Source: Simrit Dhinsa, Simrit Dhinsa, Samuel Kiernan, Gabe Parker, Zack Pokorny, Galaxy; Compilation: 0xjs@Bit chain vision world

introduction

In the first half of 2024, it was the critical period of the Bitcoin mining industry, and the economic situation changed significantly, and the market dynamics continued to evolve.Miners have experienced economic changes in roller coasters. At the beginning of the year, they have performed strongly. Until the fourth halves of Bitcoin, the incident occurred, and then the hash price fell to the lowest point of history.Despite these fluctuations, large miners still unswervingly adhere to their growth trajectory. After the depression, the economic downturn has stimulated a series of mergers and acquisitions in this field, because the miners seek integration and benefit from the scale.

In addition, the integration of AI and high -performance calculation (HPC) trend and Bitcoin mining provides miners with opportunities to distribute capacity to meet the demand curve of continuous and continuous index growth in AI/HPC.As the report is shown in the title, with Bitcoin miners, large -scale enterprises and other enterprises in competition in land and electricity, the value of Gigamine has increased significantly.Those companies with recent energy channels will have unique advantages and can use the trends of these two industries.

In this report, we will explore the change of Bitcoin mining,First of all, outline the current status of the mining economy, and then expand to the key themes after halving, such as constantly changing capital market patterns, huge demand for power capacity, increase in mergers and acquisitions, and the growth of the growth of computing power in the second half of the yearEssence

Key points

-

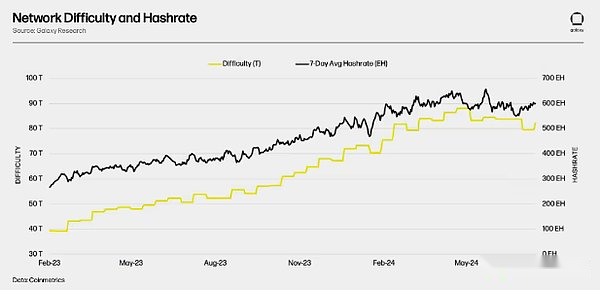

The difficulty of mining has decreased from a peak of 88.1 T (implicit computing power 630 EH), and the low point of 79.5 T (hidden computing power 569 EH) after the halving in early July, because computing power has set a new low in history.As of writing this article, the difficulty is 82.0 T (implicit computing power 587 EH).

-

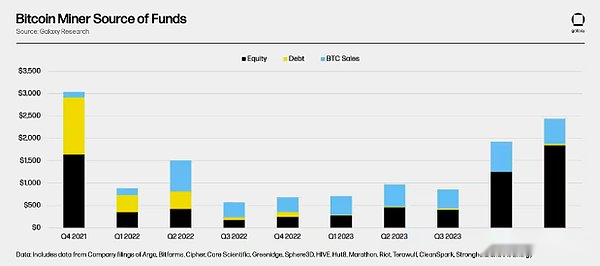

In the first quarter of 2024, the listed mining company raised a total of $ 1.8 billion in equity capital, setting the highest level of raising amounts in the past three years in the past three years.

-

Although the mining companies have raised funds through the issuance of stocks in recent months, as the value of available power capacity has soared, we expectThe debt capital market will reopen in the second half of 2024 and 2025.

-

Miners who have obtained large -scale power capacity, purchased long -term infrastructure and can obtain water and fiber are most likely to use the AI revolution.

-

In our annual report, weIt is estimated that the target range of computing power at the end of 2024 is 675 EH to 725 EHEssenceNow, combined with the analysis of the information, seasonal trends and profitability of listed mining companies, we will increase growth to between 725 EH and 775 EH.

-

From January 1, 2024 to July 23, 2024, Bitcoin miners generated a transaction fee of 12.97K BTC (as of July 23, 2024).Miners earned about 55%(23.4K BTC) of the total cost of 2023.

-

So far this year, various types of transactions have reached more than 460 million US dollars, mainly including venue sales, reverse mergers and acquisitions and company acquisitions.We expect,In the future, the industry’s mergers and acquisitions will continue.

Market situation

The mining economy in the first half of 2024

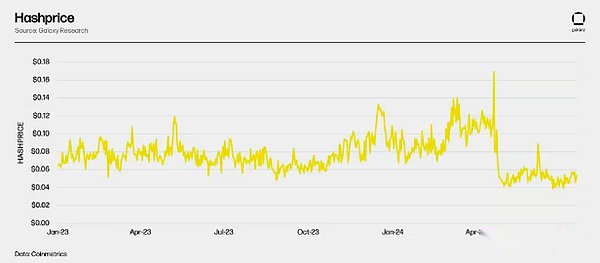

In the first half of 2024, it can be described as a story of two quarters.In the first quarter of 2024, miners enjoyed the best economic benefits in the past two years.Promoted by the rise in Bitcoin prices, the average price of hash this quarter was $ 0.094/Th.The computing power continues to rise steadily this quarter to offset the part of Bitcoin prices.The strong profit margin in the first quarter of 2024 was necessary to establish a cash balance before the fourth half of the second quarter of 2024.

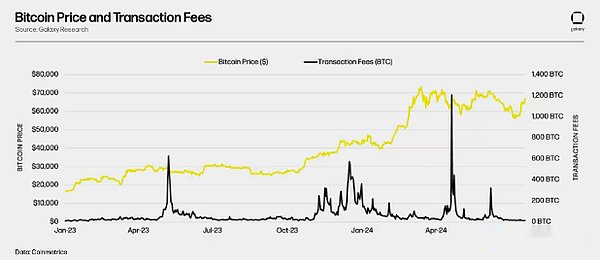

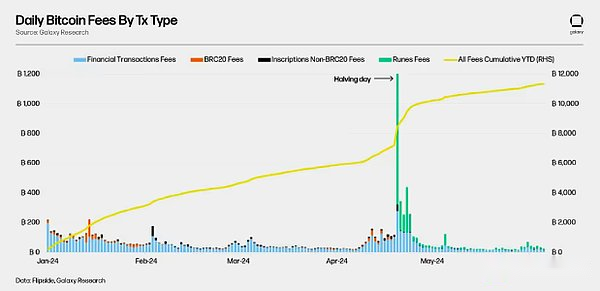

Before Bitcoin halved the fourth time, the mining economy in the second quarter remained strong.During the halving period, the highly anticipated Runes launched a trading fee storm for several days.In the week after half, the miners have generated considerable transaction income, and we will further discuss in the next section.

The transaction fee increased the market price to $ 0.17/Th in a short period of time, which reversed the impact of the decrease in block subsidies.Recall that the price of hash is the first choice of miners to extract the total income of each TH computing power every day.However, this soaring is very short, and after the transaction fee is stable, the hash price has reached a record low.Since halved, the average price of hash is $ 0.054/Th.

The transaction fee increased the market price to $ 0.17/Th in a short period of time, which reversed the impact of the decrease in block subsidies.Recall that the price of hash is the first choice of miners to extract the total income of each TH computing power every day.However, this soaring is very short, and after the transaction fee is stable, the hash price has reached a record low.Since halved, the average price of hash is $ 0.054/Th.

The difficulty of mining has decreased from the peak of 88.1 T (the implicit computing power 630 EH), and the low point of 79.5 T (hidden computing power 569 EH) after halving in early July, because the computing power set a record low.As of writing this article, the difficulty is 82.0 T (implicit computing power 587 EH).

At the current level of hash, a considerable part of the miners in the network are still profitable, but the profit margin is small.Some miners with a wait -and -see attitude may continue to operate because they can produce positive gross profit.However, when considering operating costs and additional cash costs, many miners found that they were unable to map, and cash was slowly used up.In the first quarter of 2024, the strong economic situation helped establish a cash balance, which extended the survival of inefficient miners.If the price or transaction fee of Bitcoin has not risen significantly, we expect that if the hash price will fall further, some miners will withdraw from the Internet.

At the current level of hash, a considerable part of the miners in the network are still profitable, but the profit margin is small.Some miners with a wait -and -see attitude may continue to operate because they can produce positive gross profit.However, when considering operating costs and additional cash costs, many miners found that they were unable to map, and cash was slowly used up.In the first quarter of 2024, the strong economic situation helped establish a cash balance, which extended the survival of inefficient miners.If the price or transaction fee of Bitcoin has not risen significantly, we expect that if the hash price will fall further, some miners will withdraw from the Internet.

Even if this happens, the downlink pressure caused by network computing power due to the non -profit -seeking miners off the machine will be offset through the new generation of special integrated circuit (ASIC).The nominal computing power of the new generation machine is more than twice the computing power of the previous generation.Based on the market value, seven of the top ten public miners are expected to invest 109 EH in the second half of 2024.As we are analyzing at the end of the report, although we have recently decreased, we believe that the computing power will rise sharply in the second half of 2024.If the price of Bitcoin does not rise, it will bring resistance to miners.

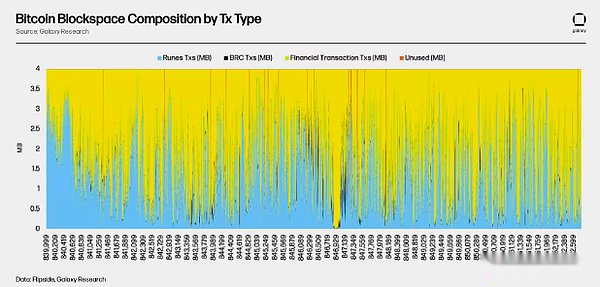

Transaction fee fluctuation

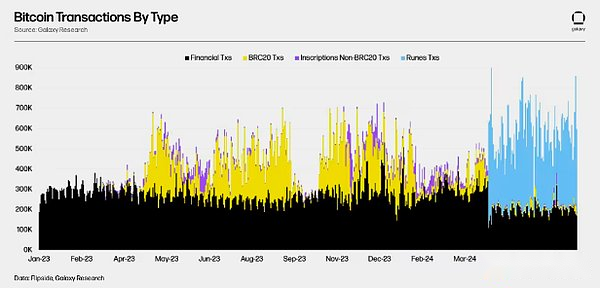

Since January 1, 2024, Bitcoin has contributed more than 99 million chain transactions.Of these 99 million transactions, 50% is a standard transaction, and we define it as a financial transaction.Runes, BRC-20 and Ordinal transactions account for 35%, 11%, and 4%of the transaction volume, respectively.Considering the homogeneous token agreement launched on April 19, 2024, RUNE -related transactions accounted for 35% of the total transaction volume of the total market share.Since its launch, Runes has an average of 63%of all Bitcoin transactions.

From January 1, 2024 to July 23, 2024, Bitcoin miners incurred a transaction fee of 12.97k BTC (as of July 23, 2024).Miners earned about 55%(23.4K BTC) of total cost of 2023.The fourth decrease of Bitcoin occurred on April 19, 2024, making 2024 a milestone year.On the day of the minus, the daily fee paid to the miners soared to a historical high, exceeding 1,200 BTC.This surge is largely due to the launch of Runes, which is a new UTXO -based homogeneous tokens, which debuted on the mining block.On this block, the Rune token XXXXFHUXXXXX has paid a fee of $ 23 million, becoming the first RUNE collection contained in the depression of the block (block 840,000).It is worth noting that 2,411 BTCs (19%) of the costs incurred to the present to the present are from half -day and three days after the decrease.

From January 1, 2024 to July 23, 2024, Bitcoin miners incurred a transaction fee of 12.97k BTC (as of July 23, 2024).Miners earned about 55%(23.4K BTC) of total cost of 2023.The fourth decrease of Bitcoin occurred on April 19, 2024, making 2024 a milestone year.On the day of the minus, the daily fee paid to the miners soared to a historical high, exceeding 1,200 BTC.This surge is largely due to the launch of Runes, which is a new UTXO -based homogeneous tokens, which debuted on the mining block.On this block, the Rune token XXXXFHUXXXXX has paid a fee of $ 23 million, becoming the first RUNE collection contained in the depression of the block (block 840,000).It is worth noting that 2,411 BTCs (19%) of the costs incurred to the present to the present are from half -day and three days after the decrease.

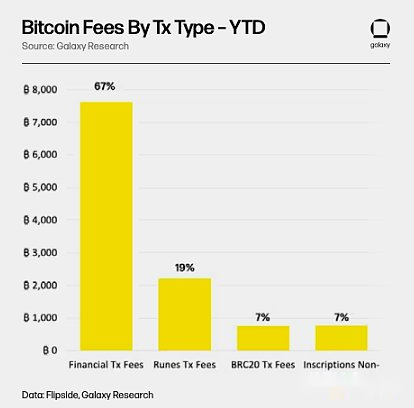

Since January 1, 2024, 67% of miners’ cost income came from standard financial transactions, while 19% came from Runes.BRC-20 and Ordinals transactions account for 14%of Bitcoin costs since the beginning of the year.

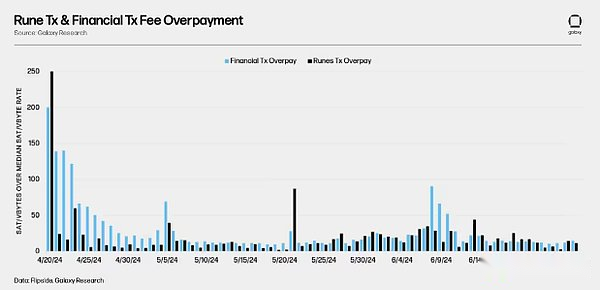

“Excess Payment” refers to the cost of transaction in the block (in the unit of SATS/VBYTE), which is higher than that of SATS/VBYTE in the same block.We choose the mid -range SATS/VBYTE level, because we believe that if you are a high time preference user, bidding near this level will provide you with a reasonable opportunity to be included in the next block.The transaction that deliberately sets up higher SAT/VBYTE rates usually has time sensitivity.During the fourth half of Bitcoin, April 20, 2024, trading costs soared sharply.The daily median counting rate reaches 590 SATS/VBYTE, and within an hour after half of the block, the average median block rate has soared to 1,840 SATS/VBYTE.Rune -related transactions pay the fee for the median/VBYTE level of 250 SATS/VBYTE (42%higher than the medium number SATS/VBYTE), which is included in the half -half block and several areas subsequent areas.piece.During the same period, the cost paid by standard financial transactions was 200 SAT/VBYTE higher than the median SAT/VBYTE (34%higher than the median SAT/VBYTE).Since halving, standard financial transactions have paid 51 days in terms of expenses than Rune transactions, and RUNE transactions have been paid for 18 days in terms of expenses than standard financial transactions.

“Excess Payment” refers to the cost of transaction in the block (in the unit of SATS/VBYTE), which is higher than that of SATS/VBYTE in the same block.We choose the mid -range SATS/VBYTE level, because we believe that if you are a high time preference user, bidding near this level will provide you with a reasonable opportunity to be included in the next block.The transaction that deliberately sets up higher SAT/VBYTE rates usually has time sensitivity.During the fourth half of Bitcoin, April 20, 2024, trading costs soared sharply.The daily median counting rate reaches 590 SATS/VBYTE, and within an hour after half of the block, the average median block rate has soared to 1,840 SATS/VBYTE.Rune -related transactions pay the fee for the median/VBYTE level of 250 SATS/VBYTE (42%higher than the medium number SATS/VBYTE), which is included in the half -half block and several areas subsequent areas.piece.During the same period, the cost paid by standard financial transactions was 200 SAT/VBYTE higher than the median SAT/VBYTE (34%higher than the median SAT/VBYTE).Since halving, standard financial transactions have paid 51 days in terms of expenses than Rune transactions, and RUNE transactions have been paid for 18 days in terms of expenses than standard financial transactions.

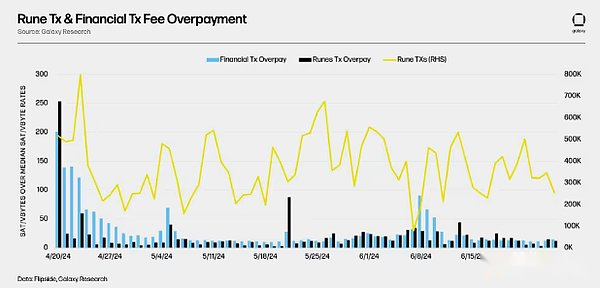

After the daily number of RUNE transactions was superimposed with the figure above, we found that the surge in Rune transactions was positively correlated with the surge in financial transactions.Sensitive financial transactions are forced to incorporate a competition block with Rune.Although the RUNE transaction will be incorporated in the block when the RUNE transactions surge in the surge in the RUNE transaction, these are regarded as an abnormal value related to the specific Rune token coin.

Block analysis data can be found that in the 10 -minute interval, the frequency of standard financial transactions and Runes transactions is different.Since halving half of the block (840,000 blocks), the average financial transaction has an average of 2.4 MB per block, while the Runes transaction has always occupied about 1.5 MB of block space.Although Runes is a more efficient homogeneous token standard than BRC-20 (0.06 MB per block), Runes’s dominant position on block space highPreferences.In the halving block, the Runes transaction consumed 2.7 MB, accounting for about 68%of the 840,000 total space.

Growth/infrastructure

Continuously changing capital market structure

In the first half of 2024, miners raised unprecedented funds.Since the fourth quarter of 2023, due to the expectations of the spot Bitcoin ETF, the valuation has begun to soar, and the miners continue to raise funds (mainly equity) to rapidly expand the scale until half.In the first quarter of 2024, the listed mining companies raised a total of 1.8 billion US dollars, setting the highest amount of raising in a single quarter in the past three years.

Before halving, miners actively raised funds to support rapid growth, holding Bitcoin, improving the efficiency of miners, and establishing cash buffer to use the opportunities in difficulties.Among the $ 1.8 billion raised, 75% came from the top three miners in the market value: Marathon, Cleanspark, and RIOT.Bitmain and MicroBT launched a new generation of mining machines at a very attractive price, which further exacerbated the sense of urgency of the miners, prompting them to expand production capacity and insert the mining machine as soon as possible to generate a strong return on investment (“ROI”).

As shown in the figure above, debt capital has basically disappeared from the market since mid -2022.Previously, the choice of debt financing available for miners was mainly revolved around the mortgage ASIC.ASIC’s challenges facing financing are ASIC pricing fluctuations, rapid depreciation of mortgage, and no additional margin in many contracts.When the mining conditions deteriorate, the machine not only reduces the cash flow, but also decreases. As LTV rises, the miners cannot repay the unable to pay off debt, and the loan is in a precarious situation.

However, as the value of power capacity soared, we expect the loan to re -enter the market in the second half of 2024 and 2025.Bitcoin miners and large -scale enterprises (that is, large data centers with scalable cloud infrastructure) have increased the value of available energy capacity on the infinite demand of power capacity.From the perspective of the lending party, the locks of miners underwriting with large -scale power capacity can be guaranteed to provide protection in the case of deterioration of the mining economy.In addition, during 2022 and 2023, miners focused on strengthening the balance sheet by reducing the reducing debt repayment and the creation of a more streamlined cost structure.Therefore, we believe that the industry is now in a more favorable position and can bear some debt, not just relying on issuing stocks to achieve growth.

Power assets are still in the price discovery period.Recently, asset sales prices have a wide range, but the overall rising trend.From the perspective of mining companies, the use of its continuous rise in the venue is attractive at the project level. This is a non -diluted alternative. It is also a differentiated factor between the peers with continuing to dilute shareholders as the main capital source.Essence

Focus on generating free cash flows and create a streamlined structure. At the same time, combining debt with cash flow can allow miners to develop in an efficient way.Extending to the field of AI and high -performance computing can also open the door to the source of new debt capital for pure miners, and these are not obtained by pure miners.

Even if there are more and more debt opportunities, the expansion “arms competition” continues, and we expect large -scale equity financing activities to last until the second half of 2024.Driven by the ambitious growth goals, the prospects of Bitcoin prices in the future, and the promotion of the AI/HPC narrative, the valuation of the listed miners has risen.The rise in these valuations helps miners to reduce the dilution of shareholders caused by equity issuance.With the large -scale listed miners announced their ambitious goals, even if the price of hash is still close to historical lows, expansion and financing activities will not seem to slow down.

MW worth millions of dollars

Miners are at the pinnacle of integrating growth trends in Bitcoin and AI/HPC.In view of the non -linear correlation between operating costs and BTC prices, the profit of the miners is still small, and it is still in a favorable position, which can benefit from the continuous bull market of Bitcoin prices.At the same time, the generation AI is one of the fastest growing technologies in history.For example, ChatGPT has 100 million users in the first two months after launch, becoming the fastest growing application in history.Coupled with the power required for the AI model training and reasoning than the power used by the traditional data center (the power consumption required for a single query of the ChatGPT is 10 times that of Google searched), the AI military reserve competition has produced a short and short -to -inGet the amazing demand of reliable electricity within time.

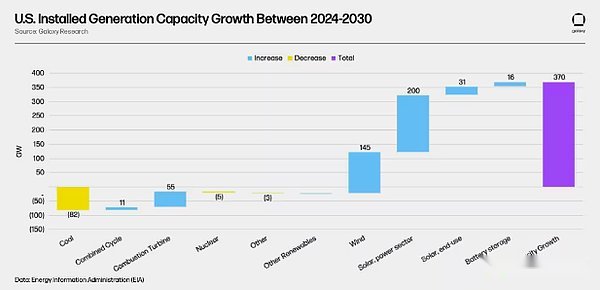

By 2030, global data center demand is expected to increase by 160%.At present, the demand for US data centers is estimated to be 21 GW, and it is expected to increase to 35 GW by 2030.The US installed power generation is expected to increase by about 370 GW during the same period.However, as shown in the figure above, the US Energy Information Administration (“EIA”) is expected to dispatch power supply (coal, natural gas, nuclear energy, etc.), which will decrease, which means that the intermittent power supply (wind energy, solar energy, etc.)It will largely fill the expected supply and demand gap.Therefore, if it is converted to Taiwa (“TWH”), it is expected that the power generation will increase by 240 TWH, and the new data center load (assuming the normal operation time is 99.995%) will increase 123 TWH (14 GW / 1000 * 8,760 hours/Year* 99.995%).The increase in intermittent power supply, coupled with the continuous growth of the demand brought by the uncomfortable data center load, may lead to the congestion, power transmission restrictions and supply shortages of power grid, because the loads of other industries (such as electric vehicles and domestic industrial manufacturing) will be expected to be loaded.increase.In the case of evaluating the rapid growth of the US growth in the United States, the power demand for the rapid growth of the United States may lead to further delay in load interconnected research and approval of climbing plans and facilities agreements.Mark Zuckerberg pointed out in an interview with Dwarkesh Podcast recently that there is currently no Gigamine Data Center. “The key is to ensure energy.” This is the biggest bottleneck in the AI super computer -driven competition.Electrical capacity competitions are in progress. Bitcoin miners with large -scale electricity, continuous land, water, and fiber connecting are the most capable of using this trend.

By 2030, global data center demand is expected to increase by 160%.At present, the demand for US data centers is estimated to be 21 GW, and it is expected to increase to 35 GW by 2030.The US installed power generation is expected to increase by about 370 GW during the same period.However, as shown in the figure above, the US Energy Information Administration (“EIA”) is expected to dispatch power supply (coal, natural gas, nuclear energy, etc.), which will decrease, which means that the intermittent power supply (wind energy, solar energy, etc.)It will largely fill the expected supply and demand gap.Therefore, if it is converted to Taiwa (“TWH”), it is expected that the power generation will increase by 240 TWH, and the new data center load (assuming the normal operation time is 99.995%) will increase 123 TWH (14 GW / 1000 * 8,760 hours/Year* 99.995%).The increase in intermittent power supply, coupled with the continuous growth of the demand brought by the uncomfortable data center load, may lead to the congestion, power transmission restrictions and supply shortages of power grid, because the loads of other industries (such as electric vehicles and domestic industrial manufacturing) will be expected to be loaded.increase.In the case of evaluating the rapid growth of the US growth in the United States, the power demand for the rapid growth of the United States may lead to further delay in load interconnected research and approval of climbing plans and facilities agreements.Mark Zuckerberg pointed out in an interview with Dwarkesh Podcast recently that there is currently no Gigamine Data Center. “The key is to ensure energy.” This is the biggest bottleneck in the AI super computer -driven competition.Electrical capacity competitions are in progress. Bitcoin miners with large -scale electricity, continuous land, water, and fiber connecting are the most capable of using this trend.

Although there are many differences between Bitcoin mining and artificial intelligence data centers, from the perspective of listing time, miners are most likely to enter the AI/High -performance computing data center market.From high -voltage substation components to downstream low -voltage power distribution systems, most core electrical infrastructure is similar to traditional data centers.Some electrical components (including main electric transformers and gas circuit breakers) have a long delivery time. Miners who purchase these assets have a competitive advantage than new entryrs facing 3-4 years of purchasing time.

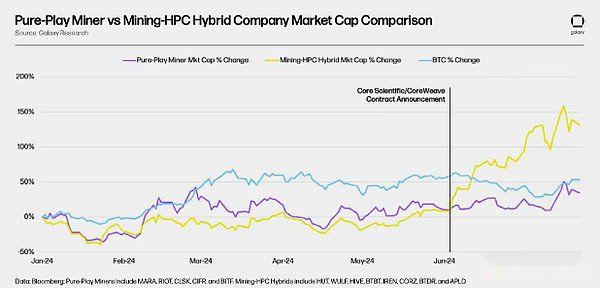

Miners have the land and power infrastructure required to build the next generation of the world’s largest data centers.Data center developers and large -scale enterprises may start bidding these parks to ensure that large -scale electricity is quickly obtained.This trend has just begun, and Coreweave acquired Core Scientific for $ 1 billion is obviously a pioneer.With the increasingly saturated traditional data center market and hosting provider, large -scale enterprises will be forced to break through the boundaries and further enter the second and third -level markets developed by brown and green land.

Miners began to get involved in AI/HPC in 2023, but the 200 MW custody transaction reached by Coreweave and Core Scientific in June 2024 made the industry catering by the industry.Before the AI boom, the value of these “giant sites” owned by large miners was purely in its Bitcoin mining potential.However, the impact of the Coreweave transaction on the stock price of Core Scientific proves that miners can benefit from AI advantages.The figure below shows that compared with the miners who are still focusing on pure mining strategies, those miners who have adopted measures to adopt measures to adopt mixed mining/AI methods have benefited a lot.

The reason why this advantage is because as of now, the economic benefits of the AI/HPC contract are very good.If it is attributed to the number of US dollars/MWS time (“$/mWh”), the power of the latest generation of Bitcoin mining machine is about $ 125/MWh (S21, the hash price is $ 0.053/day/day/day/day), And fluctuate with the change of the price of hash.Assuming that the cost of electricity is $ 40/MWh, the gross profit of each MWh is 85 US dollars/MWh.In contrast, as part of the Core Scientific/Coreweave transaction, Coreweave is willing to pay a fixed 118 US $ 118/MWh time, and 280 MW (graphic processing unit (“GPU”)+ IT and mechanical cooling infrastructure).The cost allows Core Scientific to provide custody services, even after paying most of the capital expenditure investment.

If the market continues to reward miners who pursue the opportunity of AI/HPC, we believe that the number of pure Bitcoin miners with large sites in the future will decrease, especially when the price of hash is kept at a low level.

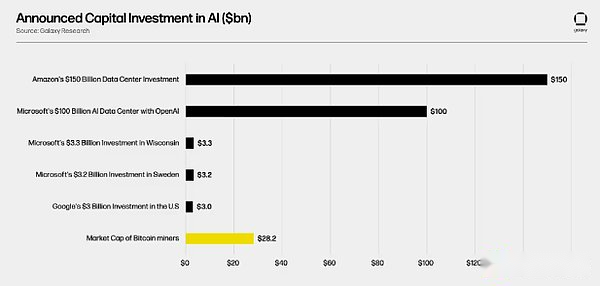

As of July 22, the total market value of the company (pure business + hybrid business) in the figure above was US $ 28.2 billion.When you compare this number with the capital that poured into AI (as shown in the figure below), it is difficult to imagine that the inhabitant miners in the future will not turn to a mixed method.With the growth of computing demand, oversized companies such as Amazon, Microsoft (the door of the interstellar, Wisconsin, Sweden), and Google have announced a plan for large -scale growth in the AI field in the next few years.

Some bitcoin miners have benefited from AI.However, unless the miners prove that they can build and operate these data centers on a large scale, they will continue to trade at the price below the price center provider.

Some bitcoin miners have benefited from AI.However, unless the miners prove that they can build and operate these data centers on a large scale, they will continue to trade at the price below the price center provider.

M & A

Throughout 2024, Bitcoin miners participated in a large number of mergers and acquisitions transactions.As our previous reports predicted, the trend of mergers and acquisitions has been consistent.Miners are increasingly enhanced their input control through the acquisition site, thereby achieving vertical integration.So far, the transaction volume of various transactions has exceeded US $ 460 million, mainly divided into site sales, reverse mergers and company acquisitions.The record low -hash price and steep ASIC efficiency curve forced miners to use more strategic methods to achieve higher excellent operations.Some of the motivations observed in 2024 include:

-

Vertical integration: The era of light assets is disappearing.In the past, the mining union custody its entire mining machine group at a fixed electricity price sacrificed the flexibility of optimizing operations to improve cost efficiency.With the halve -halked price of the halves hit a record low, this forces miners to achieve vertical integration than ever before, enabling them to manage the bleak hash price status and declining mining of mining through economic reduction or reducing operating expenses.economy.In 2024, the power access of more than 1.1 GW was easy, indicating that the control of the miners’ control of its operation is increasing.Public miners invested about $ 404,000 per MWs for power access, covering the current and future needs.

-

Business integration: The public mining industry has already appeared worthy of attention, highlighting the reverse merger, because many mining business used to be maintained by traditional fixed interest rate agreements, but these agreements are no longer economically feasible, which will cause triggers, which will cause triggersExtensive integration.

-

Diversification: 2024 is a year when it seeks synergy through diversification. Whether it is geographical expansion to emerging markets with low energy costs, or diversifying the source of income sources outside of mining.For example, BitDeer’s acquisition of ASIC Design Desiweminer reflects this strategy. By acquiring internal expertise, it promotes the launch of its exclusive ASIC, so that they can get another source of income outside Bitcoin mining.

Future mergers and acquisitions

For miners who have not upgraded the efficiency of miners or unable to adjust the cost after halving, we may see the erosion of liquidity and exhaust their capital reserves because they seek to withdraw or wait for the buyers to use their dilemma.If the price of hash has been maintained below 0.06 US dollars/ TH for a long time, we may see that the number of dilemma products increases, just like the situation at the end of 2022.In this hash price level, there is almost no profit margin except for electricity prices, let alone considering related operating costs, depreciation and any unpaid interest.For example, at the current price level of hash, some of the most popular previous generations, especially Antminer S19J Pro, generated about $ 70/MWh time.When solving the bottom line of the miner, calculated at the average electricity price of $ 60/MWh, and almost no room for considering all other related costs.

Although the financial situation of some miners is unstable, miners with power assets may become attractive acquisition targets.The demand for electricity in high -performance computing has continued to increase.For example, large -scale enterprises are facing a shortage of power capacity relative to their service needs, and they are willing to pay a lot of premium for this.Earlier this year, Amazon AWS purchased a capacity at a price of $ 677,000 per MW, which is much higher than the average mining transaction cost per MW of 2024.Asset -intensive miners have served as an agent for electricity, because the power grid interconnection schedule in the United States is still tight and the demand for AI is still strong.It is worth noting that large -scale enterprises are preparing to bid for how much power connections.

For smaller private miners, it is still a challenge to obtain affordable capital.Even if the debt market is reopened, the debt repay rate may still be insufficient.These miners may consider reverse mergers with a listed company to use the distribution in the market.

Evaluate attractive prospects

Factors affecting the company’s market value are constantly changing, and options are provided when they reduce the scope of the target attraction.This choice mainly comes from changes in the power market, premiums to listed companies based on its strategy, and opportunities to obtain capital.The goal of evaluating ideals may sometimes look like a cat -catching mouse game, trying to understand market value and foresee the wave of demand.Here are some features that may be attractive that the goals may be attractive:

-

The capacity available at any time: Those miners who not only have existing power capacity, but also have a healthy and clear -and -pass circuit may become attractive goals; “verbal commitment” will not work.The situation is the case for small miners who cannot reach scale and cannot upgrade their equipment or operate a meager profit, but they have valuable power assets that can achieve higher profits by deploying more efficient machines or turning to AI/HPC.

-

Predictable income stipulated in the contract: the letter of intent (“LOI”) and the list of terms do not emphasize stability.Miners who sign contract income within a certain period of time can obtain continuous cash.In view of the speculative nature of the mining economy, miners will be essentially affected by the fluctuations of hash prices, so the source of diversified income is wise.

-

Last generation of miners: When considering ASIC price speculation, many miners with lower efficiency of miners can sell their ASICs with discount prices below some of the peers with more efficient mining machines.This can make the price of $/Th, and provide a good price entry point for the return on investment of these auxiliary machines.The price of some previous -generation mining machines (30 J/TH) is very attractive, whether you want to mine (low cost) or speculation for sale.Although this may not be appreciated in the context of achieving high multiples, it can quickly get returns while maintaining the options of future mining machine upgrades.

In essence, some miners can become valuable goals to quickly obtain scalable electricity.Especially the miners with large interconnected protocols, power infrastructure growth channels and sufficient space.With these trilogy can increase the US dollar/MW premium that can be obtained by selling such capacity.As the demand for computing power continues to grow, we are glad to see how this will affect the valuation of miners and its attractiveness as the investment prospect.

Computing power forecast

In our annual report, we estimate that the range of computing power at the end of 2024 is 675 EH to 725 EH.We now increase the growth of 725 EH to 775 EH.In order to obtain the revised estimation value, we have studied some of the listed mining companies and its computing power goals to understand the reasonable possibilities we know, that is, the number of miners launched this year, and inferring the rest of the network.We also analyze the seasonality of historical computing power as an additional benchmark.In order to complete the analysis, we analyzed the balance point of the network profit and loss to verify the scope.

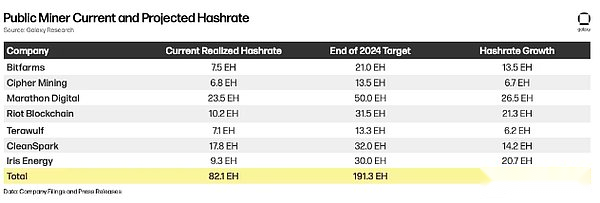

First of all, we will study the computing power growth situation of listed mining companies in the second half of 2024.In the first half of 2024, with the help of soaring valuation and raising huge funds in the stock market, listed mining companies made large -scale procurement orders on the new generation of machines.The table below summarizes the computing power figures achieved in June, the targets at the end of 2024, and some listed mining companies’ implicit computing power growth in the second half of 2024.In general, assuming that each miner has achieved established goals, these listed mine companies are expected to stimulate an incremental computing power of 109 EH, which means that only 7 miners can bring about 18% of the growth of network computing power.

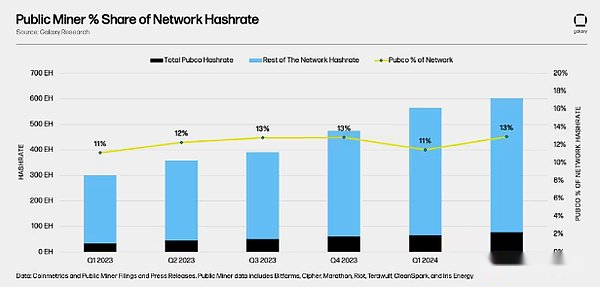

Next, in order to estimate the growth of the rest of the network, we analyzed the trend of the computing power of this part of the listed mining companies relative to the rest of the network.As shown below, from a historical point of view, this part of listed mine companies account for 11%-13%of the network.

Next, in order to estimate the growth of the rest of the network, we analyzed the trend of the computing power of this part of the listed mining companies relative to the rest of the network.As shown below, from a historical point of view, this part of listed mine companies account for 11%-13%of the network.

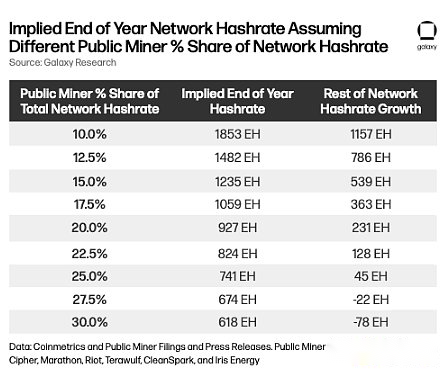

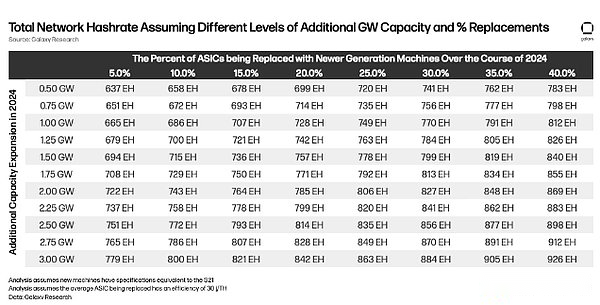

An excessive simplified method is to divide 109 EH with 13%, and get the rest of the other part of the extraordinary 838 EH.However, this is assuming that listed mine companies will continue to maintain a network ratio of 11-13%.The following scenario table shows that if we change the share of the listed mine companies at the end of the year, and assume that the current network computing power is 587 EH, the computing power of listed mine companies increases by 109 EH, and the current share of the listed mine companies in the network computing powerIt is 13%, so what will be the computing power at the end of the year.

We estimate that the share of listed mine companies in the network will increase to nearly 15%-30%, with a benchmark of 25%.This is because listed mine companies can enter the US capital market and can raise a lot of funds in the first quarter of 2024. Compared with private miners, this is a huge advantage.Based on the 25% share of the computing power at the end of the year, this means that the total network computing power is 741 EH, which means that the rest of the network will increase by 45 EH in the second half of 2024.

Therefore, from the perspective of listed mining companies, this defines our computing power growth benchmark to 741 EH.We predict that a considerable number of additional computing power will be put into use in the second half of this year. We believe that it is feasible to use the replacement machine and net new production capacity.Looking back at our analysis in the previous annual report, the sensitivity table below shows how much network computing will reach under different combinations of changing network percentage and additional GW production capacity expansion.From the network computing power of 587 EH, assuming that the new machine inserted is 17.5 J/Th, and the efficiency of the replaced machine is 30 J/Th.

We assume that the S21 has been deployed in the table above, but after 2024, the table emphasizes the impact of only the new generation of machine replacing the old generation machine on the network computing power of the network.Coupled with the announcement of the new ASIC manufacturer, it shows that the efficiency of Bitcoin mining ASIC can reach 5 J/Th next year, which will bring another meaningful improvement to the network computing power in 2025.

The next part of our analysis observes the historical computing trend of the entire summer and the end of the year.As shown in the figure below, the computing power is usually stable in summer from July to September.This may be due to the increasing proportion of networks in Texas and the Middle East, and miners have to reduce the frequency due to high temperature.In addition, due to price fluctuations, avoiding four -peak (4CP), and participating demand response plans, Miners in Texas are restricted.

After the summer, as the normal operation time increases, the demand for frequency reduction, and the new machine insertion of miners, the network computing power has begun to soar.It is expected that listed mine companies will greatly increase composition power in the second half of the year. We expect similar dynamics this year. Summer network computing power will increase slightly, and then speed up at the end of the year.

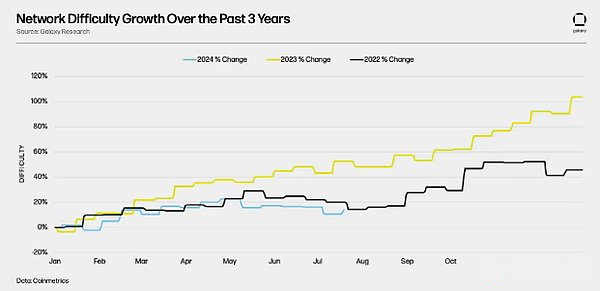

The network difficulty in 2024 is similar to the growth trajectory in 2022 and 2023.The difficulty of 2024 has changed synchronously with the difficulty of 2022.In 2022, from October to the end of the year, the difficulty increased by 14%from September to the end of the year.In 2023, from September to the end of the year, the difficulty increased by 29%.If we apply these growth rates to the current network computing power of 587 EH, it means that the range is 670 EH to 760 EH.Although the goals we have come from listed at this time are at the high -end of this scope, it allows us to be full of confidence in the perspective of infrastructure construction.

The final analysis is to understand the implicit hash price based on our target computing power to understand the economic sustainable price of the Internet.Several variables will affect this sensitive analysis, including Bitcoin prices, transaction fees, average network electricity prices and network efficiency levels.Taking into account the volatility of the transaction fee, we assume that they keep the fixed level of 10%(0.3125 BTC) of each block subsidy.

For the average network electricity price, we analyzed the decline in the recent computing power to understand the marginal unit of electricity prices.After halving, it was adjusted by 5.62%, and the computing power dropped to $ 0.052.Using Coinmetrics Mine-Watch, the estimated average network efficiency is 33.3 J/Th, which means that the average network electricity price is $ 65/MWh.

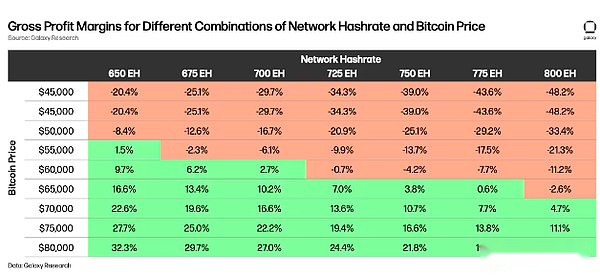

With the growth of network computing power, the machine combination will become more and more efficient.Therefore, we assume that the efficiency of networks will increase by 20%(J/Th is lower), and the efficiency will reach 26.6 J/Th.At these efficiency levels, if the electricity price remains unchanged at $ 65/MWhm time, the cost of the balance and loss of the network will be $ 0.041/Th.Although the price of hash has a quantitative income of each TH computing power, the cost of hash shows the total energy cost of each TH.If we consider Bitcoin’s price and network computing power, and assume that the transaction fee is fixed at 10%of the block subsidy, the figure below shows the average gross profit margin of the network.Assume that the price of Bitcoin remains within the range of $ 65,000 to 70,000, the network can still support the computing power of 741 EH, which further confirms that these levels are economically sustainable.

In short, according to the growth target information obtained from listed mine companies, the seasonal comparison of the previous years, and economic analysis, our preliminary computing power goal is 741 EH.Due to the uncertainty of machine deployment, we created a range from 725 EH to 775 EH near this number.We realize that many factors may lead to deviating this range.From a good perspective, the improvement of the mining economy and the release and deployment speed of machinery are faster than expected. These two factors may make us more than 775 EH.From a bad perspective, the huge deterioration of the hash rate or a large amount of capital from Bitcoin mining to AI/HPC may slow down.

in conclusion

In the first half of 2024, it was the decisive period of the Bitcoin mining industry. During this period, it faced major economic challenges and breakthrough development.Although the mining economy has reached a record low, in the face of the lowest hash price and high power demand in history, the industry has shown extraordinary toughness and adaptability.

The fusion of AI/HPC and Bitcoin mining means that many companies will make new attempts to change, because they try to use the strong and unrelated economic advantages of the industry.

As the demand of AI/HPC data centers and miners continues to increase, power supply is now obviously a bottleneck.therefore,Miners with a large amount of electricity supply are in a favorable position and can stand out.For these miners, it is essential to maintain flexibility in the future and to distribute MW capacity to the direction of maximizing shareholders.