Written by: Ryan Chen, Louis Wan (spinach)

This article was written by Ample FinTech and DigiFT

Author’s Preface:

Ryan Chen,

Head of Research and Innovation, DigiFT

At the end of 2023, we wrote a research report on real-world assets (RWA).At that time, the main market participants were still Web3 Aboriginals and the institutional participation was low.However, 2024 marked a turning point, with top global institutions such as Blackstone, UBS and Franklin Templeton entering the market.As industry practitioners, we have witnessed first-hand the intensification of competition and the beginning of two different forces converging.

This phenomenon reflects the gradual convergence of Web2 and Web3, and the exchange of data, capital and human resources is increasingly diversified and frequent.With the continuous evolution of the crypto market regulatory environment and returning to the core principles of finance, we believe that RWA will become a key direction for future development.Through faster settlement systems, more transparent markets and collaborative databases, blockchain technology will eventually become mainstream, improving the efficiency of the capital market and bringing tangible value to the real world.

Louis Wan (spinach)

Head of Research, Ample Fintech

Innovations in technologies such as distributed ledger technology (DLT) and tokenization are significantly improving the efficiency of today’s financial systems.These advances not only promise to simplify transaction processes, but will also lead to new forms of financial interaction that are more transparent, inclusive and secure.By reducing reliance on intermediaries, speeding settlement times, and embedding compliance measures through programmability, these technologies demonstrate the potential to reshape the foundations of the financial industry.

Today, we have witnessed an unprecedented level of public-private cooperation.Obviously, the driving force behind the tokenization of real-world assets (RWA) is no longer just the Web3 industry players, but the joint efforts of governments, central banks, financial institutions and international organizations.Ample FinTech has the honor to cooperate with several central banks to explore the realistic application of tokenized currencies.Ample FinTech will continue to explore practical solutions based on digital currency and smart contract applications, aiming to bring the inclusive value of programmable payments and finance to more people.

Executive Summary

-

In recent months, the tokenization field has surpassed the Proof of Concept (PoC) and entered the commercialization stage, with leading financial institutions playing a leading role.

-

Although regulation of the global tokenization market remains unclear, major financial centers are developing a more comprehensive framework, and efforts tokenization have become more welcome in some places.

-

This year, financial institutions like Blackstone, UBS and Franklin Templeton launched tokenization projects on public chains, competing with Web3 native initiatives.

-

Market opportunities, infrastructure maturity and licensing of innovative startups are key drivers of institutions’ adoption of public blockchains.

-

Private sector financial institutions are leading the way in asset tokenization, while there is an increasing coordination between the private and public sectors in monetary tokenization.

-

As demand for cross-border payments increases, the global economy is aware of the inefficiency of existing cross-border payment systems.High costs, low speeds and lack of transparency are increasingly becoming challenges that need to be solved.The G20 has developed a cross-border payment roadmap to improve the efficiency, transparency and accessibility of payment systems.Monetary tokenization has become one of the key ways to improve payment efficiency and cost.

-

Tokenization of currency not only brings cost reduction and efficiency improvement to the payment system, but also achieves programmability and automation through smart contracts.This technology can provide more innovative, transparent and speedy solutions to complex financial transactions, and the global public sector is carrying out related projects at a large scale.Introduction: Beyond Speculation

Finance is built on trust, including trust in infrastructure, trust in companies, and trust in people.The emergence of cryptocurrency and blockchain technology aims to build a more efficient and transparent financial world with globally trusted ledgers as infrastructure.If you look back at the initial design of Bitcoin, the goal is to build a peer-to-peer payment system.And Ethereum’s goal is to become a smart contract platform for decentralized applications.

Bitcoin[1]:

• Focus on creating a decentralized digital currency for secure, low-cost peer-to-peer transactions.

• Designed to remove financial intermediaries, promote financial inclusion, and build a financial system that requires no trust.

Ethereum[2]:

• Extend blockchain applications to smart contracts and decentralized applications.

• Aim to innovate financial systems through programmable currency, asset tokenization and decentralized finance (DeFi) to enable automated, transparent and secure financial transactions and services.

Both Bitcoin and Ethereum use blockchain technology to improve traditional financial systems and promote decentralization, transparency and efficiency.

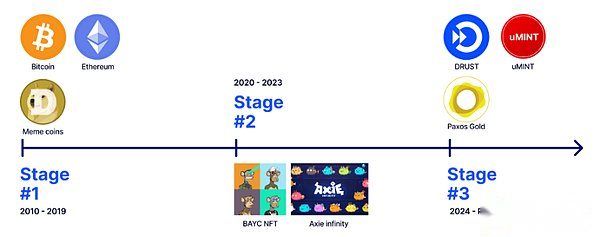

In the past few years, the native cryptocurrency market has grown rapidly and has experienced a variety of concept cycles such as ICO, DeFi, NFT and GameFi.The main innovations are concentrated on asset issuance and trading models, but they have little impact on the real world.With the development of the market, relying solely on crypto-native assets obviously cannot meet the needs of investors.In addition, the advantages of new financial technology allow innovators to further explore various application scenarios.We can clearly divide this technology-driven digital assets into three stages: • Phase 1, Crypto-Native Assets, 2010 ~ 2019:

For example, DeFi tokens, meme coins and native tokens for blockchain.These assets are essentially issued and traded on public blockchains, enjoying all the pros and cons of blockchain technology.

• Phase 2, Digital Native Assets, 2020 ~ 2023:

For example, NFT and GameFi tokens.These assets are connected to digital services or applications.

• Stage 3, Digital Twins, 2024 ~ Now:

Refers to real-world assets, asset interests expressed by ledger entries on the blockchain, such as gold tokens and U.S. Treasury tokens.At this stage, tokens are data entries on public blockchain-driven ledgers that are connected to off-chain entities or assets to enable faster settlements, real-time transparency and process automation on ledgers.

During the first two stages, Web3 is more like a casino, with hot money pouring into the market, causing big fluctuations in prices like meme coins.Web3 adoption needs to go beyond casinos, and it is important to distinguish between “cryptocurrency” and “blockchain technology”.As we enter the third phase, the challenges we face mainly come from unclear legal and regulatory environments rather than technical issues that influence the real world’s transformation to the Web3 era.

There is significant room for improvement and innovation in traditional financial markets, which can be achieved through encryption and blockchain technologies.For example, according to estimates from the Bank for International Settlements (BIS) [3], participants in the U.S. Federal Reserve Fund Transfer System used an average of $630 billion in intraday liquidity per day between 2003 and 2020, with a peak of nearly $1 trillion.In the euro system, the average and peak daily liquidity intraday is US$443 billion and US$800 billion, respectively.Participants used an average of 15% of the daily payments or 2.8% of GDP to meet intraday liquidity needs in the nine jurisdictions in the sample and a 17-year time span.These huge numbers highlight the important role played by intraday liquidity in maintaining financial stability.The cost associated with providing this liquidity is approximately $600 million per year, mainly for meeting the needs of real-time payments, managing time mismatch, reducing settlement risks and complying with regulatory requirements.The reason for this arrangement is mainly due to the inefficiency of widely used clearing and settlement infrastructure, and simple transactions take several days to complete.

Blockchain-based clearing and settlement systems can shorten settlement time to T+0 [4] and even realize real-time settlement, thereby significantly reducing the demand for intraday liquidity and reducing settlement risks.

In 2024, we see more institutions participating in this field, not only proof of concept (PoC), but also moving towards a more commercialized direction.In terms of blockchain technology and tokenization adoption, there are two main areas: monetary tokenization and asset tokenization.In terms of asset tokenization, several important milestones occurred in 2024.Mainstream financial institutions have made significant progress in the field of public blockchain.From their perspective, they focus on blockchain technology as a new and innovative ledger for recording ownership and reconciliation.

In terms of monetary tokenization, we have not only seen the adoption of stablecoins in the crypto market, but also other meaningful application cases that are being explored, such as purposeful currencies and programmable currencies.

This report focuses on the exploration, adoption and application of blockchain technology by mainstream financial institutions, especially public blockchain and decentralized finance (DeFi), and is divided into two parts: asset tokenization and monetary tokenization.Most of the cases mentioned are in the initial stages, but we can clearly see how institutions differentiate between cryptocurrency and blockchain technologies, as well as emerging trends and application paths for these technologies.

Why choose to tokenize on permissionless blockchain In the rapidly developing digital technology environment, permissionless blockchain emerged as a revolutionary concept, challenging the traditional concept of centralized systems and for decentralized applicationsA new era paved the way.Licenseless blockchain is essentially a distributed ledger technology that allows anyone to participate in the network without the approval of central authorities.Bitcoin and Ethereum are the most well-known instances of permissionless blockchains, attracting the attention of global tech experts, investors and dreamers.

The key feature of defining permissionless blockchains is its open access and decentralized nature.These characteristics distinguish it from traditional centralized systems and participation in restricted licensed blockchains.

When we talk about permissionless blockchains, one might think of cryptocurrencies, which is an application case of permissionless blockchains, and also the decentralized finance (DeFi) applications.In essence, permissionless blockchain is an open shared database that we can use to achieve efficiency.Mainstream financial institutions have realized that cryptocurrencies can be settled atomically in a few minutes, and that this feature is likely to be applied to other assets expressed in token form as well.Some of the benefits we can achieve with these technologies include:

• Higher liquidity and faster settlement

o In traditional markets, standard T+2 or longer settlement cycles have been the norm, mainly due to the transfer of settlement risks between different counterparties.This settlement delay takes up capital and increases counterparty risk.

o To shorten settlement time, a good practice is to open an account with the counterparty at the same bank or custody agency.In this way, the asset transfer between you and the counterparty can be transferred on the books within the bank and can be settled almost immediately.But opening a bank account is not easy, especially for financial institutions.By contrast, blockchain-based systems can reduce transaction settlement time to T+0 or even a few seconds, almost instantaneous.

• Convenient and low threshold accessibility

o This open architecture is redefining accessibility, and traditional systems have been trying to achieve this goal.Anyone with a smartphone has access to the full suite of financial services on-chain, which is exactly what we are seeing promises.Millions of people who are excluded from traditional finance are finding new economic opportunities through financial services on public blockchains.Small businesses can get funding without going through endless cumbersome procedures.Individuals from all backgrounds can invest and earn meaningful returns without the need for a perfect credit score or a gorgeous suit.

• Automated and trustless operations

o An important advantage of permissionless blockchain is its decentralized structure.Unlike traditional systems where “power” and “control” are concentrated in the hands of a single entity, permissionless blockchains distribute decision-making power across the entire network.

o Therefore, it is difficult for any single entity to manipulate the system or paralyze it because there is no “central” weakness.This creates an environment without trust, and participants do not need to rely on the trust of central authorities.Instead, trust is reflected in the system itself, which is governed by transparent rules and cryptographic proofs.

o Smart contracts are a classic example of this trustless environment, a self-executing contract that writes the terms of the agreement directly into the code.These contracts automatically enforce the terms of the agreement, reducing the need for intermediaries and minimizing the potential possibility of disputes.

• Global open participation

o The open nature of permissionless blockchains enables these networks to operate 24/7, allowing cross-border transactions without being restricted by traditional bank hours or international transfer restrictions.This global accessibility has the potential to revolutionize remittances and cross-border payments, making it faster and more cost-effective.

o For unbanked and underserved financial services worldwide, these systems provide a way to participate in the global economy without access to traditional banking infrastructure.All that is needed is an internet connection and a device capable of running wallet applications.

• Transparency and real-time monitoring

o Every transaction on the network is recorded on a public ledger visible to all participants.Compared with traditional financial systems, transaction records are not easy to obtain, and this kind of transaction transparency is far greater than that of traditional systems.This public nature increases trust among users, as anyone can verify the overall state of the transaction and the network.At the same time, access to transaction data is granted to different counterparties in real time for monitoring and automation.

Licenseless blockchain technology has broad prospects, but like any emerging innovation, it faces some restrictions and obstacles to overcome.With the development of the decentralized finance (DeFi) platform and the follow-up of traditional financial institutions, we have witnessed a dynamic financial ecosystem full of potential and challenges.Understanding these challenges is critical to risk mitigation and the full potential of permissionless blockchains:

• Security and privacy issues

o Unlicensed blockchains may face certain risks.For example, security risks like 51% attacks (in systems that use proof of work and proof of stake consensus mechanisms).

o If smart contracts are not properly audited and tested, security risks may also be introduced.

o Transparency is a double-edged sword when it comes to privacy.All transactions on public blockchains are visible to everyone, which can cause problems for individuals and businesses that need to be kept confidential.

• Regulatory uncertainty

o The decentralized nature of permissionless blockchains requires joint supervision between different jurisdictions, which presents significant challenges to regulators.Many governments are still working to determine how to classify and regulate cryptocurrencies and blockchain-based assets.We will dig into more details about regulation in the next section.

o The existence of crypto regulations is intended to create stability, protect investors and prevent illegal activities such as money laundering or fraud.As the crypto market is highly volatile and mostly decentralized, regulations help reduce investor risks and ensure exchanges and other crypto businesses operate transparently and impartially.

o In addition, regulations aim to integrate cryptocurrencies into existing financial systems while maintaining regulation, reducing opportunities for abuse, and promoting wider adoption by enhancing the trust of the system.The ever-changing nature of crypto regulations makes it difficult to predict because each country and region has different views on cryptocurrencies.

• Market volatility

o Cryptocurrencies are often native assets of permissionless blockchains, known for their extreme price fluctuations, and even Bitcoin with the largest market capitalization can fluctuate by 20% in a day.Tokenized assets coexisting with volatile cryptocurrencies may pass risks to mainstream financial systems, raising concerns from the SEC.For example, a large trader can use Treasury tokens as collateral, but he may need to liquidate due to severe market fluctuations.This may lead to the sell-off of underlying assets in mainstream financial markets.

• Complex user experience

o Despite the potential benefits, interaction with permissionless blockchains is still difficult for many users.The process of setting up a wallet, managing private keys, and interacting with decentralized applications can be a challenge for non-technical users.

o The irreversibility of blockchain transactions means that the cost of user errors can be high.Sending funds to the wrong address or losing access to the wallet can result in permanent loss of assets.This high-risk environment may put pressure on users and hinder adoption by the public.

• Lack of accountability mechanisms

o Licenseless blockchain presents significant challenges to anti-money laundering (AML) and understanding your customer (KYC) compliance, which are the cornerstones of financial regulation.Unlike intermediaries acting as doormen in TradFi, these open networks allow anyone to conduct transactions without prior approval or identity verification.This anonymity, while attractive to privacy advocates, also creates an environment that may breed illegal activities.The lack of centralized regulation makes it difficult to track money flows or identify parties in suspicious transactions, complicating efforts to combat financial crime.

o The rise of decentralized finance (DeFi) on permissionless blockchains has further exacerbated these concerns.The DeFi platform provides financial services, but does not have the safeguards that are usually present in TradFi, such as identity checking or transaction monitoring.Although this provides financial access to underserved people, it also creates opportunities for criminals to use the system.For example, money launderers can use complex DeFi transaction chains to mask the source of funds, making it difficult for law enforcement agencies to track money flows.As regulators work hard to solve these problems, balancing innovation and security remains a key challenge amid the continuous evolution of blockchain technology.

• Difficulty in upgrading

o Upgrading the licenseless blockchain protocol is a complex and risky process.Unlike centralized systems that can unilaterally implement upgrades, changes to blockchain protocols require consensus among diverse and decentralized participants.

o Difficulties in implementing upgrades can lead to technological stagnation, known issues or limitations not being resolved because the community cannot reach a consensus on how to resolve them.This also makes it difficult to quickly respond to newly discovered vulnerabilities or changing technology environments.Licenseless blockchain represents a breakthrough technology that has the potential to improve our digital lives and revolutionize the future world of investment.Their advantages offer huge benefits compared to traditional centralized systems.Their innovative potential unlocked in areas such as decentralized finance and new economic models is exciting.However, these systems also face significant challenges and risks, which pose substantial barriers to large-scale adoption.

Ultimately, the future of permissionless blockchains may undergo a process of evolution and improvement.Although they may not completely replace traditional systems in the near term, they have proven their potential to supplement and enhance existing financial and technological infrastructure.

As technology matures and solutions to current challenges emerge, we can expect permissionless blockchain technology to achieve wider integration in all areas of the economy and society.

This integration takes time and requires careful consideration of the trade-offs between decentralization, efficiency, security, and user experience.When comparing decentralized finance with traditional finance, it is important to consider the evolution of traditional finance.The Internet or online banking is not achieved overnight. The online brokerage and trading platforms we know today have evolved over the years and experienced many regulatory issues.Large banks or participants entering the market early on grew up with the evolution of traditional finance and eventually succeeded in the financial industry.This mentality is also applicable to decentralized finance and its blockchain integration with traditional financial ecosystems to achieve widespread adoption of decentralized finance.

Changes in legal and regulatory trends – Regulatory frameworks for each jurisdiction

The global legal environment around tokenization of reality assets (RWA) is fragmented.The legal system needs to establish clear standards to classify tokens bound by securities laws.Tokens can replace traditional securities, in which case the rules of the securities law need to be adjusted and applied.Extending the securities law to tokens that are not part of securities can lead to adverse outcomes and inhibit economic and/or technological innovation.Some jurisdictions adopt a traditional approach to distinguish between secure tokens and cryptocurrencies under existing securities laws.

With the rapid development of decentralized finance (DeFi) and tokenization, global regulators are constantly improving the legal framework for digital assets and related financial activities.This trend not only reflects the growing demand of market participants, but also shows the government’s emphasis on maintaining financial stability and protecting investor rights.With the prosperity of the cryptocurrency market and the application of tokenization technology, different regulators have different considerations and requirements for cryptocurrency-based cryptocurrencies and tokenization technology.We will focus on some of the major jurisdictions and their stance on regulation, including the United States, Hong Kong, Singapore, the UAE, the British Virgin Islands and the European Union.

USA

Regulatory Authority:The Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC) and the Financial Crime Enforcement Network (FinCEN).

Crypto regulation:

-

Security Tokens: regulated by the SEC under the U.S. Securities Act.If a token is classified as a securities under the Howway Test, it must comply with registration requirements, exemptions (e.g., D Regulations, S Regulations), disclosure obligations and standards of conduct.

-

Commodity tokens: such as Bitcoin (BTC) and Ethereum (ETH), are classified as commodities and are regulated by the CFTC.

-

Payment Tokens (cryptocurrency): If used in currency transfer services, it is subject to FinCEN’s Anti-Money Laundering/Counter-Terrorism Financing (AML/CFT) regulations.

Tokenization:

-

Tokenized securities:Deemed as a traditional securities, it must comply with all SEC regulations regarding issuance, trading and custody.

-

Digital Asset Custody Agency:Must register and comply with the SEC and CFTC regulations regarding the custody of digital assets.

Hongkong

Regulatory Authority:The Securities and Futures Commission (SFC) and the Hong Kong Monetary Authority (HKMA).

Crypto regulation:

-

SFC regulates cryptocurrencies that meet securities or futures contract qualifications under the Securities and Futures Ordinance (SFO).

-

Virtual Asset Trading Platform: License must be applied for under the Anti-Money Laundering and Counter-Terrorism Financing Ordinance (AMLO) and comply with the Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) requirements.

-

Regulatory Sandbox: Allows crypto platforms to operate under strict supervision to ensure they comply with regulatory standards.

Tokenization:

-

Safety Token: Deemed as a securities under the SFO, it is subject to the Securities Act, including the licensing requirements of the intermediary, the prospectus requirements and compliance with the provisions of the Code of Conduct.

-

Stablecoins: HKMA is developing a regulatory framework to treat stablecoins as deposit value facilities (SVFs), requiring licensing and prudent requirements similar to payment providers.

Singapore

Regulatory authority: Monetary Authority of Singapore (MAS).

Crypto regulation:

-

Payment Token: Also known as Digital Payment Token (DPT), regulated under the Payment Services Act (PSA).Crypto exchanges and wallet providers must obtain licenses and comply with anti-money laundering (AML) and anti-terrorism financing (CTF) requirements.

-

Safety Token: Regulated under the Securities and Futures Act (SFA) if qualified for securities or capital market products.Issuers must comply with prospectus requirements and obtain a license without the waiver.

Tokenization:

-

Practical Tokens: Generally not regulated under SFA, unless it is part of a specific category that triggers regulation.They must comply with AML/CFT and consumer protection laws.

-

MAS supports secure token issuance (STOs) and establishes a framework to facilitate the issuance of tokenized securities under SFA and provide guidance for regulated entities in STO.

UAE

Regulatory Authority:Dubai Financial Services Authority (DFSA), Abu Dhabi Global Markets (ADGM) Financial Services Authority (FSRA) and Securities and Commodity Authority (SCA).

Crypto regulation:

-

Security Token: Regulated under ADGM and DFSA’s financial market regulations.Issuers and intermediaries must obtain licenses, comply with codes of conduct, and comply with anti-money laundering (AML) and anti-terrorism financing (CTF) requirements.

-

Virtual Asset Service Providers (VASPs): Must be registered with each regulatory authority and comply with specific requirements (e.g. ADGM’s Virtual Asset Framework and DFSA’s Virtual Assets Regulations).

Tokenization:

-

FRANCE PENGED TONS (FRTs): Regulated according to the stablecoin and asset-backed token framework proposed by ADGM.These tokens must be completely backed by high-quality, liquid assets.

-

The UAE encourages secure token issuances (STOs) within the Financial Free Zone (ADGM and DIFC) and has established clear compliance, investor protection and issuance rules.

British Virgin Islands

Regulatory authority: BVI Financial Services Commission (BVI FSC)

Crypto regulation:

-

Security Tokens: Regulated under the BVI Securities and Investment Business Act 2010 (SIBA).Issuers and intermediaries must obtain licenses, comply with codes of conduct, and comply with anti-money laundering (AML) and anti-terrorism financing (CTF) requirements.

-

Virtual Asset Service Providers (VASPs): If the issuer meets the definition of VASPs, he or she must obtain a license under the VASPs Act.In addition, BVI FSC has issued guidance on registration applications for virtual asset service providers (“VASPs Registration Guidance”), as well as guidance on anti-money laundering, anti-terrorism financing and proliferation financing for virtual asset service providers.

Tokenization:

-

Security Tokens: Tokens that constitute securities or other financial instruments must comply with a variety of regulations, including (but not limited to) the VASPs Act, the Securities and Investment Business Act 2010 and the Financing and Monetary Services Act 2009.

EU

Regulatory Authority:European Securities and Markets Authority (ESMA), European Banking Authority (EBA) and national regulatory bodies.

Crypto regulation:

-

The EU has established the Crypto Asset Market Supervision Regulations (MiCA) to provide member states with a comprehensive cryptoasset regulatory framework.

-

Asset-linked tokens (ARTs) and electronic currency tokens (EMTs) must comply with requirements related to authorization, reserve management, capital adequacy and information disclosure obligations.

-

Crypto Asset Service Providers (CASPs): Licenses must be obtained and comply with anti-money laundering (AML)/Counter-Terrorism Financing (CTF) and Market Conduct Standards under MiCA.

Tokenization:

-

Security Token: If qualified for financial instruments, such as transferable securities, is regulated under the existing Financial Instruments Market Directive (MiFID II).

-

MiCA also involves practical tokens and provides clear guidance on their issuance and trading requirements, while practical tokens may not fall within the scope of traditional securities regulation.

Summarize

Each jurisdiction has its own unique approach in regulating cryptocurrencies and asset tokenization.Generally speaking:

-

Hong Kong and Singapore focus on a balanced approach, encouraging innovation while ensuring investor protection and market integrity.

-

The regulatory environment in the United States is more fragmented, with multiple institutions regulating different aspects of crypto assets.

-

The UAE provides a tailor-made regulatory framework within its financial free zones, promoting a regulated environment for digital assets and tokenization.

-

The British Virgin Islands have clear systems that rely on existing securities laws to manage security tokens and have VASPs Act to manage virtual asset services.

-

Through MiCA, the EU is moving towards a unified regulatory framework across member states, focusing on consumer protection, market integrity and financial stability.

Asset Tokenization: Institutions Enter Web3

Decentralized finance (DeFi) is quickly gaining attention because of its potential to revolutionize institutional financial services through blockchain technology and smart contracts.Proponents of DeFi envision a new financial paradigm with fast settlement, efficiency, composability, and open and transparent network characteristics.

Despite the optimistic outlook, DeFi has made cautious progress in the development of regulated financial activities, mainly attributed to the ever-changing macroeconomic and regulatory environment, as well as uncertainties in technological development.To date, most institutional DeFi initiatives are still in a proof-of-concept or sandbox environment.However, successful implementation is beginning to emerge, and the integration of DeFi with digital assets and tokenization is expected to accelerate in the next one to three years.

Financial institutions have been preparing for years and are aware of the change potential of DeFi.As the technological and regulatory framework matures, the integration of DeFi and institutional finance is expected to unleash new levels of efficiency, transparency and innovation.In this section, we will focus on securities, the main component of assets, to investigate how financial institutions are exploring this field.

From conception to reality: mainstream thinking on blockchain and tokenization

From an institutional perspective, tokenization is a form of data entry, which has certain advantages over traditional book entry forms, while blockchain is an account book that records ownership and facilitates transactions.

As blockchain technology and crypto industry continue to evolve, the term “real world asset” (RWA) has become increasingly common.RWA covers a wide range of things, from the tokenization of physical assets to mainstream financial instruments, and even assets related to environmental, social and governance (ESG) standards.In Web3, the first widely adopted real-world asset class is stablecoins, which we will discuss in the next section.Following closely behind are products related to Treasury bonds, as it is widely accepted as a safe asset and is more standardized.Over the past few months, we have seen rapid growth in on-chain U.S. Treasury and money market funds, with total value growing from about $100 million at the beginning of 2023 to $2.21 billion now.

Tokenization: Milestones for mainstream finance in 2024

Ethereum, Bitcoin and other public blockchains have built an open financial system that allows assets to be traded and flowed freely.This open system has brought numerous financial innovations, but due to its anonymity and open nature, it also poses major challenges to anti-money laundering (AML) and anti-terrorism financing (CFT) efforts.Mainstream financial institutions have invested a lot of time and effort in researching and exploring solutions and are gradually starting to find the best solutions.

To address the above, financial institutions have developed some best practices to enable regulators to allow such flow to occur more comfortably.Some examples include on-chain anti-money laundering screening, token whitelists and blacklist controls, etc.

These practices provide convenience for mainstream financial institutions to enter the DeFi field.2024 seems to be a turning point, with one of the important milestones being the launch of BUIDL tokens on Ethereum and followed by Franklin Templeton’s tokenization on multiple blockchains[6], andUBS issuing U.S. Treasury Fund in partnership with DigiFT[7].

Factors driving this progress include the efficiency of on-chain operations and market opportunities, all thanks to the emergence of compliant on-chain market participants.Securities, as an SEC-approved transfer agent, uses public blockchain as its infrastructure to register and record asset ownership on the blockchain.This allows Securitize to act as a distributor of Blackstone, promote the tokenization and distribution of assets on the Ethereum blockchain, embed Blackstone’s BUIDL tokens into the DeFi and Web3 fields.

Previously, Franklin Templeton also used blockchains such as Polygon and Stellar for records, but mainly relied on its traditional form of book entry, using public blockchains as secondary ledgers.However, Blackstone has made public blockchains its primary ledger, allowing tokens to be transferred directly on the chain and making ownership transfer valid.Shortly after Blackstone launched BUIDL, Franklin Templeton also released its token transfer feature, even supporting token transfers on other blockchains such as Solana, Avalanche, Aptos and Arbitrum to expand its customer base.

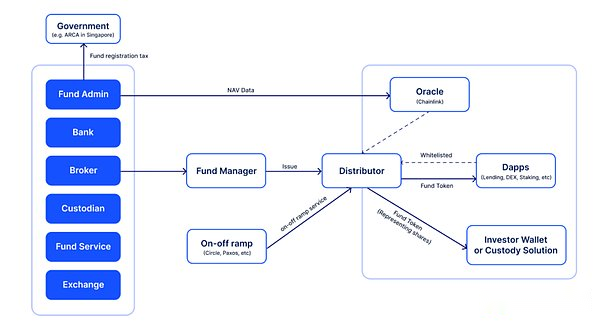

Tokenized structure

Although similar funds are already common in the Web2 market, there are still many challenges in implementing tokenization, as the operation of funds involves dozens of stakeholders and key processes as shown in the following figure

This process consists of three main components:

-

Fund Management:Fund managers will open accounts with institutions including banks, exchanges, brokers and custodians to invest and manage assets according to their strategies.

-

Fund Administrative Management:Involves tasks such as net asset value (NAV) calculation, accounting and bookkeeping, investor services, compliance reporting, expense management and audit support.

-

Fund Distribution:Distribution channels act as a bridge between investment funds and investors, providing the infrastructure for sales, marketing and delivery funds.In Web3, distribution channels will allocate funds to the Web3 ecosystem in token format.

In the tokenization process, fund distribution is the most directly related.However, in order to complete the distribution, activities such as KYC linking, anti-money laundering (AML) inspection, data updates, dividend payments and distribution are closely linked to other stages.

In the chart above, we can divide it into on-chain and off-chain sections.The processes on the right are all related to the chain, including:

On-chain Anti-Money Laundering and KYC

-

Link the customer’s wallet address to the off-chain KYC and add the address to the whitelist.

Ownership Record

-

The token represents the ownership of the fund and is guaranteed by a legal contract.In this way, transferring on the chain to another address has legal effect.

Token Contract Design

-

The token contract will be managed and controlled by the fund manager, and has functions such as role setting, forced transfer, token minting or destruction, whitelisting and blacklisting functions.

-

Distributors will be able to add or remove whitelists and mint or destroy fund tokens.

-

In the end, investors usually only have the right transfer token (transfer to another whitelist address or redemption contract).

On-chain data availability

-

This process usually involves an oracle publishing off-chain data (such as the NAV of the fund shares) to the chain.

As shown above, institutional asset tokenization involves multiple participants, requires the efforts of multiple parties, and is not simple and intuitive.Some institutions have streamlined the process and successfully launched their fund tokens in 2024.We see 2024 as a key turning point.

2024: Major milestones

Blackstone and Security launch BUIDL

Blackstone is the first company among major financial institutions to directly adopt fund tokenization, achieving this through its cooperation with Securities.

The fund, called BUIDL (BlackRock USD Institutional Digital Liquidity), is issued by Blackstone in the British Virgin Islands entity.The fund is a sub-fund invested in a parent fund managed by Blackstone Asset Management.Securitize serves as a tokenization platform, transfer agent and sole distributor of the fund as an SEC-approved transfer agent.

As a representative of fund shares, fund tokens can be transferred on-chain between whitelist addresses.With this transferability, Circle, the issuer of stablecoin USDC, added real-time redemption smart contracts to BUIDL, providing US$100 million in USDC liquidity.Investors can transfer BUIDL tokens into smart contracts and obtain USDC liquidity after confirming transactions on the Ethereum blockchain.This feature demonstrates the advantages of fast and efficient settlement of public blockchain technology.

To invest in the fund, the investor must be a qualified buyer (QP) with a minimum investment of $5 million.The fund adopts a distribution share category structure, each BUIDL fund share token is always equal to USD1 and distributes monthly income in the form of a BUIDL token airdrop.

Franklin Templeton launches FOBXX on multi-chain

It is generally believed that transfers on public blockchains have legal effect.However, this is not the case.In some legal domains, the law requires coordination of the general provisions for the transmission of intangible assets with the actual operation of blockchain technology.This will be achieved by integrating on-chain transfers into universally applicable rules.For Franklin Templeton, his fund tokenization program went through this process.

Franklin Templeton tokenized its U.S. Treasury Fund on the Polygon and Stella blockchains in 2021, using a tokenization platform Benji, which provides wallet and custody solutions for retail customers.The fund is open to U.S. retail investors.

Initially, Franklin Templeton’s Benji token could not be transferred directly on the chain.Benji only uses blockchains like Polygon and Stella as auxiliary ledgers and still relies on its own centralized system.

Shortly after Blackstone launched BUIDL, they turned on local on-chain transfers and supported other blockchains such as Ethereum, Arbitrum, Aptos and Avalanche C chains.

UBS cooperates with DigiFT to distribute tokenized funds

The project was originally a pilot project of the Monetary Authority of Singapore (MAS) “Project Guardian”.In this project, UBS has established internal capabilities to tokenize on public blockchains.Recently, UBS has established a partnership with DigiFT and another distributor (SBI) for token distribution, a DeFi distributor of US dollar money market fund tokens.

The fund token represents a share of Variable Capital Corporation (VCC), a widely used fund structure in Singapore known for its flexibility.

The partnership with DigiFT enables UBS’s money market fund tokens to attract a wider range of customers in Web2 and Web3. DigiFT’s trading smart contract provides real-time redemption capabilities, which all DigiFT users can provide liquidity to meet real-time redemption.and achieve seamless interaction with the DeFi ecosystem.

DTCC collaborates with Chainlink to launch a smart NAV pilot

DTCC and Chainlink announced the successful completion of the smart NAV pilot in 2024 [9].The program aims to tokenize mutual funds and use Chainlink’s blockchain technology to automate the distribution of NAV data.NAV is the daily valuation of mutual fund assets, and traditionally the process of distributing NAV data is manual, error-prone and slow.The Smart NAV pilot changed this situation by using Chainlink’s CCIP to deliver on-chain NAV data on public and private blockchains.

The pilot also involved key industry players such as JPMorgan Chase, BNY Merrill Lynch and Franklin Templeton, who tested how blockchain-based automation can improve transparency and efficiency in financial operations.

The main achievements of the pilot include:

-

Interoperability:Chainlink’s CCIP ensures that NAV data can be distributed seamlessly between different blockchain networks, avoiding data silos and improving access and scalability.This cross-chain capability is crucial to the future of tokenization because it allows traditional financial markets to interact securely with decentralized platforms.

-

Real-time data access:By putting NAV data on the chain, financial institutions have obtained real-time pricing information, improving market efficiency.This not only speeds up decision making, but also paves the way for mutual funds tokenization, making them easier to trade and manage.

-

Improved operational efficiency:The pilot automates multiple aspects of NAV data distribution, reducing manual errors and operational costs.Being able to deliver historical data on-chain also enhances transparency and record keeping, which is crucial.

Chainlink’s collaboration with DTCC represents a forward-looking mindset that aims to combine blockchain technology with traditional finance.By automating the transmission of key financial indicators such as NAV data, this collaboration demonstrates the potential for greater efficiency, transparency and innovation in financial markets.With the participation of major financial players such as JPMorgan Chase, BNY Merrill Lynch and Franklin Templeton, the Smart NAV pilot clearly demonstrates the growing interest of institutions in blockchain-based solutions.

After tokenization – what application scenarios are there?

Why do these mainstream financial institutions focus on tokenization?If tokens are issued on public blockchains only for recording and maintenance of asset ownership, then efficiency will not be improved.One of the direct benefits is entering a new market that increases their asset management scale (AUM).The narrative of institutional DeFi is also an exploration area, where there will be more use cases of tokenized assets that can truly solve some pain points in the traditional financial system.

Institutional DeFi takes time not only to solve business and technical issues, but also to solve legal and compliance issues.Those who acted quickly were DeFi participants.Beyond tokenization, DeFi participants add more use cases tokens issued by these institutions.

Real-time settlement capability

Real-time settlement is an ideal scenario for the capital market. If settlement can be completed in an atomic transaction, then we can reduce the settlement risk to almost zero.But in mainstream systems, only a small number can achieve this.The obstacle lies in the clearing, settlement and reconciliation processes between different trading parties.These processes take time because each participant has its own ledger and lacks trust between each other.

But in public open ledgers, real-time settlement is possible.Following the launch of Blackstone BUIDL, Circle established a real-time redemption contract for any BUIDL holder, providing US$100 million in liquidity for instant redemption [10].They will manage the received BUIDL tokens and replenish the mobile pool if needed.

DigiFT establishes an internal real-time redemption contract for asset token holders, allowing them to instantly obtain USDC liquidity, while in the background, smart contracts trigger normal redemptions to supplement the liquidity pool.

Stablecoin reserve assets

Compared with highly volatile cryptocurrencies, securities tokens such as Treasury Fund Tokens and Money Market Fund Tokens are more suitable as reserve assets for fiat currency reference stablecoins.

Sky (former MakerDAO) is the first decentralized stablecoin to adopt off-chain assets, now using tokenized assets as its stablecoin reserve [11]. Recently, they launched the RWA Grand Prix, which plans to allocate US$1 billionGive RWA tokens [12], UBS, Blackstone, Franklin Templeton and other companies to compete for this $1 billion allocation.

Other examples include the stablecoin USDm of Mountain Protocol and the stablecoin UStb of Ethena[13].

Asset packaging and division

In the financial supply chain, distributors act as channels to lower the entry barriers for specific assets and improve efficiency.One distributor case in Web3 is Ondo Finance, which is the distribution channel of Blackstone BUIDL, with a total locked position value of more than US$200 million.

Ondo packages BUIDL into a fund token called OUSG, allowing access by professional U.S. investors.Unlike BUIDLs that require a minimum subscription of $5 million, OUSG accepts a minimum of $5,000 and enables real-time USDC subscriptions and redemptions, in which case Ondo helps BUIDL broaden its audience.

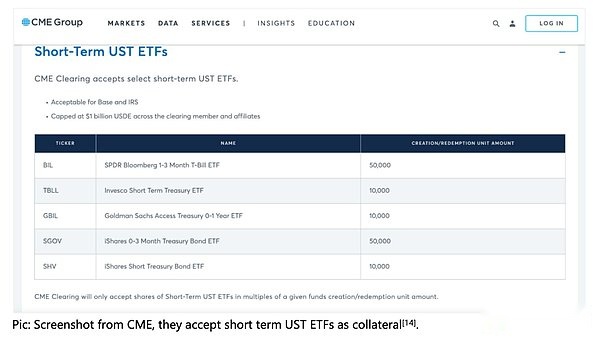

Margin mortgage

In mainstream finance, safe and profitable assets, such as U.S. Treasury bonds and corporate debt, are often used as high-liquid collateral for margin trading and derivatives trading.

Take CME as an example, which accepts a variety of assets as collateral, including bonds, funds and other securities.

Currently, using short-term US Treasury Fund Tokens or Money Market Fund Tokens as margin, rather than using stablecoins or cash, can offset the capital cost of margin trading.

In 2023, Binance partnered with some crypto-enabled banks to provide U.S. Treasury bonds as collateral for its institutional clients [15], but the entire system is still based on traditional trading venues such as Sygnum Bank.

In Web3, institutions and cryptocurrency exchanges are more familiar with tokenized assets, and with the emergence of highly liquid and secure assets such as BUIDL, they are beginning to use tokenized assets as collateral for certain transaction purposes.Due to the liquidity of instant redemption, the liquidation process will not become an obstacle.

Brokers like FalconX[16] and Hidden Road Partners[17] are already developing such use cases to attract institutional investors.

Asset Tokenization – What’s the next step?

As we move into 2024 and beyond, asset tokenization is expected to revolutionize the financial landscape by releasing unprecedented liquidity, efficiency and accessibility.We can clearly see some emerging future trends.

The native tokenized ecosystem of Web3 is gradually maturing.Traditional financial markets are already mature and participants are in different roles.In 2024, we see some startups drawing on business models and turning to Web3.For example, rating agencies (such as Particula) and accounting and auditing companies (such as Elven, The Network Firm).

In addition to U.S. Treasury bonds, Web3 investors have also developed interest in high-yield assets as U.S. interest rates begin to decline.These assets will compete with Web3 native earnings to attract investment.

Tokenization platforms and distribution channels are also focusing on traditionally under-liquid products, such as trade financing products and venture capital funds.In this process, markets with insufficient liquidity will also be democratized.

Compliance and licensing are also a major trend as we see Web3 companies obtaining licenses in such friendly jurisdictions as the UAE and the EU.With the emergence of compliance players in the ecosystem, mainstream institutions can also work with them to explore new market opportunities.

As institutions adapt to Web3 and blockchain infrastructure, on-chain liquidity and real-time settlement will also become realistic on a large scale, and the settlement process will gradually move to the chain.

Monetary tokenization

With the continuous digitalization of the global economy, the monetary system is at the forefront of another major change.From dematerialization to digitalization, and to today’s tokenization, the form and function of currency are undergoing profound evolution.In the past few years, we have seen how tokenization of real-world assets (RWA) can make asset management and financial services more efficient. Mainstream financial institutions such as BlackRock and Franklin Templeton are also actively exploring tokenization.Application scenarios.However, in addition to the tokenization of assets, the tokenization of currency has gradually become a major trend that has attracted much attention, demonstrating its huge potential to transform payment systems and financial markets.

Various pain points in the current payment system, such as high cross-border payment costs, slow settlement speeds, and the complexity of liquidity management, are driving the financial industry to seek more efficient and smarter solutions.The tokenization of currency is the core of this exploration. Through blockchain and smart contract technology, currency can achieve programmable, automated, and efficient and transparent payment and settlement.Digital currencies have introduced new efficiency and flexibility to the existing financial system, which can accelerate the flow of funds, increase transparency, and reduce dependence on intermediaries, thereby injecting new vitality into the global financial system.

New Horizons: Cooperation and Innovation of Digital Currencies

Discussions on digital currency and its application scenarios have attracted widespread attention in the early days of the rise of blockchain technology. With the rapid development of blockchain technology, the conception of digital currency has also become a hot topic in many financial technology forums and experiments.However, due to the immature understanding of blockchain technology and the way of digitizing currency in the past and the lack of corresponding legal and regulatory frameworks, many attempts have failed, which has gradually cooled down the heat of discussion in this field.

Since 2017, the industry has experienced many failed attempts and adjustments to the policy and regulatory environment, and discussions on the practical application of monetary digitalization and blockchain have gradually cooled down.However, the rise of the wave of decentralized finance (DeFi) has changed this situation.The development of DeFi has rekindled people’s interest in blockchain and tokenization. With the continuous improvement of blockchain infrastructure, discussions on digital currencies have once again heated up and entered a new stage of development.

In the past few years, many emerging technologies and standards have gradually matured. For example, cross-chain technology allows assets and data to flow seamlessly between different blockchain networks. Zero-knowledge proofs enhance the privacy and security of transactions, and new communicationsThe certification standards further improve the diversity of asset and currency tokenization.The gradual improvement of these infrastructures has paved the way for the practical application of digital currency and promoted further exploration of currency innovation and blockchain technology.

In 2020, G20 signed a roadmap on strengthening cross-border payments [18], recognizing the importance of efficient payment systems for global economic growth and financial inclusion.The core goal of this roadmap is to solve challenges in cross-border payments, improve payment speed and transparency, increase accessibility to cross-border payment services, and reduce their costs.The G20 plan has promoted the development of digital currencies, and the attention and support of major economies around the world also provide solid policy guarantees for innovation in this field.

Goals and Visions of the G20 Program

The goal of the G20 cross-border payment roadmap is to fundamentally improve the efficiency, transparency and accessibility of global payment systems, especially in the field of cross-border payments.The program aims to achieve the following key objectives [19]:

Costs

-

The global average remittance of $200 is no more than 3% by 2027

-

By 2030, the average global payment cost will not exceed 1%

Speed

-

By 2027, 75% of cross-border wholesale payments will be realized within 1 hour of initiation, and the rest will be completed within one working day; cross-border retail payments and remittances should also be completed within a similar time frame.

Access

-

By 2027, ensure that at least 90% of individuals have access to cross-border electronic remittances, and all end users have at least one option to send and receive cross-border payments.Financial institutions should also provide at least one cross-border wholesale payment option in each payment channel.

Transparency

-

Until 2027, all payment service providers (PSPs) are required to provide minimum information, including transaction costs, estimated arrival time, tracking of payment status, and terms of service.

Pain points of the current payment system

Despite the increasing importance of cross-border payments, existing payment systems face many pain points and challenges that seriously affect payment efficiency, cost and accessibility.According to the analysis of the Board of Payments and Market Infrastructure (CPMI), the main challenges faced by cross-border payment systems include [20]:

1. High cost:

Current cross-border payments involve multiple intermediaries, and each link will increase transaction costs.The high cost makes many small payments uneconomical, hindering the popularity of cross-border remittances.

2. Low speed:

Cross-border payments usually require a long transaction chain, and the clearing and settlement of multiple participants leads to a slow payment process, and batch processing and lack of real-time monitoring further extend the transaction time.

3. Limited transparency:

The lack of transparency in multiple links in the payment process makes it difficult for users to obtain detailed information about payment status and fees, which increases the uncertainty of payment and the cost of trust.

4. Accessibility is limited:

Users in many regions have difficulty accessing cross-border payment services, especially in developing countries, where financial institutions and payment services are insufficient, resulting in the widespread accessibility of cross-border payments.

5. Compliance and Complexity:

Cross-border payments involve complex compliance requirements such as anti-money laundering (AML) and anti-terrorism financing (CFT), and inconsistent regulatory provisions in different jurisdictions have put payment service providers in huge compliance challenges.

6. Traditional technology platform:

The existing payment infrastructure mostly relies on traditional technology platforms, lacking unified standards for real-time processing capabilities and data transmission, resulting in inefficiency of cross-border payments.

Application trends of distributed ledger technology (DLT) and digital currency

With the continuous evolution of cross-border payment technology, the application of distributed ledger technology (DLT) in digital currencies is becoming an important trend.DLT provides a reliable solution that can effectively address the challenges of current payment systems, especially with significant advantages in cross-border payments.Through DLT, payment systems can realize data sharing, transparency and real-time, which are all lacking in the current payment system.

The application of DLT has gradually made three main types of digital currencies a reality:Central Bank Digital Currency (CBDC),Tokenized bank depositsandStable Coin[twenty one]:

1. Central Bank Digital Currency (CBDC):

Digital currency issued by the central bank, CBDC aims to enhance financial inclusion by providing reliable digital payment tools while reducing reliance on cash.As one of the technical options to implement CBDC, the DLT-based CBDC architecture enables efficient and low-cost cross-border payments while ensuring compliance and security.CBDC is considered a liability on the balance sheet of the central bank, reflecting the central bank’s direct responsibility to the public and endorsed by the state’s credit, ensuring a high degree of stability and trust.

2. Tokenized Bank Deposits:

This is a digital representation of traditional bank deposits, using DLT technology to enable bank deposits to be traded and settled in the form of tokens.Tokenized bank deposits not only improve payment efficiency, but also realize real-time liquidation between banks, reducing the cost of capital use.Tokenized bank deposits are liabilities on the balance sheet of commercial banks. Similar to traditional bank deposits, commercial banks are responsible for repaying depositors. Their value is based on the credit of commercial banks and is influenced by the bank’s liquidity and regulatory framework.

3. Stablecoins:

Stablecoins are digital currencies that anchor the value of fiat currency or other assets, designed to maintain the stability of prices.Stablecoins are commonly used in the decentralized finance (DeFi) ecosystem to provide fast, low-cost payment solutions.DLT enables stablecoins to be efficiently transmitted globally, reducing friction and intermediary costs in traditional payment systems.Stable coins are usually issued by private companies, representing the issuer’s liabilities to the holder, and the collateral assets held are supported by their credit, and their credit depends on the quality of the collateral and the issuer’s reputation, and are usually anchored to fiat currency or other assets.

Advantages of digital currency

The rise of digital currencies is accompanied by numerous advantages, making them an important part of the financial system.Specifically, digital currencies show significant advantages in the following aspects [22]:

Shared ledger

Digital currencies utilize distributed ledger technology (DLT) to provide a unified infrastructure for cross-border and domestic payments.Compared with the information islands in traditional systems, DLT can effectively reduce operating costs.

Reduce trading time

The decentralized nature of DLT allows transactions to be completed in seconds to minutes.For example, traditional cross-border payments usually require2-5 daysThe processing time of digital currency can shorten this time toHow many seconds to minutes.

Atomic settlement

Digital currencies and DLTs have the characteristics of Atomic Settlement, ensuring that the transaction’s funds and assets are delivered at the same time, greatly reducing counterparty risks, especially in cross-border payments and high-frequency transactions. This mechanism can ensure transactions.It will only be executed when both parties meet the conditions at the same time to prevent some failed transactions.

transparency

The transparency of DLT greatly improves transaction visibility, and all transaction records can be viewed and verified by all participants.Blockchain platforms can reduce transaction reconciliation time from several days toSeconds, which means reducing counterparty risks, especially in supply chain finance and trade finance scenarios where multiple parties participate.

Eliminate intermediaries

Digital currencies are traded through point-to-point methods, reducing their dependence on intermediaries.For example, traditional international remittance systems usually pass through multiple banks or payment processors, while digital currencies allow senders and receivers to trade directly, reducing handling fees and delays.

Financial inclusion

World Bank data shows that there are still1.4 billionPeople are unable to access banking services [23], but more than 60% own mobile phones.Digital currencies can provide low-cost, accessible payment solutions through mobile devices.Especially in areas with underdeveloped financial infrastructure, digital currencies such as stablecoins allow users to participate in the global economy without a bank account, promoting global financial inclusion.

Compliance and security

Digital currencies achieve automated compliance and secure transactions through smart contracts, reduce human operational errors through pre-programmed rules, and reduce fraud and security risks.For example, in financial markets, smart contracts can automatically execute KYC (know your customers) and AML (anti-money laundering) processes to ensure cross-border transactions are compliant.

Programmability

The programmability of digital currencies allows the addition of conditions and logic to the currency, making the payment system more flexible and efficient.For example, programmability allows financial institutions to build highly customized payment processes, which can provide greater efficiency and security in scenarios such as supply chain finance, cross-border payments and automated investment.In addition, smart contracts can also embed compliance checks to ensure that AML (anti-money laundering) and KYC (know your customers) requirements are automatically completed when the transaction is executed, further improving payment security and compliance.

A new paradigm for programmable currency

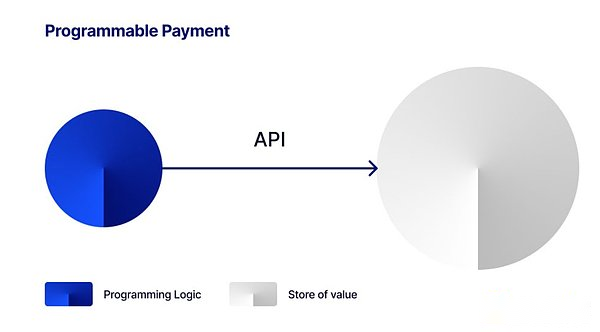

Not only can digital currencies achieve value transfer, issuers can also embed various programming logics into them, which brings many advantages, such as improving user experience, improving transparency, efficiency and accessibility of financial services, and promoting novelty in payment transactions.and creative applications such as automatic execution of conditional payments, pre-authorization, creation of conditional custodial deposits, foreign exchange exchanges for cross-border payments and complex financial operations.

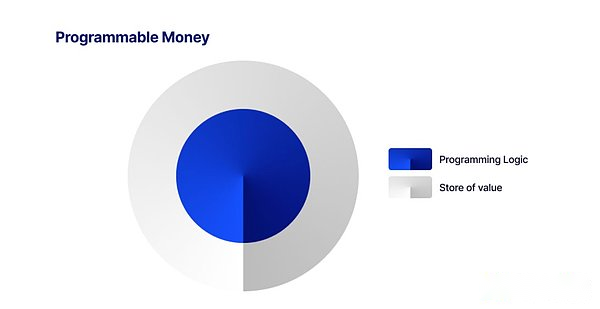

This is completely different from the definition of digital currency in traditional financial technology systems. In traditional systems, digital currency is generally established through database entries. In order to achieve “programmability”, it is necessary to develop a database-independentAdditional technical systems and connect them to the database, either provide connections internally to the entities responsible for database maintenance, or externally to the client through an application programming interface (API). The application uses traditional database APIs that expose program logic andDatabase records interact [24]. Simply put, in traditional systems, the store of value and programming logic are independent and separate, while in the decentralized ledger (blockchain), the store of value and programming of “programmable currency” isLogic is integrated into one, realizing a new paradigm.

Although digital currencies bring many benefits, the ability to simply attach programming logic to monetary units is still controversial, which mainly revolves around the “Singleness” principle of currency.According to this principle, all different forms of currencies, whether in the form of currency is deposited in a bank account, banknote or coins, must be exchanged for each other at face value.In other words, the dollar value in a personal bank account must be equal to the dollar coins in another person’s pocket. As with digital currencies, it is crucial to maintain their homogeneity.Therefore, if we want to perform some complex usage logic for programmable currencies, such as custodial payments using stablecoins from the ERC-20 standard, or for some purpose only, since the ERC-20 standard does not support such complex capabilities,The programmable currency may lose its “uniformity” if additional customized development and new contracts are required. Imagine if a programmable currency that can only be purchased with an ERC-20 compliant programmableIs the currency homogeneous?

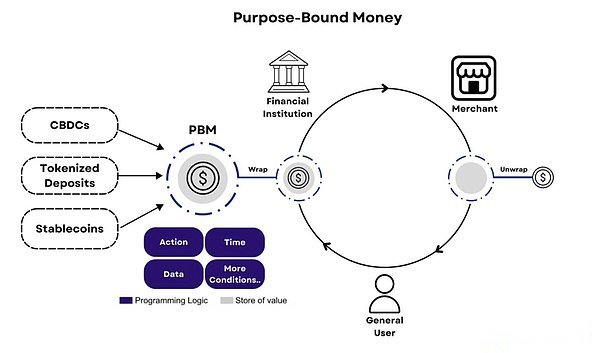

In general, the challenge of programmable payment is that in order to implement more complex programming rules, programmable currencies need to be customized to program the programmable currency themselves, which will not only cause the currency to lose its “singleness”., it also raises policy and public trust issues, and even causes excessive control of rights by institutions that manage implementation mechanisms [25]. In order to solve this challenge, the Monetary Authority of Singapore proposed a new monetary tool “intention”Money (Purpose-Bound Money) [26] attempts to explore the programmability of extending the currency without affecting the homogeneity of initial assets and “singleness”, and explains several current programmable payment forms:

-

Programmable payment: Programmable payment refers to payments that are automatically executed after preset conditions are met.For example, daily consumption limits or regular payments can be set, similar to direct deductions or long-term ordering.Typically, programmable payments are implemented by setting up a database trigger or application programming interface (API) gateway that is located between the ledger system and the client application.These interfaces interact with traditional ledgers and adjust the account balance according to programming logic to achieve automated fund management.Programmable payments have already had a wide range of application cases on the banking side and Internet payment platforms, such as:

-

Regular bill payment: Bank customers can set up automatic payment function to pay utilities, rent or loan installments regularly.As long as the scheduled date arrives and the account balance is sufficient, the system will automatically deduct and complete the payment without manual operation by the user.

-

Personal financial management: Users can set daily or weekly consumption limits for themselves.For example, if the user sets a daily limit of $50, once the day’s spending reaches $50, the system will automatically reject further spending requests, helping the user better control spending.

-

Sub-account management and allocation:Some banks and Internet payment platforms allow users to create sub-accounts and set different payment conditions for each sub-account.For example, users can set up sub-accounts to pay for their children’s education or fixed monthly pocket money, and all payments will be automatically made based on preset conditions.

-

Programmable currency:Programmable currency refers to the medium of exchange that combines store of value and programming logic. These programming rules define or limit their use, such as Transfer, Authorization, Burn, and White defined in the ERC-20 standard.Functions such as Whitelist, or definition rules, make the store of value only sent to the whitelist wallet.

The implementation of programmable currency includes stablecoins, tokenized bank deposits and CBDC. Unlike programmable payments, in programmable payments, programming logic and store of value are separated, and programming logic needs to interact with it outside the store of value system andTransfer value, while programmable currency is self-contained and contains program logic and serves as a store of value, meaning that when programmable currency is transferred to the other party, logic and rules are transferred as well.

-

Intent currency: Programmable currency refers to the medium of exchange that combines store of value and programming logic. These programming rules define or limit their use, such as Transfer, Authorization, Burn, etc. defined in the ERC-20 standard.Whitelist and other functions, or define rules, make the store of value only sent to the whitelist wallet.

The implementation of programmable currency includes stablecoins, tokenized bank deposits and CBDC. Unlike programmable payments, in programmable payments, programming logic and store of value are separated, and programming logic needs to interact with it outside the store of value system andTransfer value, while programmable currency is self-contained and contains program logic and serves as a store of value, meaning that when programmable currency is transferred to the other party, logic and rules are transferred as well.

The use scenarios of intended currency are broad, covering from daily consumption to complex financial transactions.The following are several typical application scenarios [27]:

-

Coupons: The intended currency can be used to issue and manage digital coupons.For example, a mall can design coupons in the form of intention currency that can only be used within a specific merchant, product, or time period.When a consumer purchases a product when eligible, the funds in the intended currency will be automatically released to pay some or all of the fees.

-

Cross-border payments and foreign exchange exchanges: Cross-border payments have always faced high handling fees and foreign exchange transaction fees, and are accompanied by heavy compliance requirements and manual processes.However, these issues are alleviated by adopting Purpose Binding Currency (PBM), which utilizes smart contracts to coordinate cross-border anti-money laundering (AML) and understand your customers (KYC) compliance needs.For example, PBM can preset usage conditions to comply with capital flow rules (such as FATF travel rules), and automatically complete KYC verification and whitelist/sanctions checks for users and their wallets when they achieve transaction purposes, or implement currency controlsIn countries where PBM can also introduce consumption restrictions to comply with local regulation.

Not only that, PBM is also able to achieve compliant foreign exchange exchange through composability with decentralized exchanges (DEXs).Users can make payments in one currency and then automatically exchange them for another through a smart contract.This foreign exchange process can be completed through DeFi protocols such as automated market makers (AMM), Order Book, or Vault), and the exchange rate is automatically dynamically adjusted according to the liquidity of a specific currency pair.Although this method requires a large number of currency pairs and sufficient liquidity pools on the chain, with the popularity of digital currencies and the development of decentralized ledger (blockchain) technology, this model will become more and more mature,Global cross-border payments bring higher efficiency, lower costs and stronger compliance guarantees.

-

Programmable hosting payment: Hosted payment has been widely used in global economic activities. For example, in international trade scenarios, trade entities adopt tools such as letters of credit to achieve “cash on delivery” transactions, that is, using the bank’s credit as a guarantee and when the seller performs it.Payment can only be received after its obligations.Or in the e-commerce scenario, when the user is shopping on the e-commerce platform, when the buyer places an order and pays, the funds will not be transferred to the seller’s account immediately, but will be escrowed by a third-party platform.Funds will be released from the escrow account to the seller only when the buyer confirms that the item is received and is satisfied.If the buyer does not confirm receipt within a certain period of time, the system will confirm by default, and the funds will be automatically transferred to the seller, and the right of payment will be retained before the buyer receives and confirms that the goods are satisfied.

Intent currency (PBM) provides innovative solutions to this process in the trend of programmable payments.Through PBM, payment can be pre-programmable and transferred to the other party in “programmable packaging form”, and will be automatically unpacked after the buyer confirms receipt, and the funds will be released to the supplier.This “programmable custody” mechanism ensures that funds will not be withdrawn until pre-set conditions are met, and once the transaction is completed, the payee can get payment immediately. Since the custody funds are visible to both parties to the transaction, their programmability will beThe possibility of fraud is greatly reduced.In addition, tokenized custodial funds can also be used as collateral, similar to factoring, which helps merchants more easily obtain credit support and improve financial resilience.

-

Charity / Public Use Funds:For the management of charity or public funds, the intended currency can ensure that the use of funds is strictly in line with the designated purpose.For example, a government or charity may set the relief funds to be only available in a specific supermarket or pharmacy and limited to the purchase of basic daily necessities or medicines.This characteristic of the intended currency prevents the abuse and misappropriation of funds and ensures that every donation can be used for the original intention.At the same time, the built-in compliance module can also ensure that the fund issuance and use process is transparent and traceable, and comply with relevant regulations.

Project cases of digital currency and smart contracts

The programmability potential of the combination of digital currencies and smart contracts is huge, and this combination can significantly improve the efficiency, transparency and security of financial transactions.The automation characteristics of smart contracts enable the delivery of funds and assets to be automatically completed when preset conditions are met, reducing human intervention and operational risks.This efficient and secure transaction model has shown great application value and development potential in many fields such as trade financing, cross-border payments, and supply chain management.At present, many public sectors and private institutions have conducted a series of explorations internationally. The following are several typical application scenarios:

Simplify trade and supply chain financing:

-

Project Dynamo: Project Dynamo was initiated by the Innovation Centre of the Bank for International Settlements, the Hong Kong Monetary Authority and Linklogis, creating an innovative SME financing solution on DLT by leveraging Digital Trade Tokens and smart contracts.The project aims to simplify the supply chain financing process through electronic bills of lading and programmable payment mechanisms, helping small and medium-sized enterprises obtain more efficient and transparent financial support.In addition, every node in the supply chain can automatically release funds through smart contracts, reducing the risk of default [28].

-

Australian Tokenized Invoice CBDC Pilot Project:The Australian CBDC pilot project is composed of the RBA and the Digital Finance Cooperation Research Center (DFCRC) and Unizon initiated, the pilot project demonstrates the application of tokenized invoices in third-party sales and payments, involving a wholesale car dealer (supplier), third-party financing agencies and wholesale car buyers.The supplier generates a tokenized invoice on behalf of the buyer’s payment request and divides it and sells it to a third-party financing agency to optimize the supplier’s working capital.When the invoice expires, buyers use stablecoins supported by pilot central bank digital currency (CBDC), and the system automatically settles the payments to suppliers and financing institutions at the same time [29].

Cross-border payment:

-