Author: Bing Ventures Source: Medium Translation: Shan Ouba, Bitchain Vision Realm

With the maturity of the cryptocurrency market, GMXV2, Vertex Protocol, Hyperliquid, Apex Protocol and other derived derivative exchanges have gradually attracted attention.These platforms not only challenge the leadership of GMX, but also indicate major changes in the field of decentralized finance (DEFI).This article discusses the changes in the competition pattern of decentralized derivative market after the GMX V2 is upgraded, and predicts the main trend of the future.

Decentralization derivative market size

>

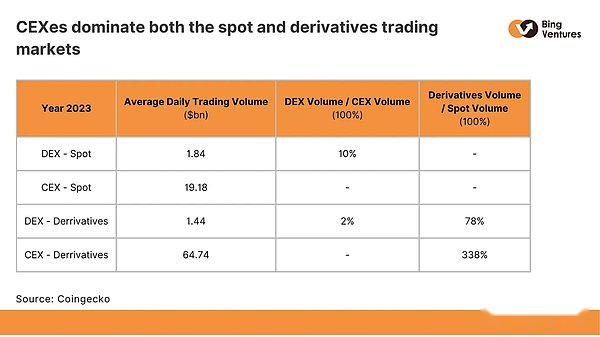

Source: Coingecko

The above table shows the average trading volume of the spot and derivatives of the decentralized exchanges (DEX) and the centralized exchange (CEX).DEX’s daily spot trading volume was 1.84 billion US dollars, and derivatives’ transaction volume decreased slightly to 1.44 billion US dollars.For the Central Exchange, the daily spot transaction volume is 19.18 billion US dollars, and the daily derivative transaction volume is US $ 64.78 billion.

The transaction volume of CEX in these two categories makes DEX’s transaction volume dwarfin.This leading advantage is the most obvious in derivatives.Although the FTX incident occurred and the subsequent series of centralized banks declined, it seemed that CEX was the primary choice for users after all.In addition, compared with the spot transaction volume, the derivatives of the Central Exchange are much larger, highlighting the popularity of its derivative products.

>

GMX V2 and its competitors

GMX v2: disruptive newcomer

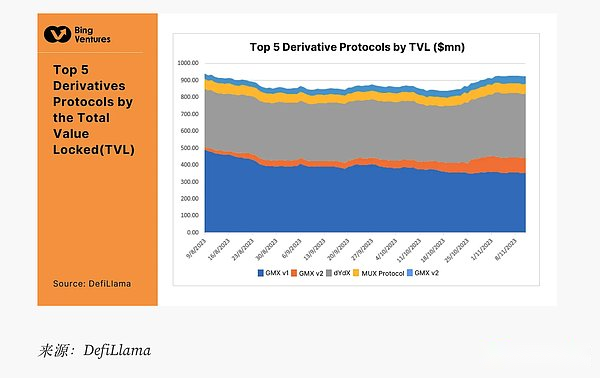

We have analyzed the market evolution since the official release of GMX V2.In the early days, the market was still led by GMX V1 and Dydx. Mux Protocol and Apex Protocol were far behind in total value lock (TVL), and GMX V2 only occupied a small market share.As of November 5, 2023, in just four months, GMX V2 had tied or even surpassed MUX Protocol and Apex Protocol (GMX V2: 89.72 million US dollars; MUX Protocol: $ 57.71 million; APEX Protocol:45.51 million US dollars).In addition, with the growth of GMX V2, the TVL of GMX V1 has declined.We think this is because users move from V1 to V2, because the latter fixes many defects of V1.

>

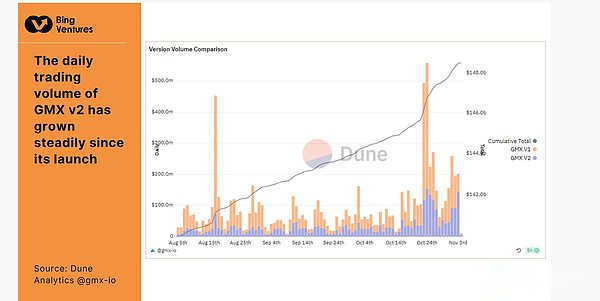

GMX V2 has steadily increased since its launch, reflecting the market’s good response to upgrades.The GMX V2’s TVL growth relative to GMX V1 shows that the upgrade is successful.In particular, the transaction efficiency has been improved and the user costs are reduced.As a result, GMX V2 not only attracted new users, but also won the GMX V1 users.However, while maintaining the stability and security of the platform, maintaining this growth and attractiveness will be challenging.This will determine the future of GMX V2.

>

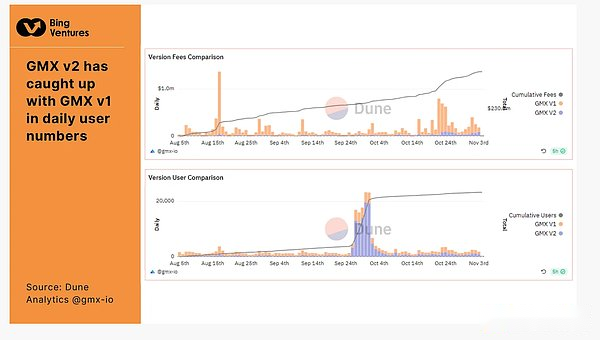

As can be seen from the figure above, the average daily user number of GMX V2 has caught up with V1.However, for V2, the source of user growth is more diversified. Because of its successful marketing and user education, it has also attracted new users.From the perspective of fees, the daily cost of V1 is still higher than V2, reflecting their different cost structures.User growth reflects the market’s recognition of the user experience and transaction efficiency of the GMX V2.How to convert new users into long -term users will be the primary problem of GMX V2.We believe that GMX V2 should give priority to continuously improving user experience and community participation to consolidate its market position.

The cost structure of GMX V2 has been adjusted to balance short and multi -heads to improve capital efficiency.Main adjustments include:

-

Reducing the cost of opening/liquidation: The cost of 0.1%of the warehouse and the warehouse of the position has been reduced to 0.05%or 0.07%, specifically depending on whether the transaction increases the bulls and short balances.If so, it is applicable to lower costs.Otherwise, the cost is 0.07%.

-

Introduction of funding fees: In the balance of power and short power, the strong one -sided one -side party pays funds.This funding rate is not fixed, but gradually adjusted according to the long -term proportion over time.For example, if the total amount of multi -position holding positions is greater than the short position, the rate of funds paid to the short -to -short payment will gradually increase, until the difference between the long and short positions is lower than the certain threshold or reaches the upper limit. At this time, the capital rate will remain unchanged.vice versa.This adaptive interest rate mechanism helps to increase arbitrage opportunities and attract arbitrage capital, thereby promoting the balance of market forces.

All in all, we believe that the primary challenge facing GMX V2 is to maintain growth and ensure the stability and growth of the platform.In the field of DEFI, security events are frequent.GMX V2 must ensure that such risks will not affect it.Another challenge is how to maintain an advantage in the fierce competition market, especially in the face of the competition of new agreements.GMX V2 needs to continue to innovate to maintain its attractiveness of its products and services.In the end, the success of GMX V2 depends on how it balances growth and stability, innovation and security.

>

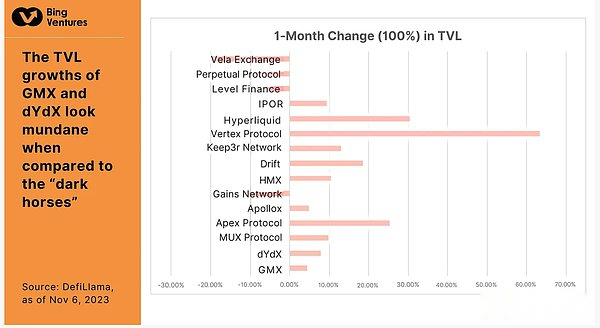

At the same time, we compared the monthly TVL change of 15 derivatives agreements by November 6, 2023.Compared with dark horses such as Vertex Protocol, Hyperliquid and Apex Protocol, GMX and DYDX TVL growth looks plain and indifferent. The latter’s TVL growth is 63.22%and 30.69%.TVL increased by % and 25.49 %, respectively.We will study them one by one in the following paragraphs to find the motivation and narrative to promote their growth.

Vertex Protocol: Getting a competitive advantage through low -cost operations

Vertex Protocol is a decentralized exchange, which has the characteristics of spot, sustainability and comprehensive currency market.The agreement uniquely combines a centralized price limit order book (CLOB) with automatic city merchants (AMM) to enhance liquidity and change user transaction experience.

The Vertex protocol is based on the Arbitrum Layer 2 (L2), which aims to reduce GAS costs and fight against miners to extract value (MEV) to promote high -efficiency and economical efficient transactions in decentralized space.The protocol contains three key pillars: under the chain sorter, AMM on the chain, and a powerful chain risk engine.The order book and AMM accumulate the liquidity of the contributors on the API as a city merchant and chain.The risk engine guarantees rapid liquidation, and the source of dual liquidity allows traders to get better prices.The growing transaction volume on Vertex proves the success of this unique model.

Vertex Protocol’s full -position margin system is friendly to experienced traders and novice traders, and significantly reduces the margin requirements.For example, the cumulative margin requirement of a VerteX trader with a $ ETH spot margin and a short -term permanent contract of $ ETH may be lower than traders who have the same position in the positioning margin account.By introducing the concept of investment portfolio margin, the system enables traders to adjust the leverage of their position across multiple positions to adapt to their personal risk preferences.If the value of the multi -headed $ ETH spot margin position falls, the excess margin (e.g., without profit) in the short $ ETH sustainable position can be used to maintain the required margin level and avoid liquidation of the poly head margin.Vertex’s method has maximized capital efficiency.

Project performance

>

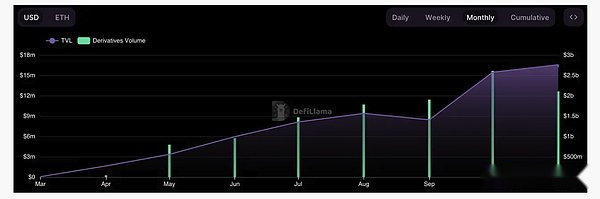

As shown in the figure above, the TVL and derivatives of the vertex protocol have been showing a stable upward trend since the establishment of the TVL and derivatives.

Total lock value

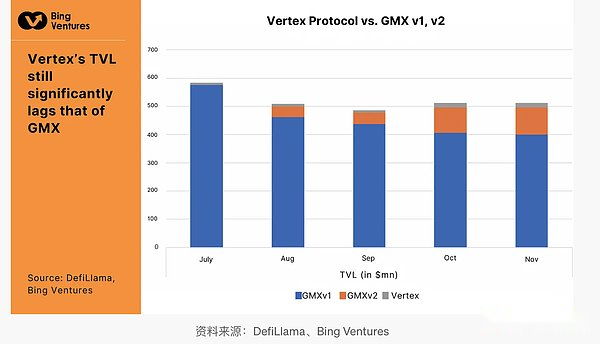

Although Vertex provides an innovative trading experience, its TVL still lags behind GMX.This is mainly because its currency market function is still underdeveloped.Only support for 5 major assets including WBTC, WETC, USDC.This limits its ability to obtain more locking value.In addition, as of writing this article, its native currency VRTX has not been launched.This means that users cannot participate in the agreement by mortgage VRTX.

>

>

Derivative

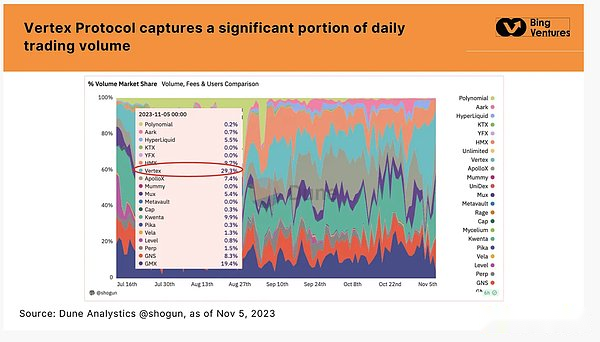

In the field of competitive DEX, Vertex Protocol accounts for a large part of the daily transaction volume, ranging from 15% to 30%.This excellent performance is very prominent even compared with industry giants such as GMX, Gains, Kwenta.Especially compared to GMX, VerteX’s transaction volume is significantly higher.As an emerging project, its transaction volume surpasses existing participants in such a short period of time, proving that its unique design is attractive to users.

>

>

Cost and income

>

>

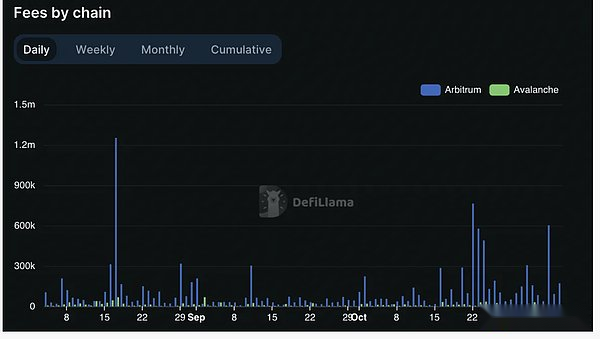

The cost of the vertex protocol; Source: DEFILLAMA

The transaction fee charged by GMX is higher than Vertex.Vertex Protocol implements a zero-cost policy for the market, and provides extremely low costs for the recipients of the main transaction pair (the stable currency pairs are 2 basis points, the core market is 2-3 basis points, and the non-core market is 4 basis points)EssenceIn contrast, the GMX V1 charges 0.1% of the open warehouse (drop to 0.05% or 0.07% in V2). If the transaction involves an exchange, it will charge 0.2% to 0.8% of additional costs.This cost structure advantage makes Vertex Protocol more attractive to users. Although its low rates may lead to less significant income growth, although compared with the growth of transaction volume.

We believe that Vertex Protocol has quickly established a foothold in the market by providing a highly competitive low -cost structure.This low -cost strategy has attracted a large number of traders who pay attention to costs, especially in the current market conditions, users are increasingly concerned about transaction costs.However, in the long run, this strategy may face profitable challenges, especially in maintaining high -quality services and platform operations.

Therefore, the vertex agreement needs to explore additional value -added services and income models, while continuing to attract users with low costs to ensure long -term sustainable development.Although the daily trading cost of GMX was significantly higher before, it has recently dropped to about $ 100,000, which is roughly the same as Vertex Protocol.Combined with Vertex Protocol’s stable growth transaction volume, it is expected that its future revenue will have the potential to surpass GMX.

Hyperliquid: The full chain of the L1 is on the order book DEX

Hyperliquid is a permanent futures decentralization exchange based on an order book.It runs on the Hyperliquid chain, which is a Layer1 based on Tendermint.One key reason for the rapid growth of hyperliquid is that it exists on its own Layer1.This allows the Hyperliquid team to flexibly adjust GAS fees, MEV, slide points, etc. to achieve the fastest and most efficient trading experience, so that the platform can support up to 20,000 orders per second.

Running on its Layer1 also enables it to build an order book on a complete chain, and each execution transaction is completely transparent, which is very needed in the market after the FTX incident.Hyperliquid L1 makes it possible to build everything as chain, decentralization, decentralization, and license.

>

On Hyperliquid, Vaults provides liquidity for various trading strategies.They can be managed by individual traders or automation by business business.Anyone can deposit in the vault to earn profits: DAO, agreement, institution or individual.As a exchange, the vault owner obtained 10%of the total profit.

Hyperliquid is also the first company to launch an index perpetual contract for Friend.tech.At first, this was based on TVL, but considering that OI continued to grow, the definition of TVL may be manipulated. After this result was clarified, it was changed to the median price of a set of static 20 top subjects.

Project performance

>

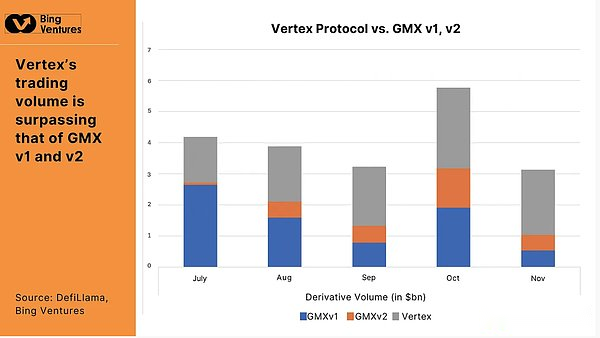

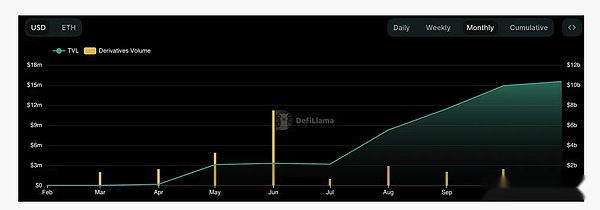

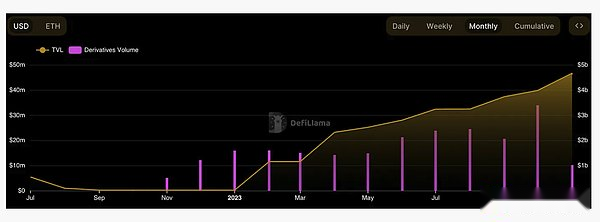

Like Vertex, the TVL of the protocol has been steadily increasing since its launch, and the monthly derivative transaction volume reached about $ 1.5 billion after reaching a peak of $ 8 billion.However, on average, Vertex Protocol still maintains a competitive advantage.

Total lock value

>

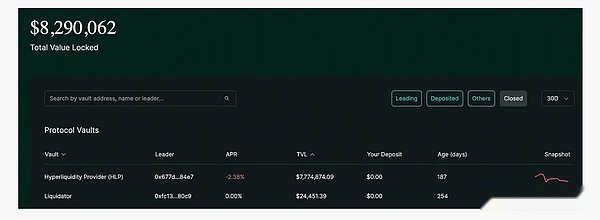

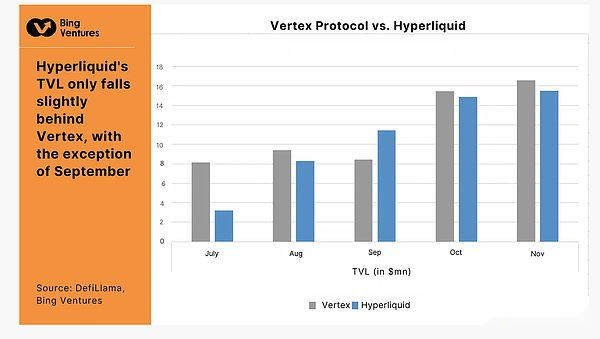

In terms of TVL, Hyperliquid still cannot be compared with GMX.But compared with the Vertex Protocol at the same time, Hyperliquid’s TVL is only slightly backward, only in September more than Vertex.We believe that its lower TVL is mainly due to its restrictions on pledge and deposit functions.The project locks funds through Vaults, and people deposit funds into Vaults to obtain profit sharing.However, there is an inherent risk of this way to trading, because profit and losses depend on the transaction skills of the vault owner.Therefore, these functions have insufficient guarantee to investors and have low attractiveness.

>

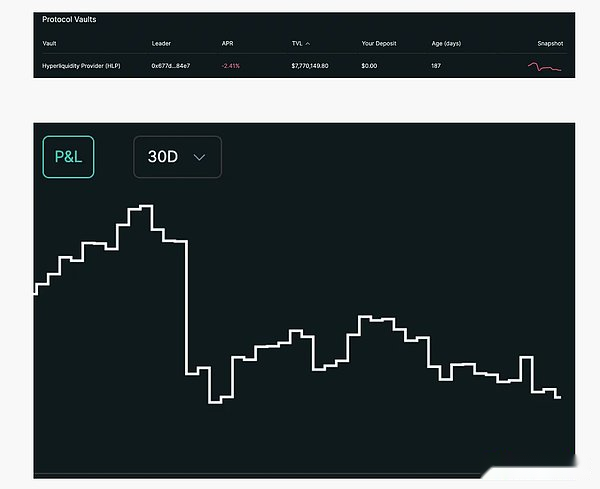

For example, the above figure shows the performance of Hyperliquidity Provider (HLP), which is a protocol vault for the market and liquidation and collecting some transaction costs.We can see that the return on investment is negative (-2.41%), and the profit and loss ratio continues to decline, which indicates that users may have a better choice than depositing funds into Vaults.

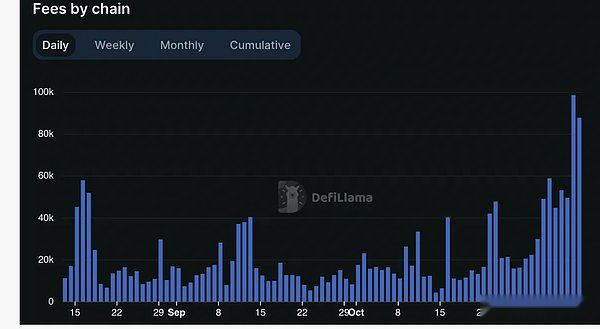

Derivative

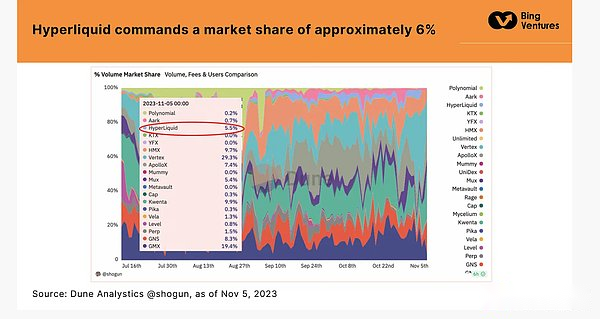

>

Source: Dune Analytic @Shogun, as of November 5, 2023

Hyperliquid occupies about 6% of the market share.Although it cannot be compared with the Vertex protocol, it is still an impressive percentage for the new agreement.However, the transaction volume in the past month has declined and failed to maintain the previous activity level.

Cost and income

The cost structure of hyperliquid is as follows:

-

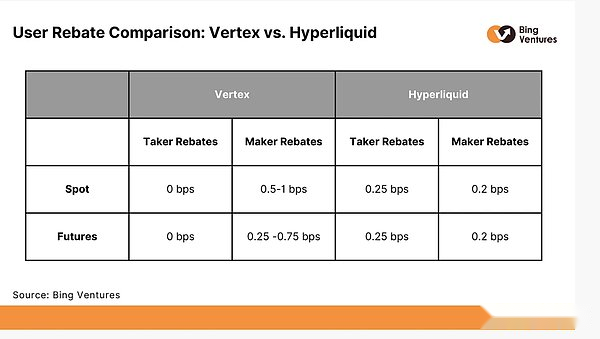

The recipient pays a fixed fee of 2.5 basis points, while the city merchants get 0.2 basis points.The recommender received 10%(0.25 basis points) of the recipient of the recommended user.The remaining expense income (about 2.05 basis points) belong to insurance funds and HLP.

-

Unlike Vertex, most of Vertex’s costs are borne by team or internal tokens, and in Hyperliquid, the cost is directly distributed to the community: 40% belongs to the insurance fund, and 60% belong to HLP.

>

Hyperliquid’s cost structure emphasizes the feedback community.In contrast, Vertex Protocol provides zero costs for traders of the main transaction pair, providing a very low cost to the recipient.It uses part of the transaction fee to support its vault and liquidity provider.This difference shows that Hyperliquid tends to reward community members who directly support network operations and risk management.

APEX protocol: multi -chain DEX supported by ZK Rollups

APEX Pro is the latest product of APEX Protocol. The second -layer scalability engine Starkex based on Starkware is constructed and runs on the order book model. It can provide a perpetual contract for peripheral deposit and provide a safe, efficient and user -friendly user experience.It is non -hosted, which means that traders’ assets are completely on the chain and can only be accessed by them with private keys.Use zero -knowledge summary expansion solutions help APEX to improve transaction security and protect user privacy.Compared with similar products such as DYDX and GMX, it provides more favorable transaction costs.The pledge and repurchase reward mechanism and recommendation plan have also increased its appeal.

The main attraction of the APEX pledge plan includes:

-

No fixed clauses or plans.Users can start and lift the pledge at any time. The longer the pledge period, the greater the return.

-

The pledge reward not only considers your pledged assets, but also your transaction activities, and consider the transaction of additional income to earn (T2E) activity scores.

Project performance

>

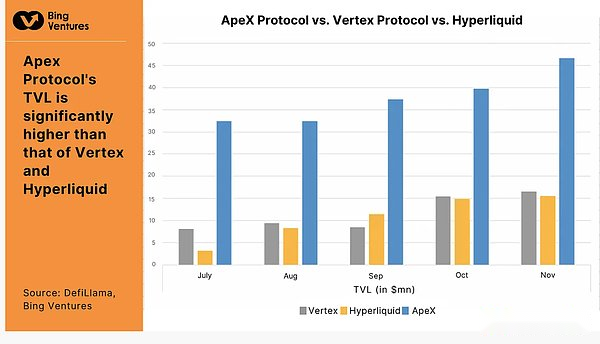

Apex Protocol’s TVL is also steadily rising.Its monthly derivatives have stabilized by about 1.7 billion, similar to the first two protocols.

Total lock value

>

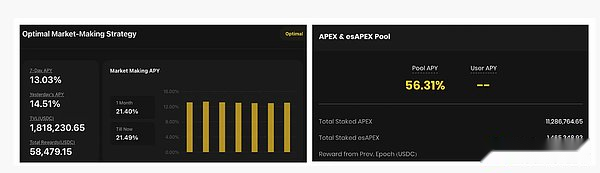

Apex Protocol’s TVL is significantly higher than the previous two.Its two -income function, the intelligent liquidity pool and the pledge pool of APEX are the main contributors of its high TVL.The past enthusiasm for participation was high.The annual yield (APY) of the pledged pool reached 56.31%, and the intelligent liquidity pool also provided users with liquidity to provide liquidity with a 7 -day yield of 13.03%.

>

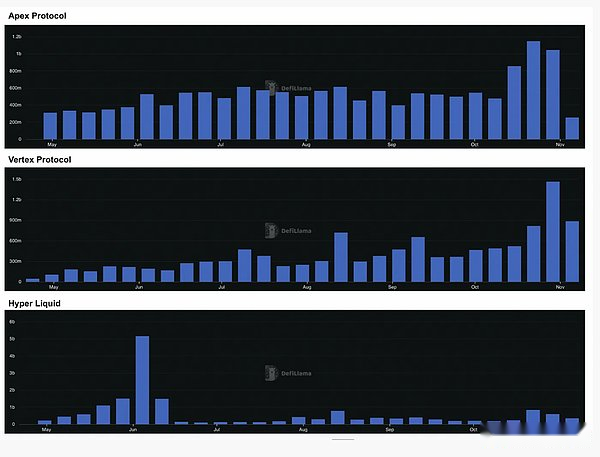

Derivative

>

Compared with the other two protocols, the growth trajectory of APEX Protocol’s transaction volume is more stable, indicating that the user base and user participation have steadily increased.

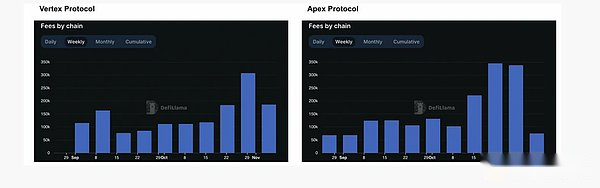

Cost and income

>

APEX’s transaction cost growth trend is similar to Vertex.We believe that Hyperliquid and Apex Protocol both establish their market position by focusing on the niche segment and user group, which enables them to more effectively meet the unique needs of these markets.Hyperliquid is famous for its innovative full chain order book, while Apex Protocol has been recognized by its multi -chain support and efficient transaction execution.

Overall comparison

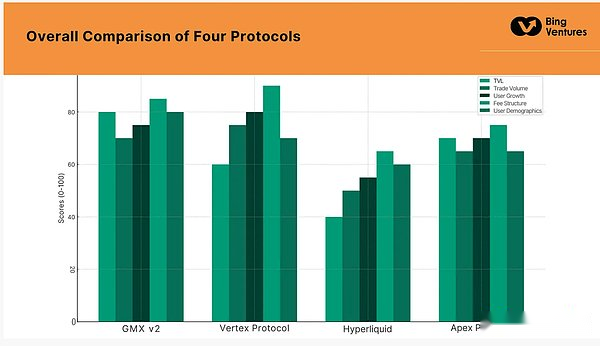

According to existing data, we scores all four protocols (GMX V2, Vertex protocol, Hyperliquid and Apex protocols) in terms of TVL, transaction volume, user growth, cost structure, user population statistics, etc.Advantages and risk tolerance.Some results showed below.

>

As an existing market leader, the GMX V2 scores high on multiple indicators, especially TVL and transaction volume.Innovative ability, user experience, and community participation are also excellent.However, regulatory compliance may be an area where it can work hard.

Xiangfeng has a significant lead in the charging structure, which is its core competitiveness.Although TVL and transaction volume are slightly lower than that of GMX V2, it has huge potential in terms of user growth and community participation.

As a newer platform, Hyperliquid’s score on all indicators is low, reflecting the challenges facing emerging platforms.However, it has the potential to catch up in terms of security and user experience.

The score of APEX is similar to Vertex on several indicators.However, it is slightly better than Vertex in terms of user experience and community participation.

Future trend of decentralized derivatives market

In summary, the position of GMX in the derivative derivative trading market is indeed challenged by the emerging agreement, especially Vertex Protocol.With the advantages of its charging structure, Vertex has begun to occupy more market share.This competitive pattern highlights that even in this relatively mature market, innovative and humanized pricing strategies are still an effective means to attract users and increase market share.

As far as TVL is concerned, emerging projects cannot be compared with GMX.This reflects that users are still cautious about depositing a large amount of assets into the new platform.The reason for this phenomenon may be that users lack trust in new platforms, imperfect product functions, or insufficient market awareness.Therefore, for these emerging agreements, attracting user funds and increasing TVL will be a major challenge.

In addition to market competition, the development of these agreements will also be affected by factors such as market demand, technological progress, and regulatory environment.The following ten trends will shape the future of derived derivatives market. For the existing participants and new participants in the market, understanding and adapting to these trends is essential.

-

Market reorganization

Due to the changes in user needs, the decentralized derivative market is undergoing major reorganizations.People not only look forward to more functions, but also have higher and higher requirements for user experience, capital efficiency, transparency and other aspects.This reorganization will lead to more flexible and innovative new participants in accordance with the needs of such user needs. -

Technical Innovation Acceleration

Technological innovation is the core of the development of new enterprises.We expect more innovative trading mechanisms, such as more efficient liquidity pools and improved risk management tools to solve the unique challenges of high volatility and unstable liquidity in the cryptocurrency market.Smart contracts will also optimize the ability of security and more complicated and more efficient financial strategies.Continuous technological innovation is essential to maintain competitiveness on the platform. -

Cross -chain transaction

With the maturity of the cryptocurrency market, users need to be more and more seamless transactions across different blockchains.The development of cross -chain function has enhanced asset liquidity and provided users with wider trading opportunities.We predict that a platform that supports multi -chain operations will gain a competitive advantage due to its enhanced interoperability. -

The requirements for supervision adaptability are continuously improved

With the development of global regulatory patterns, platforms that can be flexibly adapted while maintaining decentralization will have an advantage.This means that the platform must not only pay attention to technological development, but also pay close attention to international regulatory dynamics and adjust its operations to meet the legal requirements of different regions.Regulatory adaptability will become an important criterion for future distinction platforms. -

Improve the user experience fundamentally

User experience will become a key factor in platform differentiation.With the growth of decentralized financial user bases, simplifying the user interface and transaction processes and reducing technical barriers are essential for attracting wide user bases.This is not just a problem with interface design, but rethinking the entire transaction process.How to provide a user experience comparable or better than a centralized exchange while maintaining decentralization should be a problem that all platforms are given priority. -

Smart contract security

Smart contracts are the cornerstone of decentralized finance, and its security directly affects the reputation and asset security of the platform.The security of intelligent contracts to enhance the security of smart contracts through stricter code audit and error bounty plans is essential for establishing user trust and preventing funds from loss of funds. -

Improve capital efficiency through innovative financial instruments

The decentralized platform is facing major challenges in terms of capital efficiency.Although the traditional financial market has a series of mature tools and strategies to improve capital efficiency, the crypto market still has a lot of room for development.The future decentralized platform will focus on innovative financial instruments and complex trading strategies, which will test the market understanding and financial innovation capabilities of market participants. -

Decentralization governance

Centralized governance is the core feature of blockchain technology.Effective community participation and transparent decision -making process will increase platform credibility and user participation.In order to achieve true decentralization, we expect that the future platform will pay more attention to the opinions of the community and make the community participation an important part of the decision -making process. -

Diversified synthetic assets and derivative products

With the maturity of the market, the demand for diversified investment tools will continue to grow.Synthetic assets and various derivatives will be the key to meeting this demand.In the future, decentralized platforms will provide broader derivatives, including options, futures and various composite financial products.These diversified products will attract a broader investor foundation and enhance market depth and liquidity. -

New liquidity mining and incentive mechanism

In order to attract and retain users, it may create and implement new liquidity mining and incentive mechanisms.These mechanisms should be able to attract users to participate and maintain user activity for a long time.We expect a variety of new incentive mechanisms, including token awards and diversified long -term incentives to cultivate user loyalty and increase participation.