Original title: “RootData: 2024 Crypto Development Research Report and Annual Rankings”

Author: RootData Research

Crypto 2024 Venture Capital Market Review

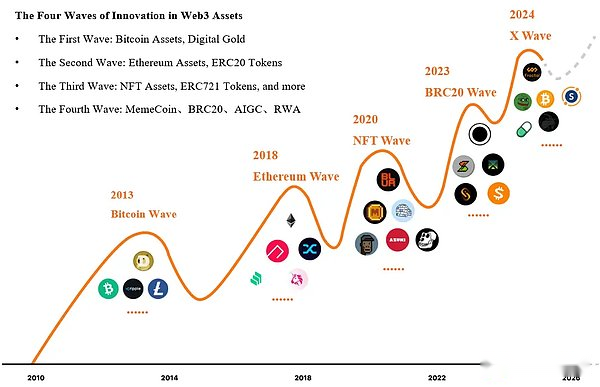

The Crypto industry enters the fourth wave of asset innovation, and the primary and secondary markets are highly conductive

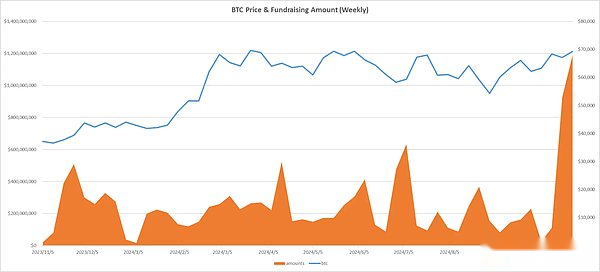

With the passage of Bitcoin and Ethereum spot ETFs, the development of the Crypto industry has a long-term and solid liquidity foundation. Overall, the primary market has a certain lag compared to the secondary market, but the primary and secondary markets are obviously conductive.The primary market showed a trend of rising first and then stabilizing in the first three quarters of 2024: the total financing amount in Q1 was US$2.545 billion (slightly increased by 0.76% year-on-year), and continued the upward momentum to US$2.75 billion (similar to 8.05% month-on-month), and although Q3 was slightly retracement to$2.406 billion, but it still increased significantly by 26.05% year-on-year.

In fact, the Crypto industry has entered the fourth wave of asset innovation, mainly driven by non-EVM MemeCoin, BRC20, AIGC, and RWA assets. In the past 12 months, the market does not seem to have reached a large-scale consensus on these asset innovations, which is alsoThis is an important reason why the primary market cannot create new price highs like BTC.In our opinion, one of the laws of the development of the Crypto industry is to find new native assets with the greatest consensus and realize the influx of new assets to drive funds.

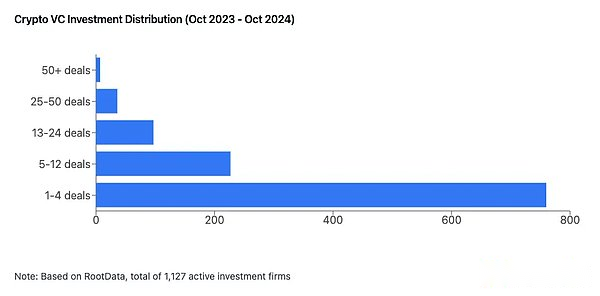

Changes in transaction structure: 54.9% of institutions have not taken any action in the past 12 months, and only 12% of projects have completed two rounds of financing or more

54.9% of institutions have not taken any action in the past 12 months, and the average amount of financing has increased by US$53,139 per round compared with 2023, an increase of about 0.62%.The Crypto primary market has a clear head effect. Through a questionnaire survey of investors by RootData in September, most investment institutions do not take action or are inactive, which is due to:

-

No major innovation has been seen in the industry;

-

High opacity in project information;

-

Uncertainty caused by rapid changes in the industry;

-

Poor liquidity and poor exit.

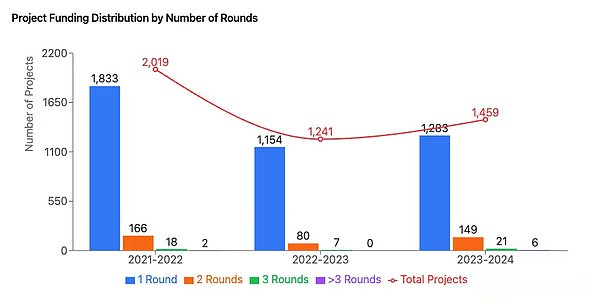

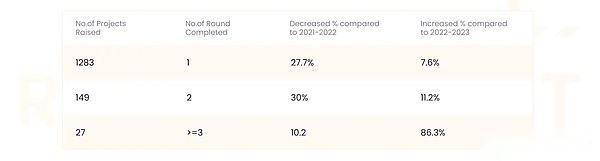

RootData statistics show that a total of 1,459 financings have occurred in the past 12 months, and only 1,283 projects have completed one round of financing, 149 projects have completed the second round of financing, and 27 projects have completed the third round of financing; compared with 2021-The three data in 2022 decreased by 27.7%, 30.0% and 10.2% respectively, but rose by 7.6%, 11.2% and 86.3% respectively compared with 2022-2023. This also shows that the industry is still in its early stages and there are many unsuccessful markets.The technology and innovation of falsification also show that many projects will face pressure from subsequent financing.

Popular investment tracks and ecology competition: Base ecosystem is the L2 with the largest growth rate in the past 12 months, and DeFi is considered the most undervalued track by more than 41% of investors

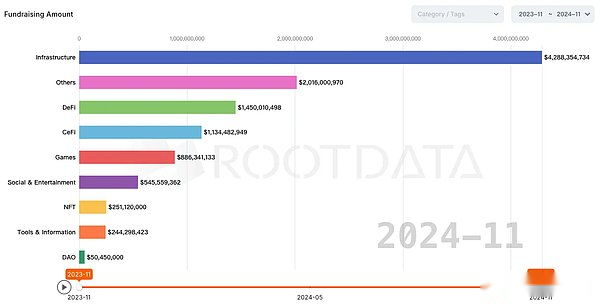

Infrastructure tracks have invested more than $4.2 billion in the past 12 months, and DeFi tracks have invested more than $1.4 billion. According to a September investor survey, DeFi is being considered by more than 41% of investors to be the most current.In an undervalued track, the L1/L2 track is considered to be overvalued by 48% of investors.

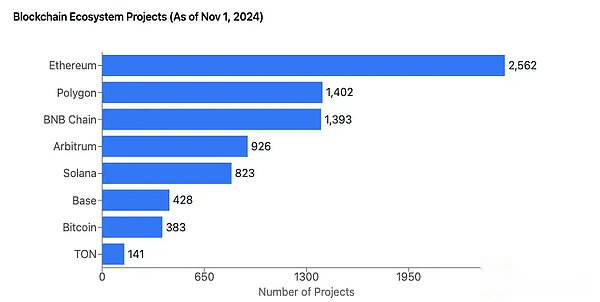

With its first-mover advantage and complete developer ecosystem, Ethereum continues to dominate the ecosystem list with a scale of 2,562 projects. Solana ecosystem rebounded strongly after experiencing the impact of the FTX event in 2022, with the number of projects reaching 823. Bitcoin ecosystemThe TON ecosystem is also developing rapidly, with 383 ecological projects and 141 respectively.

It is worth noting that Base, as an L2 solution supported by Coinbase, has rapidly accumulated 428 projects since its launch in August 2023, achieving a growth of more than 28% in the Ethereum L2 ecosystem, making it the L2 network with the largest growth rate in the ecosystem.

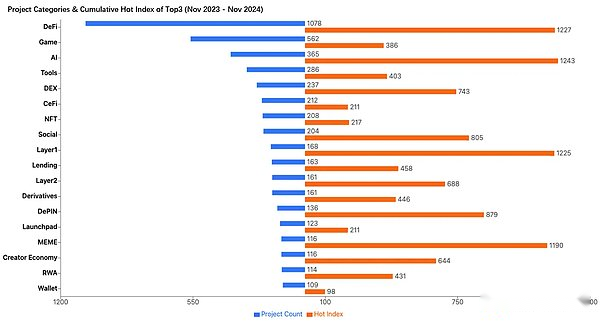

L1, DeFi and AI tracks are the most popular. DeFi, Game, and AI have added the most tags in the past 12 months. Monad has the highest single financing.

According to RootData statistics, DeFi has added the most tags to new projects in the past 12 months, followed by Game and AI sectors. However, it is worth noting that DeFi and AI are also the most popular sectors in the past 12 months, and Game isAdded popular tags for new projects, but it lags behind in the popularity rankings, perhaps because Game has not created satisfactory results in both product and token price performance in the past four quarters.

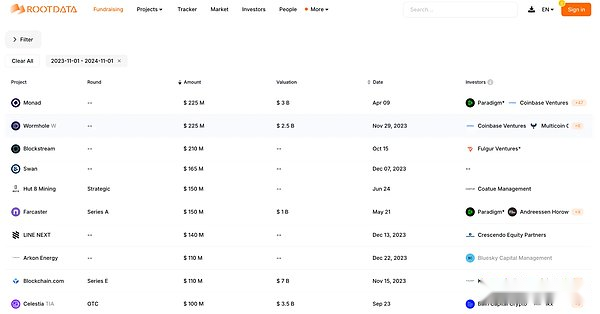

Looking back at the top 10 investment and financing transactions in the past 12 months, Monad ranked first with a valuation of US$3 billion in April this year. It is worth noting that among the top 10 transactions, in addition to the common CeFi, mining and other capital.Outside the high-development track, Celestia announced in September that US$100 million OTC financing ranked among the top ten transactions, which may also reveal that OTC trading will become one of the important trends in the industry.

List background and standards

Since the release of RootData List in 2023, its list results are being paid attention to by more entrepreneurs, investors, LPs and general Crypto enthusiasts. RootData is committed to demonstrating the core strength and trend characteristics of industry development through rigorous data analysis.

The statistics of this list are from October 31, 2023 to October 31, 2024. A total of five lists are released, specifically: Top 50 projects (TGE completed), Top 50 projects (TGE not performed), and Crypto VC Top50 investment institutions, Top 10 angel investors, Top 20 best CEOs.

Top 50 projects (TGE completed)

-

Liquidity characteristics: Tokens, which have been listed on the list, have now been launched on five major mainstream exchanges (Binance, OKX, Bybit, Upbit and Coinbase).Among them, 82% of the tokens in the project are online on at least three major mainstream exchanges.

-

Track features: The projects on the list come from 22 tracks, most of which are Layer1, DeFi, and AI track projects.Compared with last year, there are 5 new MemeCoin projects on this year, which is due to our belief that MemeCoin is building a new asset product category and reflects its unique value in enriching Crypto asset classes and helping Crypto become popular.

-

Financing characteristics: The median financing of the projects on the list was US$23.15 million, with an average of 2 rounds of financing, and 13 projects on the list did not raise funds.It is worth mentioning that according to FDMC/Raised calculations in the past 12 months, all of the top 5 projects are on the list, Celestia (3,670x), Ondo Finance (1,819x), Jito (1,322x), Ethena (1,134x), Sei (816x).

Top 50 projects (TGE not completed)

-

Financing features: The median financing of projects selected for this list is US$25.71 million, with an average financing round of 2 rounds. Seven projects have valuations of US$1 billion (inclusive), and 4 projects have not disclosed financing.

-

Track features: Most of the projects on the list cover 26 tracks, with modularity, DeFi, infrastructure and AI accounting for a large proportion. In the past four quarters, although GameFi, CeFi, and NFT tracks have fallen into a period of innovation stagnation, we still chooseProjects with innovative representatives in these tracks.

Crypto VC Top50

The 50 institutions on the list made an average of 28 shots and led the average of 7 shots in the past four quarters.To some extent, these institutions have shaped the investment trends and characteristics of Crypto over the past four quarters.46% of institutions are distributed in North America, 20% are distributed in China (including Hong Kong, Macao and Taiwan), and the remaining 34% are distributed in Singapore, Dubai and other places.

Among the selected institutions, Crypto native investment institutions (including the Crypto project strategic investment department of traditional investment institutions) account for about 80%, and the rest are traditional investment institutions. Different types of institutions are promoting the early entrepreneurial and innovation ecosystem of Crypto to become more robust.

Angel Investor

As the investor group is rapidly rising today, RootData has currently included 2,037 angel investors (at least once invested).These active angel investors are mainly successful Crypto entrepreneurs, with the average number of 18 attempts in the Top 10 angel investors in the past 12 months.As the angel investor group continues to grow, Crypto’s early innovation and entrepreneurship ecosystem will become healthier.

CEO Top 20

According to a survey for investors released by RootData in September, 75% of investors are listing CEOs and teams as the first factor in investment considerations. RootData currently includes 1,827 Crypto project CEOs, and we believe that high-quality Crypto CEOs belong toScarce resources are the most critical force in the development and growth of the industry.

About RootData

RootData is a data platform for discovering and tracking of Web3 assets. It is the first to encapsulate the on-chain and off-chain data of Web3 assets. It has higher data structure and higher readability. It is committed to becoming a productivity-level tool for Web3 enthusiasts and investors.