1.Crypto’s business model

Recently, there have been many criticisms about the accumulation of value of Ethereum and L2. The ever-changing exploratory development of Ethereum and L2 has brought difficulties to their value assessment.This article tries to give some directions to think.Before talking about how to view the business model of Ethereum and L2 in detail, let’s take a look at the business model that exists in the entire Crypto.

1.1 “Enterprise” category

Core: Control + Monopoly (licensing), price discrimination brings profits

The focus of this type of model is to achieve the goal of increasing revenue through a high degree of control over services and agreements, which is no different from traditional company business standards.Decentralization here is highly abandonable, and it only needs to be accepted by users.In essence, as a profit-oriented company, it is necessary to ensure efficient operation, so there should be no situation of control diplomacy.

For such projects, what is competitive is the business model, that is, the ability to discriminate against prices, the rapid response to meet user needs, and the ability to bring about user growth. Tokens are mainly a means of customer acquisition and assetization.

Taking Solana Foundation as an example, its high control over the ecology can be said to have even the right to shut down.Solana calls herself Global Onchain Nasdaq, and has always emphasized fundamentals, especially business models and profits, which constitute the core value of this story.Solana’s revenue comes mostly from MEV revenue, that is, price discrimination arising from monopolizing the block space, while SOL assets themselves are asset-based tools that are centrally held.

1.2 “Protocol” Class

Core: Unlicensed participation (asset issuance, business), open and relatively fixed charging standards

The focus of this type is to create open and almost unchanged protocol standards, which are behind them by DAO and foundation governance, but less intervention, so that the protocol can operate autonomously.The use of the agreement is Permissionless, and the profit model is open and difficult to change. Anyone can use the agreement to create markets, assets to obtain their own business or profits.”Agreement” often has another assessment of the degree of autonomy, that is, the degree of decentralization has a scope. At least, the team has the right to renew the agreement and is subject to market supervision; at most, the company destroys its own right to renew the agreement and hands the product over to the market for disposal; at most, the company destroys its own right to renew the product., there are differences in decentralized governance of different degrees, hard or soft.Tokens serve more as dividends and governance here.

For such projects, the test is the sustainability of product operation, the sustainability of demand, and the network effect brought by entry time, and often find pioneers of PMF with significant competitive advantages.

1.3 “Assets” category

Core: Focus on the value of the asset itself

Including BTC, Memecoin, decentralized algorithm stablecoins, etc.The asset itself is recognized based on its characteristics, and the empowerment of the asset is continuously completed based on this.The attributes of the asset itself include three aspects. First, the consensus and network effects brought about by the “earliest adoption” in specific scenarios, such as BTC as the value store, USDT as the payment medium, and ETH as the asset issuance; second, the attributes of the asset mechanism, including rarity, deflation mechanism, price anchorage, etc.; thirdly, it is widely accepted and disseminated due to its symbolic meaning. For example, BTC is widely understood as “digital gold” and ETH “programmable credit currency”, Memecoin’sCultural effects, etc.

For such projects, the test is the strength of consensus, the ability to adopt and continuate assets.

In the Crypto world, different projects and assets correspond to the above-mentioned business models or combinations. We can also try to evaluate the current Ethereum and L2 from this perspective.

2.What is L2’s business model?

2.1 The current positioning of L2

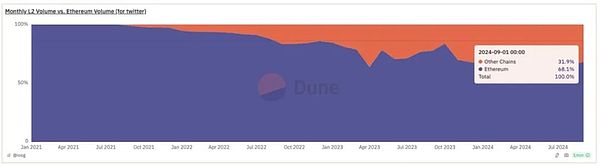

L2 was initially positioned as Ethereum’s Scaling, which carries Ethereum transactions on a large scale.Such a purpose has actually been achieved to a certain extent.From the perspective of diversion of Ethereum transactions and bringing incremental growth, it is relatively successful.At present, L2 has become an important part of the Ethereum ecosystem, with transactions accounting for 85% of the total and transaction volume accounting for 31%, becoming an important part of Ethereum’s fundamentals.

Source: Dune Analytic

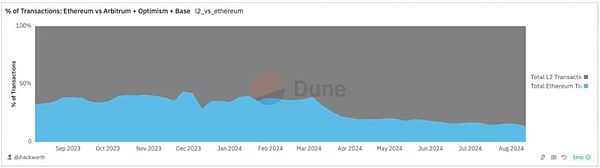

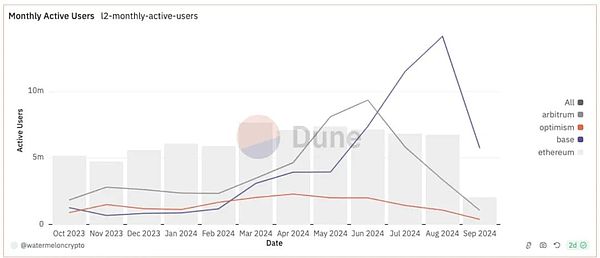

The number of active addresses is 3-4 times that of Ethereum

Source: Dune Analytic

Due to the cheap transaction cost of L2, the actual increase in Ethereum’s overall transaction data will be more inflated, but we can still see the impact of L2 adoption.

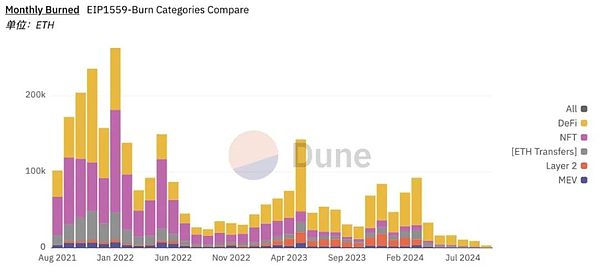

However, L2 did not bring about the same proportion of revenue to Ethereum under such transactions.The income brought by L2 is mainly divided into two aspects. The first is the DA fee, which is the transaction data fee before EIP4844, and the Blob fee after EIP4844.The second is MEV. In addition to the current Based Rollup, L2 has completely swallowed this income into its own pocket, and in the short term, the expectation of giving back to Ethereum is low.This actually made Ethereum enter inflation at present, and the concept of ultrasonic currency gradually declined.

Source: Dune Analytic

Here we explain why DA fees cannot be the contribution of L2 to L1’s income.

-

Only when DA reaches saturation will it incur priority fees, that is, monopolize pricing capabilities.

-

DA is a commodity in an unsaturated state. In the long run, users can hedge and find substitutions.

-

DA’s demand growth rate is disproportionately the supply growth rate.There are a large proportion of robot transactions in L2, and these transactions are not as necessary as real user transactions.If the C-side cost brought by DA fees is too high, this part of the transaction will naturally slow down.Therefore, it is not a reasonable conclusion that the so-called increase in the number of transactions will be saturated by several times.

In essence, expansion itself is contrary to DA fees. Under the pursuit of continuous expansion, making money should not be designed based on the degree of transaction congestion. The architecture of Ethereum L2 is also naturally referenced.The Beta asset, which was previously regarded as ETH, is still narratively true, and L2 still holds its own title of “Ethereum L2”.In fundamentals, it has gone further and further.In the future, L2’s revenue will no longer mean Ethereum’s revenue.Both should have their own valuation systems.

2.2What kind of business model are different L2?

2.2.1 Universal L2

Universal L2 refers to the general-purpose L2, and pursues itself to become an application ecosystem.Many of the early Universal Rollups have moved towards alliance form. Most of the current Universal Rollups have innovated in the mechanism of interest distribution to better motivate developers to innovate and retain and actively participate by users.The trend of L2 is that it will gradually no longer rely too much on Ethereum, and maximize its customization through some modular solutions.

The management method of Universal L2 is expanded outward from various teams as the core. The competition faced by Universal L2 is directly from the competition from external L1. The income acquisition of Universal L2 is almost 100% of the revenue under its profit distribution mechanism.In the bag.

This positioning is more in line with the “enterprise” model we mentioned and is suitable for valuation in a way similar to Alt L1, which means its value is an assessment of its ecosystem, fundamentals, especially revenue.Compared with Alt L1, its advantage is that it can make full use of Ethereum’s community and ecosystem, as well as the liquidity of ETH.The disadvantage is that Token’s assetization ability is relatively lacking, and its customer acquisition ability is slightly insufficient compared to Alt L1.

2.2.2 Alliance L2

Alliance L2 is similar to Ethereum, and has its own first and second layers (L2/L3). The difference between Alliance and Ethereum is that it requires permission to issue L2/L3 within the alliance, which ensures the business model of Alliance L2.

The early Universal L2s all went to Alliance L2, which also means that after gaining a certain level of market attention, Alliance L2 is often a better business.Before the transformation, Arbitrum, Optimism, and zkSync, and Initia have been working in this direction recently.For alliance-type L2, it is essentially already developing its own L1 ecosystem, but it is still backed by Ethereum’s security and the use of ETH to make settlement currency.The characteristic of Alliance L2 is that through its own management capabilities, it changes the business model and participants within the ecosystem.Therefore, it is more appropriate to regard Alliance L2 as a “protocol” with a high degree of centralization.

Source: Dune Analytic

Alliance L2 is more regarded as an Ethereum with control, and an ecosystem like Optimism still decentralizes the tasks of application development.The difference from Ethereum is that such decentralization is more strategic.Through the licensing model and centralized management model, resources can be concentrated, synergistic effects can be expanded, and excellent resources can come in to share liquidity and ecology, and feed back to the original ecology through the revenue gate after the new ecology is launched.This is also why Coinbase and Sony choose Optimism.With the help of L2’s “enterprise” ability, we hope that more breakthrough applications will be born.

We have previously mentioned that the “protocol” type patterns have different decentralization scopes.In the process of exploring protocol decentralization, chains or applications often emerge, such as DyDx, the earlier in the Arbitrum ecosystem and later TreasureDAO.How to develop and consolidate your own ecosystem while balancing the degree of decentralization of the agreement is the core of the value of measuring alliance L2.

2.2.3 Appchain L2

Appchain L2 is more of an app with new business models and value capture. Its valuation should be returned to the application itself and the L2 business model brings new value to the application, regardless of its application itself, it is more in line with the “enterprise”.Or “protocol” mode.Most App Rollups will choose to rely on Alliance L2, which has a lower startup cost and a stronger ecological radiation effect to rely on.

Appchain is currently mostly attached to Alliance L2 and RaaS, and the cost of building a chain is very low.However, in the design of chain adaptability, supporting infrastructure (such as data browsers, etc.) still requires investment.For Appchain, the visible benefit is through more efficient utilization of tokens and capture of MEVs, etc., and what is abandoned is the Lego effect and stronger liquidity on a chain.In terms of input-output, not all applications are suitable for Appchain. Suitable applications have strong endogenous cycles, such as Perp DEX, Gamefi, etc.In the long run, if the narrative popularity of transforming L2 is lost, it is more important to reasonably evaluate ROI.

3. How does L2 affect Ethereum’s business model?

After Merge, especially after EIP1559, Ethereum still captured higher priority fees and MEVs based on transaction volume in limited block space before obtaining a large amount of L2 expansion and EIP4844.After the expansion of L2 capacity, it actually gave up the MEV of this part of the transaction, and also reduced the priority fees brought by the native transaction of L1.After EIP4844, this part of the income as a DA was given up.Actively giving up such income is not a typical enterprise’s approach.In fact, Ethereum has never developed into the “enterprise” model we define.The transfer of this part of the profit is actually to give the space to the greatest extent under the premise of allowing the DA and settlement layers to adhere to a high degree of decentralization and autonomy, so that L2 can sacrifice a certain amount of decentralization under the minimum economic burden.to develop as large as possible and as many applications as possible.

3.1 Ethereum as L2 issuance protocol

Since establishing the path to Rollup Centric, Ethereum has moved towards a more “protocol” rather than an “enterprise”.Although some requirements for Rollup are put forward, such as L2beat Rollup stages, there is no actual interference.Currently, Vitalik has put forward some requirements for Ethereum Alignment, which will bring the governance model of Ethereum’s “protocol” closer to a more cohesive direction.But overall, it is still a “protocol” with a very high degree of autonomy, and its long-term role is to issue Ethereum L2.

At present, Ethereum L1 still carries more than half of the transaction volume in the entire ecosystem.In the long run, Ethereum provides a platform (settlement layer) that has a highly decentralized autonomy, censorship resistance and the highest security.

Generally speaking, the model of a license-free issuance platform pumps a certain proportion from the issuance and transactions of new assets, such as Uniswap extracting user handling fees, Pumpdotfun charges user currency issuance fees in the early stage, and predicts the market to extract user transaction fees, etc.

Therefore, although Ethereum is an L2 issuance protocol, it did not set a profit gate through L2 in the early stage.This led to the birth of a large number of L2 ecosystems that depend on Ethereum liquidity and community but do not contribute income to Ethereum, which means that Ethereum is the most pursuing decentralized autonomy in the “protocol” model.Looking at the relatively successful non-licensing agreements, such as Uniswap, have turned on the fee switch on some pools with absolute monopoly and network effects. After the agreement obtains the network effect, it will try to obtain it at a scale that users can accept.Costs are the advantages brought by centralized management.At present, for Ethereum, on the one hand, it is trying to try the fee gate through Based Rollup and other things, and on the other hand, it does not force the pursuit of profits, so that the L2 ecosystem, which originally had no profit gate, will continue to develop rapidly.

3.2 Ethereum as a store of value asset& programmable trust currency

ETH has been difficult to value through the “enterprise” and “protocol” model for a long time, because the early L1 business model will no longer be established after expansion.After all, an agreement that is willing to give up its own profits and an agreement that is willing to permanently close the fee switch should no longer be valuated from the perspective of traditional enterprise agreements.

The original intention of Ethereum to abandon fundamentals is to give more room for the overall ecological development.With the prosperity of the ecosystem, the value of Ethereum will eventually fall on the monetary value of ETH.So, what value can the potential prosperity of the Ethereum ecosystem bring to each other?

Some people believe that it is a security attribute brought by ETH.But at the same time, some people who believe in the value of distributed networks and Anti-crypto believe that P2P networks should not be bound to specific and speculative currencies to provide incentives for nodes. Some people believe that more speculative models should be used, such asStablecoins or early forms of PoW mining provide incentives.The decentralization pursued by distributed networks and the continuous reduction of costs, the pursuit of capital-intensive PoS mining is not a natural adaptation, and requires many governance methods to improve.At the same time, the security value of ETH itself is affected by its own price and is quite reflexive.These two points we mentioned in our previous article discussing economic security.ETH is currently doing well in terms of incentives and security models, but in the long run, it is not what it is best at.

So what is the most important value of ETH compared to the Ethereum network and will be recognized by the market?

Source: @0xdoug

We may find some clues from the development history of Ethereum. There are five highlights in Ethereum history so far:

-

Direct token release

-

DeFi Summer Liquidity Mining

-

Liquidity pledge

-

L2 mining

-

Re-stake AVS mining

In the earliest stage, the issuance of token assets directly through Ethereum opened up a new world of asset issuance and also allowed Ethereum to find the original PMF.From then on, the main development nodes of ETH were closely related to asset issuance.

In the DeFi Summer era, the asset issuance model evolved into liquidity mining, which not only made ETH as the asset that supports asset issuance, but also made it a liquidity target with pricing power.So ETH found a second PMF – a liquidity-denominated asset.From then on, the asset issuance of the Ethereum ecosystem will be accompanied by thoughts on improving liquidity.

Liquid pledge, while solving the pledge demand, leads to the enhancement of the liquidity pricing value.Since then, asset issuance has gradually introduced the attribute of ETH time opportunity cost mining, that is, staking, which is Ethereum’s third PMF.

L2 mining is a manifestation of such asset issuance + liquidity pricing + time cost mining.By bridging ETH to L2, pledging and mining the native Token/DeFi protocol tokens, while providing liquidity, which flows to each protocol through the liquidity engine on L2.The three PMFs of ETH are integrated.

Re-staking and AVS mining are another implementation of the integration of three.The liquidity re-pled agreement releases liquidity, similar to the re-pled agreement of EigenLayer, providing pledge, mining AVS native tokens through time cost indefinitely.

Ethereum is constantly repeating and improving this model, constantly creating demand and value for ETH itself in asset issuance and Defi use cases.It is also constantly strengthening ETH in the first choice of interest-generating assets, asset issuance, liquidity provision, or asset exposure and gas demand, which will all allow ETH to be distributed to the agreement and users, becoming Ether.The primary goal of infrastructure in the ecology, the agreement focuses on and the first choice of value currency in the user’s mind.

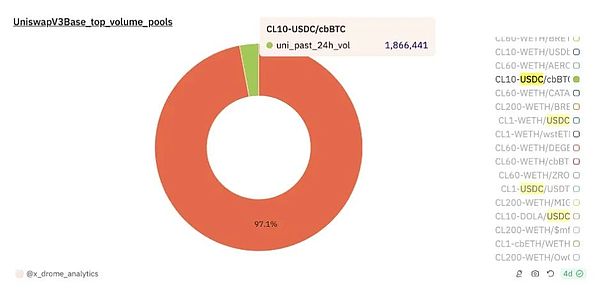

At present, there is not fierce competition for this value. For example, the currency pairs with ETH as settlement units in the mainstream Uniswap pool account for more than 80%.But ETH still faces some potential competition.Including competition for L2 native assets and derivative assets in store of value, such as $cbBTC on Base, and competition for off-chain liquidity brought by the intent network.

USDC/WETH vs USDC/cbBTC, Source: Dune Analytic

But in the long run, the incremental market of economic activities will bring about demand growth around the network effect brought by ETH construction, and as Myles said, all value will become more valuable.

4. Summary

Crypto’s valuable business models include three categories: enterprises, agreements, and currency themselves. The differences between the first two are mainly in the centralized control, monopoly, adjustments and price discrimination capabilities of the agreement. The agreement itself also pursues different degrees of autonomy.Currency itself lies in the network effect generated by the early use of a certain scenario with Traction.

Due to the early positioning of Ethereum and its L2 strategy, the value of Ethereum is driven to the level of licenseless “protocol” and ETH “currency”.Also, due to Ethereum’s vision, leadership structure and early L2 strategy, Ethereum has semi-actively and semi-passively abandoned revenue from L2, reducing the burden on L2 to open up growth space for L2.Although the standards of Ethereum Alignment from the Ethereum Foundation are becoming clearer and clearer, the overall open autonomy positioning has also made Ethereum no longer positioned as a simple “enterprise”.

The powerful early L2 ecosystem evolved into alliance L2, which is essentially a more centralized leadership and licensed L2 issuance “protocol” that continues Ethereum’s mission in a more centralized model.Universal L2 returns to the competition of L1 as a “enterprise”, and compared with L1 outside the Ethereum ecosystem, it has advantages at the startup level and disadvantages at the token level.The value of Appchain should return to the business model. With improved “application” itself (more “enterprise” or “protocol” with a higher degree of centralization), the ROI of the chain needs to be considered.The booming development of L2 is based on the highly decentralized Ethereum model, abandoning revenue to bring support and space.

Ethereum, on the premise that DA has proven to be not a suitable business model, has gradually positioned as a licenseless L2 issuance agreement that abandons the profit gate.It actively abandoned its monopoly ability in the stock market, hoping that it could be exchanged for its hematopoietic ability in the incremental market.The L2 alliance and some L2, which have strong corporate nature, brings new increments without paying taxes to Ethereum, is Ethereum’s biggest bet.

The value of Ethereum as a currency comes from the continuous asset issuance and liquidity games on Ethereum.Five PMF Moments continue to bring value and use inertia to ETH assets themselves.With the expansion of the overall Ethereum ecosystem, ETH, as the most valuable asset in the ecosystem, plays a crucial role in every step from the start-up to operation of the new ecosystem, which relies on the powerful network effect of ETH.As the ecology stabilizes, although some native assets/Wrap assets will play a supplementary role, it is difficult to affect the absolute share of ETH.

If there is a day when the L2 ecosystem will flourish in the future, as ETH with network effects, even if it does not necessarily have a monopoly effect, it will still obtain huge returns on adoption brought by incremental volume. By then, Ethereum will gradually establish the value dominated by ETH assets.form.

After understanding the trade-offs of Ethereum as the ecosystem and the value positioning of ETH and L2, we believe that L2, as the new force of the Ethereum ecosystem, will move forward lightly with a commercial interest-driven model, choose rich technical architectures, develop in multiple directions, and internallyAdvantages of vertical integration quickly open the ceiling of use cases.ETH will be the most network-effective asset and will gain value discovery as the entire ecosystem flourishes.