Author: Charles Yu, Galaxy; Compilation: Tao Zhu, Bitchain Vision

summary

-

The Bitcoin ETF received a net inflow of $15.1 billion between launch (January 11, 2024) and June 15, 2024.

-

Nine issuers are competing to launch 10 spot Ethereum ETFs in the United States.

-

After all 19b-4 applications were approved on May 23, the SEC expects to allow these instruments to be traded effectively in July 2024.

-

Like Bitcoin ETFs, we believe that the main new net market is independent investment advisors, or investment advisors affiliated with banks or brokers/dealers.

-

We expect net inflows to account for 20-50% of BTC ETF net inflows in the first 5 months, and our target is 30%, which means $1 billion in monthly net inflows.

-

Overall, we believe that ETHUSD is more price sensitive to ETF inflows than BTC because a large portion of the total ETH supply is locked in staking, bridging and smart contracts, while centralized exchanges are less supplying.

Preface

For months, observers and analysts have downplayed the possibility of the U.S. Securities and Exchange Commission (SEC) approval of spot-based Ethereum Exchange-traded products (ETPs).This pessimism stems from the SEC’s reluctance to explicitly state that Ethereum is a commodity, no contact between the SEC and potential issues, and the SEC’s investigation and pending Ethereum ecosystemNews about law enforcement actions.Bloomberg analysts Eric Balchunas and James Seyffart expect a 25% chance of approval in May.However, on Monday, May 20, Bloomberg analysts suddenly increased the likelihood of approval to 75% after reports that the SEC had contacted the stock exchange.In fact, all Ethereum spot ETP applications were approved by the SEC later this week.As we wait for the actual launch of these tools after the S-1 file takes effect (we expect to happen sometime in the summer of 2024), this report takes clues from the performance of Bitcoin spot ETP to make the demand for Ethereum ETPpredict.We estimate thatSpot Ethereum ETP will see a net inflow of approximately $5 billion in the first five months of trading (about 30% of the net inflow of Bitcoin ETP).

background

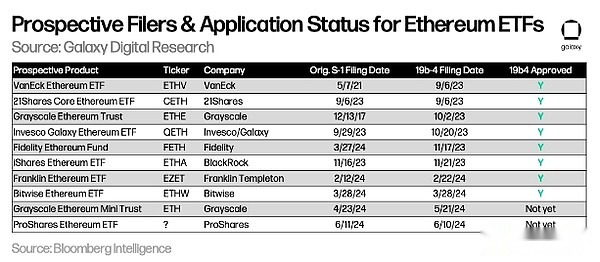

Currently 9 companies are competing to launch 10 exchange-traded products (ETPs) that hold spot ETH.Some issues have been resolved over the past few weeks.ARK chose not to work with 21Shares to develop Ethereum ETP, while Valkyrie, Hashdex and WisdomTree have completely withdrawn their applications.The following figure shows the current status of applicants sorted by 19b-4 application date:

Grayscale is looking to convert Grayscale Ethereum Trust (ETHE) to ETP, just as the company has done with its Grayscale Bitcoin Investment Trust (GBTC), but has also applied for a “mini” version of the product.

Grayscale is looking to convert Grayscale Ethereum Trust (ETHE) to ETP, just as the company has done with its Grayscale Bitcoin Investment Trust (GBTC), but has also applied for a “mini” version of the product.

The Securities and Exchange Commission (SEC) approved all 19b-4s (the change in rules that allow stock exchanges to list final spot ETH ETPs) on May 23, but now every issuer needs to repeat with the regulator about its registration statement.communicate.The product itself can’t really start trading until the SEC allows these S-1s (or S-3s of ETHE) to take effect.Based on our research and reports from Bloomberg Intelligence, we believe that Ethereum spot ETP may start trading as early as the week of July 11, 2024.

Lessons learned from BTC ETFs

Bitcoin ETFs have been online for about less than 6 months and can serve as a useful basis for checking the possible acceptance of Ethereum spot ETFs.

Some observations in the previous months of Bitcoin Spot ETP transactions are as follows:

-

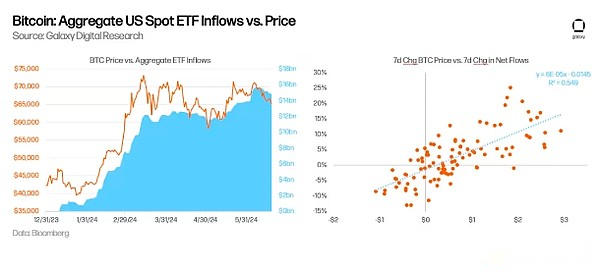

So far,The inflow of funds rose unexpectedly.As of June 15, the U.S. spot Bitcoin ETF has accumulated more than $15 billion inflows since its launch, with an average net inflow of $136 million per trading day.These ETFs hold a total of approximately 870,000 BTC, accounting for 4.4% of the current BTC supply.BTC is trading at about $66,000, and the total asset management size of all U.S. spot ETFs is about $58 billion (Note: GBTC held approximately 619,000 BTC before the ETF was launched).

-

ETF capital inflows are part of the reason for the rise in BTC prices.Regressing the 1-week change in BTC 5 price and 1-week ETF net flow, we calculated r-sq to be 0.55, indicating that the two variables are highly correlated.Similarly, we also foundPrice changes are better traffic leading indicators,vice versa.

-

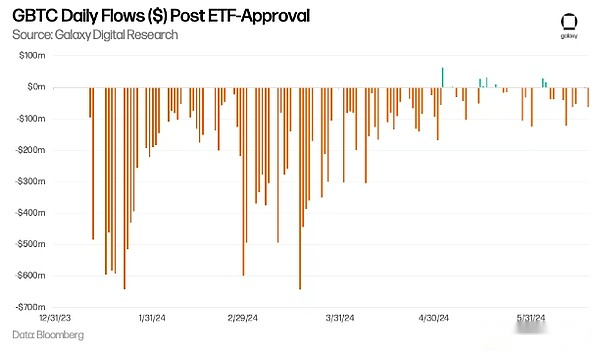

Closed positions in GBTC trading has always been a prominent issue in the overall traffic of ETFs.Since converting trusts to ETFs, GBTC has experienced substantial capital outflows in its first few months.Daily GBTC outflows peaked in mid-March, with outflows reaching $642 million on March 18, 2024.The outflows have slowed since then, with GBTC even starting in May for several consecutive days (78 days of outflows before the first day of net inflow on May 3).As of June 15, BTC balances held in GBTC have dropped from 619k BTC to 278k BTC (-55%) since the launch of the ETF.

-

ETF demand is mainly driven by retail investors; institutional demand has rebounded.13F documents show that as of March 31, 2024, more than 900 U.S. investment companies held Bitcoin ETFs worth approximately US$11 billion, accounting for approximately 20% of the total Bitcoin ETF holdings, indicating most demandIt is driven by retail investors.The list of institutional buyers includes well-known banks (e.g. JPMorgan Chase, Morgan Stanley, Wells Fargo), hedge funds (e.g. Millennium, Point72, Citadel), and even pension funds (e.g. Wisconsin Investment Commission).

-

The wealth management platform has not increased access to Bitcoin ETFs yet.While Morgan Stanley is reportedly exploring convenience for its brokers to solicit customer purchases, the largest wealth platform has not yet allowed its brokers to recommend Bitcoin ETFs.Access to Bitcoin ETFs across wealth platforms, including brokerage dealers, banks and RIAs, is likely to last for several years.so far,The release of sales-driven inflows from institutional platforms is small, but we believe it will become an important catalyst for Bitcoin adoption in the short and medium term.

Estimate potential ETH ETF inflows

Using Bitcoin ETP as a proxy, we can estimate the potential demand for Ethereum-like products.

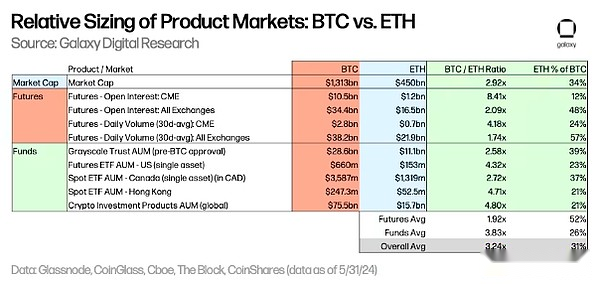

To estimate the potential inflows of ETH ETFs, we apply BTC/ETH multiples to Bitcoin U.S. spot ETF inflows based on the relative asset sizes of multiple markets traded by BTC and ETH.As of May 31:

-

BTC’s market value is 2.9 times that of ETH.

-

On all exchanges, the BTC futures market is approximately 2 times that of ETH based on open contract levels and trading volume.For CME, especially, BTC’s open contract level is 8.4 times that of ETH, while BTC’s daily trading volume is 4.2 times that of ETH.

-

The asset management scale of various existing funds (by Grayscale Trust, by product (e.g., futures, spot) and selected global markets) shows that the BTC fund size is approximately 2.6 to 5.3 times larger than the ETH fund.

Based on the above situation, we believe that the inflow of Ethereum spot ETFs will be about 3 times less than the inflow of spot bitcoin ETFs in the United States (consistent with the upper limit multiple), with a range of 2 to 5 times.in other words,We believe that the inflow of Ethereum spot ETFs may be 33% of the inflow of spot bitcoin ETFs in the U.S., with inflows calculated in US dollars ranging from about 20% to 50%.

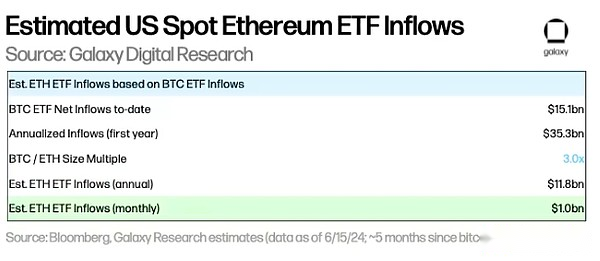

Applying this multiple to the $15 billion Bitcoin spot ETF inflows as of June 15 means that monthly ETH ETF inflows were approximately $1 billion in the first five months after Ethereum ETF was approved and launched (Estimated range: $600 million to $1.5 billion per month).

Due to several factors described below, we found that some estimates are lower than our predictions.That is, our previous report’s forecast of $14 billion inflows of Bitcoin ETFs in the first year was based on the entry of wealth management platforms, but before these platforms arrived, there had been a large amount of capital inflows in Bitcoin ETFs.Therefore, we recommend being cautious when predicting a sluggish demand for Ethereum ETFs.

Some structural/market differences between BTC and ETH will affect ETF traffic:

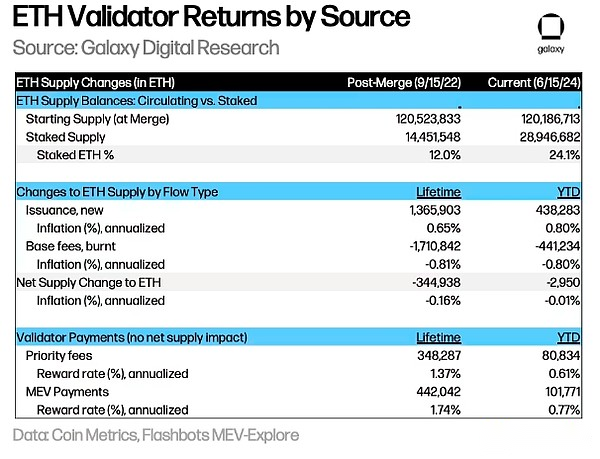

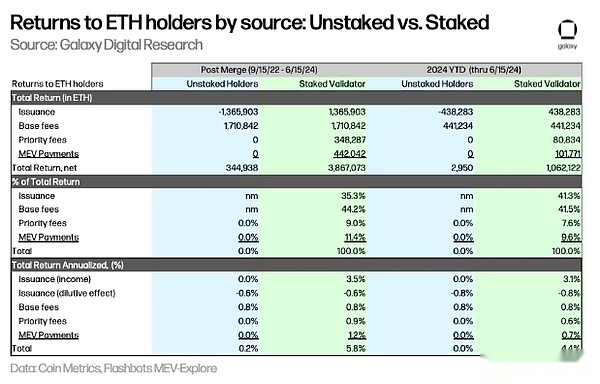

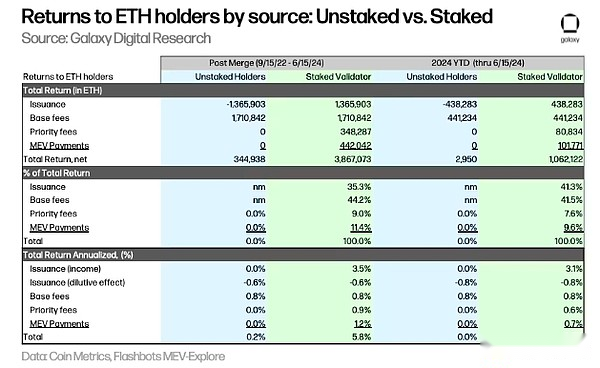

The demand for spot Ethereum ETFs may be limited due to the lack of staking rewards.The opportunity costs of non-staking ETH include: (i) inflationary rewards paid to the validator (also negative dilution effects), (ii) priority fees paid to the validator, and MEV revenue paid to the validator via repeater.Using the combined data (>9/15/22) to 6/15/24, we estimate that the annualized opportunity cost including pledge rewards is 5.6 percentage points (or year-to-date data) for spot ETH holders4.4 percentage points), non-significant difference.This will reduce the attractiveness of spot ETH ETFs to potential buyers.Please note that ETPs provided outside the United States (such as Canada) provide additional benefits to holders through staking.

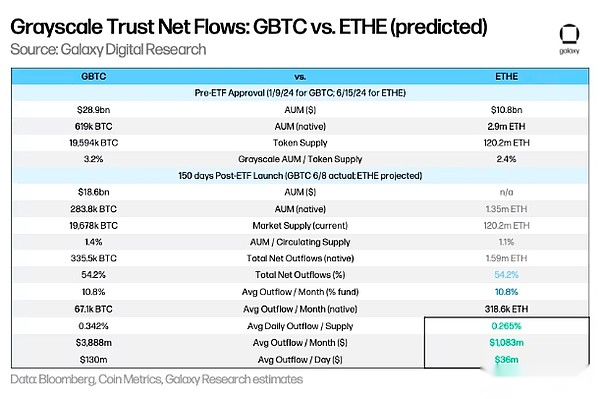

Grayscale’s ETHE may drag down the inflow of Ethereum ETFs.Just as GBTC Grayscale Trust experiences a large amount of capital outflows during the ETF conversion process, the conversion of ETHE Grayscale Trust to ETF also leads to capital outflows.Assuming that the rate of ETHE outflow in the first 150 days is consistent with the rate of GBTC outflow (i.e., 54.2% of the trust supply is withdrawn), we estimate that the monthly outflow of ETHE is approximately 319,000 ETH, at the current price of approximately US$3,400, 1.1 billionThe US dollar may flow out at an average of 36 million US dollars per day.Note that the percentage of supply held by these trusts is 3.2% of BTC supply and 2.4% of ETH supply, indicating that the drag on ETH price of ETHE ETF conversion is relatively small relative to the GBTC conversion.Furthermore, unlike GBTC, ETHE does not face forced sellers due to bankruptcy (such as 3AC or Genesis), which will further support the idea that ETH has relatively less selling pressure associated with Grayscale Trust compared to BTC.

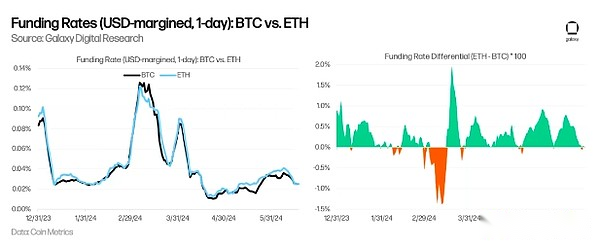

Baseline trading may have driven demand for Bitcoin ETFs from hedge funds.Baseline trading may have driven the adoption of ETFs by hedge funds that want to use the spread between Bitcoin spot and futures prices for arbitrage.As mentioned earlier, the 13F document shows that as of March 31, 2024, more than 900 U.S. investment companies held Bitcoin ETFs, including some well-known hedge funds such as Millennium and Schonfeld.Throughout 2024, ETH’s average financing rate on various exchanges was higher than BTC, which suggests that (i) the demand for long ETH is relatively large, and (ii) spot ether ETFs may attract greater demand from hedge funds, which look atGet up and enter the basis trading.

Factors affecting the price sensitivity of ETH and BTC

Since our Ethereum ETF inflow is estimated to be approximately equal to BTC inflow relative to market capitalization, we expect the price impact to be roughly the same under other conditions.However, there are several key differences in supply and demand between the two assets, which may lead toEthereum is more sensitive to the price of ETF traffic:

-

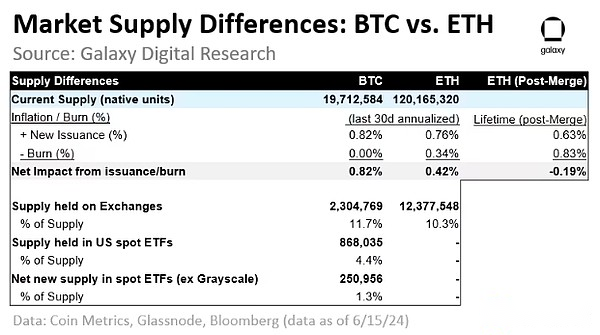

Supply held by the exchange:Currently, the exchange holds a higher proportion of BTC supply than ETH supply (11.7% vs. 10.3%), which suggests that ETH supply may be tighter,And assuming proportional levels, ETH prices will be more sensitive to price inflows relative to market capitalization (note: this indicator relies heavily on exchange address attribution and varies greatly between different data providers).

-

Inflation and destruction:Following the latest halving on April 20, 2024, BTC’s annual inflation rate is ~0.8%.After the merger (>September 15, 22), Ethereum net issuance was negative (-0.19% per year) because the basic fee paid to the stakeholder (+0.63%) has been burned (-0.83offset by %).In the last month, ETH basic expenses were relatively low (annualized -0.34%) and failed to offset new issuances (annualized +0.76%), resulting in an annualized net inflation of +0.42%.

-

Supply held in the ETF:Since its launch, the net BTC amount entering the U.S. spot ETF (excluding the starting balance of GBTC) totaled 251,000 BTC, accounting for 1.3% of the current supply.If calculated at an annualized rate, the ETF will absorb 583,000 BTC, or 3.0% of the current supply of BTC, which will far exceed the dilution level of miners’ rewards (inflation is 0.81%).

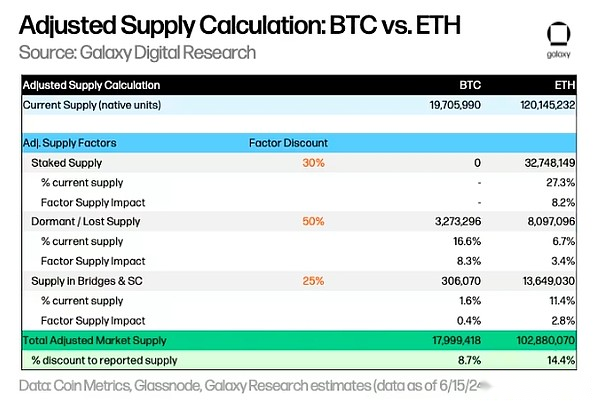

However, the actual market liquidity available for purchase of ETFs is much lower than the reported current supply.We believe that better representing the available market supply for each asset of ETF will include adjustments to factors such as staking supply, dormant/loss supply, and supply held in bridges and smart contracts:

-

Pledge supply (discount: 30%):The pledge supply reduces the amount of liquidity that the ETF can absorb.Currently, there is no option to stake BTC.ETH is required to protect network security, but stakers can use part of ETH staked elsewhere.Currently, the amount of pledged ETH accounts for approximately 27% of the current supply of ETH, and we apply a 30% discount to estimate the available market supply, resulting in an 8.2% factor supply discount.

-

Dormant/lost supply (discount: 50%):Some BTC and ETH are considered unrecoverable (e.g., lost keys, rowing accidents), so this reduces available supply; we used more than 10 years of sleep for the supply of BTC and ETH held in the last active address 7 years agoThe supply volume is equivalent to 16.6% and 6.7% of the current supply volume of BTC and ETH, respectively.We apply a 50% discount rate to this balance, as the supply held in some of the supposed hibernation addresses may be restored to online at any time.

-

Supply in Bridges and Smart Contracts (Discount: 25%):This is a supply locked in bridges and contracts for production reasons.For Bitcoin, the BitGo hosted packaged BTC (wBTC) BTC balance is approximately 153k BTC, and we estimate that the number of locks in other bridges is roughly the same, accounting for approximately 1.6% of the BTC supply in total.ETH locked in smart contracts accounts for approximately 11.4% of the current supply.We apply a 25% discount to this balance than the staking supply because we assume that the supply is more liquid than the staking supply.

Applying discount weights to each factor to calculate adjusted supply for BTC and ETH, we estimate that available supply for BTC and ETH is 8.7% and 14.4% less than their reported current supply, respectively.

Overall,Compared with BTC, ETH should be more price sensitive to relative capital weighted inflows, because: (i) the available market supply is low based on adjusted supply factors, (ii) the exchange supply is relatively low, and (iii) the net emissions are reduced.Each of these factors should have a multiplication effect (rather than an additive effect) on price sensitivity with other factors, and prices tend to better reflect greater changes in market supply and liquidity.

Looking to the future

Looking ahead, several issues we face in adoption and second-order effects:

-

How should PM and allocators view BTC and ETH?Will existing holders migrate from Bitcoin ETF to ETH?For the allocator, some rebalancing is expected.Will spot Ethereum ETFs attract new marginal buyers who have not bought BTC yet?What would it be like for potential buyers who only hold BTC, only hold ETH, or a mixture of the two?

-

If so, when can I add a stake?Is pledge reward not important for the adoption of Ethereum spot ETFs?Given the lack of alternative investment products, will the investment demand for accessing DeFi, tokenization, NFT and other crypto-related applications drive more adoption of Ethereum ETFs compared to Bitcoin?

-

What are the potential impacts on other alternatives?Are we more likely to see other alternatives ETFs approved after Ethereum?

Overall, we believe that the potential launch of spot Ethereum ETFs should have a significant positive impact on Ethereum market adoption and the wider cryptocurrency market for two reasons: (i) Expanding accessibility across various wealth sectors, (ii) Get greater acceptance through formal recognition regulators and trusted financial services brands.ETFs can expand the influence of retail investors and institutions, provide wider distribution through more investment channels, and can support Ethereum in the portfolio to use in more investment strategies.Furthermore, more knowledge about Ethereum among financial professionals will ideally facilitate investment and adoption of the technology.

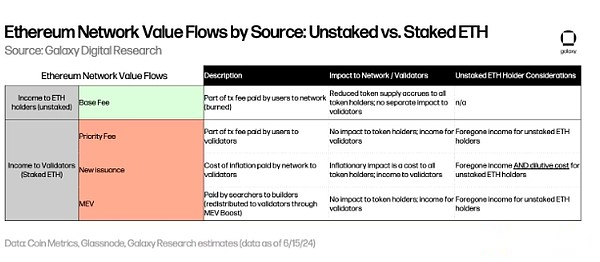

Appendix: Accrued value of positions and non-position ETH holders

Generally speaking, changes in ETH supply come from the basic expenses of new issuances (paid to validators) and burning, which is enough to offset the inflationary impact of new issuances since the launch of Shanghai upgrades (aka “merger”) in September 2022, thusReduced ETH supply increased by 0.20% by net value.

If the issuer is prohibited from pledging ETH in the ETF, the ETF will bring considerable opportunity costs in terms of loss of validator income and dilution.Looking at pledge validators from the perspective of unstaken ETH holders and nonstakenators, considering the accumulation of value in various value streams:

-

The basic expense portion of the user’s transaction fees is burned down, which reduces supply and benefits equally by unstaked and pledged ETH holders.

-

The preferred fee portion of user transaction fees is the revenue collected by the validator (no impact on unstaked ETH holders).

-

MEV payments are paid to builders by searchers and reassigned to validators via MEV Boost, similar to a priority fee, providing income to pledged validators without impact on unsolicited ETH holders.

-

New issuances of block rewards have a dilution effect on all ETH holders; however, for staking validators, the new issuance acts as another source of revenue, sufficient to offset the dilution effect of the new issuance.