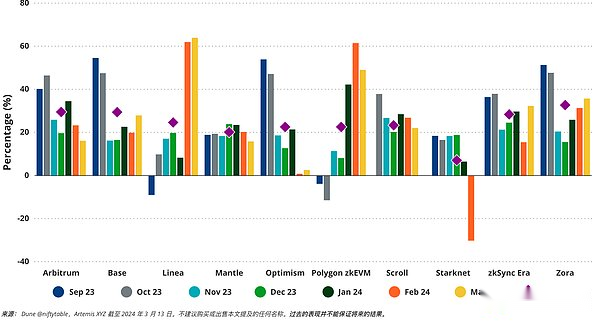

In 2024, the cheapest chain of the average trading cost was Mantle ($ 0.17), ZKSYNC ($ 0.21) and StarkNet ($ 0.25).Each chain can use different technologies to stand out in terms of pricing.Mantle is an Oru that can keep the transaction cheap because it accepts the price below the average margin (19.9%) and use its own data usability (Mantle DA) for a complete transaction batch release, and update its status root to Ether EtherFang, the second one is the least frequent is every 20.7 minutes.ZKSYNC is a kind of ZKU. Because the transaction volume is high (94.9 million), it is the highest among all L2. Therefore, it can be priced at transactions at a low price, which makes it prove that the system is very economical.At the same time, the zku chain StarkNet has the lowest frequency of settlement to Ethereum in the top 10 L2, once every 57.8 minutes, and only release status differences instead of complete transaction data.The savings of these two costs make each transaction settlement to Ethereum at least.Strangely, we estimate that Starknet has lost $ 0.09 per transaction as of March 13, 2024.

L2’s competition differentiation

>

2. Layer-2S developer experience

Developer experience is another important point of Layer-2’s competitive advantage.The simplest fundamental understanding of developers to experience is to achieve EVM compatibility.This means that smart contract code, tools and developer libraries can be transplanted directly from Ethereum to L2.Because Ethereum has a huge development personnel network, this is considered to bring an advantage to each L2.At present, most L2 is compatible with EVM.However, due to the limitation of zero -knowledge proof, ZKU usually has the subtle difference that developers must follow.

Some developers also believe that compliance with EVM compatibility is a disadvantage, because EVM has major restrictions on the blockchain function, and at the same time exclude developers who are more familiar with other computer languages.For example, the StarkNet smart contract is written in a language called cairo, which is more efficient for zero -knowledge expansion of StarkNet.Of course, this is a trade -off. Anyone deployed to StarkNet must understand the complexity of Cairo.Movement Labs is another L2 developer that allows Move language to write smart contracts, which has attracted developers who want to learn MOVE.For those who are more familiar with Solana programming language Rust, Eclipse is building a second -level blockchain running in the Solana virtual machine.

3. Second -layer user experience

User experience is another pillar of Layer-2 competing with each other.The most basic component is to load assets and delete assets from L2.In most cases, there is no significant difference in the employment between L2, but some centralized exchanges (CEX) allow the assets of the machine to be moved to each L2.For example, Kraken allows users to extract USDC to Arbitrum and Optimism, while Coinbase allows transplanted USDC to Optimism and Base.

The incoured point of transactions on the final L2 marks a significant difference between the user experience between the optimistic summary (oru) and the zero -knowledge summary (ZKU).For Oru, the final determination occurs after the end of the fraud challenge, and for ZKU, the ultimate certainty is after the state root and its proof are published to Ethereum.One of the consequences of the final difference is to withdraw from L2.For oru, users must go back to Ethereum after 7 days.For ZKU, the same process may only take an hour, depending on the frequency of settlement and proof of ZKU, and the security system of each chain.Although ZKSYNC publishes a certificate every 6 minutes and is updated every hour, due to ZKSYNC’s security module, users must have a 24 -hour waiting time to receive the Asset Bridge to Ethereum.

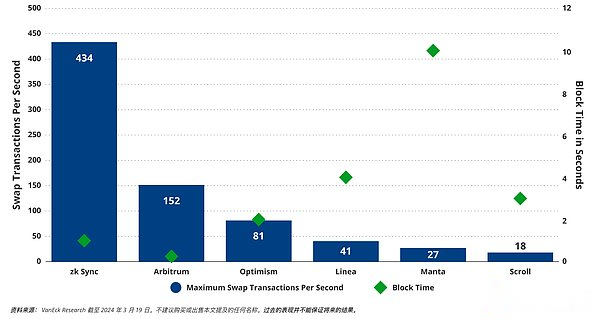

Current throughput and delay

>

When users interact with L2, familiar tools and interfaces are essential.From Ethereum to L2, the familiar wallets and blockchain browsers have greatly improved the comfort of users.This seamlessness is very important, because most L2 uses similar experiences to Ethereum to ensure that personnel who migrate cross -platform migration have the smallest learning curves.In the field of quantified user experience indicators, delay and throughput are particularly prominent.Delay refers to the time required by the network after the transaction is submitted, while the throughput measures the ability of the network to deal with transactions per second.

The slowest block time or round -trip time (RTT) -The duration of user transactions to the sequencer and receiving recovery confirmation -usually defines the delay of L2.For example, Arbitrum has a very low delay potential of 0.25 seconds. Although the actual delay may change according to the geographical factors and the distance between the user and the sequencer, the sequencer is located in the Silicon Valley data center.

ZKSYNC is famous for its highest theoretical throughput and can handle up to 434 exchange transactions per second.However, delay and throughput are adjustable parameters in the L2 network.

The current bottleneck of ZKU is that the proofer handles the speed of transaction transaction, while Oru is limited by transaction data compression efficiency and Ethereum absorbing these data.At present, L2 voluntarily restricts its throughput and is consistent with the capacity of Ethereum.If L2 should make full use of Ethereum’s block space (Considering the current data limit of Ethereum is about 937.5KB per block, plus 375kb from three data BLOB), theoretically expand to each block can be extended to each blockAbout 1.3 MB, or 110kb per second.

For a specific L2 like ZKSYNC, the average transaction is 62 bytes per transaction, and the full use of the Ethereum block space may surge to 1764 transactions per second.In contrast, an oru like ARBITRUM has an average of 255 bytes per transaction, which can reach the processing rate of 429 transactions per second under the same conditions.

By integrated data availability blockchain (such as CELESTIA) can further increase throughput.However, this method has caused people to worry about harming the safety of users, as replacing blockchain may not be able to provide security guarantees at the same level as Ethereum.The choice of expanding throughput in this way is a delicate choice. It needs to be balanced between the inherent safety provided by the improvement of the improvement of the improvement performance and the stability of Ethereum.

4. Trust assumptions of the second level

>

L2 has a large difference in security and activity provided by users.Security refers to the attributes of the blockchain to ensure that only the account owner can access his/her assets, and active is to ensure that the assets can be used to ensure that the assets can be used.Since L2 depends on a single sequencer, the sequencer is both ordered to settle the block and “propose” to settle the L1 (Ethereum). Therefore, the faulty of the sequencer is the most concerned issue for L2 users.This is because each L2 currently runs a sequencer. If it fails, the L2 cannot handle transactions.Although the assets will not be stolen when the interruption occurs, users cannot access them before the interruption is resolved.At the same time, if the malicious entity can take over the sequencer, they may create fraud transactions to take the assets from L2.The current weakness of all L2 is that they only run a sequencer each, and the sequencer is usually concentrated by the foundation behind L2.

L2 manufacturer realizes the problems caused by the faulty of the sequencer or the reception, and some manufacturers have implemented a new type of safety valve.These vary from L2 and their security.What makes things complicated is that some of these security measures provide possibilities for other attack fields.Some fences created to protect users include allowing users to delete assets under certain conditions, use L1 host to submit L2 blockchain transactions, and even propose L2 blocks.In most cases, when a significant failure occurs somewhere in the L2 system, these are the case.

Some L2 is developing a framework for anyone who can become the sequencing person, and allows multiple sequencers to take turns sequencing.This will be accompanied by people who run the sequencer to establish economic bonds (likely to be each L2 native currency) to punish cheaters.ESPRESSO, ASTRIA, and Fairblock are project examples for building software for decentralized sequencers.At present, L2 Metis has gone the farthest aspects of decentralized sequencers on L2.Metis’s community recently passed a governance vote that voted to create a decentralized sorter and allow the framework of multiple sorters.

The next point of the trust that we discuss above assumes that changes are called “data usability”.ZKU provides the correct status update evidence, and the evidence provided by oru allows anyone to prove that the status update is incorrect.However, in these two cases, it is important to understand the source of data to generate ZKU or Oru.Ideally, these data are easily “available” on L1 (Ethereum) so that anyone can verify the basic data of generating proof.Blockchains such as Immutable X and Metis preserve complete transaction data in other positions.Although ZKU does not need to publish complete transaction data, chains like Linea and Polygon ZKEVM need to publish complete transaction data, and StarkNet and ZKSYNC only release status differences.In addition, L2 publishes data to Ethereum, while others are published to a special data availability blockchain (such as CELESTIA).Publishing data on other chains can be said to make L2 security lower than Ethereum because it introduces new trust assumptions.

Another interesting dynamics of Oru is that there is almost no one that can prevent fraud in terms of current situation.This means that anyone who uses them will be reviewed by the sorter (the transaction is not completed).Arbitrum is an exception that allows fraud to prove it.But even in Arbitrum’s cases, only entities listed on the list can submit fraud evidence.On the other hand, ZKU relies on proofers (different entities from sorters).If the ZKU proof fails, some chains allow users to submit their own certificates (only zero -knowledge mathematics!), So that the transaction is included in L2.

In any case, there are many problems in the second floor in terms of trust assumptions.However, they currently have hundreds of thousands of daily active users. Therefore, no one will care about before major problems.In order to simplify our views on a series of guarantee measures taken by L2, we rank them from the highest risk to the lowest risk, and find that Arbitrum is the gold standard (although it is still not enough).

5. Layer-2S ecosystem scale

L2’s bridge TVL

>

The most important competitive factor of L2 is the ecosystem created by each L2.Blockchain is a market for services and digital products.The more useful things do on the blockchain, the greater the value generated through user transactions, the demand for its original currency and the network effect.Unfortunately, the indicators of measuring blockchain activities do not always be correctly transformed into the value of the blockchain ecosystem.The application of Goodhart believes that once a certain indicator becomes important in cryptocurrencies, these indicators are more likely to be manipulated.When we consider the airdrop farmers, this rule becomes more ironic, and they are conducting meaningless activities for free airdrops to obtain tokens.

Generally speaking, it is important that users are willing to bring value to the blockchain and participate in meaningful activities to generate costs.In this regard, Arbitrum, Optimism, and BLAST have stated that they have an ecosystem that is very important for users because these users have connected $ 16.3B, $ 7.85B and $ 2.43B on each user bridge.In most cases, Layer-2 generates user interests and activities through the airdrop of its native token.For example, Optimism has presented nearly 25% of its current floating supply volume to users in the form of activity airdrops.Arbitrum has presented to tokens to individuals who have used more than $ 1.84B to individuals who have used Arbitrum.BLAST further uses this concept to attract the value of the bridge, provided that Blast itself and the team built on BLAST may be airpaced to the tokens.In conceptual point of view, Layer-2 competes for free tokens, and the value of these tokens increases with the development of each L2 network.

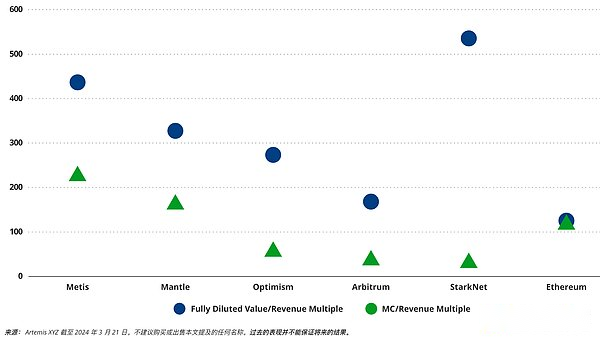

Complete dilution value (FDV)/income and market value (MC)/income

>

By measuring the multiple of the past 12 months (TTM) revenue and a full diluted valuation (FDV), the multiple of each L2 far exceeds Ethereum.However, if we change the multiples to the value of floating token supply rather than completely diluted, this dynamic will change.This is a strange disconnection, which is related to the issue timetable of L2 token -most L2 projects only release a small part of its supply.In fact, we see that L2 transactions are more based on guessing accumulated long -term value, not the current income dynamics.We attribute this dynamics to L2’s future income may be much higher than Ethereum.

We expect that L2’s income will exceed Ethereum, because Ethereum cannot match the transaction throughput or user experience of L2.We are increasingly seeing the integration of the universal rolling curtain market by a few major participants.This is due to the combined and shared network effects on the chain application.It is also due to the summary framework such as OP Stack or Arbitrum Orbit, and the OP/ARB tokens accumulate value from other L2 or even Layer-3 (blockchain submitted to L2).It is also obvious that due to the many advantages of the zero -knowledge framework (ZKU), most of the summary will eventually turn to the zero -knowledge framework (ZKU).

In the long run, we still believe that the Ethereum block space will be expensive. As a result, many L2 will be awarded to a unified proof layer, which will be a certificate of “recursively” combination of its components.This is especially true of applications and specific departments.An example of concept is polygonal aggregation.In conceptual point of view, things like the “aggregation layer” can also greatly improve the user experience, because they often publish proofs and status roots to allow them to cross L2 and Ethereum Bridge in the Ethereum Bridge within a few hours.

Therefore, we see cruel competition between L2, of which the network effect is the only moat.Therefore, we generally look at the long -term value prospects of most L2 token.The first 7 tokes of L2 already have a total of $ 40B of FDV, and there are many powerful projects intending to launch in the middle.This means that in the next 12-18 months, FDVs in L2 token may increase $ 100B.For the cryptocurrency market, it seems that it is too far away to absorb even a limited supply without a large discount.In addition, although there are reason to believe that some L2 tokens will become valuable, it is more difficult to predict more valuable ways than other cryptocurrencies.In particular, this is the case, because L2 token is not even the basic currency in its own ecosystem.

In addition to the leading position of a small summary in the general L2, we predict that there will be thousands of summary in the future.These L2 will be subdivided by department, application or function.Enterprises may clearly build a summary as their own income and/or cost center, such as building the second -level chain of asset management.Other types of chains may be specifically targeted at the entire department, such as the summary of the social media network, and applications that want to build products and services for the social media network.

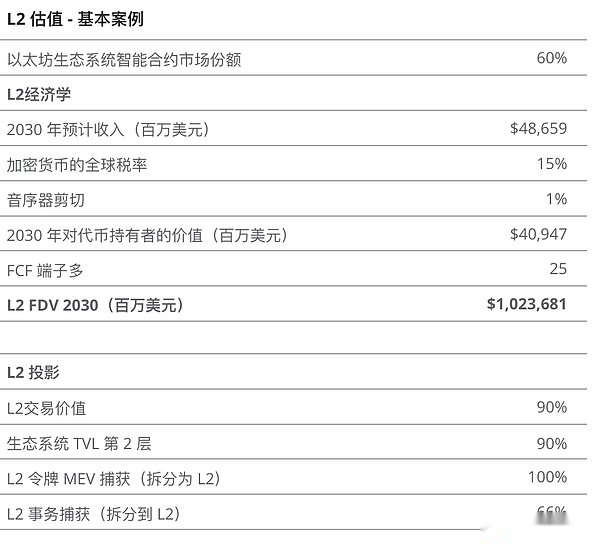

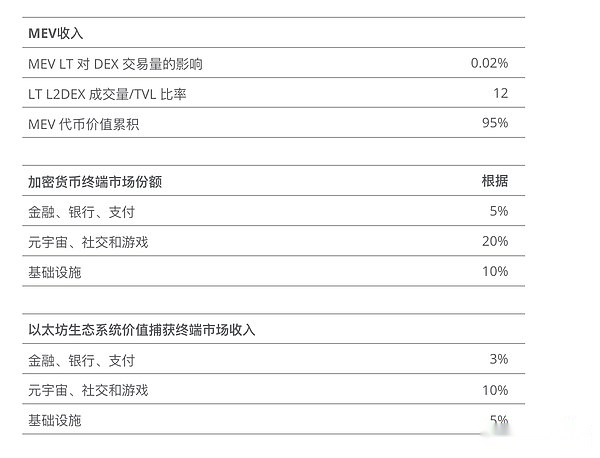

2030 Ethereum Layer-2 valuation forecast

By applying the FCF terminal multiple to our expectations for future cash flow, we found the 2030 valuation of L2 space.We estimate the income of these cash flow through the following ways:

>

>

Source: Vaneck Research as of March 21, 2024.Past performance does not guarantee future results.The information, valuation scenarios and price targets in this report have no intention of calling, purchasing or selling suggestions for financial proposals or any actions, or as a prediction of the future performance of Layer-2.Layer-2’s actual future performance is unknown, and it may be very different from the assumptions described here.There may be unexplained risks or other factors in the scene, which may hinder performance.These are only based on the simulation results of our research, for explanation.Please conduct your own research and come to your own conclusions.