Author: Zack Pokorny, Galaxy; Compilation: Tao Zhu, Bitchain Vision

summary

This report is the second part of the three-part series of reports, which deeply explores the risks and returns of pledge, re-pled and liquidity re-pled.The first report provides a comprehensive overview of staking, how staking works on Ethereum, and important considerations for stakeholders when participating in this event.This report outlines the restaking, how pledges work on Ethereum and Cosmos, and the important risks associated with it.

Preface

The industry’s experiments in extending blockchain through modularity have led to the creation of many new protocols and support middleware.However, each of these networks requires the establishment of its own security moat, usually through a variant of Proof of Stake (PoS) consensus, a resource- and time-intensive process that leads to many isolated security pools.

Re-staking is the use of the economic and computing resources of one blockchain to protect multiple blockchains.In the case of PoS blockchain, restaking allows the staking weights and validator sets of one chain to be used on any number of other chains.The result is a more unified and efficient security system that can be shared by multiple blockchain ecosystems.

While it is not always called “re-staking”, the concept has a long history.The Polkadot ecosystem tried this idea back in 2020.Cosmos launched a restaked version called Replication Security in May 2023; in June 2023, Ethereum will be staked through EigenLayer.Most of the value of the restaking agreement comes from staking on Ethereum.Ethereum is the most economically secure PoS blockchain with a total stake of over $100 billion, with more than one million validators pledging ETH (don’t confuse the term “verifier” with verification nodes, because in the Ethereum ecosystem, these two are not the same).”Economically” is expressed in italics to emphasize the difference between the economic security of a chain and its overall ability to be protected from attack or manipulation.The economic security level of a chain does not always indicate the overall security of the chain.

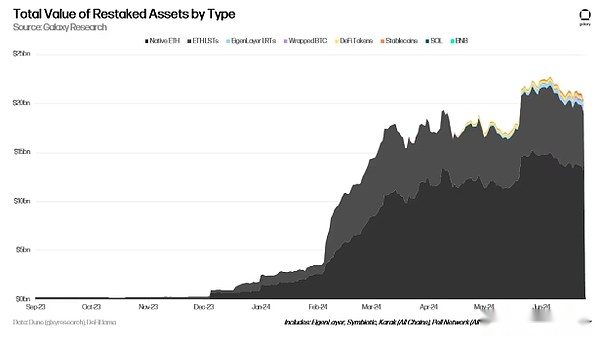

As of June 25, 2024, assets worth $20.14 billion were replenished.Ethereum is the largest agreement to support restaking so far, with ETH and its derivative assets restaking deposits of $19.4 billion, of which $18.3 billion was deposited by users in 2024.It is worth noting that Picasso and Solayer have pledged an additional $58.5 million on Solana, and an additional $223.3 million in BTC on various chains through Pell Network and Karak, including Bitlayer, Merlin, BSC, etc.Below is a chart of the total value of restaking assets by type based on leading restaking solutions (EigenLayer, Karak, Symbiotic, Solayer, Picasso and Pell Network) based on total locked value.

An estimated $1.7 billion is resolidated through the Cosmos Hub Verifier and its resolidated model called replication security.

Although the benefits of re-pled to promote modularization and unified economic security topics are obvious, there are risks that cannot be ignored during the implementation process.This report outlines the major restaking solutions built on top of the Ethereum and Cosmos ecosystems.It will not dive into the risks posed by products built on top of restaking agreements such as mobile restaking.This will be the main focus of the next report in this series.

Important definitions and models

Here is a list of terms and definitions that will be used repeatedly in this report:

-

reduce– Punishment given to validators who fail to complete the work correctly or accurately.In addition to losing a portion of the equity, the validator may be imprisoned (temporarily removed from the active validator set) or removed (permanently removed from the active validator set) as a supplementary non-economic penalties.

-

Cut conditions– The basis for the validator to be punished (cut).This may include double signatures, downtime, or other misconduct specific to a particular network.

-

Liquid staked tokens (LST)– Liquidity of illiquid assets stored on behalf of the chain validator is a substitute for tokens.

-

Liquidity Re-staked Tokens (LRT)– Liquidity alternative to tokens representing illicit ETH, LST and other assets used as re-solidated collateral.

-

Node operator– An entity that runs the node and provides other services to the active verification service.The term covers EigenLayer node operators and Cosmos Hub validators that report replication security.

-

Active Verification Service (AVS)– Any platform that relies on restake resources to ensure security.In this report, the active verification service is abbreviated as AVS.The term covers the EigenLayer AVS and Cosmos consumer chains in the report.

-

Economic security– The dollar-denominated value of assets pledged by the network verifier.

-

Computational security– Verify the hardware and software required for the network.

-

Basic Network– The network of its pledged assets or validator sets are used for economic and computationally protecting AVS, also known as the “base protocol” or “base chain”.This term can be applied to the contexts of Cosmos Hub and Ethereum.

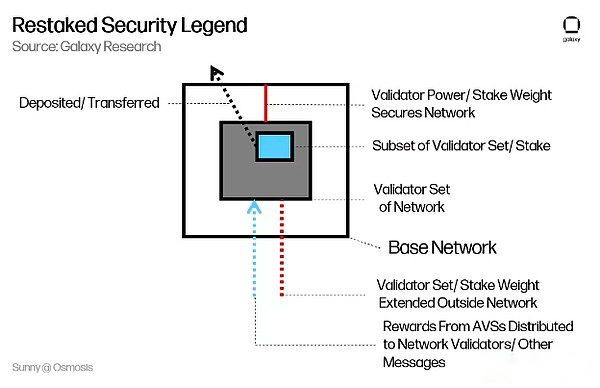

The following legend is the key to understanding some of the restaking models covered in the report.It is based on a keynote address by Sunny Aggarwal at the 2023 Shared Security Summit.

Re-staked on Ethereum

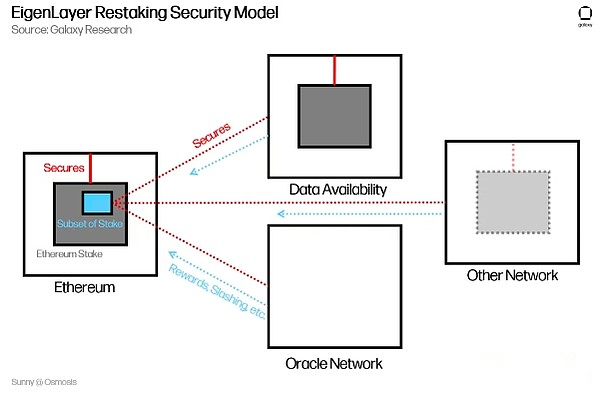

EigenLayer is a set of smart contracts on Ethereum that can be used to restake assets to protect external services called AVS (Active Verification Service).The smart contract specifies the details of the relationship between the node operator and EigenLayer AVS.These details include components such as fine cuts, reward payments, AVS registration and validator exit.AVS does not inherit security from EigenLayer itself.EigenLayer smart contracts act as a middleware technology that connects AVS with Ethereum validators and node operators and their underlying staking assets.

The following figure out how EigenLayer restaking works.Please note that EigenLayer is an optional system.Not all Ethereum validators (also known as Beacon Chain validators) must be EigenLayer node operators and vice versa; Beacon Chain validators who opt to join EigenLayer can point their withdrawal vouchers to EigenLayer, allowing AVS to cut theirShares and pay rewards to them, while also taking responsibility as a Beacon Chain verifier.

EigenLayer allows AVS to lease a subset of Ethereum stakes that can be natively staked in beacon chain validators or LSTs. AVS may or may not have its own set of validators and staked assets.In return, the leased Ethereum equity subset will receive rewards from each AVS for complying with additional cuts.They are complementary to beacon chain rewards obtained directly by beacon chain validators or accumulated through LST.A single ETH or LST unit can be leased by any number of AVS.However, each AVS adds additional cuts to that unit of value.

At the time of writing,EigenLayer is in the early stages of development and does not enforce any cuts or restake rewards.In theory, EigenLayer acts as an open market where AVS can freely purchase economic security from a subset of Ethereum validators, and Ethereum users and node operators can choose the AVS they are willing to protect with staking assets.This is a feature of EigenLayer, and other similar cross-chain staking solutions (i.e. replication security) do not have them.This is a market-driven approach that can find the supply and demand balance of restaking ETH with less friction, although today’s airdrops may affect it.

Re-pled on Cosmos

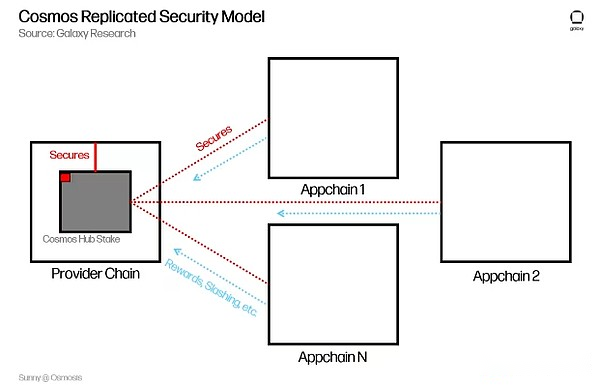

Cosmos’ replication security is implemented by the Cross-chain Verification (CCV) module, which is located at the application layer of the Cosmos protocol stack.Replication security is implemented by the in-protocol infrastructure of Cosmos Hub and the consumer chain, rather than by applications on top of the chain itself.Replication security relies on light clients, a lightweight client software version that can run on resource-constrained devices, for both Cosmos Hub and consumer chains.It also relies on the Inter-Blockchain Communication (IBC) protocol to transmit messages about Cosmos Hub validators, their share, and the rewards they receive from protecting consumer chains.

在复制安全机制下,几乎所有Cosmos Hub 验证者及其质押(投票权排名前95%)都必须确保通过治理的消费者链安全,即使他们不投票支持在此过程中加入消费者链(因此称for “copy security”).The validator set and staking weights of Cosmos Hub are actually copied to all consumer chains.This is different from EigenLayer’s approach, where restakers, node operators, and beacon chain validators voluntarily decide to restake to their AVS of choice.如果 ATOM 质押者不希望他们的资产受到消费者链削减的影响,他们可以将他们的质押重新委托给前 95% 以外的验证者,这些验证者可能无法保护消费者链。However, doing so requires a trade-off that may result in lower ATOM staking rewards for the principal, among other risks.As of June 25, 2024, 113 of the 180 validators in the active set of Cosmos Hub were below the 95% threshold.

下图概述了复制安全性的工作原理;请注意,它看起来与EigenLayer 类似,不同之处在于整个ATOM 质押(减去5% 的红色区块)保护消费者链,并且消费者链在任何情况None of them have their own set of sovereign validators (Cosmos Hub validators replace them).Cosmos Consumer Chain Stride uses “governors”, the verifier who accepts STRD stakes to vote on governance.However, these governors do not build blocks or verify transactions on the network.

It is worth noting that the Cosmos Hub Verifier runs separate software and, in some cases, separate hardware to protect the consumer chain using its ATOM staking.Although almost every Cosmos Hub validator protects every consumer chain, consumer chain transactions will not be executed on the Cosmos Hub and will not occupy the Cosmos Hub block space; the base chain and the blocks of each consumer chainSpaces are mutually exclusive.

Partial set security (more information and proposal voting) was introduced as part of the Gaia upgrade, allowing a subset of ATOM staked to protect consumer chains.Partial set security is more similar to the EigenLayer model, because Hub validators have the option to protect consumer chains; consumer chains can outline the minimum amount of pledge required to protect their chains.Before adding a permissionless consumer chain to start, partial set security will depend on governance in the first iteration.As of June 25, 2024, no Cosmos chain has been launched under partial set security.

Additionally, a proposal was released in early May 2024 to introduce secure aggregation into Hub starting with BTC.If passed, this will allow Hub verifiers to receive BTC delegations through Babylon to protect Hub and its consumer chains and pave the way for any on-chain asset to use as economic security through Hub verifiers.

General re-staking agreement

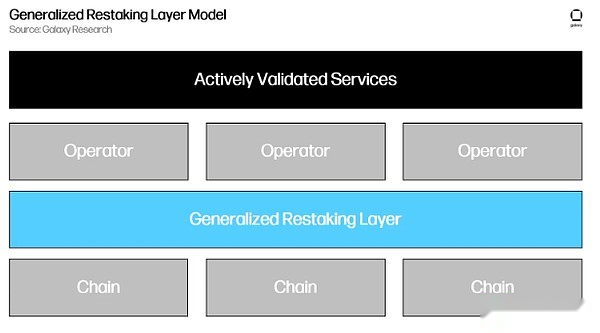

Re-pled in broad sense, also known as general re-pled, is a re-pled system that can concentrate many native assets on the chain during the re-pled process.This approach has nothing to do with assets and the underlying chain, as it allows the concentration of many pledged assets on multiple chains.The model is “broadly speaking” because assets can be brought together from many chains.At a high level, broad restaking depends on an additional layer between the economic security source chain and the AVS or a series of contracts across multiple blockchains.The following is a simplified diagram of the working principle of generalized replenishment.

Picasso and Karak are examples of common or universal restaking platforms.

Picasso

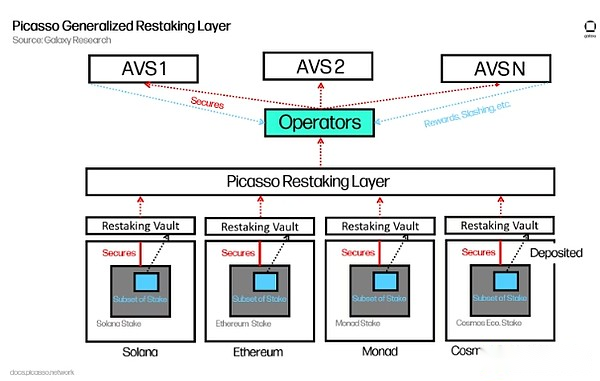

Picasso is a universal restaken blockchain built using the Cosmos SDK.It connects the base chain to Picasso via IBC.The Picasso chain receives detailed information about assets deposited on the base chain through IBC and then allocates user funds to AVS accordingly.The “Orchestrator” smart contract on the Picasso chain is responsible for allocating user funds to Picasso node operators, registering and unregistering AVS, and a number of other responsibilities.At a high level, Picasso’s restaking solution is very similar to EigenLayer’s solution, which allows a subset of network staking weights to opt in to protect AVS.The architecture is copied to multiple base chains and eventually aggregated on Picasso.Node operators under Picasso are selected through governance.At the time of writing, the Replenishment Layer only accepts deposits from Solana and native SOL as replenishment collateral via SOL LST.Picasso’s roadmap includes scaling to Cosmos chains and assets after AVS begins rolling out on Solana.The first AVS was launched in April 2024 and supports IBC connections between Solana and external blockchains.

Karak

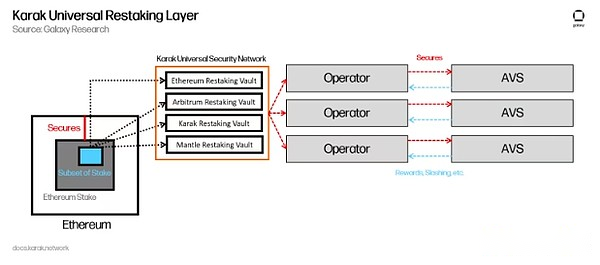

Karak is a universal restaking layer that accepts deposits from Ethereum, Arbitrum, Mantle, BSC and the Karak network, which is built on top of Karak as a universal layer 2 of AVS.It relies on ETH LST as its main staking asset and is supplemented by stablecoins, Pendle tokens, EigenLayer liquid re-staking tokens (LRT), liquid staking BNB and packaging Bitcoin.Accepted LSTs are packaged and bridged from Ethereum, or are native assets of the chains they can store.Its functionality is similar to Picasso in that it allows the consolidation and restaking of multiple assets in multiple networks.Unlike Picasso, which exists as a standalone Tier 1 and spreads assets through IBC, Karak is strictly a collection of smart contracts built across multiple chains, including Ethereum Tier 2.Karak also accepts a wider range of assets than Picasso, such as stablecoins.

Under any restaking solution, the benefits of a unified security model are also accompanied by risks.The risks of the replenishment model can be classified by the three major stakeholders involved in the replenishment supply chain.This includes the base layer network, node operators, and AVS.The next part of this report will dig deeper into the risks these entities assume in the context of EigenLayer and Cosmos restaking.The end user who entrusts assets through the restake solution is downstream of these entities and thus inherits all the disadvantages of risks, with the symptoms detailed below.

Risks facing basic networks

The security of the basic network comes from the original pledged assets in its chain, which are the same as the assets used during re-pled.Therefore, the main risk of re-staking to the basic network lies in the reduction events that affect the security of the basic chain and the centralization of the basic chain staking allocation.

Reduction events that affect the security of the basic chain

在再质押层强制执行的削减条件可能会对基础链及其之上的应用程序的安全性产生负面影响,主要是如果再质押层的质押集中在少数节点运营商手中。This is particularly concerning for EigenLayer and Ethereum, as of June 25, 2024, Ethereum has a diverse suite of applications with a total lock value (TVL) of $41.2 billion (excluding EigenLayer’s TVL,Including it is $59.3 billion).AVS-triggered penalties may significantly reduce the number of pledged assets that can be used to protect the underlying chain, depending on the relative size of the re-pled assets and the pledged assets on the underlying chain.

As of June 25, 2024, only about 17% of the total amount of Ethereum pledged on Beacon chain was resolutely pledged, while 98.26% of all resolute ETH was captured by EigenLayer.Beacon Chain deposits re-pled through EigenLayer account for 11.93%.Cutting down restaking ETH most directly affects the security of the Ethereum protocol, because these deposits represent collateral directly to the Ethereum protocol.This is unlike restaking LSTs, where tokens with the value of the Beacon Chain deposit can be cut before the underlying deposit itself.Therefore, there are potential ways to cut LST without changing the security of the underlying chain.More information about this idea will be presented in a future report focusing on the dynamics of LRT.EigenLayer currently does not enforce any cuts on node operators, so the risk of negatively affecting Ethereum’s security through restaking is minimal.However, this situation changes when the cuts are implemented.Cosmos replication security takes a similar approach when it is first launched to limit cut penalties.The steps EigenLayer takes in this regard are not unique to restaking solutions.

With replication security, 95% of Cosmos Hub stakes are used to protect AVS.Therefore, the impact of the cut penalties executed on the AVS layer on Hub’s economic security is close to 1:1.This idea also applies to centralized forces on Hub staking, which will be studied later.Unlike Ethereum, Cosmos Hub does not support smart contracts or the applications they support.However, economic security still plays an important role in protecting networks.

In addition to the underlying chain security share that faces the risk of reduction through restaking, there is also a need to consider the types of violations that AVS can perform that may lead to reduction.

Intersubjective defects in feature layers

Not all cut violations on AVS can be verified objectively and encryptedly.The Eigen Foundation proposes this idea in a white paper explaining the $EIGEN token.In this paper, the team explained that inter-subjective failures in certain AVSs (such as oracles) (i.e., failures that are not easily verified on the chain) may lead to a split in the underlying chain.Executing on-chain behavior on EigenLayer AVS may require off-chain protocols or social consensus between network observers—a tedious process that can lead to underlying chain segmentation if node operators have broad disagreements about the correct state of AVSfork.

To address the burden on Ethereum consensus due to inter-subjective failures, validators can use EIGEN tokens to perform inter-subjective cuts through token forks instead of base chain forks.This idea was originally proposed by Paul Sztorc in 2014 through the Truthcoin white paper and has recently gained popularity through EigenLayer.It essentially mitigates the need for social protocols among base layer validators by allowing node operators to express their preference for intersubject errors and claims at the restake layer through EIGEN tokens.

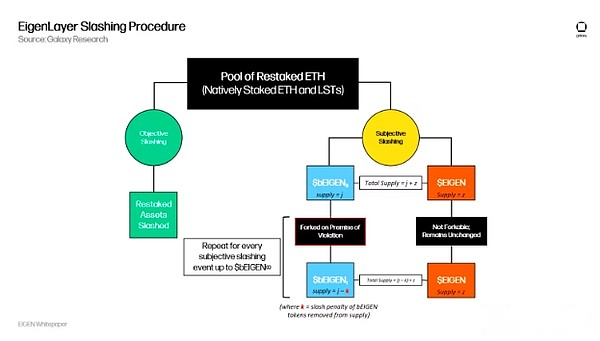

The following figure highlights the EIGEN token cut-off procedure:

The objective cut-down procedure is shown on the left side of the picture above.Objective penalty cuts are mathematically proven violations such as double signatures and downtime, which can be verified through on-chain protocols.For these violations, the re-private assets can be cut without general consent between chain observers.The inter-subject cut procedure is shown on the right side of the figure.Punishment in these cases may require social agreements between chain observers.With EIGEN tokens, node operators can rely on protocols that cut staked EIGEN supply instead of staked ETH.Therefore, EIGEN has two “categories”:

1) Original EIGEN, which can be stored in an externally owned account (EOA) or used to interact with a decentralized finance (DeFi) application.

2) bEIGEN or pledge EIGEN, forked and may be subject to a reduction penalty.

Each new fork of bEIGEN results in a decrease in supply, as the cut penalty manifests as the removal of the cut off violators from the circulation supply.By cutting tokens and reaching social consensus on the next fork, EigenLayer can more effectively extend Ethereum PoS security beyond its boundaries by limiting the input required by the Ethereum base layer.If you like, AVS can also replace EIGEN with its own token as an inter-subject token.This is a basic explanation of how the EIGEN token and inter-subject cuts work; precise details can be found in the EIGEN white paper.

Cosmos’ objective flaws

With replication security, AVS is limited to cuts in the same way as Cosmos Hub.This includes downtime and double signatures, objectively verifiable failures resulting in imprisonment and up to 5% of the stake cuts.Part of this is that replication security requires the vast majority (over 95%) of base layer economic security and validators to protect AVS.Therefore, validators conspiring to attack the consumer chain will lead to a plunge in the price of ATOM (Cosmos Hub staking assets).This idea does not apply to partially set security or EigenLayer’s restaking methods, as only a small percentage of the total interest can be used to protect AVS.

Cosmos Hub validators vote on governance proposals to review which AVSs can be protected by replication security.This process reviews the consumer chain before they can participate in shared security.Once accepted as a consumer chain and launched on the mainnet, additional measures are taken to protect the Hub from consumer chain cuts.They include:

1) Governance proposals to review the integrity of AVS’ dual signature statements for Hub node operators.This protects Hub from accepting slash packets sent by malicious AVS, thus permanently deleting honest validators in the network.In the future, Cosmos Hub developers are working to enable AVS to submit slash packets that can be automatically verified by Hub, rather than through governance.Proposal #818 is an example of this process.In this case, two Hub validators unexpectedly double-signed on Neutron (Cosmos Consumer Chain).

2) Restrict or stratify slash penalties for downtime, so that at a single point in time, only 1% of the Hub validator sets can be slashed and imprisoned.This keeps Hub active even if there is real misbehavior at the AVS layer.However, proving downtime with encryption can be difficult.

3) Limit the impact of consumer chain on slash parameters.Only Hub validators can outline the penalties that consumer chains can impose on their stakes and validator sets.Doing so ensures that the Hub’s activity and overall security are not threatened by AVS.

Fraudulent voting will be introduced in the next iteration of Cosmos Shared Security.These governance proposals allow for the reduction of validators who perform non-objective verifiable attacks that stem from the characteristics unique to partial set security (i.e., subset issues).

Restaking introduces the possibility of cutting back on additional parameters based on AVS enforcement (rather than strictly executed by the underlying chain).This introduces a higher degree of reward and punishment.However, on Cosmos Hub, the ability of consumer chains to enforce additional cuts is strictly limited and controlled by Hub validators through governance.On Ethereum, due to its restaking solutions and the nascent and diversity of AVS, the impact of cuts on the security of the underlying chain is not yet clear.Similarly, no penalties are currently imposed on Ethereum’s largest restaking solution, EigenLayer AVS.In the future, it may be introduced in EigenLayer to support automatic cuts initiated by AVS, resulting in the damage to protecting Ethereum’s underlying interests.

Centralization of equity allocation in basic chain

The same reasons for promoting centralization of equity in the underlying network environment can exert additional concentrated pressure through verification of AVS.This is driven primarily by the revenue and overall profitability generated by node operators (integrated with the opportunities offered by AVS), their timing of listing and scaling capabilities.Therefore, measures taken to prevent the centralization of equity in the basic agreement, whether they are the rules that are enforceable by the algorithm or the self-regulatory measures taken by the base layer validators, may be circumvented by the introduction of re-staking proceeds.

What is unique about replication security is that the Cosmos Hub validator set and native stakes are effectively replicated in AVS, and each node operator participating in replication security runs the same additional service.However, the rewards received by node operators from their entitlements are not equal.Node operators with larger management equity balances receive higher rewards than node operators with smaller management equity balances.While all Hub node operators have the same cost to protect AVS, the rewards are variable depending on the number of interests managed.Therefore, Hub node operators with large administrative stake balances have a better chance of offsetting the cost of protecting new AVS.Smaller node operators face greater risks of operating at a loss or shutting down operations completely.

Under the implementation of partial collection security and secure aggregation, the cost/reward dynamics of running AVS will change for node operators as they will be able to choose to protect different AVS collections.However, this may still lead to large node operators unequally receiving staking rewards, as users may choose to delegate additional staking to operators that receive higher restaking benefits than other operators.In these cases, the staking distribution of the base layer may experience stronger centralization pressure than it is now.

Re-staking will also bring centralized pressure to Ethereum.Certain restaking agreements such as Karak and Symbiotic do not provide permissionless Beacon Chain node operators to join.In these cases, users who want to re-stake native ETH must do so through a set of licensed node operators, otherwise the user can pledge other assets (such as LST), which are already the source of centralization of the underlying layer.Re-staking agreements that support native re-staking without permission are more beneficial for the centralization of the base layer staking because it allows anyone to obtain re-staking rewards at any time without a set of licensed node operators.EigenLayer supports native staking ETH through EigenPods without permission.Any user can start EigenPod to run as the Beacon Chain validator node operator and receive a restake reward.To do this, node operators must enable the EigenLayer smart contract to implement additional cuts on the ETH they staked.As of June 27, 2024, 3.9 million native ETHs have been locked in EigenPods.

Re-staking of liquidity on Ethereum will also create centralized pressure.LRT applications that accept native ETH deposits as re-solidated collateral may centralize Beacon Chain staking in a manner similar to LST applications.LST applications incentivize users through higher staking returns and liquidity of native ETH deposits, just like LRT applications.The advantage of LRT over LST is that LRT passes on the additional benefits of restaking to the user, while LST does not.If the LRT application does not accept native ETH as re-staking collateral, the user must pledge other assets, most commonly LST, thereby increasing the demand for LST and increasing the concentration of these current pledged assets at the base level.

Risks faced by node operators

The risks faced by node operators are primarily operational risks, related to their ability to scale and establish streamlined processes for adding and removing AVS.Failure in any of these areas can lead to reduced staking or lack of competitiveness in the product.Each AVS added by a single node operator brings them additional complexity, cost, and responsibility.

Different types of AVS also mean that node operators may require unique costs and procedures to support each AVS, making processes and infrastructure across services difficult to replicate.This can cause node operators to run dozens or even hundreds of services, requiring unique infrastructure and processes to run across hundreds to thousands of validators.Ultimately, the diversity of AVS may make scaling and management operations of node operators very difficult.

Cancelling AVS-supported programs is as important as adding support.In the context of restaking, AVS churn may be high, which is particularly important.Ensuring a smooth downstream process is important to avoid being cut or causing chaos in AVS operations.This is especially true when the node operator uses the same server to run AVS and Ethereum validator software.

Node operators also face social risks.Adding and deleting AVS directly affects the benefits and risks of end users who restake assets through restaken node operators.It is an extremely important responsibility of the node operator to convey details about opt-in/exit AVS and notify the end user of operations that may affect their entrusted funds.Failure to do so may lead to a decrease in end-user trust, which can damage the business and pose reputational risks to node operators.

Risks of proactive verification of services

Economic security is shared or centralized under restaking, which means that many AVS and underlying chains have the right to cut the same value that jointly protects them.The risk is that entities outside the protocol may directly affect the security of AVS (AVS to AVS and base chain to AVS), such as the impact of AVS cuts on base chain security.Other AVS and underlying chain cut risks include protecting the dollar value fluctuations of AVS’ assets, and their ability to fully incentivize node operators.

Economic security is measured in US dollars and is provided in native units of digital assets (for example, AVS is guaranteed by ETH worth $100 million).Protecting the value of AVS’s assets to fluctuate its economic security.Using higher quality, more liquid assets to protect AVS is key to mitigating their economic security volatility.Some AVS may still choose to use more volatile assets for various reasons, such as new user acquisition or ecosystem coordination.The risk of US dollar fluctuations is not unique to AVS, and the underlying chain also faces the same resistance, namely, the US dollar value fluctuations of native pledged assets, especially in the first few months and years after the mainnet is launched.

Second, node operators and end users put pressure on AVS to generate enough “real” value (whether from transaction fees or revenue generated by AVS features) to make them profitable enough for node operators to serve them.Therefore, AVS may choose to launch with inflation tokens to fully repay debts owed to node operators.Even so, over time, node operators may think they are not receiving enough incentives to continue running certain AVS.This may cause some AVSs to not have enough validators and staking assets to protect them, which will negatively affect the security of these AVSs.

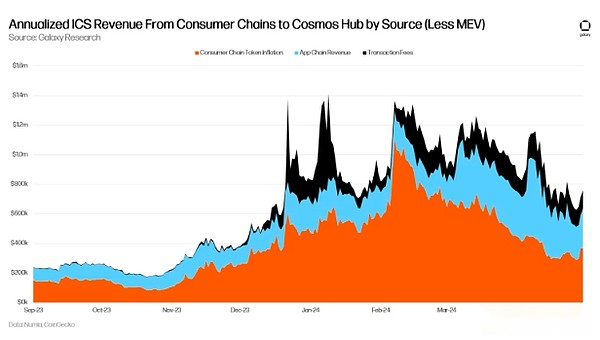

While we don’t know what the incentive landscape will look like with EigenLayer resolution, we have some idea of how Cosmos replication security (excluding MEV) will look like before April 2024 (the price per ATOM is about $8.75).Galaxy Research estimates that the consumption chain adds about 0.04% to Hub validators, or $0.003 per ATOM earned by voting rights.

Under replication security, the difference between resolution dynamics on Cosmos and Ethereum is that the market-driven nature of EigenLayer allows the supply and demand of resolution services to naturally find a balance when they are too scarce or too rich.

Similarly, in the first few months and years after the mainnet was launched, the basic chain faced the same resistance, which was to motivate people to participate in security.However, these two risks are especially important for AVS dependency restaking solutions, because they do not directly possess the security they depend on.Depending on the restaking yield and EigenLayer smart contract capabilities, competition for shared security can be intense between AVS and causes validators to frequently retune the set of AVS they support at any given time.This in turn may promote faster turnover of AVS and intensify volatility in AVS economic security.

Other considerations

There are some other risks and considerations worth highlighting.These include replenishment and leverage, the impact of airdrops on replenishment agreements, and the impact of replenishment on asset liquidity.

Re-pled and leveraged

Re-pled itself is not financial leverage.Instead, it is a more abstract type of leverage, depending on the responsibilities and capabilities of the node operator.This is because node operators are penalized for their actions and operational capabilities in the AVS rules they opt into, rather than based on asset prices (such as margin approximation).This is similar to taking on more and more responsibilities at work.The more projects you take on, the more likely you are to make mistakes, get fired, or lose your salary.However, if you misallocate your own company-sponsored 401k and lose all your savings, you won’t lose your job.

The penalty basis for restaking is within the control of the node operators because they voluntarily opt in to cut conditions and control the hardware/software they run.This is not the case with financial leverage, because individuals cannot control the market that ultimately punishes them.This is a key difference, because the basis of punishment depends entirely on the capabilities and behavior of the node operator. The punishment for one node operator will not affect the interests of another node operator (i.e., a validator cannot be used for anotherA validator’s wrong behavior is cut), just like the negative feedback loop/daisy chain effect of financial leverage lifted.

Even so, as explained earlier in this report, penalties on node operators may have a chain effect on the security of AVS and underlying chains.For example, if 1 ETH protects three AVSs are cut by one of them, then all three AVSs protected by this 1 ETH have a negative impact on their security.This can make malicious attacks and collusions on AVS and its underlying chains easier.

The impact of airdrop mining and chasing rise and fall on re-polization

Airdrop mining may distort the supply of restaken tokens.Points incentivize users to deposit assets into replenishment agreements without being affected by the demand for replenishment securities of AVS, thereby increasing the supply of replenishment assets.Airdrop mining can also have a negative impact on the design of the application.The fast-paced nature of points and the momentum of the ecosystem may prompt developers to launch applications before they are ready to be deployed or fully enriched for their intended use.The result could be Phantom apps that are not used for a long time, or applications that lack critical features, such as the ability to extract or transfer assets.Ultimately, all of this force driving re-private inorganic supply must be lifted, which could negatively impact asset prices and lead to other problems with the DeFi products associated with re-private.Over time, the industry will have a clearer understanding of what the real supply of restaking looks like (which is a function of demand), especially as restaking protocols deployed on Ethereum and Cosmos become more fully functional.

Re-private liquidity vacuum

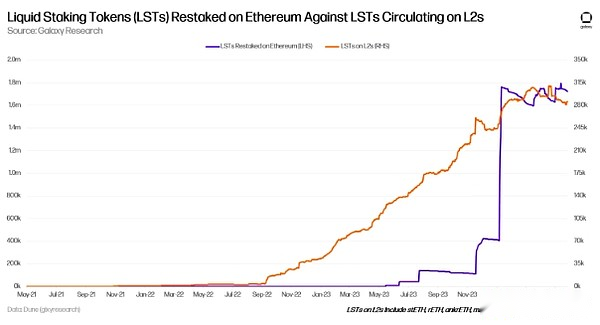

Another consideration in the context of Ethereum restaking is to attract liquidity to Ethereum L1.The goal of Ethereum’s rollup-centric roadmap is to drive L1 activity and liquidity downlink, but restaking incentivizes activity to stay or return to L1.This dynamic is highlighted through restaking protocols and LRT protocol-level points planning.

The following figure shows this trend from the perspectives of restaking LSTs on Ethereum L1 and LSTs on L2.The number of LSTs on L2 peaked in April 2024 and has been in range volatility since February 2024 after 21 months of sustained growth.Meanwhile, the number of LSTs pledged on Ethereum L1 has grown parabolicly.

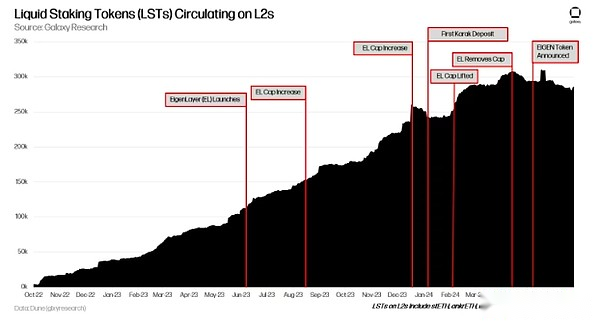

The figure below tracks the full process trend of LST observed on L2 and superimposes key replacing events.

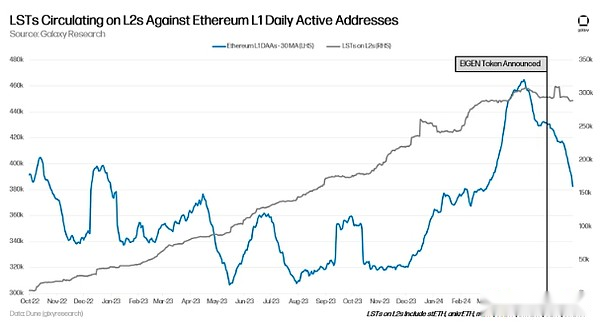

With LST liquidity on L2 and hype about restaking applications increasing, the Daily Active Address (DAA) on Ethereum L1 also reached its highest level in 35 months with a 30-day moving average;This indicates that restaking is attracting users to return to L1.The 30-day moving average of the number of DAAs on Ethereum last reached 460,000 addresses in May 2021.

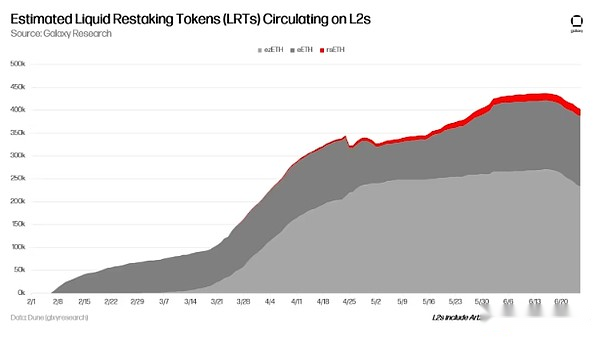

While LST liquidity on L2 has been flat, LRT has become increasingly prominent.LRT can be found on Arbitrum, Base, Blast, Linea, Mode, OP Mainnet, and Scroll, with 69% of native unit supply on Arbitrum and Blast.What is not shown in the chart is 24,744 ezETH and 7,396 eETH on Mode.

Despite the increasing importance of LRT on L2, LST has a much higher liquidity and adoption rate than LRT.However, as described in the above analysis, the importance of LSTs begins to diminish because they are locked in the restaking protocol initiated on the Ethereum base chain.It is important to consider the potential impact of stagnant LST expansion on the overall liquidity of decentralized financial applications on L2, especially when LRT liquidity is comparable.

in conclusion

Re-staking is an important primitive in the evolution of public chains; it aims to create a more unified and efficient security model for blockchain applications that can be exported and shared by multiple protocols at the same time.This idea and its implementation in the Ethereum and Cosmos ecosystems are still in the early stages of experimentation and research.Many details about how restaking agreements work in practice are still unknown.Furthermore, their exact impact on stakeholders such as base networks, node operators, and AVS remains unclear.However, in this report, we detail the important risks and considerations of restaking at the early stages of its evolution for the major entities participating in the activity.Areas for further research include mobile restaking agreements and other types of products and services that can be built on restaking agreements.