Author: Atis E, Independent Researcher Source: Medium Translation: Shan Ouba, Bitchain Vision

In the next few months, Uniswap Dao seems to be readySupplement the agreement to the UNI pledkerVoting.This article shares the perception and speculation of individuals’ future impact on this vote.

Uni pledge proposal abstract

The UNISWAP Governance Forum is currently discussing a proposal to transform UNI into a fee shared tokens.The main idea is:

Upgrade the UNISWAP protocol governance to achieve the cost of the agreement that does not require licenses and proceduralization

In proportion to the UNI token holder who has been pledged and entrusted to allocate any agreement costs

Allow governance to continue to control core parameters: which mining pools are charged and the size of the cost

This initial proposal is the basis of another future proposal. The proposal will actually introduce the agreement fee on some Uniswap V3 pools:

Assuming the voting on the chain is successful, the community will choose to charge fees.

As a representative of Uniswap, I generally agree with the proposal to assign costs from the UNISWAP V3 pool to the UNI pledgers.I think this will be an interesting experiment.The full preparation behind the proposal clearly shows the ability and ability of the foundation.

There are still uncertainty, such as specific pools of implementation costs and exact agreement tax rates.The cost switch must be customized for each pool, which means that the cost of activation costs for the selected Uniswap V3 pool group.Economically, it is meaningless to charge for mining pools with small capacity or short life, especially when considering the DAO governance work required for each cost conversion decision.The selected mining pool is likely to be consistent with the mining pool with 0.15% of the front -end cost of Uniswap Labs.According to the previous voting, the agreement rate is expected to be set between 10% to 20% of the total exchange fee.

At present, there is no public plan to implement charges on V2, V4 or Uniswapx.These versions can be solved in future discussions, and the V3 cost conversion experiment will be used as an important reference point.

The future of V3

UNISWAP V3 is currently the most dominant iteration of the platform. From some point of view, it is also the largest DEX.However, I think Uniswap V3 is already declining, the reason is as follows.This means that trying cost switching on V3 is a relatively low -risk behavior.

V4 is coming and will greatly replace V3 to a large extent

Uniswap’s development strategy has some similarities with Intel’s previous Tick-Tock model, that is, architecture progress (“TOCKS”) is optimized (“Ticks”).In this case, the UNISWAP V1 and V2 represent a tick cycle, and V3 and the upcoming V4 form another cycle.

Uniswap V1 was a major progress compared to the technical level of the time.V2 is similar to the architecture, but has new functions such as ERC20/ERC20 swap and price prophecy machine, and has made other enhancement of the overall design.Despite the competition of V3, V2 is still strong, highlighting its lasting attraction.

V3 introduced another architecture leap, and liquidity concentrated.However, it does have some major shortcomings, which not only uses more complicated, increases the market risk of limited partners, and is more likely to be affected by the leakage of the arbitrage MEV, especially in the lower cost level pool of volatility assets.

I predict that the design of Uniswap V3 will not continue from the long run, and the V2 model that has been tested for a long time may last longer than it.Once launched, V4 is expected to surpass V3 soon, which is due to the following improvements:

-

GAS optimization: V4 introduces various optimizations, including a single -case design that reduces the cost of ERC20 transmission and significantly reduces the transient storage mechanism of GAS costs.

-

It is conducive to the innovation of limited partners: It aims to re -regain the function of losing the value of arbitrage (LVR) by auction and dynamic costs to provide a more favorable environment for limited partners.

-

Support V2 function: V4 will re -integrate a full range of liquidity positions, accommodate the transfer fee tokens, and allow LP donations in the liquidity pool, and other enhanced functions.

In essence, V4 aims to solve the shortcomings of V3 and at the same time integrate the advantages of its predecessor.

DEX pattern competition intensifies

1. AMM competitors continue to rise

The UNISWAP V3 initially used its innovative centralized liquidity model and restriction permit to dominate the industry.However, these special advantages no longer exist.The core code of V3 has been in GPL for nearly a year.High -quality competitive AMMs are constantly emerging.Uniswap V3 does still have the most Lindidi, the most tested and the most solid code library, and some competitors have fallen into a hacking attack.However, these benefits will inevitably weaken over time.

2. Continuous development transaction mechanism

The chain transaction is moving towards a systematic development.Therefore, we expect the transaction ratio through AMM will decline.Although it is now announced that the AMM model is still too early, the rise of platforms such as Uniswapx and COWSWAP may continue and increase its market share.

3. Emerging chain and ROLLUPS centered on DEX

Regarding the dedicated UNISWAP application chain or Rollup is a convincing argument for both sides of DEX.

-

Case: As Dan Elitzer emphasized, in the current model, the exchangers paid Ethereum network costs higher than the exchange fees paid by their limited partners they have to UNISWAP.This is shocking inefficient.In addition, the loss of traders caused by the incomplete execution caused by the slide point is greater than the falling fee -at least 2021/2022 is the case.The DEX trading user experience is significantly improved every year, but if the focus of Ethereum is still the settlement layer, these problems are unlikely to be completely resolved in the future.People can continuously optimize the design of DEX and complicate it, but it is impossible to completely copy the CEX transaction experience on the chain with 12 seconds of outlets -at least without sacrificing decentralization or review resistance, it isImpossible.

-

Reasons for opposition: No one is willing to connect their assets cross -chain to improve their trading experience slightly.In addition, we do not need further liquidity fragmentation.

However, the potential of Ethereum shared sorting online may change the rules of the game.This innovation will achieve sync between Rollup, allowing the dex contract to seamlessly access all the liquidity involved in Rollup on the DEX contract on the Uniswap Rollup.Such development will eliminate most of concerns about decentralized liquidity and inconvenience of users.

All in all, these factors make Uniswap V3 continue to occupy the dominant position of the main network.Trying the cost conversion will not cause much loss.

Question of limited partners: taxpayers without representatives?

Risk of expense conversion

If the charging conversion causes many liquidity providers (LP) to exit Uniswap, it may be counterproductive.Losing a limited partner will mean a reduction in the liquidity of the capital pool, thereby reducing the attractiveness of the capital pool to traders.The reduction of exchange activities will reduce the income of the remaining limited partners, resulting in more limited partners to leave.This may trigger a chain response, the liquidity continues to decline, leading to the worst situation -death spiral.

Fortunately, so far, Defi traders seem to be not too sensitive to price changes.Even though some limited partners decided to leave after the charges, the overall transaction volume may not decrease significantly.This means that the remaining partners who stay will eventually obtain a higher annual interest rate (before considering the cost of the agreement).To some extent, these higher transaction income will offset the cost of the agreement cost, thereby achieving a stable balance.

What supports this view is that Gauntlet’s research (currently being updated) shows that as long as the cost is not too high, the death spiral is unlikely to happen.Their data -driven method is reassuring. If they are cautiously charged, they will not cause limited partners to flow out of large scale.

The fair value of the agreement tax rate

The tax rate of 10%to 20%is not uncommon in the real economy.However, this cannot be directly transformed into Uniswap. The reason is as follows:

-

Generally, the goal of taxation is profit, not total income.For the limited partners on Uniswap, the exchange cost represents their total income, not net income.The conclusion of using the impermanent loss model or loss and re -balance (LVR) model (suitable for non -protected and hedge LP) to measure LP income is that the net profit margin of Uniswap V3 LP is almost zero.Therefore, in this case, the tax system aiming to accurately collect income will generate the minimum income, which highlights the incompatibility between traditional tax logic and limited partners’ income dynamics.

-

Taxation is used to fund public services in the traditional economy, such as infrastructure and medical care.Re -assigning tax revenue to the UNI tokend holders cannot essentially ensure the interests of contributors (that is, limited partners) in a way that meet the expectations of typical taxpayers.

Despite these challenges, there are still convincing reasons to consider the cost of the agreement:

-

The agreement fee is more like VAT (VAT), not income tax or capital gains tax.One of the main features of VAT is that it is paid by customers, not paid by the provider.Limited partners can force exchanges to pay more to some extent and offset the cost of the agreement by migrating their assets into a pool with a higher cost level.However, if there is no coordinated action, this change is unlikely to occur widespread, which will cause LP liquidity in the Uniswap V3 to continue to underestimate.

-

The cost distribution model is to encourage UNI token holders to actively participate in governance by requiring tokens to share income sharing.Studies have shown that positive authorization can increase the degree of decentralization of DAO.This is also a major progress that enables the Uniswap ecosystem (especially foundation and DAO) to achieve sustainable self -development rather than relying on the Ministry of Finance.

LP and DAO

Combined with the above situation, it is obvious that the purpose of cost conversion is:

-

Part of the cost income of the exchange of uniswap LP

-

Enhance the function of the Uniswap ecosystem.

However, it was not a limited partner who was required to perform this transaction -or at least not the main partner.The current situation is a kindNo tax levy.At least, there is not enough representativeness.It is clear that there are only millions of UNI votes that give priority to supporting LP.

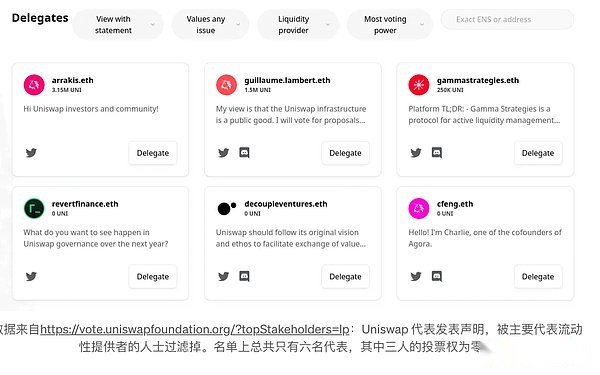

>

In addition, there are some famous trading companies between large DAO representatives.There are obvious potential interest conflicts between them and Uniswap LP (especially retail LP).

My position is that limited partners are the lifeblood of any decentralized exchange, and their voting rights should reflect this.It is hoped that the upcoming UNI pledge and re -authorization will provide UNISWAP LP with more opportunities to get more votes.

A technical step that increases LP voting right is to allow the UNI tokens to authorize in its liquidity position.This requires some technical changes, but it is definitely feasible.

Compensation LP?

There are currently some ideas about how to associate the support of limited partners with the cost conversion plan, such as:

-

Liquidity mining plan

-

For “loyalty” LP airdrop

-

Natural gas rebate

Even if the limited partner has enough voting rights to pass these ideas (this is uncertain), I find that none of these ideas are completely convincing:

-

Targeted liquidity incentives can be effective as a means of tax reinstation.However, they may disturb the free market and damage UNISWAP as the reputation of neutral platforms.The accurate target positioning is challenging and requires a lot of monitoring, research and management costs. Increased incentive measures with unclear goals will mainly attract the limited partners of the map, which may damage the ecosystem.

-

If the public DAO voting is involved, the standard for airdrops is easily manipulated by large token holders.Future airdrops are more likely to lead to governance crisis, destroy the neutrality of UNISWAP, and encourage airdrop mining as an LP speculative strategy.In addition, the airdrops without KYC will bring inadequate benefits to the big holder or Sybils, and requiring KYC will be a worse choice, which contradicts the spirit of uniSWAP that does not need to be licensed.

-

Natural gas rebates will be unfair to active limited partners, rather than those limited partners or retail limited partners who bear lower risks.Their long -term impact will be a strategy that prompts limited partners to adopt worse.

The strategy of the UNISWAP Foundation focuses on the development of an ecosystem is more feasible than any of these options (except for targeted liquidity mining).The ideal situation is that the share of limited partners is relatively small, but the cake is much larger.

in conclusion

-

Encourage UNI token holders to entrust their tokens to improve the decentralization of DAO and the sustainability of the ecosystem.

-

At present, the implementation fee conversion on V3 will provide key data, providing information for future decisions of the future version of Uniswap and other protocols in the ecosystem.

-

Limited partners are those who have obvious short -term losses in the expected cost conversion, and are not sure whether the long -term expected income of the ecosystem is sufficient to make up for their losses.

-

LP should work hard to achieve better coordination and stronger speech in DAO decision.This includes support for more conservative cost conversion methods: for example, only a small number of mining pools are collected not more than 10%.