Author: coinbase Source: coinbase official website Translation: Shan Oppa, Bitchain Vision

A summary of one sentence

Various classifications of ETH (Ethereum) roles raise some questions about their position in the portfolio.We clarified some of the narratives and pointed to possible potential drivers for the asset in the coming months.

Main conclusion

Although Ethereum has performed poorly year-to-date, we believe its long-term positioning remains strong.We think it has the potential to see upward surprises later in the cycle.

We also believe that Ethereum has some of the strongest ongoing demand drivers in cryptocurrencies and maintains a unique advantage on its expansion roadmap.

ETH’s historical trading model shows that it benefits from a mix of “store of value” and “technology token” narratives.

The U.S. approval of spot Bitcoin ETF reinforces Bitcoin’s store of value narrative and its position as a macro asset.On the other hand, the open question about ETH’s basic positioning in the cryptocurrency field still exists.The first layer (L1) blockchains of competition, such as Solana, undermine Ethereum’s position as a “preferred” network for deployment of a decentralized application (dApp).The growth of Ethereum Layer 2 (L2) and the decrease in ETH burning also seem to affect the asset’s value accumulation mechanism at a high level.

Nevertheless, we still believe that Ethereum’s long-term positioning remains strong and that it has important advantages that significantly distinguishes it from other smart contract networks.These advantages include the maturity of the Solidity developer ecosystem, the popularity of EVM platforms, the practicality of ETH as a DeFi collateral, and the decentralization and security of its mainnet.Furthermore, we believe that advances in tokenization may affect ETH more positively in the short term, relative to other L1 blockchains.

We found that ETH’s ability to capture store of value and technical token narratives is demonstrated in its historical trading model.ETH is highly correlated with BTC, showing behavior consistent with BTC store of value patterns.Meanwhile, it decouples from BTC during a period of long-term rising BTC prices (such as other altcoins), acting like a technology-oriented cryptocurrency.We believe ETH will continue to juggle these roles and have a chance to perform well in the second half of 2024 despite underperforming year-to-date.

Deal with opposition narratives

ETH is classified into multiple roles, from its “ultrasonic currency” that supplies combustion mechanisms to its “Internet bonds” that have non-inflationary pledge income.With the expansion and restake of L2, narratives such as “settlement layer assets” or the more profound “universal objective working token” have also surfaced.But ultimately, we believe that these categories cannot fully capture the dynamics of ETH.In fact, we believe that the complexity of ETH use cases increases the difficulty of defining a single value capture metric.Instead, the convergence of these narratives may even appear negative because they may weaken each other—diverging market participants’ focus on positive drivers of tokens.

Spot ETH ETF

Spot ETFs are crucial to BTC as they provide regulatory clarity and new pathways for capital inflows.These ETFs structurally change the industry and, in our view, challenged previous cycle patterns, namely capital rotation from Bitcoin to Ethereum to higher beta altcoins.There are barriers between ETFs and centralized exchanges (CEXs), only the latter can reach the wider crypto asset universe.Potential approval of spot ETH ETF eliminates this barrier to ETH, allowing ETH to enter the capital pool currently only enjoyed by BTC.In our opinion, this is ETH’s biggest unanswered question in the near future, especially in the current challenging regulatory environment.

Although there is uncertainty in timely approval given the SEC’s obvious silence to issuers, we believe that the existence of the U.S. spot ETH ETF is only a matter of time, not a question of whether to approve it.In fact, the main reasons used to approve spot BTC ETFs also apply to spot ETH ETFs.That is, the correlation between CME futures products and spot exchange rates is high enough that “the supervision of CME can reasonably anticipate detection of…inappropriate behavior in the spot market”.The time period for the relevance study in the Spot BTC approval notice began in March 2021, one month after the launch of CME ETH futures.We believe that this evaluation period was chosen intentionally so that similar reasoning could be applied to the ETH market.In fact, the correlation analysis proposed by Coinbase and Grayscale previously showed that the spot and futures correlations of the ETH market were similar to those of the BTC market.

Assuming the correlation analysis holds, we believe that the remaining possible reasons for rejection may be due to the nature difference between Ethereum and Bitcoin.In the past, we have discussed some differences in the size and depth of ETH and BTC futures markets, which may be a factor in the SEC decision.But among other basic differences between ETH and BTC, we believe that the most relevant to the approval issue is Ethereum’s Proof of Stake (PoS) mechanism.

Since regulatory guidance on asset pledge has not been clearly specified, we believe that spot ETH ETFs that allow pledged are unlikely to be approved in the near term.There is a significant difference from Bitcoin due to beheading conditions, differences between verification clients, possible opaque fee structure for third-party staking providers, and the complexity of liquidity risks (and exit queue congestion) of unstaking.(It is worth noting that Europe has staking ETH ETFs, but overall, exchange-traded products in Europe are different from those offered in the United States.) Nevertheless, we do not think this should affect the status of unstaking ETH.

We believe there is room for upward surprise in this decision.Polymarket predicts the probability of approval on May 31, 2024 is 16%, while Grayscale Ethereum Trust (ETHE) trades at a 24% discount on net asset value (NAV).We believe the probability of approval is close to 30-40%.As cryptocurrencies begin to become an election issue, we think it is also less certain whether the SEC is willing to pay the necessary political capital for support.Even if the first deadline of May 23, 2024 was rejected, we believe the lawsuit could overturn the decision.Furthermore, it is worth noting that not all spot ETH ETF applications require approval at the same time.In fact, the Uyeda Commissioner’s statement on the approval of the spot BTC ETF criticized the hidden “motive to accelerate application for approval, namely to prevent the first-hander advantage.”

Challenges to replace L1

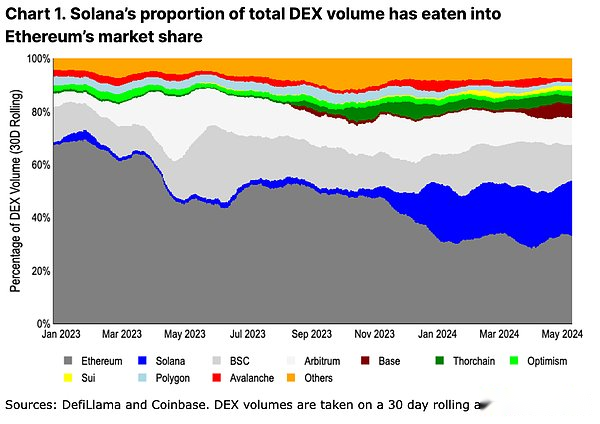

At the adoption level, the rise of highly scalable integration chains (particularly Solana) seems to be sucking Ethereum’s market share.High throughput and low rate trading shift the center of trading activity away from the Ethereum mainnet.It is worth noting that Solana’s ecosystem has grown from accounting for only 2% of decentralized exchanges (DEX) trading volume in the past year to 21% now.

In our opinion, the current alternative first layer (L1) blockchain provides a more meaningful differentiation in terms of Ethereum compared to the previous bull cycle.The shift to non-Ethereum virtual machines (EVMs) and redesigning decentralized applications (dApps) from scratch leads to a unique user experience (UX) in different ecosystems.In addition, the integrated/monopoly extension approach enables more composability across applications and avoids the problems of poor bridging user experience and fragmentation of liquidity.

While these value propositions are important, we believe it is too early to extrapolate the incentive metrics of activity as a confirmation of success.For example, the number of Ethereum L2 transaction users has dropped by more than 80% from its peak airdrop period.At the same time, between the announcement of the airdrop on November 16, 2023 and the first collection date on January 31, 2024, Solana’s share of the total decentralized exchange (DEX) increased from 6% to 17% from 6% to 17% from the time it was announced on November 16, 2023..(Jupiter is the leading DEX aggregator on Solana).Jupiter also has three unfinished rounds of four airdrops, so we expect the Solana DEX event to remain high for a while.At the same time, the assumptions about long-term activity retention are still speculative.

Nevertheless, the leading Ethereum L2 (Arbitrum, Optimism and Base) trading activity now accounts for 17% of the total DEX volume (plus 33% of Ethereum).This may provide a more appropriate comparison to an alternative L1 solution for ETH demand drivers, as ETH is used as a native gas token on all three L2s.MEV and other additional demand drivers in these networks have not been developed, which also provides room for future demand catalysts.We believe this is a more equivalent comparison of integration and modular extension approach in terms of DEX activities.

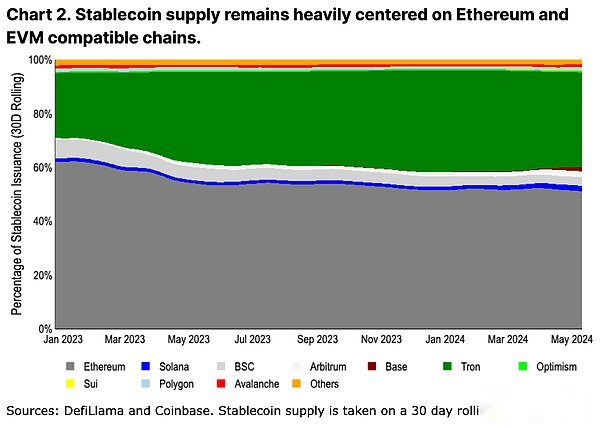

Another more “sticky” adoption indicator is the stablecoin supply.The stablecoin distribution changes slowly due to bridging and issuance/redemption friction.(See Figure 2. The color scheme and sorting are the same as Figure 1, Thorchain is replaced by Tron).Calculated by stablecoin issuance, activity is still dominated by Ethereum.We believe that this is because the trust assumptions and reliability of many new chains are still insufficient to support a large amount of capital, especially those locked in smart contracts.Large capital holders are often indifferent (proportionally calculated) to Ethereum’s higher transaction costs and tend to reduce risk by reducing liquidity downtime and minimizing the bridge trust assumption.

Even so, in high-throughput chains, stablecoin supply is growing faster on Ethereum L2 than Solana.Arbitrum surpassed Solana’s stablecoin supply ($3.6 billion and $3.2 billion, respectively) in early 2024, while Base’s stablecoin supply has grown from $160 million to $2.4 billion year-to-date.While the final conclusions about the expansion debate are unclear, early signs of stablecoin growth may actually favor Ethereum L2 rather than replace L1.

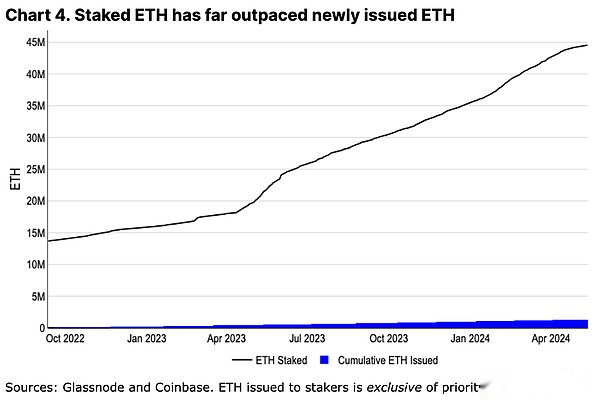

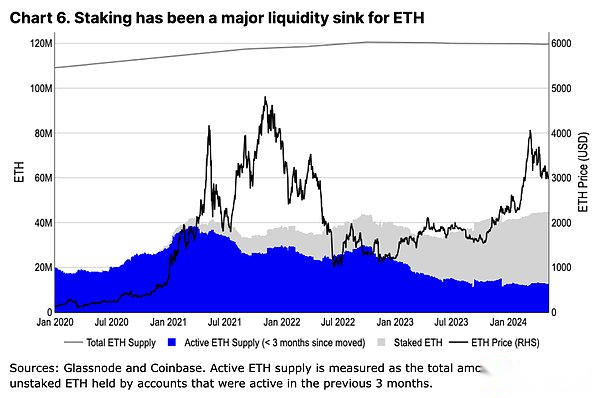

The growing adoption of L2 raises concerns that they actually have an erosion of ETH—they reduce the need for block space in L1 (and thus reduce transaction fee burning) and may support non-ETH gas tokens in their ecosystem (Further reduce ETH combustion).In fact, ETH has reached its highest annualized inflation rate since its transition to Proof of Stake (PoS) in 2022.Although inflation is often understood as an important component of BTC’s structural nature, we don’t think this applies to ETH.All ETH issuance is accumulated in the hands of the pledger, and the collective balance of the pledger far exceeds the cumulative ETH issuance since the merger (see Figure 4).This is in direct contrast to Bitcoin’s Proof of Work (PoW) miner economics, where miners need to sell a large amount of newly issued BTC to fund operations in a competitive hash rate environment.While miners’ BTC holdings are tracked in the cycle to cope with their inevitable sale, the minimum operating cost of pledged ETH means that pledgers can continue to accumulate their positions.In fact, staking has become a precipitation of ETH liquidity – the growth rate of pledged ETH is 20 times higher than the issuance rate of ETH (even if burning is not included).

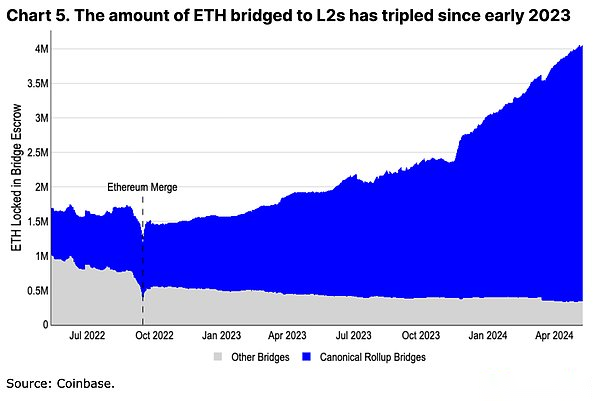

L2 itself is also an important demand driver for ETH.More than 3.5 million ETH have been bridged to the L2 ecosystem, becoming another liquidity precipitation for ETH.In addition, even if the ETH bridged to L2 is not burned directly, the new wallet pays the transaction fee and their reserves constitute a soft lock on the increasing number of ETH tokens.

In addition, we believe that even if L2 is expanded, some core activities will remain on the Ethereum mainnet forever.Re-staking activities like EigenLayer or governance actions for major protocols such as Aave, Maker and Uniswap are still firmly rooted in L1.Users with the highest security needs (usually holding the largest capital) may also leave funds at L1 until a fully decentralized sorter and permissionless fraud proof deployment and testing is completed – a process that can take several yearstime.Even if L2 innovates in different directions, ETH will always be an integral part of its fiscal reserves (used to pay L1 “rentals”) and local accounting units.We firmly believe that the growth of L2 is not only beneficial to the Ethereum ecosystem, but also to ETH assets.

Advantages of Ethereum

In addition to common metric-driven narratives, we believe Ethereum has some difficult but equally important advantages.These may not be short-term trading narratives, but represent a core set of long-term strengths that can maintain their current dominance.

Quality collateral and accounting units

One of the most important use cases for ETH is its role in DeFi.ETH is able to leverage operations in Ethereum and its L2 ecosystem with minimal adversary risk.It acts as collateral in money markets such as Maker and Aave and is also the basic trading unit for many on-chain DEX pairs.DeFi expansion on Ethereum and its L2 will lead to additional liquidity precipitation of ETH.

Although BTC remains the dominant store of value asset on a wider scale, using wrappers on Ethereum introduces the bridge and trust assumptions.We don’t think WBTC will replace ETH’s use in Ethereum-based DeFi—WBTC supply has remained stable for more than a year, more than 40% below its previous high.Instead, ETH can benefit from its utility in various L2 ecosystems.

Continuous innovation in decentralization

An often overlooked component of the Ethereum community is its ability to continue to innovate while decentralizing.Some have criticized the long release timeline and delayed development, but few have acknowledged the complexity in weighing the goals and goals of various stakeholders to achieve technological advancements.Developers with more than five execution clients and four consensus clients need to coordinate design, test, and deploy changes without affecting mainnet execution.

Since Bitcoin’s Taproot upgrade in November 2021, Ethereum has achieved dynamic transaction burning (August 2021), shifting to PoS (September 2022), enabling staking withdrawals (March 2023) andCreate blob storage for L2 extensions (March 2024) – and many other Ethereum Improvement Proposals (EIPs) included in these upgrades.While many alternative L1s seem to be able to develop more quickly, their single client makes it more vulnerable and centralized.The path to decentralization inevitably leads to some degree of rigidity, and it is unclear whether other ecosystems have the ability to create equally effective development processes when starting this process.

Fast L2 innovation

This is not to say that Ethereum innovation is slower than other ecosystems.Instead, we believe that innovations around execution environments and development tools actually surpass their competitors.Ethereum benefits from the rapid centralized development of L2, all of which are paid to L1 by ETH.The ability to create various platforms with different execution environments (such as Web Assembly, Move, or Solana virtual machines) or other features (such as privacy or enhanced staking rewards), meaning L1’s slower development timeline doesn’t hinder ETH fromMore technology comprehensive use cases are adopted.

At the same time, the Ethereum community strives to define different trust assumptions and definitions around sidechains, validiums, rollups, etc., which increases transparency in the field.For example, similar efforts (such as L2Beat) in the Bitcoin L2 ecosystem have not yet emerged, where its L2 trust assumptions vary widely and are often not fully communicated or understood by the wider community.

EVM surge

While innovations around the new execution environment do not mean that Solidity and Ethereum Virtual Machines (EVMs) will be outdated in the near future, instead, EVMs have spread widely to other chains.For example, the research on Ethereum L2 is adopted by many Bitcoin L2.A large part of Solidity’s drawbacks (e.g., prone to reentering vulnerabilities) now have static tool checkers to prevent basic vulnerabilities.Additionally, the popularity of the language creates a full-fledged audit department, a large number of open source code examples and detailed best practice guides.These are very important in building a large developer talent pool.

Although the use of EVM does not directly lead to ETH requirements, changes to EVM are rooted in the development process of Ethereum.These changes are then adopted by other chains to maintain EVM compatibility.In our opinion, EVM’s core innovations may still be rooted in Ethereum — or soon adopted by L2 — which will focus developers’ attention and new protocols within the Ethereum ecosystem.

Tokenization and Lindi effect

We believe that driving tokenization projects and increased regulatory clarity in globally may also benefit Ethereum in the first place (in public blockchains).Financial products often focus on technical risk mitigation rather than optimization and feature richness, and Ethereum has advantages as the longest-running smart contract platform.We believe that slightly higher transaction fees (in USD, not minutes) and longer confirmation times (in seconds, not milliseconds) are secondary issues for many large tokenization projects.

Additionally, hiring a sufficient number of developers is a key factor for traditional companies looking to expand on-chain operations.Here, Solidity becomes the obvious choice because it forms the largest subset of smart contract developers, which echoes the above-mentioned view of EVM propagation.Blackrock’s BUIDL fund operates on Ethereum, as well as the JPM’s ERC-20-compatible Onyx Digital Assets Fungible Asset Contract (ODA-FACT) token standard is an early sign of the importance of this talent pool.

Structural supply mechanism

The change in the active supply of ETH is significantly different from that of BTC.Although prices have risen since the fourth quarter of 2023, the three-month circulation supply of ETH has not increased significantly.In contrast, within the same time frame, we observed an increase in active BTC supply by nearly 75%.Long-term ETH holders do not increase circulation supply like Ethereum still operates in PoW in the 2021/22 cycle, but rather a growing part of the ETH supply is pledged.This once again confirms our view that pledge is an important liquidity precipitation for ETH and minimizes structural selling pressure of assets.

The evolving trade system

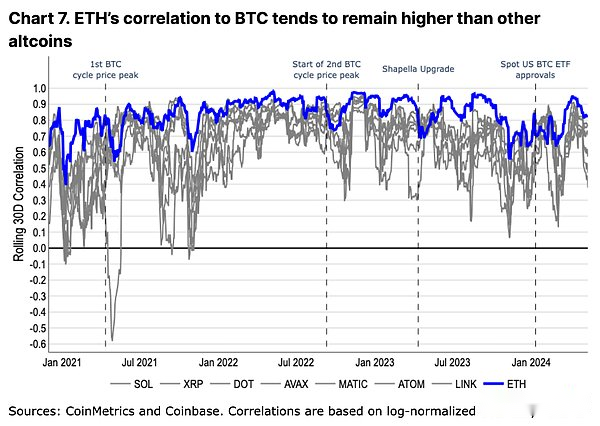

ETH’s historical trading model is closer to BTC than any other altcoin.At the same time, it will also be decoupled from BTC during bull peaks or specific ecosystem events—a pattern that has been observed in other altcoins, but to a lesser extent (see Figure 7).We believe that this trading behavior reflects the market’s relative valuation of ETH, both as a store of value token and as a technical practical token.

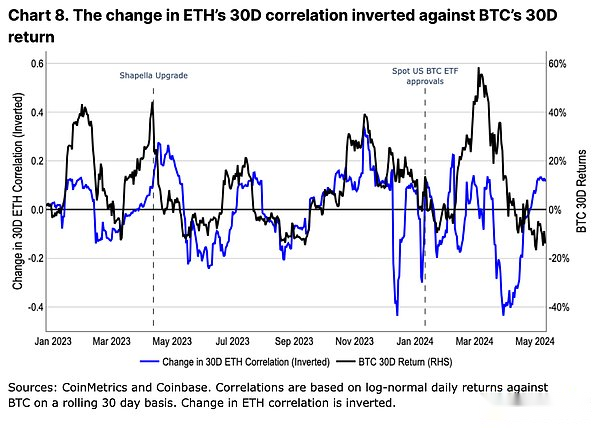

In 2023, the correlation change between ETH and BTC is inversely related to the price change of BTC (see Figure 8).That is, when BTC appreciates, the correlation between ETH and BTC decreases, and vice versa.In fact, changes in BTC prices appear to be a leading indicator of changes in ETH correlation.We believe that this is an indicator of the market’s excitement for altcoins led by BTC prices, which in turn improves its speculative performance (i.e., altcoins trade differently in bull markets but consistent with BTC’s performance in bear markets).

However, this trend has weakened after the approval of the spot US BTC ETF.In our view, this highlights the structural impact of ETF-based capital inflows, with a completely new capital base that only accesses BTC.Emerging registered investment advisors (RIAs), wealth managers and financial institutions have different views on BTC in their portfolios than many crypto locals or retail traders.In a purely crypto portfolio, BTC is the least volatile asset, while in more traditional fixed income and stock portfolios, it is often considered a small diversified asset.We believe that this shift in BTC utility has an impact on its trading model with ETH, and if spot U.S. ETH ETFs appear, similar changes (and re-adjustment of trading model).

in conclusion

We believe there are still potential upward surprises for ETH in the coming months.ETH does not appear to have a major supply-side pressure source, such as token unlocking or miner selling pressure.On the contrary, staking and L2 growth have proven to be an important and growing precipitation of ETH liquidity.We believe that ETH’s position as a DeFi center is unlikely to be replaced due to the widespread adoption of EVM and its L2 innovation.

Nevertheless, the importance of potential spot US ETH ETFs cannot be underestimated.We believe that the market may underestimate the timing and probability of potential approvals, which leaves room for upward surprises.During this period, we believe that ETH’s structural demand drivers and technological innovations within its ecosystem will allow it to continue to span multiple narratives.