Source: Coinbase; Compilation: Tao Zhu, Bitchain Vision

summary

-

In December 2024, on-chain lending usage reached an all-time high.We believe that this sector will continue to grow as the overall chain economy expands.

-

Most on-chain lending markets have floating interest rates based on liquidity utilization thresholds.Therefore, historically, rising lending rates have been linked to other signs of leverage in the market, such as high perpetual futures financing rates.

-

We believe that programmatic lending agreements will continue to be adopted, especially at new innovative levels such as interest rate trading and custodial vaults.Having said that, we believe that traditional financing channels are still important, especially for institutions.

Lending solutions are the core part of the cryptocurrency market structure and have been one of the pillars of the on-chain economy since the beginning of the birth of Decentralized Finance (DeFi).Crucially, the DeFi lending protocol enables financing access in a programmatic and license-free manner and operates 24/7.As the industry matures, the total lock-in value (TVL) in the DeFi lending protocol hit an all-time high of $55 billion in December 2024.

In addition to financing utility, we believe that the transparency of the on-chain lending market also makes it a useful indicator of market positioning.Lending demand (especially stablecoins) is proxyed through floating interest rates, which usually reflects the demand for leverage.We found that stablecoin lending rates correspond to other popular market indicators, such as perpetual futures financing rates.Excessive use of certain assets (such as ETH) as collateral may also affect their performance during periods of volatility.

We believe that the on-chain lending industry will continue to grow as the diversity of assets on the collateralized chain continues to increase.On-chain protocols are increasingly integrated into existing platform interfaces, such as BTC-backed loans on Coinbase.at the same time,At the forefront of the DeFi market, we believe interest rate trading and custodial vaults may be the two drivers of future growth.That being said, we also believe that traditional financing solutions are still important to investors (especially institutions) because their interest rates are more predictable, discretionary, and the risk profile is different.

Overview of the lending mechanism

The lending market plays a core role in the traditional financial market, namely promoting liquidity and capital efficiency, so that enterprises can expand, individuals can invest, and institutions can manage risks.These services have traditionally been provided by banks or other financial intermediaries.But in the early days of cryptocurrencies, limited institutional participation has driven demand for cryptocurrency native lending markets.This leads to a DeFi lending market built on the blockchain track.

The DeFi lending platform operates through smart contracts to programmatically control the end-to-end lending process.Borrowers obtain loans by depositing crypto assets such as ETH as collateral to borrow other assets such as stablecoins.The amount of loanable is determined by the loan-to-value ratio (LTV) of the mortgaged asset.

For example, borrowers who deposit $10,000 ETH can get a USDC loan of up to $8,050 based on the current 80.5% LTV ratio on the Aave V3.(The LTV ratio of collateralized assets can be adjusted through governance on Aave.) Some agreements support multi-asset mortgages and borrowing, where mortgages and borrowing valuations are aggregated in one account.Other protocols may isolate lending pools to better manage risk management, while others run a hybrid model of isolation pools and cross margin pools.

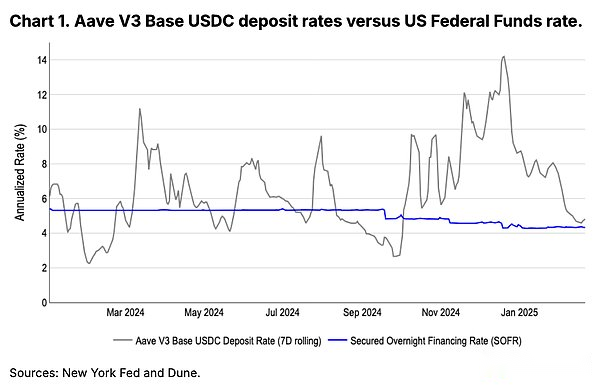

On the other side of the market, loans provide assets to liquidity pools to earn income, which are paid in interest by the borrower.Historically, these yields have often far exceeded the interest rates of short-term U.S. Treasury bills, making them an ideal place for cryptocurrency local investors to earn their earnings through stablecoins (usually without interest).See Figure 1.

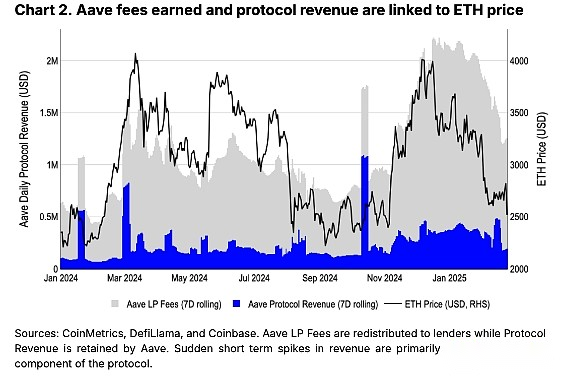

The smart contract enforces repayment terms and interest accumulation, while using some interest expenses as agreement income.Aave, the leading DeFi lending market, received $395 million in fees in 2024, with $86 million of them going to the agreement.(Note: Lightning loan fees also contribute to these figures.) Aave fees seem to be related to ETH price performance.We believe this is due to the hot market, which has increased demand for leverage (more will be introduced below).

If the collateral value is below a certain threshold, the agreement solvency is enforced through automatic liquidation.Unlike traditional financing solutions, lenders may make margin notifications before selling collateral assets to repay loans, and when the LTV ratio exceeds a predefined threshold, the DeFi lending agreement will automatically auction collateral.Once defaulted, the liquidator was motivated to purchase the borrower’s collateral to repay the borrower’s debt.The mortgaged assets are sold at prices below market value to help liquidators take market risks (such as slippage) and inspire more people to participate.The liquidation bonus (i.e. discount) can reach up to 8.5%.

Variable interest rates and signs of leverage

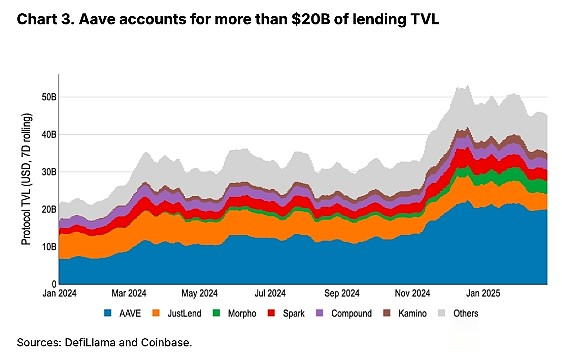

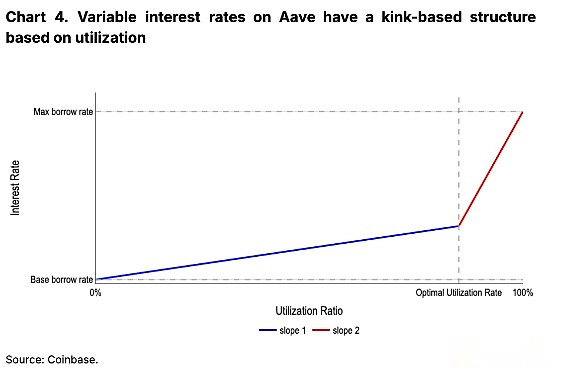

To optimize asset utilization, lending rates in most major lending markets will fluctuate based on market conditions.When borrowing utilization is low, interest rates are lowered to attract borrowers.Conversely, when utilization is high, interest rates will increase to attract more lenders.While variable interest rate calculations vary by protocol, we think Aave’s computer system is worth highlighting because it accounts for nearly half of all borrowing TVLs.(Note: We are following Aave V3.)

Each liquidity pool (i.e., assets) on Aave has several key parameters, including the base borrowing rate, the highest borrowing rate, and the best utilization rate.(Utilization equals borrowed assets divided by total liquidity.) The effective borrowed interest rate gradually increases in a linear manner relative to utilization before reaching the optimal utilization rate.However, when the optimal utilization rate is exceeded, the borrowing rate increases dramatically, albeit still linearly.The exact rate of growth for each section (i.e. slope 1 and slope 2) is determined by governance.This gives the borrowing rate a kink structure as shown in Figure 4.The kink structure helps explain why stablecoin borrowing rates may soar rapidly during demand periods—beyond optimal utilization, with interest rates rising dramatically.

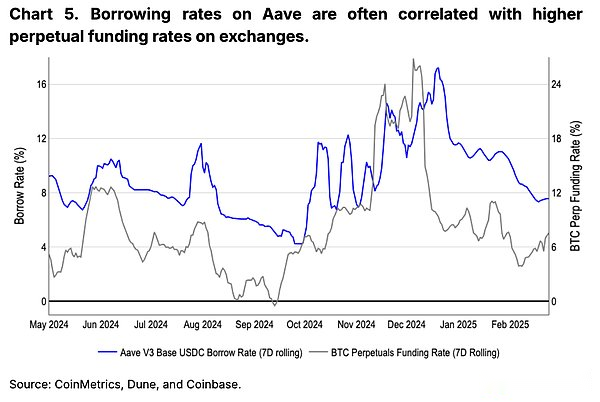

We believe thatLending demand (especially in the stablecoin market) may be an indicator of leverage in the cryptocurrency market.Investors can deposit their long assets as collateral, borrow stablecoins, and buy more assets to go long.In fact, investors can actually use collateral assets to short borrowed assets.In our opinion,Rising interest rates for stablecoin lending (especially those above the best utilization rate) are a sign of a hot market.Figure 5 highlights the relationship between USDC lending rates on Aave and ETH perpetual financing rates.(The financing rate is the annualized fee for retaining long positions in the perpetual market.)

Collateral concentration

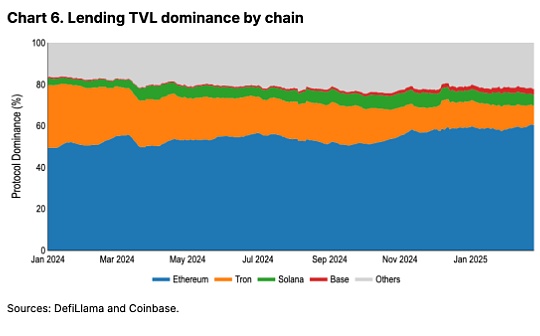

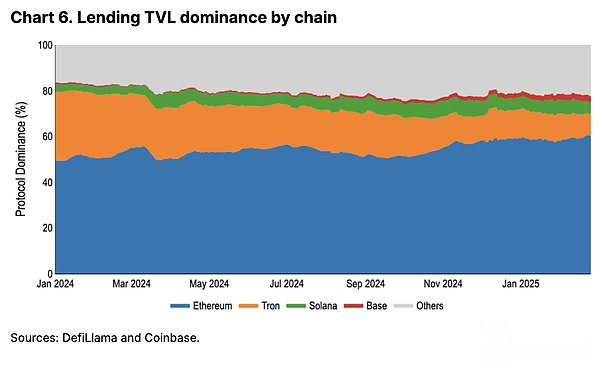

The reliability, security and overall maturity of the Ethereum DeFi ecosystem make lending TVL completely centralized on the network.In particular, Ethereum’s stability ensures that liquidity is reliably obtained during market volatility (when the lending facilities (and clearing processing) is most needed).Although Solana’s network stability has substantially improved over the past two years, its contribution to lending TVL is still 5.2%, compared to Ethereum’s 60.4%.

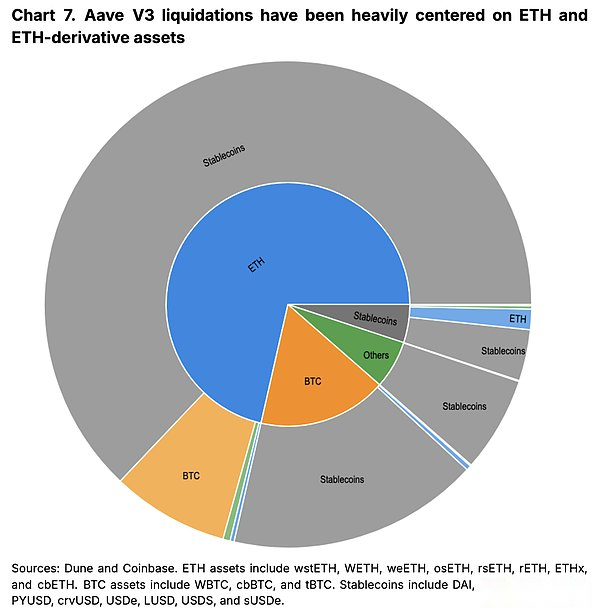

However, this brings aThe side effect is that ETH has become the most widely used collateral asset for DeFi lending.This leads to it often experiencing larger liquidation events during a period of sharp market contraction (due to programmatic sell-offs in liquidation).In our opinion, this explains to some extent why ETH may not perform well during periods of massive cryptocurrencies clearing.

Figure 7 shows a summary of all clearings on Aave V3 on Ethereum since January 1, 2024.The inner circle displays liquidated assets by collateral type, while the outer circle assets displays repaid debt positions (i.e., borrowed assets).Since the beginning of 2024, 71% ($575 million) of all liquidated assets on Aave are ETH or ETH derivatives, such as liquid staking ETH.Meanwhile, stablecoins account for 89% of borrowed assets ($655 million) in liquidated positions across all product types.

Frontier Development

While lending agreements are now a staple of the on-chain market, integration and innovation are still taking place at an alarming rate.In terms of integration, more and more companies and agreements are being built on the basis of core DeFi lending facilities.For example, Coinbase has enabled license-free BTC-backed loans powered by Morpho.As lending smart contracts are increasingly tested and trusted, agreements involving more complex and simplified financial products are being established.We thinkInterest rate trading and custodial vaults may be two key areas to be watched here.

Since the lending market currently operates in a variable interest rate model, it can be speculated whether the future interest rates are higher or lower than the current one.A new area of the earnings trading market, such as Pendle, has created a bilateral market that enables investors to understand how yields change over time.While the underlying earning assets are beyond the scope of the lending market (and into points tilling tokens, etc.), we believe that as more mature participants enter the market, and more assets are enabled on the lending market, they may become more important to the lending market.

Meanwhile, the custodial vault architecture helps depositors simplify the earning experience on agreements such as Morpho.The earnings opportunities for different agreements, liquidity pools and lenders may vary.The escrow vault enables depositors to provide assets to a single vault where the manager designs strategies and rebalances positions across multiple loan pools.The manager earns fees and the depositor can also get excess returns.

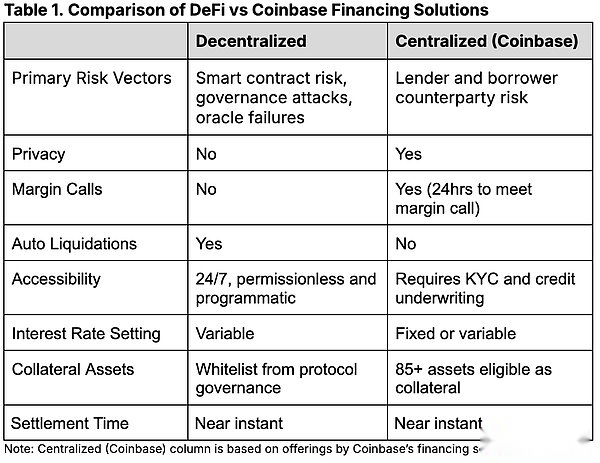

Comparison with traditional financing channels

Although we thinkIf market conditions remain unchanged, DeFi lending platforms will continue to grow their usage in the coming year, but we believe that traditional financing channels will continue to play a key role in the market due to greater flexibility and different risk profiles.For example, agency lending solutions like Coinbase enable customers to use their assets to generate revenue by acting as fully outsourcing lending agents to match borrowers and lenders on both sides of the market.

This may have some advantages for some institutions that may not be willing to settle transactions purely on-chain, especially during market volatility, where clearing is most likely to occur.A clear definition of the boundaries of counterparty and jurisdiction is also a key consideration for risk-aware institutions.Additionally, DeFi lending protocols and user positioning data are public, making it difficult to conceal the lending activities of large market participants.Experienced participants may be able to identify key liquidation thresholds or other positions the institution wants to keep cautious.

in conclusion

There are many opportunities for earnings in the cryptocurrency space.Traditional financing is important for cryptocurrencies because it is particularly suitable for institutional investors’ needs – providing clearer borrowing costs, greater discretion and clear counterparty risks.However, the increase in on-chain lending usage highlights the growth and maturity of the DeFi industry.As the total value locked in DeFi lending protocols reaches new heights, these programmatic and license-free solutions are becoming increasingly important to providing flexible financing options.We believe thatInnovations such as interest rate trading and custodial vaults are promising signs of further development in the field.