Author: Donovan Choy and Thor, Onchain Times; Compilation: 0xjs@作 作 作 作 作

introduction

In the rapidly changing encryption industry, thousands of projects come and go.

The time to withstand the time of residence is a few enviable projects, and they have found some form of product market fit.

What agreements do users actually pay for?This article will analyze the most profitable business model of the crypto industry since 2024.

Eighth place: Base

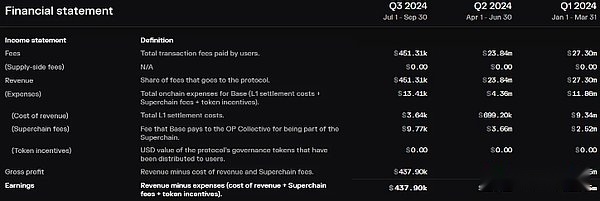

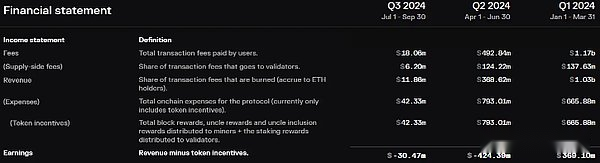

Base was launched by Coinbase in the third quarter of 2023. It is an Ethereum L2 chain based on Optimism Stack.Less than a year after the launch, Base has created an impressive $ 52 million income since the beginning of the year, becoming the eighth agreement for income.The income comes from the user payment fee on Rollup.

Source: Token Terminal

In terms of income, Base’s profits are quite considerable, and the profit at the beginning of the day to the present is about $ 35 million.There are two key factors here.First of all, because the BLOB fee was introduced in the EIP-4844 implemented on March 13, Base greatly reduced data availability costs.Base immediately took advantage of the BLOB cost. The cost of data availability fell from US $ 9.34 million in the first quarter of 2024 to US $ 699,000 in the second quarter of 2024, a significant decrease of about 13 times.Secondly, the high yield of Base compared to its L2 competitors is also due to the cost of incentives for tokens paid, because it does not have its own native currency.

Seventh place: lido

Lido’s business model has a fundamental connection with Ethereum.Historically, Lido’s responsibility is to lock the pledge ETH on the benchmark chain.With its STETH derivatives, Lido allows ETH pledges to obtain online rewards (ie ETH issuance, priority fees and MEV rewards) by pledged ETH and unlock their pledged capital.Until April 2023, the Shapella hard fork upgrade allowed the credit chain to withdraw, all of which changed.

Lido’s business model has a fundamental connection with Ethereum.Historically, Lido’s responsibility is to lock the pledge ETH on the benchmark chain.With its STETH derivatives, Lido allows ETH pledges to obtain online rewards (ie ETH issuance, priority fees and MEV rewards) by pledged ETH and unlock their pledged capital.Until April 2023, the Shapella hard fork upgrade allowed the credit chain to withdraw, all of which changed.

Today, Lido is still very popular because it allows ETH holders to participate in network verification and get a certain percentage of network rewards.Another advantage enjoyed by Lido pledges is the efficiency of automatic compound interest, while single pledges are limited by 32 ETH pledge.

Lido actually acts as a bilateral market connecting ordinary ETH holders and professional node operators.ETH pledged ETH is guided by the diverse node operator group approved by Lido DAO.As of today, a total of 109 node operators, most of which were added when they implemented simple DVT (distributed verification technology technology) modules in April.

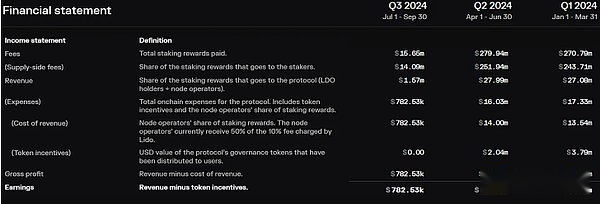

The liquid pledge giant ranks seventh in revenue.So far this year, Lido has created a $ 59 million income on its two chains: Ethereum L1 and Polygon Pos.Lido’s income comes from 10% of the user pledge reward, and then distributed to node operators and Lido DAO vault at a ratio of 50:50.

After minusing 5% pledge rewards and LDO rewards paid to the CEX/DEX liquidity pool paying to node operators, the total profit of Lido DAO has reached $ 22.5 million to the present to the present.

Source: Token Terminal

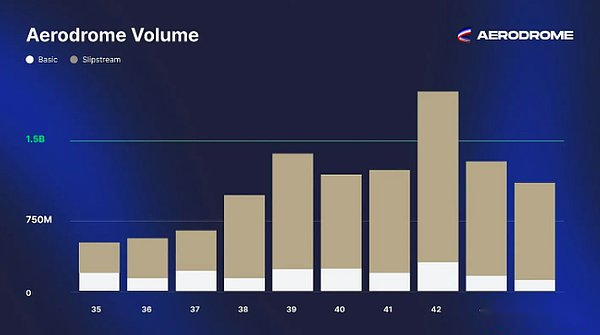

Sixth place: Aerodrome

AERODROME is the AMM Dex on Base L2, founded by the founder of Velodrome Dex on Optimism.Aerodrome was launched in August 2023 and quickly became the largest DEX on Base, with a total lock value of $ 470 million.According to the data of tokenterminal, Aerodrome has created $ 85 million in revenue so far this year, and has paid $ 29.7 million to tokens in the past 30 days.

What is the secret of Aerodrome’s success?It copys crazy and combines many successful mechanisms in the field of Dex.

In order to attract deep liquidity, Aerodrome relies on its Aero token VECRV (voting custody CRV) to bribe tokens.Aero token holders can lock Aero for four years and get the right to vote. Based on the number of Veaero votes received every week, how many tokens will be launched in the future.On Aerodrome, the 100% pool transaction fee is obtained by Aero lockers, and the proportion of LP and CRV locks on CURVE is 50:50.Another interesting change is that unlike Curve, rewards are directly proportional to the transaction volume of the pool, thereby encouraging Veaero voters to launch the most productive trading pool.These two core protocol design mechanisms are key incentives behind the Aerodrome deep liquidity pool.

In order to simplify its voting custody system, Aerodrome borrowed from CURVE’s approach and implemented its own “VOTIUM” version, called “Relay”. In this system, the locked Aero token will automatically vote pools, and compound profit income can be exchanged for exchangesBack to Velo.

Another factor of Aerodrome’s success is “SlipStream”, which is the fork of the UNISWAP V3 episodes of liquidity contracts.This undoubtedly helps Aerodrome compete with UNISWAP on a particularly large transaction volume such as WETH/USDC.

Source: Twitter

Fifth place: Ethena

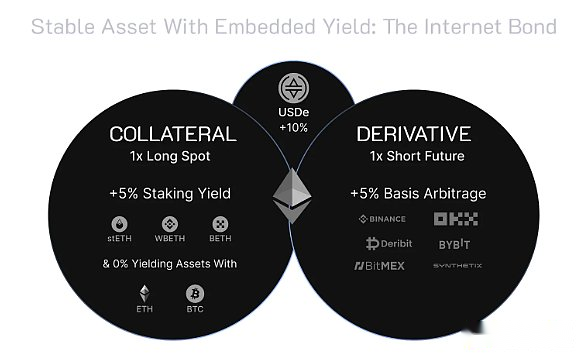

The most successful agreement in 2024 is undoubtedly Ethena.With the support of major investors Dragonfly and Arthur Hayes, Ethena has jumped as a new entry of the stabilized currency market.Since its launch in January 2024, the growth of USDE has reached its impressive $ 3.6 billion market value, becoming the fourth largest stable currency asset today.However, its USDE tokens are not technically a stable currency linked to the US dollar, and more accurately, it is a synthetic US dollar.

How does Ethena operate?Like Maker’s DAI, Ethena’s USDE is a stable asset linked to the US dollar, mainly supported by ETH and STETH deposits.However, the difference is the way of USDE income.The USDE income comes from Delta hedging strategy, which uses the financing interest rate difference between CEX and DEX perpetual futures market.When CEX’s financing interest rate is positive, Ethena earns financing fees by the short position of the exchange.At the same time, Ethena’s multi -inch payment financing fee for DEX with a financing interest rate.These positions at the same time make USDE keep it hook, regardless of the direction of ETH’s directional reverse wind.

Ethena does not charge any agreement.At present, its main income comes from ETH deposited by pledged users to earn online distribution and MEV capture.According to the data of Tokenterminal, Ethena is the fifth largest income agreement today with an annual income of $ 93 million.After the cost of paying in the Susde income, Ethena’s income is $ 41 million, making it the most profitable DAPP so far this year.

However, it is worth noting that Ethena’s business aims to stand out in the bull market, and the bull market cannot continue forever.Ethena’s successful points activities are also unsustainable.With each wave of ENA unlocking, people’s interest and confidence in Ethena are constantly weakened.To cope with this situation, Ethena tried to introduce practicality into ENA through two ways: lock ENA in the second quarter to obtain the highest points, and recently used the vault on Symbiotic to obtain reconstruction benefits.

Fourth place: solana

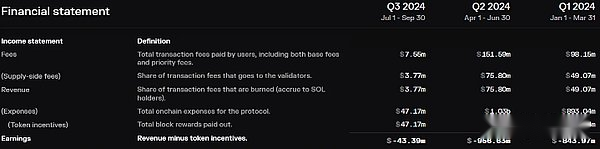

For the blockchain that was almost declared dead less than a year ago, Solana performed quite well.Solana’s recovery is promoted by multiple factors: Memecoin transactions, its “State Compression” update (helping to attract DEPIN) and NFT transactions, and JTO airdrops, which are highly praised in December 2023, triggeredThe huge amount of capital flowed into Solana.

Solana is currently ranked fourth in revenue, with an annual income of US $ 135 million since the beginning of the year.This is a transaction fee paid by users to use the network.However, if we consider the tokens (cost), Solana seems to have no profit, and we have paid $ 311 million to tokens in the past 30 days.

Source: Token Terminal

This leads us to the tricky issue of L1 business valuation.Supporters of Solana may think that evaluating the profitability of L1 blockchain based on the basis of “income -cost = profit” above is unrelated.This criticism believes that network distribution is not a cost, because L1 token holders on the POS chain can access these value streams by pledged on the popular liquid pledged platform, such as JITO or Ethereum on the Solana or Ethereum on the Ethereum.Lido.

Third place: Maker

MAKER was launched at the end of 2019, and its business model is simple and easy -to -understand — the encrypted mortgage that collects interest rates is issued by the agreement to issue DAI stablecoins.However, behind the scenes, Maker’s internal operation is quite complicated.

Since its establishment, Maker has experienced many changes.In order to stimulate the DAI demand, MAKER generated costs through the “DAI savings rate” (DSR), and DSR is the pledge yield of DAI.In order to survive in the bear market, Maker set up a core department to focus on purchasing real -world assets such as US Treasury bonds.In order to expand the scale, Maker has relied on USDC stable currency deposits since 2022, which has sacrificed decentralization.

Today, the total supply of DAI is 5.2 billion, a 55%decrease from the historical highest level of about 10 billion in the bull market in 2021.The agreement has generated $ 176 million in revenue so far this year.According to MakerBurn, the annualized income of the agreement was US $ 289 million.In recent months, a large part of income (14.5%) is attributed to the controversial decision made by DAO in April, that is, the USDE mortgage of Ethena in the MORPHO vault is allowed to issue DAI loans to the collateral.RWA income is also quite considerable, with an annualized income of $ 74 million, accounting for 25.6%of the total revenue.

How much money can Maker make?As mentioned above, one of the methods that MAKER tries to motivate DAI needs is the benefits paid by the user of the pledged DAI through DSR.Not every DAI holder can use DSR, because it is also used in various purposes in DEFI.Assuming that the DSR is 8%and the pledge rate is 40%, the cost of MAKER is about 166 million US dollars.Therefore, after deducting the fixed operating costs of another $ 50 million, MAKER’s annualized income is estimated to be approximately $ 73 million.

Second place: tron

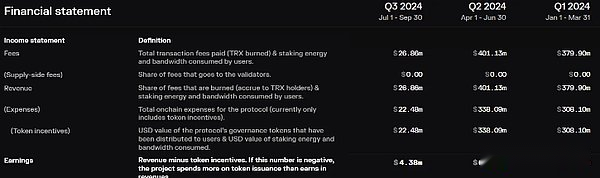

The L1 public chain TRON network created the second largest income in Web3. According to data from Tokenterminal, its revenue so far this year is about $ 852 million.

Source: Token Terminal

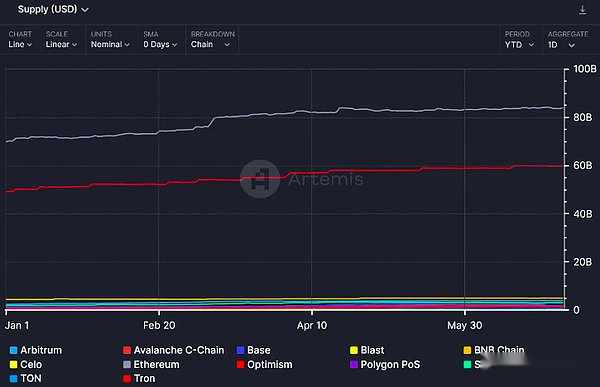

TRON’s success is largely derived from a large number of stable currency activities on its network.In an interview with the ARTEMIS David Uhryniak in the Tron Dao ecosystem development director, most of these stable currency traffic comes from users of developing economies such as Argentina, Turkey and Africa.According to the figure below, we can see that TRON usually tied with Ethereum and Solana to stabilize the highest transfer volume.

The main use case of TRON, as a stable currency network, is also reflected in its stable currency supply of 50-60 billion yuan, second only to Ethereum.

First place: Ethereum

Finally, let’s take a look at the highest income business in Web3 today: Ethereum.Calculated from the beginning of the year to the present, Ethereum’s income is about 1.42 billion US dollars.

So what is the profitability of Ethereum?When we subtract the transaction fee paid by the Ethereum main network to subtract the inflation reward paid to the POS verifications, we can see from the figure below that the network is profitable in the first quarter, but loses in the second quarter.In the second quarter, losses may be due to most transaction activities transferred to Ethereum Rollup to use lower GAS costs.

Source: Token Terminal

However, like other L1, the “income minus profit” framework used to evaluate the profitability of blockchain has confused the real value flow of the ETH pledged.Internet distribution.

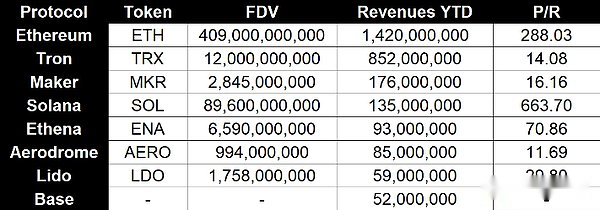

The eight major cash cows so far to date

To sum up all the above content, we get the following table:

Honor Nomination: AAVE

In the field of DEFI lending, AAVE topped the list with a noise of $ 31 million in revenue since the beginning of the year.In the past three years, AAVE has always occupied the leading position in the field of lending. It is currently calculated in active loans, with a market share of 62%.

The last major release of AAVE was V3 in March 2022, introducing functions such as cross -chain exchange and independent lending markets.The agreement was recently announced to be launched in May, which is planned to be released in 2025.The key upgrade of V4 is a unified liquidity layer. It is supported by Chainlink’s CCIP, which can aggregate liquidity between different chains.Other improvements include AAVE special chain, automatic interest rate curve, smart account and updated liquidation engine.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}