Author: Jupiter Zheng, Partner, HashKey Capital Secondary Fund

On May 24, the U.S. Securities and Exchange Commission (SEC) formally approved 8 Ethereum Spot ETF Form 19b-4,

This means that the regulatory authorities’ position has changed from tough to softening. The US Ethereum spot ETF seems to be just one step away from the final launch. Market sentiment has also been ignited recently, and the secondary market is even more ignited.

At the same time, in sharp contrast, it was “first to eat” as early as April 30, and launched six Hong Kong crypto asset ETFs covering Bitcoin and Ethereum, which has seemed quite lonely in the past month., and even suffered criticism for its “unsatisfactory” market data performance.

The market always likes to overestimate the short-term effects of new things and underestimate their long-term influence. This article aims to clarify how Hong Kong crypto ETFs have performed in the past month?What are the incentives behind it, and what variables the market ignores, and what paths may it take next?

“Downturn” and variables in the data

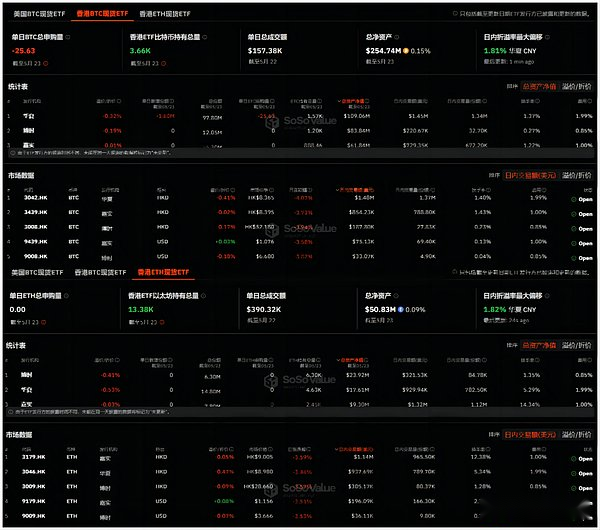

On April 30, Bose HashKey Bitcoin ETF (3008.HK), Bose HashKey Ethereum ETF (3009.HK), Huaxia Bitcoin ETF (3042.HK), Huaxia Ethereum ETF (3046.HK), and Jiashi BitcoinSpot ETF (3439.HK) and CATL Ethereum Spot ETF (3179.HK) are officially ringing the bell and listed on the Hong Kong Stock Exchange and trading is open.

If we look at the opening data,The issuance scale of 3 Bitcoin spot ETFs reached US$248 million on the first day of April 30 (Ethereum spot ETF was US$45 million), which actually far exceeded the first launch of US Bitcoin spot ETFs of approximately US$125 million on January 10.Scale (excluding Grayscale), which also shows that the market expects high subsequent performance of Hong Kong crypto ETFs.

The market’s criticism of these six Hong Kong crypto ETFs is mainly concentrated on its “sluggish” trading volume compared to US crypto ETFs: on the first day of listing, the total trading volume of the six Hong Kong crypto ETFs was HK$87.58 million (about 11.2 million)), of which three Bitcoin ETFs had trading volumes of HK$67.5 million, which is less than 1% of the total trading volume of US Bitcoin spot ETFs on the first day (US$4.6 billion).

The transaction volume then fell all the way, and it even fell below $1 million on May 23.

However, it is worth noting that the transaction volume of Hong Kong crypto ETFs shows a clear inverted trend with the asset management scale: as of May 23, 2024, the total asset management scale of 6 Hong Kong virtual asset spot ETFs exceeded US$300 million.Among them, the total holding of Bitcoin spot ETF is 3,660 BTC, with a total net assets of US$254 million; the total holding of Ethereum spot ETF is 13,380 ETH, with a total net assets of US$50.83 million, a small percentage compared with the first day.Slightly increased.

Although the scale of US$250 million is still far inferior to the US Bitcoin spot ETF of about US$57.3 billion, this actually ignores the objective “pool size of the Hong Kong ETF market and the US ETF market”.Difference”—The total volume of the Hong Kong ETF market is only US$50 billion, while the size of the US ETF market is as high as US$8.5 trillion, a difference of about 170 times.

Therefore, from the perspective of relative proportion,The 250 million Bitcoin spot ETF accounts for 0.5% of the Hong Kong ETF market, while the 57.3 billion US dollars accounts for 0.67% of the US ETF market. There is actually no order of magnitude gap between the two., at the same time, this is still a performance of less than a month of launch, which also indirectly shows that Hong Kong’s crypto ETF has also had a huge impact on Hong Kong’s local financial market.

If you look closely at the changes in internal data of Hong Kong crypto ETFs in the past month, the three companies, Huaxia, Jiashishi and Boshi HashKey, have also shown a trend of one increase and another decrease:

The BTC and ETH positions of Huaxia and Jiashi have both declined significantly, while Boshi HashKey’s latecomer momentum is still good, with a total asset management scale exceeding US$100 million, exceeding 33% of the total, an increase of US$30 million from the first day – currently BoshiHashKey has the highest ETH position, while BTC is second only to China, and the gap has quickly narrowed from the initial thousand to less than 500.

“Sweet Troubles” behind the unexpected approval

Data will not lie. Behind the inverted trading volume and scale trend of Hong Kong crypto ETFs, it actually reflects a “structural” undercurrent – the multi-faceted stakeholder polishing process and clearing bottlenecks.

If you look back at the pace of Hong Kong regulators’ approval and launching 6 crypto ETFs in one go, you will find that the most important market feedback is “reasonable, unexpected”:

-

It is reasonable that since the Hong Kong government has embraced virtual assets and Web3 in 2022, a series of relevant policies and regulatory frameworks have been steadily advancing, including the crypto asset ETFs that everyone is looking forward to.All stakeholders have long begun to prepare;

-

Unexpectedly, the judgments made by all parties about ETFs are mostly concentrated in the third quarter or the second half of the year, so they have been gradually polishing the operational process and technical docking issues, but the Hong Kong government unexpectedly accelerated in April.The approval progress greatly exceeded market expectations, which forced all parties to focus on material declaration and other work.The original deployment plan is not suitable.

In short, this leads to stakeholdersThe application work is in advance, and the problems of operation, channel, product and other dimensions that were originally planned to be carefully polished have not been completely solved, so they can only be put to the ETF for “make-up lessons” after it is launched., thus causing some obvious “sweet troubles”.

Here we have to mention the physical redemption model pioneered by Hong Kong cryptocurrency ETFs (i.e., redemption for holding coins), allowing investors to directly subscribe to ETF shares using Bitcoin and Ethereum – investors can directly hold BTC and ETH to subscribe to ETF shares., supports cash redemption, and at the same time, the share of cash subscription ETFs also supports BTC and ETH redemption.Taking the 3008.HK and 3009.HK issued by Bose HashKey as an example, each share of 3008 corresponds to 1/10,000 BTC, and each share of 3009 corresponds to 1/1,000 ETH.

Participated securities companies: China Merchants Securities International, Mirae Asset Securities, Victory Securities, Ed Securities

Market Makers: Eclipse Options (HK) Limited, Jane Street Asia Trading Limited, Optive Trading Hong Kong Limited, Vivienne Court Trading Pty. Ltd.

The advantage of this innovative mechanism is to help investors realize the two-way circulation of virtual assets and traditional assets, but also involves multiple stakeholders:

-

Participating Trader (PD) is an institution selected by the ETF issuer (Boshi HashKey, Huaxia, Jiashi) and assumes the responsibility of adding new ETF units in the primary market. Currently, there are Shengli Securities, China Merchants Securities International, Shengli Securities, and Huaying Securitieswait;

-

Brokerages are the main channel for investors to trade ETF secondary markets. Investors can buy and sell ETF shares like stock trading through brokerage accounts;

-

The custodian is responsible for custodial crypto assets corresponding to the ETF and ensure the security of the assets;

-

Market maker, providing ETF market maker services, and is responsible for buying and selling ETF shares in the secondary market to ensure market liquidity;

Therefore, it is necessary to participate in the running-in between different institutions such as traders (PD), securities firms, custodians/exchanges, and market makers to cooperate to open up the bottlenecks in the entire trading chain.

That is, the docking efficiency of each link has become a major problem that all parties need to solve after the ETF goes online. The above picture shows the coin subscription of HashKey encryption ETF as an example:

-

Investors needOpen an account on the PD first;

-

Then within the specified timeSubmit ETF share creation directive;

-

Send coins to PD again, and the coins will beHosting to HashKey Hosting Servicemiddle;

-

ThenETF share created by Hong Kong Central Computing Institute,andSend to PDWhere, againGive it to the broker through PD;

-

And it will be necessary to followOrdinary investors trade in brokerage firms;

This involves investor KYC information docking during the opening of a PD/broker account, subscription and creation share in the primary market, docking between PD and custodian, docking between PD and broker, etc., which are also the main points of current card points.Therefore, many funds, especially the primary market funds, are still waiting and watching, which can easily lead to a vicious cycle of negative feedback, namely, the sluggish trading volume → the slow entry of arbitrage institutions → the continuous sluggish trading volume.

However, everything is slowly being resolved, and the changing trend of asset management scale in the past month is a clear example.

Encrypted ETFs may still take 2 months to ferment

Therefore, from this perspective, the actual performance of Hong Kong crypto ETFs still needs time to ferment. If the estimate is based on the current actual situation,It is expected that it will take at least 1-2 months to polish and streamline the details of relevant operational processes, channels, technical connections and other aspects.

Then let’s look forward to what changes are worth looking forward to in 2 months?

First of all, with the optimization of operational processes, technical docking, etc., more and more PD, securities and other roles enter the market, their original customer base will naturally become a seed pool for incremental users, achieving coverage of users andThe scale of reaching funds will undoubtedly greatly expand the future imagination of Hong Kong’s crypto ETFs.

At the same time, two months later, traditional financial institutions that are now staying on the sidelines and need more time to evaluate,It can also launch more derivative products such as leverage, lending, asset management and other products based on ETF products to achieve financial innovations that were difficult to directly use bitcoin physical assets to complete the implementation, and meet the needs of various investors to layout crypto assets..

The two can also promote each other to form a positive feedback path – the access of more PD, brokerage firms and more users will further promote more financial innovations in encrypted ETFs, and various structural products based on spot ETFs andDerivatives will also bring more possibilities to the Hong Kong market and achieve a virtuous cycle.

At the same time, there is another new biggest variable worth paying special attention to – for institutions, Hong Kong Ethereum spot ETF has become a time window to “take the lead” of the US ETF.

The reason is that although the US SEC has approved 8 Ethereum spot ETFs 19b-4 forms, it is still in the waiting stage for “the boots to finally land”. The market generally expects that it will take at least 1-2 months before it is officially launched..

ThatDuring this window period, you are interested in Ethereum spot ETF, especially if you want to ambush the next incremental capital entry and ETH rises on a large scale, you can use the Hong Kong ETF, a safe and compliant cheap channel.Other players achieve “snatch”, take the lead in laying out this almost obvious alpha opportunity.

summary

In “Waiting for Godot”, Godot symbolizes hope and a bright future. For today’s Hong Kong crypto ETF, Godot is the running-in and optimization of the entire transaction process between different institutions.

Behind the inverted trading volume and scale trends, the multi-faceted stakeholders are polishing the process and clearing the bottlenecks. In 2 months, it may be the key node for Hong Kong ETFs to start volume and usher in a real opening.