Author: Alex Thorn, Gabe Parker; Source: Galaxy; Compilation: Songxue, Bitchain Vision

Preface:

2023 is a milestone year for cryptocurrencies, with BTC rising more than 160% and ETH rising 90%, but cryptocurrency venture capital is still down significantly from the glorious year of 2022.The tightening monetary policy has increased capital costs and reduced venture capital allocation across the board, while several major events in venture capital-backed cryptocurrency industry startups have further reduced allocation interest.Ultimately, by the end of 2023, the investment in cryptocurrency venture capital was only 1/3 of the previous two years, and the transaction volume was only slightly more than the previous two years.However, the cryptocurrency industry appears to surge in 2024, and central banks are also preparing to relax monetary policies, and the combination of these two may lead to a renewed interest in cryptocurrency venture capital this year.

Venture Capital

Number of transactions and investment capital

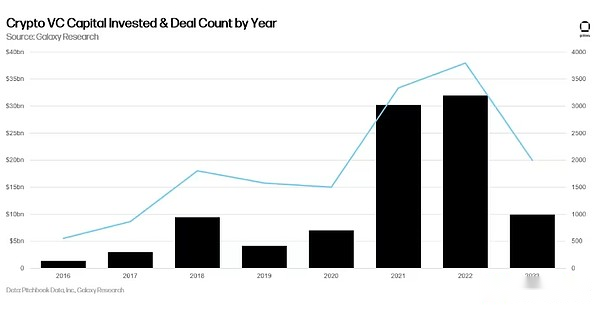

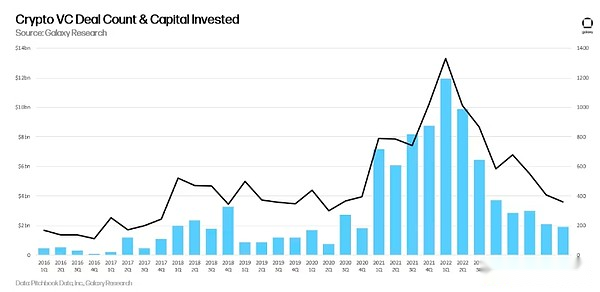

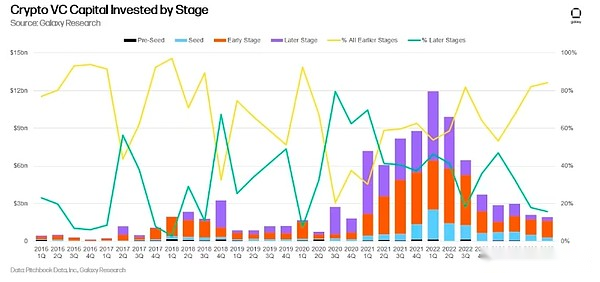

In terms of transactions and investment capital, 2023 is the third largest year for cryptocurrency venture capital, although both indicators have dropped significantly from 2022.

By quarter, transaction volume and capital investment continued to hit new lows.359 transactions invested $1.98 billion in the fourth quarter of 2023, slightly lower than the third quarter of 2023.

The number of transactions hits its lowest since the second quarter of 2020 and the lowest since the fourth quarter of 2020.

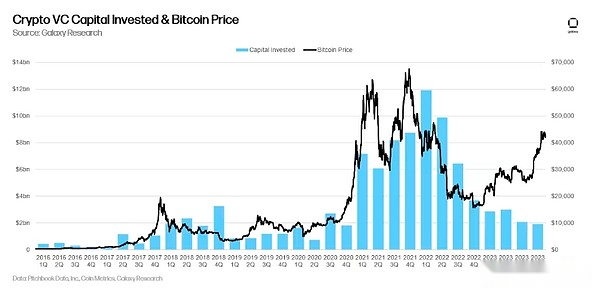

Venture Capital Investment and Bitcoin Price

While venture capital is often associated with Bitcoin prices, this correlation has broken significantly in 2023, with Bitcoin rising 160%, while cryptocurrency venture capital continues to hit new lows.

Stage venture capital

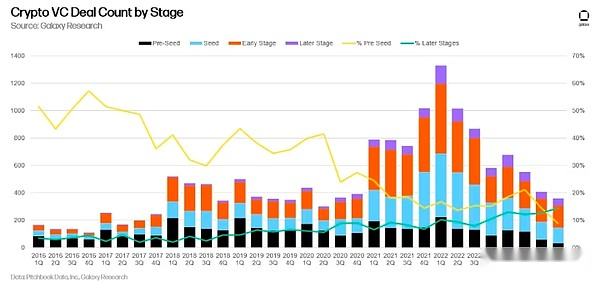

Throughout 2023, early stage companies accounted for the majority of venture capital transactions, and this trend accelerated throughout the year.In the third and fourth quarters of 2020, less than 20% of transactions were completed by later companies.

Although the share of transactions before seed rounds increased from mid-2022 to mid-2023, the share of transactions at the earliest stages dropped sharply in the second half of 2023.

Valuation and transaction size

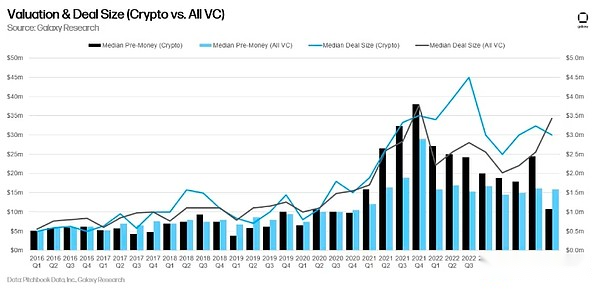

Venture-backed cryptocurrency companies valuations fell sharply in 2023, reaching the lowest median pre-investment valuation since the fourth quarter of 2020, while all venture capital pre-investment valuations fell initially in early 2022Stay relatively stable.The fourth quarter fell 33% from its all-time high of $4.5 million in the third quarter of 2022.

Investments by industry

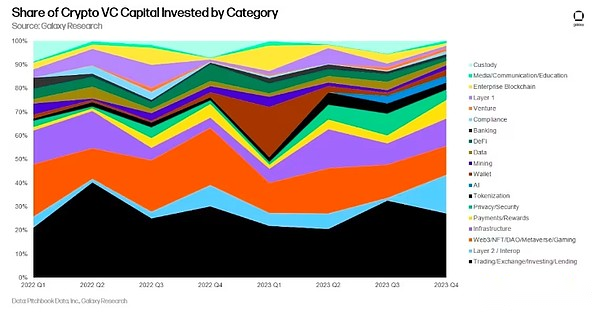

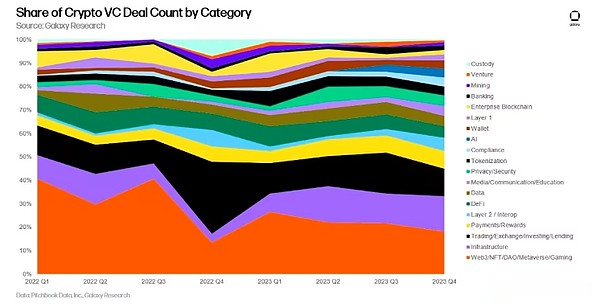

Startups focused on trading, exchange, investment and lending companies raised the most venture capital funds (27% of the total) for the fourth consecutive quarter.Our Layer 2 and interoperability category raises second (16%), with Wormhole’s $225 million financing.Web3 ranks third with 12% financing.Our new AI category is stable at around 3% of all funds raised.

In terms of transactions, Web3 continues to lead, with the category including gaming, NFT, DAO and Metauniverse related companies, followed by infrastructure companies, surpassing trading, exchange, investment and loan companies, ranking second.

Investments by stage and category

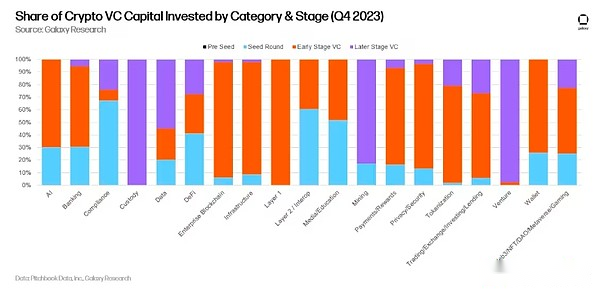

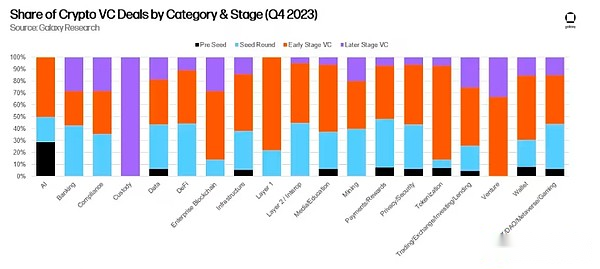

From a stage perspective, startups in the compliance category tend to be seed stage, while capital in the venture capital and custody category tends to be late stages.If a company is a platform for financing or capital deployment, it is classified as “VC”.Note that a company raised late-stage funds in the custody category but did not disclose the size of the transaction, so a column in this chart is based on extremely limited data.

In terms of transaction count, it is worth noting that 50% of AI startup transactions are seed or pre-seed transactions, indicating that businesses are showing strong interest in this emerging category.

Investments by geographical location

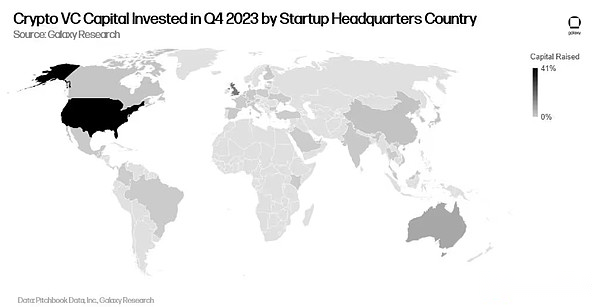

In 2023, the United States continues to dominate in the number of transactions and investments.Nearly 40% of transactions in the fourth quarter involved U.S.-based startups.

From the perspective of invested capital, the situation is similar.Despite regulatory resistance, the U.S. dominance continues.

Group investment

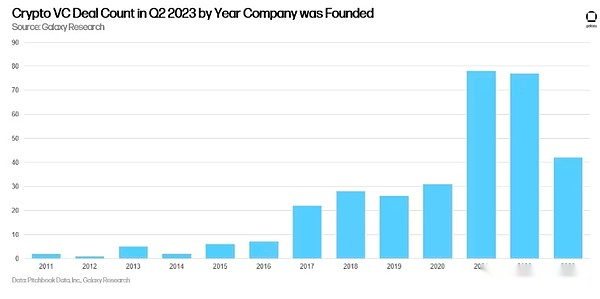

In the fourth quarter of 2023, the largest number of companies established in 2021 (78), followed by companies established in 2022 (77) and companies established in 2023 (42).

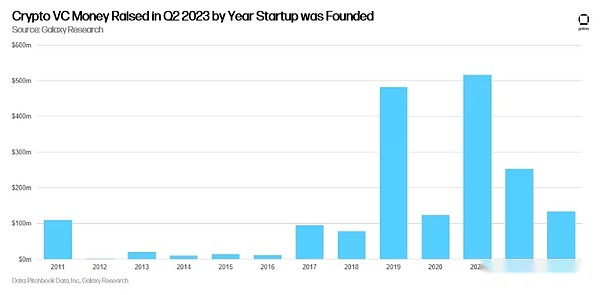

The companies founded in 2021 raised the most money ($516 million), with startups founded in 2019 ranked second ($482 million).

Cryptocurrency Venture Capital

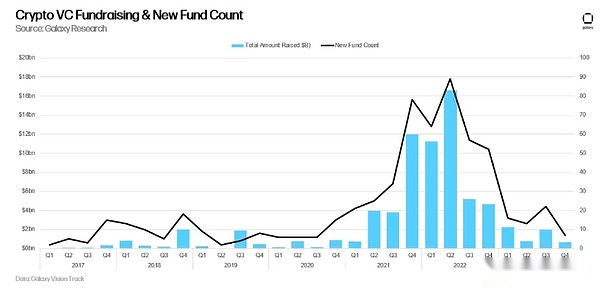

Fundraising for cryptocurrency venture funds remains extremely challenging.The macro environment and turmoil in crypto market infrastructure startups has hindered allocators from making the same level of commitment to cryptocurrencies as they did in 2021 and 2022.In the fourth quarter of 2023, the number of new cryptocurrency venture capital funds was the smallest and the amount of allocated.

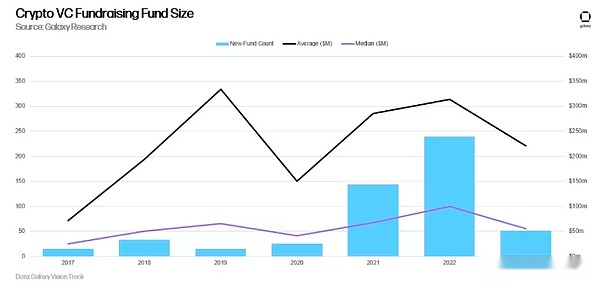

Yearly, 2023 is the year with the fewest number of newly launched cryptocurrency venture capital funds since 2020.The average fund size fell by 30% year-on-year, while the median fund size fell by 45%.

Summarize

2023 has been a tough year for crypto VCs, and the ecosystem has not yet bottomed out firmly.Despite the rebound in liquid cryptocurrency prices, venture capital activity has continued to hit new lows every quarter.Both founders and investors continue to face a difficult financing environment.

Bitcoin ETFs will put pressure on cryptocurrency venture capital and hedge funds.The ability of allocators to obtain cryptocurrencies at low fees through regulated spot Bitcoin ETFs will present additional challenges for asset managers seeking to launch new active funds.While some managers have done so, managers who are not currently benchmarked on BTC will face pressure from open or implicit practices.

Pre-seed trading continues to decline both in terms of actual value and relative to it.Only 32 pre-seed transactions were completed in the fourth quarter of 2023, accounting for only 8.9% of completed transactions and 0.26% of invested capital, down from the 217 highest transactions (43%) in the first quarter of 2019 and 2016 No.The highest capital investment in the first quarter was 19%.

Trade and Web3 companies continue to dominate, but AI is showing growth.Companies that provide investors with ways to buy and sell cryptocurrencies continue to dominate their financing, but Layer 2 and interoperability investment increased in the fourth quarter, with Wormhole bridge raising a large amount of money.Artificial intelligence is becoming a more interesting category, with several startups entering the space.

The United States continues to dominate the cryptocurrency startup ecosystem.While the U.S. maintains a clear lead in transactions and capital, regulatory challenges in the U.S. could force more companies to turn overseas.If the United States is to continue to be the center of technological innovation, policy makers should be aware of how their actions or inactions may affect this ecosystem.