Author: ASXN Digital Asset Research Company, Translation: Bitchain Vision xiaozou

The Ethereum spot ETF will be launched on July 23.There are many aspects of ETH ETF that are not visible in BTC ETFs and are easily overlooked by the market.

ETHEOutflow forecast

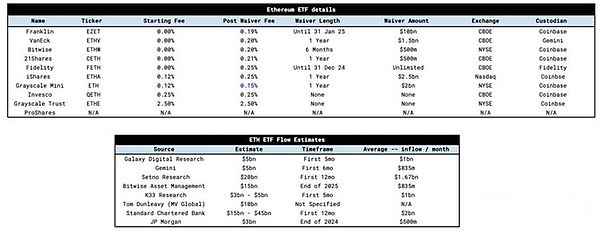

ETF ETFs have a charging structure similar to BTC ETFs.Most ETF providers do not charge any fees for a specific period of time in order to better accumulate asset management scale.As is the case with BTC ETFs, Grayscale has been keeping its ETHE rate at 2.5%, an order of magnitude higher than other providers.The key difference here is the introduction of the Grayscale mini ETH ETF, which was previously applied for use in a BTC ETF but was not approved.

This mini trust product is a new ETF product from Grayscale, with an initially disclosed rate of 0.25%, similar to other ETF providers.Grayscale’s idea is to charge a 2.5% fee from less active ETHE holders while attracting more active, more cost-sensitive ETHE holders to their new product without letting the money go awayOn lower-cost products, such as Blackrock’s ETHA ETF.After other providers cut 25bps fees over Grayscale, Grayscale pulled back the mini trust fee to 15bps, making it the most competitive product.Most importantly, they transferred 10% of the ETHE AUM (Asset Management Size) to the mini trust and presented this new ETF to the ETHE holders.This transition is completed based on the same basis, which means it is not a taxable matter.

The corresponding impact is,GBTCCompared with the holder transitions to this mini trust,ETHEThe outflow will be more gentle.

ETH ETFInflow forecast

There are many valuations regarding ETF inflows, and we highlight some of them below.These valuations are standardized and the average valuation is $1 billion per month.Standard Chartered Bank has the highest valuation at $2 billion per month, while JP Morgan has a lower valuation at $500 million per month.

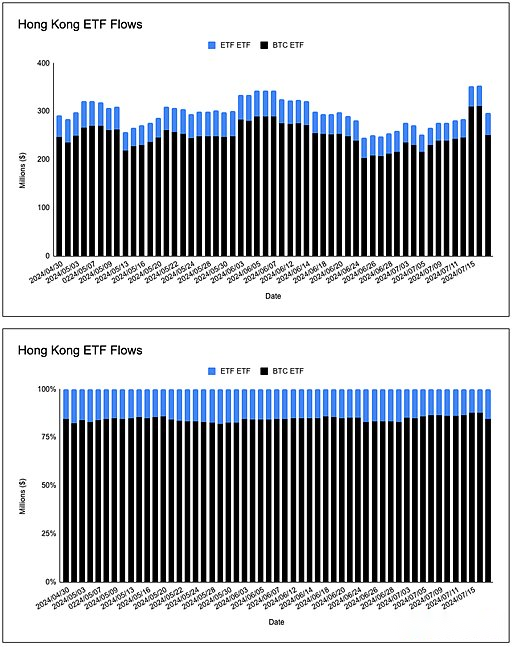

Fortunately, we received help from Hong Kong and European ETP (exchange-traded products) and the ETHE discount closing to help us estimate traffic.If we look at the asset management scale of Hong Kong ETP, we can draw two conclusions:

(1) The relative asset management scale of BTC and ETH ETP is higher than that of BTC vs. ETH, with a relative market value of 75:25, while the asset management scale is 85:15.

(2) In these ETPs, the ratio of BTC to ETH is quite constant and is consistent with the ratio of BTC market value to ETH market value.

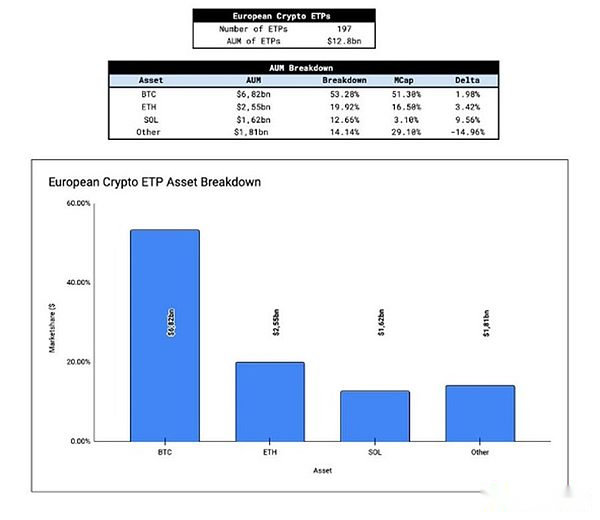

In Europe, we have a larger sample size to study—197 cryptocurrency ETP with a cumulative asset management scale of US$12 billion.After we conducted data analysis, we found that the segmented data of the asset management scale of European ETP is roughly consistent with the market capitalization of Bitcoin and Ethereum.Solana is over-allocated relative to its market capitalization, at the expense of “other encrypted ETP” (anything except BTC, ETH or SOL).Solana aside, a model is beginning to emerge—a global breakdown of asset management scale between BTC and ETH roughly reflects a market capitalization-weighted basket.

Given that GBTC outflows are the origin of the narrative of “sell the news”, it is important to consider the possibility of ETHE outflows.To simulate potential ETHE outflows and their impact on prices, it is necessary to view the proportion of ETH supply in ETHE.

Once adjusted according to Grayscale Mini Seed Capital (10% of ETHE AUM), the ETH supply ratio is similar to the GBTC at the time of release as a function of the existing total supply in ETHE.It is not clear how the rotation vs. exit ratio of GBTC outflow is, but if we assume that the rotation flow is similar to the exit flow ratio, thenETHEThe impact of outflow on priceGBTCThe outflow is similar.

Another key message that most people ignore is ETHE’s NAV (Net Asset Value) premium/discount.ETHE has been trading within the 2% coupon value range since May 24, while GBTC traded within the 2% net asset value range for the first time on January 22 (just 11 days after GBTC converted to ETF).The approval of spot Bitcoin ETFs and its impact on GBTC are slowly reflected in the market, while the ETHE discounts for NAV transactions are more reflected in the existing narrative of GBTC.

When the ETH ETF goes live, ETHE holders will have 2 months to exit in a price range close to the face price.This is a key variable that will help prevent ETHE outflow, especially exit traffic.

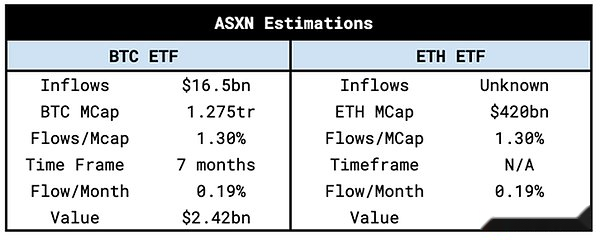

ASXNThe internal estimate is monthly8Yizhi12$100 million.This is by weighted average of monthly Bitcoin inflows and multiplying byETHThe market value is calculated.

Our estimates are supported by global cryptocurrency ETP data, suggesting that the market cap weighted basket is the dominant strategy (we may see rotational flows from BTC ETFs, with a similar strategy).Additionally, given the unique dynamics of ETHE trading at face value prior to launching and launching the mini trust, we are open to the surprise of upward ETH price.

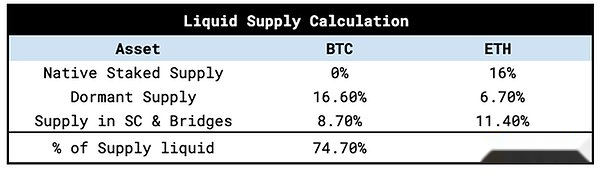

Our estimates of ETF inflows are proportional to their respective market caps, so the impact on prices should be similar.However, it is also important to measure how much proportion of an asset is liquid and can be sold – assuming that the smaller the “circulation rate”, the greater the price will react to inflows.

There are two special factors that affect the liquid supply of ETH, namely the supply in native staking and the supply in smart contracts.Therefore, the flow and percentage of ETH is lower than BTC, making it more sensitive to ETF inflows.It is worth noting, however, that the liquidity difference between the two assets is not as large as some think (ETH’s cumulative +-2% order depth is 80% of BTC).

Our approximate calculations of liquid supply:

Ethereum reflexiveness

When we are studying ETFs, it is very important to understand the reflexivity of Ethereum.This mechanism is similar to BTC, but Ethereum’s destruction mechanism and the DeFi ecosystem built on it make the feedback loop even more powerful.

The reverse loop looks like this:

ETH inflows in ETH ETF → ETH price increases → interest in ETH → DeFi/chain usage increases → DeFi basic indicators improve → EIP-1559 destruction increases → ETH supply decreases → ETH price increases → More ETH inflows in ETH ETF → RightETH’s interest rises → …

One thing that BTC ETFs are missing is the lack of “wealth effect” in the ecosystem.In the emerging Bitcoin ecosystem, we don’t see much profit being reinvested into projects or protocols at the base layer.As a “decentralized application store”, Ethereum has a complete ecosystem and will benefit from the continuous inflow of underlying assets.

We believe that this wealth effect has not been paid enough attention, especially in DeFi.There are 20 million ETH ($63 billion) of TVL in the Ethereum DeFi protocol. As ETH trading rises, ETH DeFi’s investment appeal is becoming more and more attractive as USD-denominated TVL and revenue surge.

ETH has a reflexive nature that does not exist in the Bitcoin ecosystem.

Other factors to consider

1. What will be the rotational inflow from BTC ETF to ETH ETF?Suppose there is a portion of BTC ETF configurators who are reluctant to increase their net cryptocurrency exposure but want to diversify.TradFi investors in particular prefer market cap weighting strategies.

2. How well does TradFi understand ETH assets and Ethereum smart contract layer?Bitcoin’s “digital gold” narrative is both easy to understand and well-known.How much will the narrative of Ethereum (the settlement layer of the digital economy, three-point asset theory, tokenization, etc.) be understood?

3. How will previous market conditions affect ETH’s traffic and price trends?

4. The elites in the Ivory Tower have designated two crypto assets as bridges to their world – Bitcoin and Ethereum.These assets have crossed the well-known spirit of the times.How the launch of spot ETFs has changed the way TradFi capital allocators think about ETH considering they are now able to offer products that can be charged.TradFi’s desire for earnings makes the native earnings Ethereum through staking very attractive to providers, and we believe that staking ETH ETFs is “if” rather than “when”.Providers can offer 0-fee products, and simply staking ETH on the backend to earn an order of magnitude higher than the normal ETH ETF fee.