Author: DFG Office Source: Medium Translation: Good Ouba, Bit Chain Vision

introduce

Re -pledged and liquidity pledged on those users who hope to add ETH returns to users who want to bring ETH returns on the basis of good news brought by ETH ETF.According to DEFI LLAMA data, these two categories of TVL have amazing growth, ranking fifth and sixth among all categories.The re -pledge ecosystem has recently developed rapidly, but before understanding the additional benefits brought by re -pledge and liquidity, let us first solve the basic principles of pledge and liquidity pledge.

The background of the background of Staking and liquid Staking

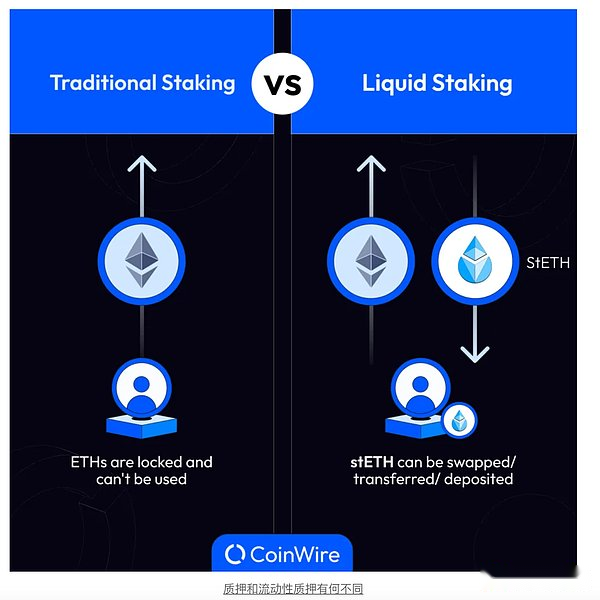

Ethereum pledges involved ETH to protect the network and get additional ETH rewards.Although the pledge ETH will generate a return, it involves the risk of being cut off and the risk of insufficient liquidity caused by the unable to sell ETH due to the lifting period.

To become an authenticator, individual pledges need a lot of early funds, that is, 32 ETH, which is an unbearable threshold for many people.Therefore, verificationrs such as Consensys and LEDGER, that is, the service platform provides a collection pledge service, allowing multiple users to merge their ETH holdings to meet the minimum pledge requirements.

Although these services allow the number of pledges to be appointed in ETH, the ETH of the pledged ETH is still in a “lock” state and cannot be accessed until the pledge is lifted (it takes a few days).Liquidity is born as an innovative alternative, and it casts a liquidity tokens in exchange for user ETH deposits.Liquid tokens represent ETH pledged. These ETH will accumulate rewards and can be used to participate in DEFI activities to increase returns.Lido is the pioneer of liquidity pledge, and then companies such as Rocket and Stader followed closely.These solutions not only make pledge easier to obtain, but also improves the flexibility and potential returns of investors.

The rise of pledge

This is a concept proposed by Eigenlayer for the first time. It involves the use of pledged ETH to protect modules that cannot be deployed or verified on EVM, such as side chains, prophecy machine networks, and data availability layers.These modules usually need to actively verify services (AVS), which are protected by their own tokens and will encounter problems such as guiding their security networks and low trust models.The pledge solved this problem, because security can be guided from the large -scale verification device of Ethereum, and attacking its pool pledge requires a greater cost.

Although Eigenlayer is the first re -pledge agreement, some other agreements have also become competitors.Although they are designed to provide security with re -pledged assets, there are subtle differences between them, and we will discuss these differences in the next section.

Overprinting agreement

Currently supporting deposit assets

The types of deposits supported by each agreement are important because it determines their ability to accommodate the deposit flow.Over time, agreements with wider asset support are more likely to attract greater traffic.At present, EIGENLAYER only supports ETH and ETH mobile pledges (LST), while Karak and Symbiotic support a wider range of asset scope.This diversity is the main factors of these three re -pledge agreements.

Karak accepts various assets, including LST, mobile re -pledged token (LRT), Pendle LP tokens and stablecoins.At the same time, Symbiotic supports LSTA, Ethena’s ENA and Susde.Although they currently accept different types of assets, both plans to expand their products.Karak can accept any assets for re-pledge, while Symbiotic allows any ERC-20s to be used as a pledged collateral.EIGENLAYER’s current scope of assets is relatively limited, but the future plans include dual pledge and LP re -pledge options.

Security model

At present, EIGENLAYER only accepts ETH and its variants. Compared with other small market value tokens, these tokens are less volatile.This is very important because it can reduce the risk of large fluctuations, and this fluctuation may endanger the network security based on active verification services (AVS) based on Eigenlayer.In contrast, agreements such as Karak and Symbiotic provide a wider range of assets for re -pledges, providing more flexible distributed security services (DSS) and networks (on Karak) and networks on their platforms (on Karak) and networks (on Symbiotic)Safety options.

Provide multiple assets for re -pledges to achieve customized security, enabling services to determine the level of economic security they need.By receiving tokens that generate income, services based on the rebuilding agreement can reduce the additional benefits required by attracting verifications, thereby making the service more cost -effective.This customized method allows the service to determine the types and levels of its required safety.

In terms of design, both Eigenlayer and Karak have upgraded core smart contracts, which are managed by multiple signatures.They have three and 2 different multiple signatures, controlling different parts of the infrastructure, and scattered control to different users.On the other hand, Symbiotic has an unsatisfactory core contract that can eliminate governance risks and single -point failures.Although this can eliminate centralized governance problems, if there are any errors or defects in the contract code, re -deployment is needed.

Despite pledge support to support pool security, there is a risk of collusion between operators.For example, if a network worth $ 2 million is protected by a $ 10 million reinforcement ETH, then attacking the network is economical, because the attack cost (5 million US dollars) is higher than the return ($ 2 million).However, if the same $ 10 million and then pledged ETH to protect another 10 million US dollars worth of $ 2 million, then attacking is economical.In order to alleviate this situation, restrictions on the re -pledged assets of the authentication dedicated to other services can be used to prevent re -pledge ETH concentration.

Supporting chain stores and partners

Eigenlayer and Symbiotic mainly accept only assets stored on Ethereum, but Karak has now supported deposits from 5 chains.Integrating more chains for receiving re -pledge assets, reducing the demand for re -pledge infrastructure other than the news bridge access to Ethereum.However, most TVLs are still held in Ethereum, and the use of re -pledged assets on Ethereum can provide the highest security.

Karak also launched the second layer of network K2, which acts as a sandbox environment that DSS is tested before upgrading on Ethereum.Compared with Eigenlayer or Symbiotic, neither of these two networks provides a similar test environment like Karak, but the protocol can also use different chains to test.

Although there are differences in the above -mentioned re -pledge agreement, they seem to eventually integrate together to provide similar services with each other, covering different recreational assets.Therefore, the success of each agreement depends on the partnerships they can establish so that they can build services on their infrastructure.

Since Eigenlayer is a pioneer in the field of repayment, the number of AVS built on its infrastructure is also the largest.The more famous AVS on Eigenlayer includes EIGENDA, Altlayer and Hyperlane.Although Karak only announced one DSS, they have successfully integrated Wormhole to develop decentralized verification device networks and decentralized relay networks used for their native token transmission (NTT).Although Symbiotic is the latest, Ethena recently announced that Ethena will use its re -pledge framework and Layerzero’s decentralized verification device network (DVN) to ensure the cross -chain transmission of USDE and SUSDE assets.

Over time, more services may use such re -pledge infrastructure to ensure safety.A platform that can always establish a partnership with large participants is likely to win over other platforms in the long run.After exploring the prospects of re -pledge, it is important to study the next layer of flow and re -pledge agreement, in order to understand the subtle differences and how they add value to the entire ecosystem.

Liquid again pledged overview

LRT type

When you deposit with the agreement, the LIquid Re -Pairing Association Council provides you with its liquid packaging tokens.According to the agreement you choose, you can choose several asset deposit options.

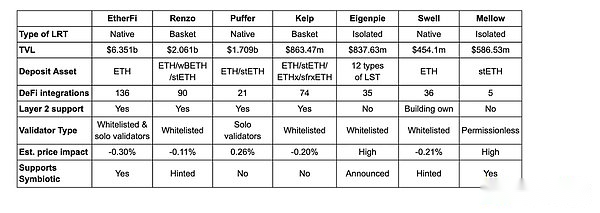

For example, in addition to native ETH and STETH, Renzo also allows WBETH deposits, while Kelp allow ETHX and SFRXETH deposits.No matter which token you deposit into these agreements, you will receive their LRT, EZETH and RSETH.These two LRTs are regarded as a basket -based LRT because the LRT tokens are represented by the combination of basic assets.Gathering multiple LST to the same LRT may bring complex management challenges and additional risk of transaction.

Other mobile re -pledge agreements provide native LRT, and users can only store native ETH.For Puffer, although it currently accepts STETH, it will eventually convert STETH into native ETH for native pledge.In the past, this was an advantage, because Eigenlayer had the upper limit of deposit on LST, and there was no native ETH.However, they later canceled the upper limit of the deposit of all types of assets. Native LRT eliminated the risk of the LRT token and the underlying LST assets and their opening of the risk of other LST protocols.

Both Eigenpie and Mellow currently have independent LRT, which distribute specific LRT tokens in exchange for specific deposits and insurance libraries.Although this isolates the risk of LRT token to its respective LST/insurance libraries, it also causes further dispersing liquidity, because there is almost no or without the DEX pool flow.assets.

DEFI and Layer 2 support

The value proposition of the liquid re -pledge agreement is that you can unlock capital efficiency and use the assets you deposited to get cumulative benefits from re -pledge and DEFI.PENDLE is the most widely used platform for these protocols, because its income transaction mechanism allows users to use leverage to cultivate points on the liquid and pledge protocol.Many deposits also provide liquidity on Pendle, because if they hold positions to expire, they can provide liquidity without impermanence.

Many DEFI integration has expanded to other fields and protocols.These LRTs are also used as the liquidity of DEX exchange on platforms such as CURVE and Uniswap, for users who want to withdraw in advance without waiting for the withdrawal of the pledge period.Insurance libraries have also emerged, and they provide different revenue strategies for these LRT through circulation and options.Now, some lending platforms (such as JUICE and Radiant) also provide LRT as a borrowing service for mortgages.

In order to cope with lower GAS fees, these LRTs also support various layers 2.Users can choose to pledge assets directly on L2, or they can transfer the re -pledged assets from Ethereum to L2 to reduce DEFI’s GAS fees.Although most TVL and transaction volume are still on Ethereum, extending these LRT to L2 can also expand their market share, because smaller participants are hindered by high Ethereum GAS expenses.

Support the re -pledge protocol

The liquidity re -pledge protocol was originally built on Eigenlayer because it was the first agreement to provide re -pledge.Subsequently, Karak went online, but did not require these liquidity re -pledge protocols to integrate alone with them, because users can deposit their LRT directly into Karak after pledged the liquidity re -pledge protocol operator on the Eigenlayer.Therefore, most liquidity re -pledge agreements have been integrated with Eigenlayer and Karak.

On the other hand, Symbiotic was launched at the end of June. Unlike Karak, it does not allow LRT to deposit LRT into its platform.This allows only LST to store Symbiotic for re -pledge.If the flow -re -pledge agreement wants to provide LRT for Symbiotic, they must set up a insurance library or operator to allow the user’s deposit to be entrusted to them so that they can be pledged on Symbiotic.

In view of the recent disputes over the Eigenlayer airdrop, many users are not satisfied with the airdrop terms, and some users have begun to issue withdrawal requests on the platform.As users and farmers look for the next agreement to earn income and farm airdrops, Symbiotic seems to be the next logical choice.Although Symbiotic has set its deposit limit to about 200 million US dollars, it has been working with many other agreements.Mellow is the first liquidity re -pledge agreement based on Symbiotic, but many of the previous agreements on Eigenlayer are now cooperating with Symbiotic to maintain market share.

Re -mortgage increase

Since the end of 2023, the deposit has increased.The liquidity re-pledge ratio (tvl/tvl in tvl/pledge of liquidity reinsurance) has reached more than 70%, and it has continued to increase by about 5-10% in recent months, which indicates that most of the liquidity of the re-pledge is the liquidity of the re-pledged pledge is the liquidity of the re-pledged pledge isCoupled with liquidity re -pledge protocols.With the expansion of the re -pledge class, the liquidity re -pledge agreement is expected to expand.

However, there are obvious signs that the withdrawal of the withdrawal of the withdrawal of Eigenlayer and Pendle deposits has decreased by more than 40% after the expiration of June 27.Although the deposit expired in PENDLE can be extended, the outflow of funds may be caused by the tokens of the TEGE and most of the major liquidity re -mortgage protocols in 2024.

Farmers will continue to be farmers.Although Eigenlayer’s airdrop EIGEN has been launched, it is still unable to trade until the end of September 2024.Therefore, farmers may take out their deposits and look for other airdrops to cultivate.Over time, some of the liquidity may flow to other protocols, namely Karak and Symbiotic.

Even for the liquidity re -pledge protocols that have been launched, they also have subsequent airdrop seasons, and its LRT can still be used in Karak, while working hard to integrate with Symbiotic.As Symbiotic and Karak’s future TGE and their deposit limit increase, users are likely to continue to cultivate on these agreements.

in conclusion

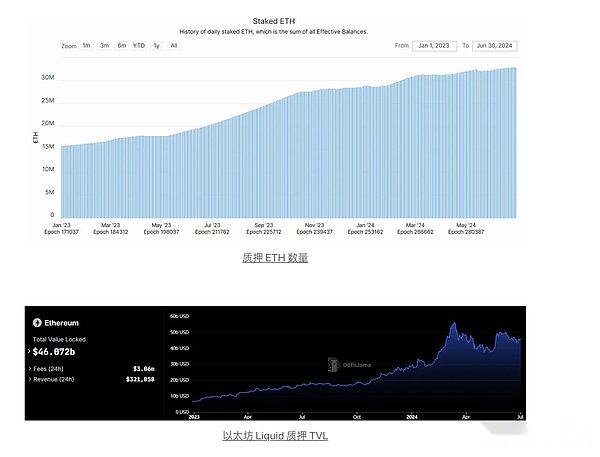

As of July 1, 2024, nearly 33 million ETH pledged in the balance, of which about 13.4 million ETH (US $ 46 billion) pledged through the mobile pledge platform, accounting for 40.5%of all pledged ETH.Due to the increase in native ETH deposits on Eigenlayer, and LST deposit limit is limited, this proportion has recently declined.

With the AVS reward and reduction of the activation, the new services on the pledge agreement can be rewarded through the New Type allocation, similar to pledge returns on LIDO.Although the airdrop farmers may eliminate liquidity from the distributed airdrop rewards, the benefit seeker may be attracted over time.

At present, the proportion of re -pledge and mobile pledge is about 35.6%, close to the proportion of mobile pledge ETH to total pledge ETH.As the re -pledge platform finally cancels the upper limit of deposits and expands to other assets (including trying to pledge Milady), it may attract more capital inflows in the future.