Author: Coinbase Research Translation: Good Ouba, Bit Chain Vision

Ethereum’s equity certificate (POS) consensus mechanism is the largest economic security fund in cryptocurrencies, with a total of nearly US $ 112B.However, the authentication of network security can not only earn basic rewards through locking ETH.For a long time, the mobile pledged token (LST) has been a way for participants to bring their ETH and consensus layer income into the DEFI field -they can be traded in other transactions or re -mortgaged as a mortgage.Now, the emergence of re -mortgaging has introduced another layer in the form of liquidity to re -mortgage tokens (LRT).

Ethereum’s relatively mature pledge infrastructure and excess security budget enable EIGENLAYER to grow into the second largest DEFI protocol (total lock value (TVL) to $ 12.4B) in an ecosystem.EIGENLAYER enables verificationrs to ensure the security of active verification services (AVS) by reassembling ETH to get additional rewards.Therefore, intermediaries that exist in the form of liquid reinventing protocol have become more and more common, which has promoted the spread of light rails.

In other words, we believe that from a security and financial perspective, re -pledge and LRT may bring additional risks compared to existing pledged products.With the growth of the number of autonomous driving systems and the differentiation of light rail operator strategies, these risks may become increasingly opaque.Nevertheless, re -pledge (and pledge) rewards are laying the foundation for the new DEFI agreement.If these proposals are implemented, separate discussions that reduce pledge distribution to minimum feasible distribution (MVI) may further increase the relative importance of long -term recalculation yields.Therefore, excessive attention to re -seizing opportunities is becoming one of the biggest encryption themes this year.

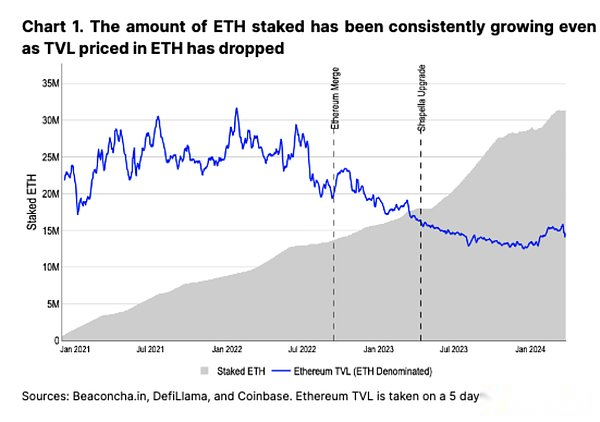

The re -mortgage agreement of the EIGENLAYER was launched on the Ethereum Master Online in June 2023. AVS will be launched in the next stage of its multi -stage deployment (the second quarter of 2024).In fact, Eigenlayer’s “re -mortgage” concept establishes a method of protecting the new features of Ethereum, such as data availability layer, summary, bridge, prophecy machine, cross -chain message, etc., and may get additional additional additions in this process.award.This represents a new source of income in the form of “security is service”.Why is this a hot topic? As the largest POS cryptocurrency, ETH currently has a huge economic foundation to protect its network from malicious majority attacks.However, at the same time, the continuous growth of verifications and pledged ETH can be said to have exceeded the scope required for the protection of the network.At the merger (September 15, 2022), 13.7 million ETH pledged by pledged, probably enough to ensure that 22.1 million ETH network TVL at that time.As of the news that we are about to release, about 31.3 million ETHs have been pledged, and the number of ETH pricing has tripled, but Ethereum is actually lower(It is lower than the end of 2022), 14.9 million ETH (see Figure 1).Basic pledge of Ethereum

>

The security, liquidity and reliability of too much pledged ETH and basic assets have unique advantages and help promote the security of other decentralized services.In other words, we believe that re -mortgaging as a concept is largely inevitable, as an extension of ETH’s inherent value.However, there is no free lunch in the world.In order to ensure the correctness of these services, the mortgage is re -mortgaged for behavioral verification, and it may be detained or reduced, similar to traditional mortgage.(In other words, when the first group of AVS was launched in the second quarter of 2024, it will not be enabled and cut.) Like pledges, re -pledged operators will get additional ETH (or AVS tokens) due to their services.

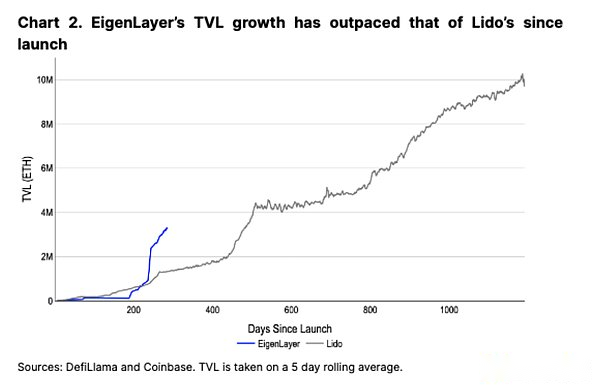

So far, Eigenlayer’s TVL growth is shocking, second only to Lido (Ethereum leading liquid pledge agreement).EIGENLAYER achieves this goal, while retaining the maximum deposit limit of the process, and before starting any real -time AVS.In other words, it is difficult to decompose the continuous heavy pledge needs with the user’s interest in short -term points and airdrop mining.Although the number of ETH pledged in the pledge may continue to grow with the maturity of the agreement, we believe that when the end -of -time mining or the early AVS reward is lower than expected, the TVL may decline short -term.Discussion of pledge

>

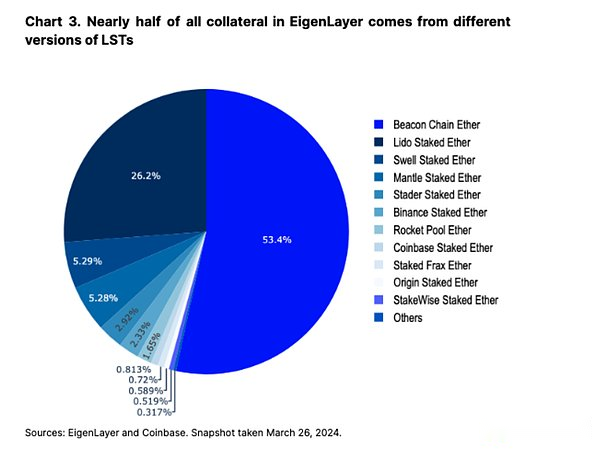

EIGENLAYER is based on the existing pledge ecosystem by mortgaging various underlying LST LST pools or native pledge ETH (via EigenPods).In terms of procedure, the verifications point their withdrawal address to EIGENPODS to obtain EIGEN points. These points will be exchanged for protocol rewards in the future.LST (1.5 million ETH) in EIGENLAYER accounts for about 15%of all LST, and the total amount of ETH locked in Eigenlayer occupies nearly 10%(3m, a total of 31.3 million ETH) of all ETHs pledged.(LST itself accounts for 43%of all pledged ETH in the ecosystem.) In fact, we believe that after the pledge demand has stabilized after October 2023, the recent interest in new authenticists is caused by re -pledge.In February 2024, more than 2 million ETHs were betted at the same time as the upper limit of the EIGENLAYER deposit was suspended at the same time.In fact, some LST providers are raising their target APY as a way to attract new users to use their own platform with their own interest.

>

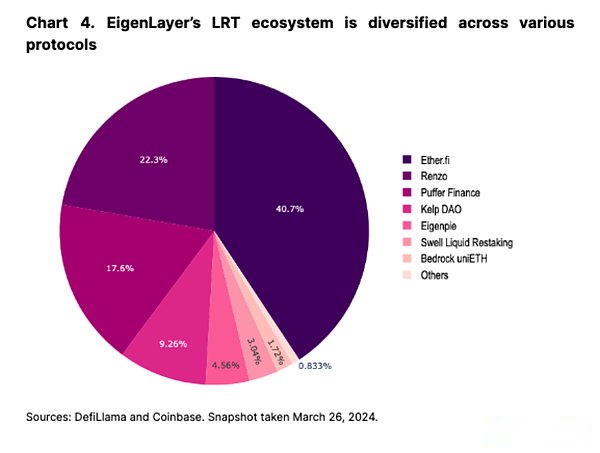

Drawing on the popularity of LST, the rich LRT ecosystem has developed, and more than six protocols provide a liquidity of the liquidity of various points and airdrop schemes to reintegrate to the token version.About 2.1 million (62%) of the 3M ETH protected in Eigenlayer was encapsulated in the secondary agreement.We have seen similar models in the liquid pledge market and believe that with the development of the industry, the diversification of alternatives will be very important.

>

In the long run, if the volume of native pledge issuance decreases due to the increase in pledge participation (with the addition of more verifications, the yield will be reduced), re -pledge may become an increasingly important way for ETH yields.A separate discussion of reducing the separation of ETH emissions in this pledge may further improve the correlation of re -pledge yields (although this is still in the early stage of the discussion stage).

Nevertheless, the AVS yield is expected to be relatively low after launch, which may challenge the light rail in the short term.For example, the largest light rail Ether.Fi charges 2% annualized platform fee for its TVL for its “vault management”.However, not all light rails have the same charging structure, so there is room for competition in this regard.However, if we use these 2% of the cost as the standard for calculating the cost of profit and loss, AVS will need to pay about 200 million US dollars (based on $ 12.4B for re -mortgaging value) for EIGENLAYER’s security services every year to achieve profit and loss -moreThe cost is more in the past year.This raises a question: how much AVS needs to generate a business to increase the overall income of ETH pledges.

The emergence of active verification services

To this day, any AVS has not been launched on the main network.The first AVS (early 2024) will be EIGENDA. This is a data availability layer that can play a similar role in storing the BLOB storage of Celestia or Ethereum.Following the success of the DENCUN upgrade to reduce the cost of the second level (L2) of more than 90%, we believe that EIGENDA will become another tool in the modular tool library, which can achieve cheaper L2 transactions.However, building or migrating L2 to use EIGENDA is a slow process. It may take several months to bring meaningful income to the agreement.

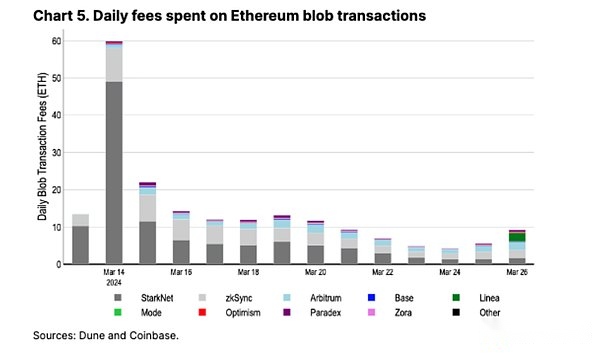

In order to estimate the initial income of EIGENDA, we can compare with the Ethereum BLOB storage cost.At present, about 10 ETH is used for many major L2 BLOB transactions per day, including Arbitrum, Optimism, Base, ZKSYNC, and Starknet (see Figure 5).If EIGENDA sees a similar level of use, according to our conservative estimates, the annualization rate of re -mortgaging rewards each year is about 3.5K ETH, which is equivalent to about 0.1%of the additional rewards.We believe that although additional AVS may increase income rapidly, the cost of the previous few months may be lower than expected.

>

Other AVs built in the EIGENLAYER ecosystem include interoperability networks, fast final layers, position certification mechanisms, COSMOS chain security guidance procedures, etc.The opportunity space for AVS is extremely extensive and growing.Restakers can choose to choose which AVS they want to use ETH mortgage products, although this process becomes more and more complicated for each new AVS.

This raises a question: how to deal with different LRTs (1) AVS selection, (2) potential reduction and (3) final token finance.In the traditional pledge, the one -to -one mapping between the verifier’s responsibility and the income is clear. Considering all the factors, LST becomes a relatively simple thing.However, through the re -pledge, the more unusual complexity (and the diversity of LRT issuers) of how to accumulate and distribute income (and loss).LRT not only pays basic ETH pledge rewards, but also pays a set of AVS rewards.This also means that the potential returns paid by different light rail issuers will be different. At present, many light rail modes have not been completely clear.However, because each project has only one LRT, all toke holders in the given protocol may be unified by AVS incentives and cut conditions.The design of these mechanisms may vary from light rail providers. A suggestion is to adopt a layered method. Light rail issuers can adopt a series of AVS of “high” and “low” risks, although this requires the establishment of unfarished risk standards.In addition, according to architecture design, the final reward of tokens may still pay the sum of all AVS, and we believe that this violates the purpose of the risk -stratified framework.Alternatively, decentralized autonomous organizations (DAO) can decide which AVS selection, but this triggers whose key decision makers in these DAOs.Otherwise, LRT providers can act as the EIGENLAYER interface and allow users to retain which AVS decision -making power is used. However, when released, the re -mortgage process should be relatively simple for operators, because EIGENDA will be the only AVS that needs to be protected.However, one feature of Eigenlayer is that investing in an AVS ETH can be further put into other AVS.Although this can increase income, it will also exacerbate risks.When the layered structure involving the reduction between the services and the claims conditions, the same re -pledged ETH to multiple AVS will bring challenges.Each service will create its own custom reduction conditions, so such a situation may occur: one AVS cuts the re -pledged ETH due to improper behavior, and the other AVS hopes to recover the same re -pledged ETH as the right to suffer.Compensation from participants.This may lead to a final cut -off conflict, although as mentioned earlier, EIGENDA will not have cutting conditions at the first start. What makes this setting further complicated is Eigenlayer’s “pool security” model (where AVS uses the pledged ETH public pool to protect its services) can be further customized through “belonging security”.In other words, each AVS can be obtained (extra) of ETH, which is only used to ensure the safety of its specific services -this is a kind of insurance or security network form for AVS payment premium.Therefore, with the launch of more AVS, the role of operators has become more complicated in technology, and the reduction of rules has become more difficult to follow.In addition to the complexity of the LRT expansion, many potential strategies and risks have been abstracted from the token holders. This is a problem because we think that people will eventually go to these light rail providers with the highest returns.Therefore, light rails may be motivated to maximize their yields to obtain market share, but this may be at the cost of higher (although it is hidden) risk.In other words, what we think is the return of risk adjustment, not an absolute return, but it may be difficult to maintain transparency in this regard.This may lead to additional risks, because LRT DAO will be motivated to maximize the mortgage to maintain competitiveness to the greatest extent. In addition, if LRT expenditure is completely carried out in ETH, LRT may also cause downward selling pressure on non -ETH AVS rewards.In other words, if LRT needs to convert the native AVS token to ETH (or ETH equivalent) to re -assign rewards to LRT token holders, the value of re -mortgage may be limited by repeated selling pressure. In addition, light rails also have valuation risks that cannot be ignored.For example, if the pledge withdrawal queue is extended (Ethereum is reduced from 14 to 8), LRT may temporarily deviate from its basic value.If LRT becomes widely accepted in DEFI (such as LST in the borrowing agreement), this may accidentally exacerbate the liquidation, especially in the low liquid market. This is assuming that these DEFI protocols can first correctly evaluate the mortgage value of LRT.In fact, LRT represents different investment portfolios, and the risk status of these shares may change over time.You can add or delete new constituent stocks, or the risk of income or solvency of AVS itself may change.Assuming, we may see such a situation: market downturn may affect multiple AVS at the same time, thereby destroying the stability of LRT and amplifying the risk of mandatory liquidation and market fluctuations.Recursive lending will only enlarge these losses.On the other hand, agreements that can decompose LRT into its principle and income component can help reduce this risk to a certain extent. Finally, as Ethereum co -founder Vitalik Buterin emphasized, in some cases, major faults in the re -mortgage mechanism may threaten the underlying consensus agreement of Ethereum.If the number of ETH pledged ETH is large enough compared to all pledged ETH, there may be economic incentives to enforce errors that may lead to unstable network. The re -mortgage protocol of Eigenlayer is expected to become the cornerstone of various new services and middleware on Ethereum, which in turn can generate meaningful ETH reward sources for verifications in the future.The AVS from EIGENDA to Lagrange can also greatly enrich the Ethereum ecosystem itself. In other words, the use of an LRT packaging device around the underlying protocol may cause hidden risks due to opaque re -assigning strategies or temporary dislocation of the underlying protocol.How to choose the AVS they want to protect and allocate risks and rewards to LRT holders are still an unspeakable issue.In addition, the initial yield of AVS may not reach extremely high expectations of market settings, but we expect that as the AVS adoption rate increases, this situation will change over time.Nevertheless, we believe that the re -mortgage supports the open innovation of Ethereum and will become the core part of the ecosystem infrastructure.Potential question

New risk

in conclusion