Author: Beichen

There are more and more discussions about PayTech. Solana, Binance, Coinbase and other crypto industry giants focus on Web3 payments. Traditional finance such as Visa, Sequoia Capital, and Temasek are also frequently investing in crypto payments, which makes people have a kind of thing that happened on DePIN in early 2023.Familiarity – the influential capital of the new and old worlds is being laid out, and the narrative is all about attracting resources in the real world.In the third world such as Southeast Asia and South America, USDT has even become a better choice than its own fiat currency.

Information from various levels and channels points to the same direction, that is, Web3 payment(PayFi/encrypted payment)The wind is blowing.After all, if the global payment market is compared to a fantasy wedding cake, then as long as the cake is lost, it will become a billion-dollar giant, and this gold rush has just begun.

However, since the concept of Web3 payment includes too many irrelevant things, it is necessary for us to first define whether FinTech (fintech) evolved from the traditional financial system with stablecoins such as USDT as the core, or from Bitcoin, or fromA payment system based on distributed ledger technology (DLT) is produced.

Web3 payments achieved with financial technology only add USDT and other stablecoins based on the fiat currencies originally provided, and still adopts the traditional nested clearing and settlement system.The only value of this type of product lies in the USDT as a shadow dollar and other stablecoins, otherwise it will be no different from supporting Q coins and Happy Beans.

Web3 payment based on distributed ledger technology is now very convenient to transfer money, but high-frequency payment has not yet been implemented.This type of Web3 payment is actually economic thoughts that have been brewing for hundreds of years and has been verified in the cryptographic test site for more than ten years. Moving forward in this direction, you will find that a magnificent journey is setting sail at dawn at dawn!

1. Web3 payment under the traditional financial technology system

Most Web3 payment products, the so-called Web3 actually refers to stable coins such as USDT. The product level is still no different from other Web2 payments. It is developed based on the API of a certain link in the traditional payment system, but it supports USDT.Currency types like that.Moreover, since alternative currencies are grafted, the channel cost is actually higher than that of fiat currency.

Let’s first break out of the complex slander of technology and finance to clarify the true nature of the payment system of traditional financial technology. The quality of Web3 payment will be much clearer.

1.1. The evolution of traditional payment systems and PayTech

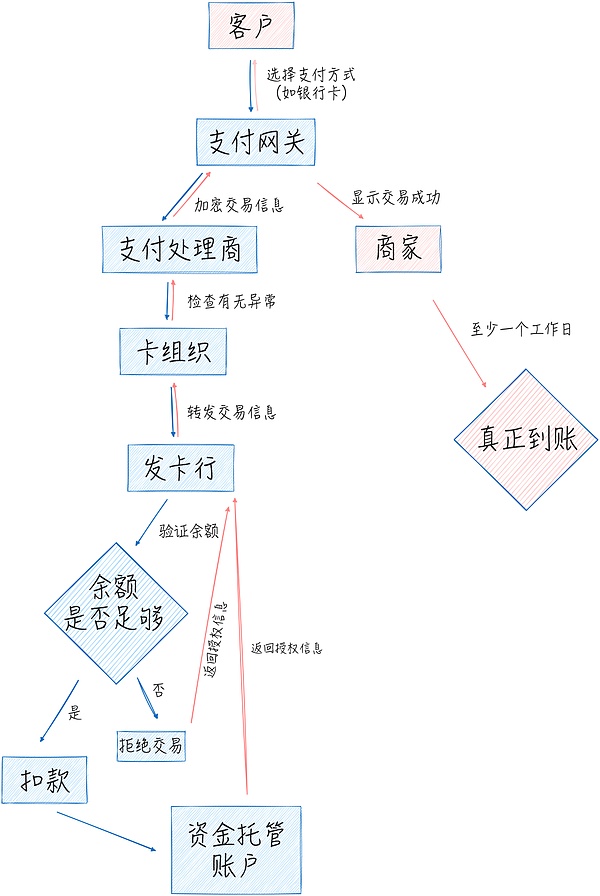

Let’s first analyze the traditional payment processing process using the payment scenarios in daily life as an example.When we check out at the convenience store, we can scan the code on our mobile phone and confirm the payment, but thisIn less than a second of the action, six or seven participants completed it after more than a dozen procedures..

First, the customer will choose a payment method (such as a credit card, debit card or digital wallet such as Alipay). After confirming, the payment gateway will encrypt the information of the transaction and pass it to the payment processor/processor. After checking that there are no exceptions,Release, transfer it to the card organization (such as Visa, Mastercard), and then transfer it to the issuing bank where the bank card is located. After verifying whether it is sufficient, the funds will be deducted from the customer’s account (but note that there is no direct transfer, butFirst hosted), then the information is returned according to the original route and sent to the merchant through the card organization, payment processor/processor, and payment gateway. The merchant shows that the payment is successful.However, it will take at least one working day to actually arrive, and the settlement process is also very complicated, so I will not repeat it here.

Such a complex processing process in the modern financial system was gradually established in the era of postal carriages.Fintech companies have not changed this system, butStarting from a certain link in the process and being responsible for accelerating information processing. This is the full value of FinTech lies in.After all, with the accumulation of countless transactions, each link means huge wealth.

Although banks have been electronic since the 1970s, FinTech’s idea has always been to move businesses online to accelerate processing.The internal structure and processes of the bank have not changed. At most, the construction of the middle platform has been promoted for intensive purposes in order to compete with third-party payment companies.

As a cross-bank clearing network, the core business of card organizations is to solve the issuance, settlement and reconciliation of cross-bank transactions. It also began to be electronicized in the 1970s, but the business logic is no different from the paper bill era. FinTech only accelerated the processing.speed.

However, card organizations represented by Visa launched a payment terminal – POS machine on this basis, which not only soon occupied the mainstream payment market in the retail industry, but alsoFrom then on, the payment ecosystem has revolved around payment terminals.For example, a group of hardware manufacturers represented by VeriFone (Whirfeng) have been created, and the role of payment service providers (PSP) has been differentiated, and the tasks of payment service providers have been abstracted into payment processors/processing.and payment gateway.

If card organizations are said to have established a banking network so that merchants can receive transfers from more banks, then PSP (payment service provider) further allows merchants to receive more card organizations and other payment channels (such as laterPaypal) transfer.As for the payment processor/processor and payment gateway, they are responsible for transmitting and checking information at different stages.

FinTech in the above links is all accelerating the efficiency of information processing. The entire process is still complex and lengthy, and of course the cost is also high..For example, the inconspicuous payment processor is expected to exceed US$190 billion by 2030.

FinTech, which can be called a revolutionary one, is Paypal in 1998. Users use their email to register an account/digital wallet. After recharge, they can bypass the traditional financial system and transfer money without loss within the platform. They only need to deal with banks when withdrawing cash.Only then will the expense be incurred.Although Paypal’s handling method is no different from the Happy Beans of the game company, it is this simple and crude way that tear a hole from the traditional financial system., forcing traditional finance to stagger into the era of Internet payments, at the cost of financial technology companies represented by Paypal are constantly facing prosecution and suppression.

Although the payment field after Paypal is soaring rapidly in business, such as the rising star Alipay has gradually built a financial service platform that can completely replace banks, and even established a credit system that surpasses the banking system, the progress in FinTech is onlyMicro-innovation like QR codes has no mechanism revolution.

1.2. Web3 payment based on financial technology

Now, whether it is a cryptocurrency giant or a traditional payment company, all the Web3 payment projects launched are based on traditional payment systems, but we can still introduce them in detail.

1.2.1. Traditional payment companies: treat USDT as happy beans

Traditional payment companies are actively entering Web3. Although they also have the consideration of acquiring new users, they are largely an offensive defense, afraid of missing out on the trend of cryptocurrency.Just like candidates in the US election competed to express their support for cryptocurrencies, they only spent a lot of effort to gain resources from non-core strategic maps.

In fact, traditional payment companies have not changed the traditional financial system in the past, and they will not change even when they enter Web3.They just took advantage of their existing market share and added the asset class of cryptocurrency to the many services they provide., the technical difficulty is equivalent to adding Happy Beans.

From banks (such as ZA Bank) to card organizations (such as Visa) to payment service providers (such as PayPal), they claim to embrace crypto, and they do have quite in-depth research, but what they say doesn’t matter, what matters isWhat are they actually doing.All the business is summarized as allowing consumers to use their bank cards to purchase cryptocurrencies, transfer and pay, that is, as a “transfer channel between fiat currency and cryptocurrency” to earn exchange fees, this is completely the OTC market.As for technologies like “making end consumers experience seamlessly”, it is not surprising, because Happy Beans are the same.

The traditional payment company that can truly go further in Web3 payments is PayPal, which issued the US dollar stablecoin PYUSD (PayPal USD) on Ethereum and Solana.PayPal claims to “use distributed ledger technology (DLT), programmability, smart contracts and tokenization to achieve instant settlement and be compatible with the most widely used exchanges, wallets and dApps…” because it can not onlyEarning the exchange fee between fiat currency and PYUSD can also extend the deposit time of funds, which is the same as Binance’s original intention of launching BUSD.

PayPal’s longer-term goal is to replace bank cards as the main payment channel.Of course, at present, it has neither the basic base of e-commerce platforms nor the offline merchant market. Moreover, major platforms are also launching their own payment tools (such as Apple Pay), so they try to return to their peak moments through PYUSDThere seems to be little chance.

Compared with PayPal, which lacks payment scenarios, Square, a payment platform established in 2009, has established a huge merchant payment network offline, and has promoted its own payment tool Cash App through fee discounts and other methods, which seems to replace bank cards and become the main payment.Channel trends.It is worth mentioning that Square’s founder Jack Dorsey is also the co-founder and former CTO of Twitter.

Square’s official entry into Web3 is to develop Bitcoin mining machines, but its former employees came out to establish the Web3 payment company Bridge in 2023 and received US$58 million in investment from Sequoia Capital, Ribbit, Index and other institutions, and in October it was again.It was sold to payment processor Stripe for $1.1 billion.What Bridge does is actually to let customers deposit US dollars and euros, create stablecoins, and then transfer money with stablecoins. If you treat stablecoins as happy beans, you will suddenly feel enlightened.Of course I am not criticizing Bridge, in fact, Bridge has quietly realized the grand narrative promised by Ripple back then.

Similar products include Huiwang, which is said to be a Chengdu team, but the main reason why it can make a prosperous product in Southeast Asia is that there is a large policy space there, and the collection tools for black and gray products are undoubtedly very large.Need for urgent needs.

The underlying product than payment tools is the currency itself. Now, in addition to USDT and USDC, many stablecoins in specific scenarios have emerged, such as OUSG and USDY launched by Ondo Finance supported by BlackRock, which are used to invest in the short-term United States.Treasury bonds and bank demand deposits.

all in all,Web3 payment of traditional payment companies is equivalent to the technical difficulty of Happy Beans. The threshold lies in whether you can find your own payment scenario..

1.2.2. Cryptocurrency giants: keen on issuing joint bank cards

If traditional finance uses the method of supporting Happy Beans to earn OTC fees, then cryptocurrency giants in turn use the method of supporting bank cards to earn OTC fees. In short, they are rushing in both directions to connect bank cards and HappyThe channel between beans.

The reason why exchanges such as Coinbase and Binance chose to cooperate with veteran payment giants such as Visa and Mastercard to issue joint crypto bank cards is certainly to leverage the infrastructure of traditional finance to attract more crypto assets, and there is another secret reason., that is to build a brand.After all, as long as you issue a card, you can claim to support “redeem and consume cryptocurrencies at more than 60 million online and offline merchants around the world.”In fact, you only need to cooperate with a member bank in Visa International, or even directly outsource it to a third-party card issuing agency..

There are countless cases of this kind, some of which are like around 2015 when mobile payment was just booming. Many mobile payment startups emerged, and their technology and even licenses were shelled, but it did not prevent the capital market from favoring this new trend.

The operating cost of co-branded cards of cryptocurrency giants is actually quite high. For example, the OneKey Card launched by the hardware wallet OneKey has been offline after more than a year of operation.According to the announcement, “There are many challenges here. It is very difficult to balance these factors at the same time to achieve low-cost operation of small teams, low handling fees, stable operation of card segments, anti-black and gray production, compliance.”

Later, PayFi, a new on-chain finance concept built around sending/receiving settlement, appeared, trying to redefine payments, claiming to be “free from the constraints of traditional banking systems and enable users to send cryptocurrencies worldwide at low fees., and the option to easily withdraw crypto assets to personal custody.But judging from the current solutions, they are all seizing the market of OTC merchants in the framework of the traditional payment system.andTheir compliance is destined to be no different from the traditional banking system and Happy Beans in the end.

The Web3 payment solution that can truly bring about a mechanism revolution on PayTech must be a solution based on distributed ledger technology.

2. Blockchain payment: Blockchain payment inside and outside the regulation are two species

Whether it is the central bank CBDC, private institutions or public chains, distributed ledger technology (DLT) cannot be avoided when discussing Web3 payment. Even though many of them treat USDT as happy beans, at least the happy beans here are issued based on DLT.of.

DLT is essentially a database maintained by multiple nodes, each sharing and synchronizing the same replica.Blockchain is a kind of DLT, but DLT is not necessarily a blockchain.With the impact of blockchain and cryptocurrencies caused by the birth of Bitcoin, DLT is increasingly regarded as a new infrastructure to replace traditional centralized entities to transfer funds, and of course, most of them are still in the experimental stage as an alternative.

The biggest advantage of DLT is that it is a point-to-point (P2P) network, so both parties to the transaction no longer need complex intermediaries.Financial transactions can be verified directly through public ledgers, thereby realizing clearanceCalculate, and DLT also operates 24/7.Moreover, when doing payment based on DLT, there is another advantage that currency is programmable – not only can different currency rules be defined through smart contracts, but also can achieve more complex functions when interacting with other smart contracts.

The above is the common advantage of DLT for payment, but the problem is that the difference between DLT and DLT is even reproductive isolation, such as public chains and alliance chains.Moreover, even if they are all public chains, only the different types of consensus algorithms (such as PoW and PoS), the confirmation speed and cost structure may vary greatly, let alone payment applications built on different types of DLTs.

The industry seems to ignore these differences and only cares about the fast and slowness of TPS and whether it is compliant or not.However, unlike the academic community that relies on peer review (maybe if the paper is published too much, it becomes authoritative), the development of DLT will ultimately be left to the market for verification.

2.1. Alliance Chain andCBDC isThe product of sexual intercourse

The alliance chain is largely a product of incompatibility with the centralized system——Based on DLT technology, and strictly control access rights.This seemingly decentralized centralized solution can meet regulatory compliance, but in essence it is still a closed system.This is destined to only play a role in reducing costs and increasing efficiency in a certain link in the traditional financial system, and will not change the system itself.

In the most mainstream narrative, central bank digital currency (CBDC) seems to be the end point of Web3 payment.Although CBDC itself is a false proposition, it is not only technically, but even from a currency perspective.Some CBDC solutions are not as good as alliance chains, because they are just a centralized database at all, and they can only be said to be borrowing some DLT technical features, such as multi-nodes and consensus mechanisms.But what is even more absurd is that some technologies that use centralized databases have put together a relational database with version numbers. There are no blocks or chains, but they boast about innovations in blockchain, such as Sui.

soPayment applications and CBDCs based on alliance chains are only partial tool iterations for clearing and settlement systems within the organization, rather than paradigm revolution involving the entire financial system..Moreover, in theory, iteratively, it would be better to use centralized databases directly.

This phenomenon of using new technologies to repeat old business is only a special product of the transition stage.Hong Kong has accumulated many cases in building financial products based on DLT, and at present, it has not brought about a qualitative leap in business.So let’s focus on those Web3 payments that are truly built on the public chain.

2.2. Public chains are imitating alliance chains

True Web3 payments should be built on public chains, which is also the original vision of Bitcoin and blockchain.Over the years, along this idea, Lily Liu, chairman of the Solana Foundation, formally proposed the PayFi concept in July this year.

She willPayFi is defined as “a new financial primitive built around the time value of currency” and is a financial innovation above the settlement layer.DeFi solves transaction problems, while PayFi involves a wider range of economic activities – sending and receiving, such as supply chain finance, payroll loans, credit cards, corporate credit, interbank repurchase and other scenarios, so the market is also larger.

Lily Liu believes that PayFi’s success must meet three conditions: fast and low-cost, widely used currency, and developers. The final conclusion is that only Solana can meet perfectly.The previous discussions are not criticized, but this conclusion will definitely attract many opposition from competitors, such as Ripple.

Ripple officially started PayFi in 2012 (the term was not available at the time). It is positioned as a blockchain that allows global financial institutions to transfer money with XRP. It was once highly expected to break the SWIFT monopoly and was selected in 2019.Forbes’ 50 most innovative fintech companies.

Ripple’s Layer1 is XRP Ledger, a blockchain based on federated learning. Strictly speaking, it is a consortium chain, although it claims to be a public chain (it can only be said to be open source).The initial business was to copy Bitcoin, but it was faster – letting everyone directly use its native asset XRP to transfer money.

The Ripple team holds a large amount of XRP and continues to sell and make profits. It has repeatedly pulled the market in the secondary market by releasing repurchase news and cooperating with market makers to increase trading volume.When they sold XRP, they deliberately blurred the relationship between XRP and Ripple’s equity, so they were targeted by the SEC and were deeply involved in dispute for four years. They should settle down in the near future, but it does not hinder the basic fact that XRP is useless.Ripple later realized that no one would pay with an air currency like XRP, which is price fluctuating (even Bitcoin is not suitable for retail payments due to volatility), so he tried to launch a stablecoin RLUSD, build CBDCs for various countries, and provide asset agents.Asset Tokenization and hosting services.

If you only judge based on Ripple’s promotional materials, you will feel that Ripple has covered more than 80 payment markets around the world with more than US$50 billion in transaction volumes due to its advantage of completing payments in a few seconds.But in fact, Ripple’s xCurrent targeting banks only records cross-bank transfer information on Ripple’s blockchain. The most core automatic reconciliation engine technology is actually no different from traditional clearing institutions.The value of this business is mainly reflected in licenses and channels, Ripple acquired in 2023.As for using air coins with price fluctuations like XRP to make consumption payments, it is even more false.

In a nutshell, Ripple plays the role of a top marketer in the PayFi market.Just like the crypto company mentioned earlier, as long as it cooperates with a member bank in Visa International, it can claim that its products “redeem and consume cryptocurrencies at more than 60 million online and offline merchants around the world.”

In short, when talking about PayFi, almost all public chains emphasize how fast it is, how cheap it is, and how compliant it is. However, PayFi products based on public chains (such as Huma Finance) are still in the traditional payment system.Just use blockchain as an accounting tool.Apart from the absence of KYC, what is the difference between it and the alliance chain?

2.3. Bitcoin Lightning Network and Limitations

So it still depends on the encryption native solution built on the public chain, but it is often limited by the block size and confirmation time of the public chain, so it can only be used as a remittance transfer and cannot support high-frequency small payments in daily life.The Lightning Network is a good solution.

Simply put, a payment channel is established off-chain. This channel is equivalent to a multi-signment wallet created by Account A and Account B. They both recharge in the wallet and then can transfer unlimitedly (the actual amount of each transfer isThe above is to update the wallet balance allocation status to form a new UTXO, that is, the unspent transaction output), and will not be handed over to the Bitcoin network for verification until the last transfer is closed.soLightning Network can realize high-frequency payments without changing the underlying mechanism of Bitcoin.

There may be a question here, that is, the balance changes in the payment channel are not linked, so how to ensure security?The security of the traditional financial system depends on the credit guarantee of the institution, but Lightning Network ensures the security of the payment channel through cryptographic technologies such as LN-Penalty and HTLC (hash time lock contract). I will not repeat it in detail.

It should be noted that the security channel discussed just now is one-to-one, but in actual transfer, it is impossible to build a multi-signment wallet with everyone, so a one-to-many solution emerges, that is, multi-hop routingtechnology.In layman’s terms, there is a payment channel between A and B, and there is also a payment channel between B and C. Then A can transfer money directly to B, and then to C. Account B acts as a relay node, A and BThere is no need to build a separate payment channel.According to the six-degree separation theory, you can know any person in the world through six people.

This one-to-many solution requires relay users to be online regularly and have sufficient funds, otherwise transactions may fail. Lightning Network uses technologies such as multi-path routing and node redundancy to overcome these challenges.butIn actual use, this design is too ideal——Suppose the user is willing to lock in a large amount of funds in advance, and assuming that the user is willing to tolerate various technical restrictions, these are allRuns contrary to the capital efficiency problem that PayFi originally wanted to solve.

Lightning Network’s solution was later expanded from Bitcoin to other public chains.For example, Fiber Network built on Nervos CKB has Turing’s complete smart contract capabilities and is more flexible in asset management, but it still does not break out of the dilemma brought by payment channel design.

This raises a very profound question: finance is a complex system, and it may be difficult to reshape the entire payment system just by innovation at the technical level.So what kind of design can bring about a systematic paradigm revolution?

3. The end point of currency is that there is no currency

Finance has always existed as a complex system, and it is difficult to bring substantial changes if it is just technology, so it is necessary for us to re-examine this system.

Finance is an instrument system developed to serve real transactions, in which currency plays the role of a value account unit, which leads to extremely complex trading systems, clearing systems and credit systems.Because we cannot avoid currency, to be precise, to be legal currency, and to be more precise, to be difficult to avoid US dollars, soThe current Web3 payment track and even the entire crypto market are the highest pursuit to be included in the shadow dollar economic system represented by USDT..

“The great luck of a man is that he must embark on an extremely difficult road, whether in adulthood or childhood, but it is the most reliable road; the misfortune of a woman is surrounded by almost irresistible temptation;She was asked to strive for it, only encouraged to slide down to reach the Pure Land. When she found herself fooled by a mirage, it was too late, and her power was exhausted in a failed adventure. “

This passage comes from “The Second Sex” written by Beauvoir in 1949. I think the “women” in it can be completely replaced by “crypto”. At least the Web3 payment track is running selflessly on this road to falling to the paradise.What I want to point out is that we can go along another extremely difficult road, which has been deduced by hundreds of years of economic thoughts, and has been initially achieved in the crypto test site over the past decade.verify!

Therefore, some commonly needed and easy-to-storage commodities were naturally adopted as general equivalents and entered the commodity currency stage.For example, animal skins, livestock (the word “money” in many languages has an etymological relationship with livestock), grains, cloths, salt and shells, etc.

Later, with the expansion of trade scale, the requirements for portability, durability, and separability became increasingly high, and currency began to concentrate on metals and entered the stage of metal currency.

However, with the development of the scale of trade, even if it is precious metal currencies, it is not convenient for merchants to store and carry them in large quantities. They choose to store precious metals in goldsmiths with vaults and guards, and then directly hold storage bills similar to warehouse receipts.Trading in the market, this kind of bill is gradually recognized by law as a quasi-currency.

Because under normal circumstances, no one will frequently retrieve precious metals stored by themselves, goldsmiths often over-issued invoices. At this time, the value of the invoices is based on the credit of the goldsmith.Later, more professional banks evolved from goldsmiths (most bankers in London were still members of the Goldsmiths Guild in the 18th century). From then on, based on institutional credit, they directly entered the banknote stage, and of course, they also established relatively standardizedCurrency issuance and redemption rules.

Speaking of which, as the earliest paper currency, Jiaozi was issued in the Southern Song Dynasty and the background of the issuance in the Southern Song Dynasty was similar, and the subsequent development paths were similar. Private commercial institutions first issued and competed freely, and then monopolized by the government, and endorsed by the state credit, and will issue it.The power is concentrated in the central bank and the forced circulation of fiat currency (this is extremely bad!).

After entering the national credit currency stage, the right to issue currency has become part of national sovereignty, and the currency itself has not undergone any greater changes (at most, after the collapse of the Bretton Woods system, it was liberated from the constraints of the gold standard and released further), the next development is about technology.

As the scale of trade expands, paper money (essentially bills) cannot meet the demand.However, if both parties open an account in the same bank, then they do not need to use paper money. They can complete the transaction through pure book records such as bank transfer, which simply requires the bank to conduct complex liquidation behind the scenes.This kind of clearing can naturally serve the transfer between different banks, so a bank network and a bank credit system have gradually been formed, including

Looking back here, we can find that currency is generated by trade in services and is intended to efficiently match supply and demand, from commodity currency to credit currency, even national credit currency is no exception.

However, national credit currency relies on the central bank’s regulation, and regardless of whether the central bank’s regulation is correct, the starting points of the central bank’s interests in each country are inconsistent. Therefore, these policies will eventually disrupt the original price structure, guide resource investment in the wrong direction, and continue to accumulate errors.Until finally getting together was liquidated.Therefore, Hayek advocated denationalization of currency, and needed a free currency movement like the free trade movement in the 19th century, and then a new banking system was formed.

Since with the evolution of the exchange mechanism (especially the clearing system), currency has evolved from a physical exchange medium to an abstract unit of account, can the exchange of goods and services be further completed directly?after allThe creation of money is only to overcome the limitations of barter.This is by no means regressing to primitive society. The reason why barter is replaced by currency is because the market at that time was too small and there was a lack of enough coincidence to match demand.

But with the expansion of market size and the evolution of exchange mechanisms, these can be overcome.In fact, in Argentina in the 1990s, some communities had tried to use internal credit bonds as alternative currencies to help vulnerable groups participate in economic activities in barter, and achieved phased success (the peak is 6 million people)However, because of the flood of issuance, it was as unfinished as the junk bonds issued by local governments today, but the crypto world directly eliminated the possibility of unfinished.

However, I would like to add one thing here. The author does not extremely believe that currency should be completely eliminated, but only believes that currency will no longer be needed as an intermediary for transactions in the future, but it still needs a common value reference standard. After all, the ratio between massive commodities is almostEndless.The ideal unit of measurement should not be a fiat currency with unlimited inflation, but it should not be a limited supply of gold, Bitcoin and other assets, because this means that the cost of latecomers must be higher than that of early holders, soThis will inevitably lead to the tendency of holders to hoard, which will eventually lead to unnecessary deflation.

This technology that touches the deeper financial system is the blockchain opened by Bitcoin.As a point-to-point value exchange system that requires no trust, you can directly skip the multi-level clearing system in traditional finance (what they do is nothing more than calculate the amount).

Moreover, in the blockchain world, each token means a certain value, ownership or even access right, which means they are naturally a kind of goods or services native to the chain, and they can be divided into DEX.(Decentralized exchange) for exchange, skip the currency intermediary to calculate the exchange rate directly, so not only does not require physical currency, but also does not require currency at all.

This solution seems to be a fantasy of Satoshi Nakamoto’s cracks from the stone, but in fact, as early as 1875, British economist and logician William Stanley Jevons wrote “Money and its Exchange Mechanism” (Money) in his book as early as 1875.and the Mechanism of Exchange deduced the development path of currency, believing that in the future, he would enter the stage of bartering, and he prophesied that the US dollar was unswervingly moving towards international currency.

Moreover, cryptography practices over the past few decades have also verified this conjecture.

After many conjectures and experiments of ideas and technologies, Satoshi Nakamoto published “Bitcoin: A peer-to-peer electronic currency system” in 2008. Based on his predecessors, he compared consensus algorithms with public key cryptography.Combined, a decentralized currency has been truly realized and the era of blockchain has been opened.

However, he stubbornly believed that Bitcoin does not require a scripting system, which gave latecomers a chance.For example, in 2012, Yoni Assia proposed Colored Coins

Colored Coins allows Bitcoin to represent various digital assets, but due to the functional limitations of Bitcoin, it can only be issued and traded, and still cannot support Turing complete scripts.So Vitalik Buterin, a core member of the team, started a new start and released the Ethereum white paper “Next Generation Smart Contracts and Decentralized Application Platform”. Since then, the blockchain with a built-in Turing complete programming language has been officially launched, allowing anyone to write smart contracts and decentralize..

So far,

in conclusion

In the forked garden of the path of Web3 payment, the converts are performing the joy bean tricks to attract countless audiences.The rebels’ path is full of thorns, which is destined to be “taking an extremely difficult road, but it is the most reliable road.”

From Jevins to Hayek, liberal economists have foreseeed that money will eventually return to a more essential form of exchange.From cyberpunk to cryptoanarchism, creators and cryptographers have already shown us this possibility in the test grounds of the crypto world.

On this difficult but reliable path, we look forward to more like-minded partners joining together to contribute to the technology stack and business scenarios and pioneering our paradigm revolution.Welcome to follow and discuss~