Original author: Steakhouse

“Recommended message: This article reexamines some core issues in the current ETH ecosystem Restaking, AVS and Liquid Restaking tracks, and presents an analogous risk and reward assessment framework predictively.enjoy!“

Trust is an essential component of economic activities and human cooperation.In corporate interactions, trust is primarily established through reputation and legal enforcement.Decentralized trust networks are a new type of coordination mechanism that allows individuals to conduct remote transactions without the need for trust intermediaries.Ethereum and Proof of Stake Systems create a concept of collateralized crypto-economic security in which native tokens are used as collateral by network providers to provide decentralized trust.

Restaking expands Ethereum’s crypto-economic security by creating a “decentralized trust market”.This is done by bringing together Ethereum’s restakers and validators (the provider of decentralized trust) with seekers of decentralized trust AVS (active verification service).Please note that Ethereum itself is in principle an AVS.Other AVSs can lead the creation of a new decentralized trust network through restaking to provide specific services.

Resolution ETH providers must conduct a risk/reward assessment of the network they provide for them with secure collateral.Expected total returns are an important part of crypto-economic security, as higher returns make decentralized trusted providers more attractive to participate in the network.

In this article, we explore the restake pattern in order to price the restake risks in these AVS networks and come up with a simplified value assessment framework.Our rough framework considers the “cost of trust” used in capital market pricing risks.Decompose into:

Return on trust = Return on price + Job income + Re-staking income – Loss of default

Reprivators should evaluate available opportunities in a systematic manner and determine whether the returns are equal to the risk.The market has very high expectations for re-staking returns, which is priced through multi-layer points.Ultimately, we believe that the market will have to face the reality of AVS monomer economics and the ability to withstand its security budget.

Restaking 101

What is AVS?

Active Verification Service (AVS) is a business that requires high trust to provide utility and gains trust through encryption security mechanisms rather than traditional, centralized security models that rely on trusted intermediaries.

In the broadest sense, decentralized applications (dapps), smart contracts and blockchains themselves are all delivered securely through crypto-economics.Many services rely on the default security model of some of the largest networks, such as Ethereum, that require services to meet the standards of that network.However, some services may choose to create their own security models for a variety of reasons:

•Fine-grained customization of specific rules, features, pricing or performance

•Complete sovereignty over governance and operational decisions

•Innovative or novel mechanisms at consensus or other protocol layers

•Neutrality

•Trust assumptions and specific security requirements

Unfortunately, a decentralized network with native crypto-economic security can be both expensive and complex to build from scratch.In fact, the relative lack of success of many Layer 1 blockchains demonstrates the high cost and coordination complexity to guide a decentralized crypto-economic security network with many distributed validators.In addition, the token prices of many Layer 1 blockchains are highly volatile, often causing unstable amounts of crypto-economic security present in the network and pushing up the long-term capital cost of these projects.

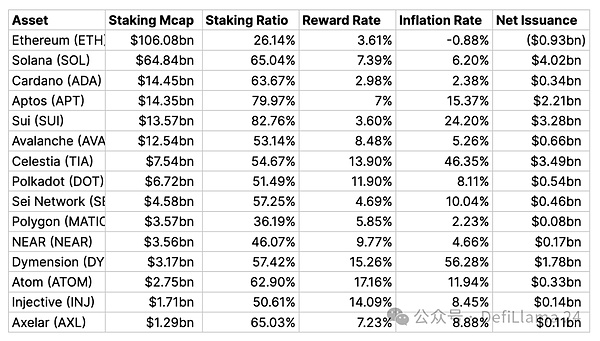

Source: stakerewards.com As of March 24, 2024

Although inflation is not a good indicator of decentralization, it can be seen as a useful signal that the network seeks to balance with the number of validators it seeks to motivate.In new, bootstrap networks, such as Dymension, inflation is very high, as compensation for attracting new pledges.If long-term network “revenue growth” can overcome the impact of dilution, paying new validators to join the network is a long-term sustainable expenditure.

What is re-pled?

Restaking is the restaking of ETH LSD assets for new active verification services (AVS), which impose new cuts on capital.AVS has the option of “leasing” their security from Ethereum stakers instead of booting a brand new crypto-economic security network from scratch using their native tokens.Restaking allows ETH stakers to gain enhancement from a capital efficiency perspective while providing AVS with potentially more stable security, no longer affected by native token price fluctuations.Ethereum’s vibrant economic and ecosystem activities make ETH a superior, blue-chip collateralized asset, similar to the concept of “hard currency”.

There are advantages to choose these services to rent their security in “hard currency” rather than building a brand new crypto security system from scratch.

In PoS security systems, stakers accept opportunity costs and price tokens that they must commit to in order to verify the network.The network must provide a high enough staking return to:

1) Attract depositors;

2) offset the fixed costs of the services provided by the verifier.The more trust (stake) is required to protect services, the higher the cost of meeting the needs of the stakeholder.In addition, the more value AVS products and services carry, the more security trust it requires.In the monomer economics of AVS, the cost of safety is an expense.

The economics of AVS require a large amount of capital to provide this level of security, which ultimately means that a large amount of utility should be provided from the service and the corresponding cash flow should be earned.Otherwise AVS that cannot capture enough value will be forced to find creative ways to fill this fee, such as by increasing inflation in native tokens, or they will eventually face the problem of business shutdowns.

The prerequisite for re-pled is that leasing capital is cheaper than purchasing or local construction pledge.When put together, the size and cost of security can really reduce costs.Just like many businesses with heavy physical inventory, leasing is often the right decision for early or immature businesses.

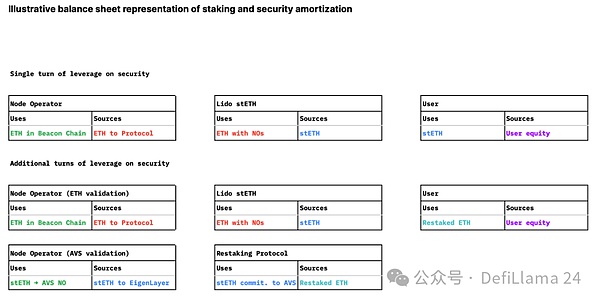

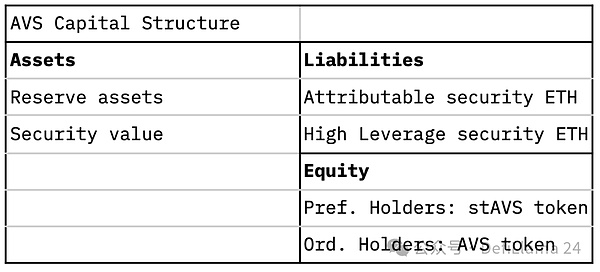

From the balance sheet perspective, we shifted from the linear, single-time leverage of user equity to a multi-layer, leverage security model with different security needs and amortized capital.This comes at the expense of increasing the leverage risk to the underlying collateral.

From the AVS perspective, amortization security in leasing with ETH collateral is a financial engineering that looks a bit like debt relative to equity.We assume that the need for security will be relatively inelastic because it is an external variable.

The more AVS provides security for more assets, the higher the demand for collateral will increase the cost of re-pending, but for the same amount of assets, there is no pressure to increase security – although there is a high probability of local panic,If the security collateral is withdrawn, the re-collateralization fee becomes more expensive.

The security cost will be the supply and demand balance of replenishment fees.Assuming that if AVS fails to meet its payment obligations, the reprivators will have no motivation to provide secure collateral and will withdraw their pledge, thus making the new guarantee more expensive.If there is more re-staking collateral available, the cost of security should be reduced under other conditions, as is the case for both AVS and re-stakingers.

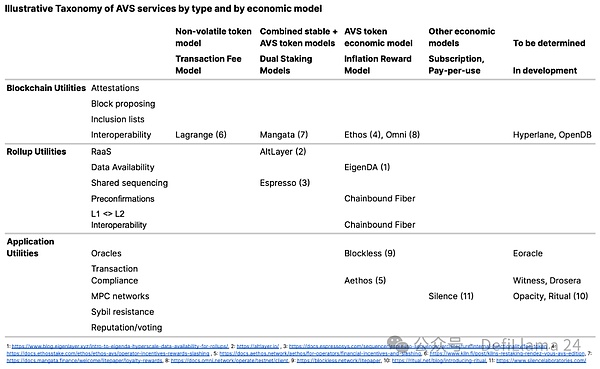

What are the different types of AVS?

At the time of writing this, it’s a bit of an illusion, as there are no AVS available yet, although some are expected to launch on the mainnet soon.Therefore, the classification of AVS is quite speculative.However, we can imagine a scenario of virtual services and try to classify them in a useful way to identify value and risk drivers.From an economic perspective, relevant classifications may look at how AVS creates value and motivates participation.

The following is a non-exhaustive list of AVS at present, as new service types may appear in the future, which have less dependence or correlation to the underlying Ethereum base layer.

We expect that replenishment fees and their relationship with the AVS monomer economy will be the only source of truth about whether AVS can continue to lease security through replenishment ETH and bring attractive returns to replenishers.The rewards received by the re-pledger are also piled up on the axis of risk from small to large and reward variability from small to large.

The easiest way to evaluate the sustainability of AVS’s staking security model is to make an analogy by drawing on debt service coverage (DSCR) in traditional business:

DSCR = Income / Total Debt

We can adjust it slightly to accommodate restaking and generate restaking operational affordability ratios (ROAR):

ROAR = AVS cash proceeds / Total cost of secure rent seeking

Among them, AVS cash income can be broken down into:

AVS Cash Income = Profitability x Efficiency x TVL = AVS Income / Sales x Sales / Assets x Assets

Without any AVS operational history, we can’t really tell what level of ROAR is enough now.Simply put, AVS must be able to structurally cover the security costs it needs, or it needs to rethink its security needs and find other solutions.If an AVS is too small to afford to pay for L1’s verification in hard currency ETH collateral, one way to bridge the gap is by issuing native tokens similar to equity until they can reach a scale of slowing down dilution.The proportion of fees paid in non-volatile tokens or dilution through native tokens will determine the choice of AVS from the creditor’s perspective or equity investor’s perspective.

However, this introduces a concept similar to the benefits sustainability faced by the new Layer 1 blockchain, which must increase its issuance to pay for new security.The reflexive danger of native token is that few crypto-economic protocols find a sustainable balance between issuance and issued tokens.Ethereum is one of the few major ones at the network level.

AVS’ tendency to issue its own tokens may be at least partly due to the potential market inefficiency in the crypto market, which reduces the effective capital cost relative to native tokens from other sources of capital.While equity issuance will be a heated debate in traditional commerce, often the most expensive source of funding for businesses, crypto appears to benefit from an over-inflated P/E ratio, which overall reduces the cost of capital for new tokens.

To assess whether such issuance is sustainable in the long term, the reprivator must determine whether the price return of the native token (return growth x multiple growth x supply changes) will overcome the initial inflation period.Rental secure boot boot is an operational leverage that can help AVS scale faster than they have to guide their own L1 networks themselves.Distributing native tokens also has additional market benefits, potentially binding participants in the AVS ecosystem together in the long run.

However, there is still a bit of a familiar problem here, as the main purpose of re-staking is to provide lower cost security through amortized collateral and to avoid the inflation cost issue that leads a brand new L1 from scratch for crypto-economic security.

How to measure the cost of trust?

In traditional finance, the total return of equity investors is the sum of price returns and dividend returns.Right now:

Total return = Price return + Dividend earnings

Price returns can be further broken down into 3 value drivers:

Price return = earnings growth x earnings multiple growth x token supply changes

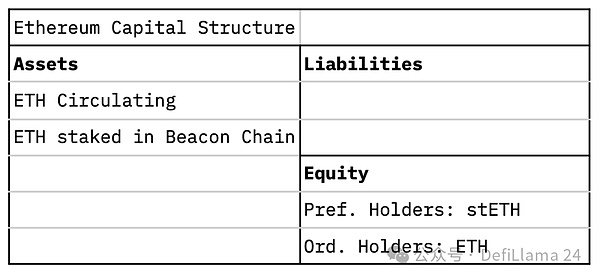

Dividend earnings are additional interim cash flow granted to the capital provider.All capital providers typically receive the same dividend yield.

In decentralized trust networks like Ethereum, there is a medium-term cash flow granted to work providers.The work in the Ethereum context is to participate in the verification transaction by providing 32 ETH as collateral for the security of the crypto economy.Unlike dividend earnings, work earnings depend on whether the ETH holder pledges.

Total return = ETH Price return + Job gains

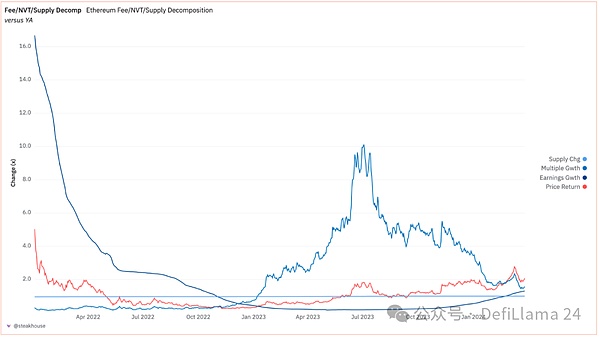

This “work gain” is essentially negative for non-stakeholders as they are diluted by a new issuance of ETH rewarded to the stakeholders.To some extent, pledgers can be considered preferred shareholders, who are entitled to dividend payments, while pledgers can be considered common shareholders, who are subject to dilution.There is a hypothetical example in the appendix that illustrates the impact of whether an ETH holder pledges on its total returns.Meanwhile, the following figure shows the breakdown of ETH’s price returns, including changes in Gas expenses in USD, changes in network multiples, and changes in supply growth.Multiply these three components over a specific period equals the price return of ETH.

Source: Dune. https://tinyurl.com/2yzvxk4u

The re-pled economy adds a new dimension to the capital structure.Lease crypto-economic security AVS from ETH re-pledgers will have quasi-debt/equity characteristics.In the context of the theoretical AVS balance sheet, the mixed nature of the replenisher comes from the replenishment rewards that will sometimes be paid in ETH, sometimes in AVS’ native tokens, or a mixture of the two.If the reprivators get their income in the form of ETH, they will be more like AVS’s “debt investors”; the reprivators do not explicitly benefit from the upward potential of the AVS economy.If the re-pledgers earn profits from AVS’s native tokens, they will be more like AVS’s “equity investors.”In addition, depending on the number of times ETH is re-staking, there will be the concept of “priority” and the perceived security of re-staking ETH.This depends on the number of times ETH is restaked.The probability of “default” of re-staking ETH may increase exponentially as the number of times the same ETH is re-staking to secure another AVS.In the most favorable case, the “attributeable security” that is exclusively retained by AVS and paid for by ETH resolute proceeds can be considered “high-level debt.”As ETH is restaked in various AVSs more often, ETH will be considered “primary debt.”

If the ETH re-stakers in AVS receive the reward in the form of ETH, their total return is simply the re-stake income.In other words, the re-pledgers are not directly exposed to the risk of the upward potential of the AVS economy.If ETH restakers receive rewards in AVS’s native tokens, their total returns will include the price return component of the AVS token.Therefore, re-pledgers are concerned about the upward potential of the AVS economy in terms of the degree to which they hold issuance.

Total return = ETH price return + ETH pledge income + re-pled income

in

Re-staking Income = Re-staking Income (non-volatility component % + AVS token % x AVS token price return)

The trust cost of a single AVS: The above tells us the rewards required by the restakeholder, so the “trust cost” of the AVS network depends on three main factors:

•The number of times ETH supplied to AVS is re-staked (i.e., the fewer times ETH is re-staked = the lower the trust cost)

•The re-pled person receives the re-pled reward (i.e., native token = higher trust cost)

•The price return of AVS tokens will reflect the business foundation in the long run

With this, repants who receive repentee rewards with AVS’ native tokens will need to carefully consider the long-term sustainability of the network.The chart above shows the price return breakdown of Ethereum.We can imagine that similar exercises can be based on the restakers’ perception of the feasibility of AVS business, on a forward-looking basis for the AVS they will restake.

The trust cost of multiple AVS: The role of an AVS operator or LRT is to aggregate the total lock value (TVL) from the restaker in order to restake in multiple different AVSs to increase the return on restaken ETH.We cannot quantify the correlation between different AVS and the possibility of increased cut losses.Nevertheless, we acknowledge that the expected loss of a single cut event will increase as ETH is restaked multiple times in various AVS.

Trust Return Formula: Given the above, we have come up with a simple intuition about “trust Return” in the restake economy.Right now:

Return of trust = ETH price return + ETH staking income + re-staking income – default loss

AVSAgainWhat should be the pledge return?

At present, there is no history and no concept of how much a restaking AVS can afford as a secure budget for ETH collateral.We propose a simplified framework for evaluating a hypothetical AVS that, if viewed as a business, might be affordable, taking into account constraints such as returns that its token holders may require.

In short, the level of security AVS promises to provide for its business should be proportional to the value or activity performed on the AVS.Inadequate commitments could disrupt AVS or disrupt its operations.Too much commitment poses the risk of bearing unaffordable expenses that AVS users cannot obtain additional marginal benefits.

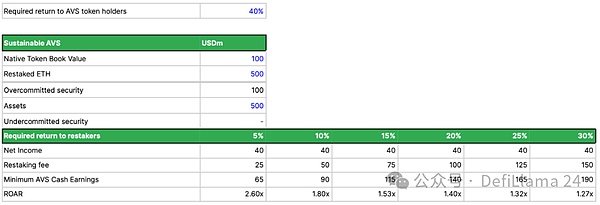

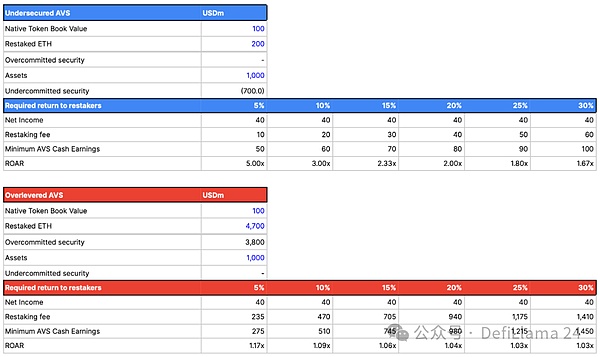

Leveraged work income (AgainPledge)

This is a schematic, simplified representation of what the AVS balance sheet needs to look like and the minimum level AVS cash earnings need to be reached on an annual basis to achieveAgainThe different rates of return required by the pledger (i.e. re-pled fees or benefits).We also demonstrate the corresponding ROAR ratios to signal sustainability and compare with situations where AVS is not secure enough to run its services and situations where security is too much to afford.

To clarify the actual expectations of these reverse engineering revenue thresholds: To date, only a few projects on Ethereum generate more than $100 million in revenue each year, including Ethereum itself.

Today, EigenLayer and higher leverage derivatives (such as Liquid Restake Protocols) use the concept of points to attract initial capital to commit their collateral for re-staking.This is a wise move because it avoids early commitments token dilution and allows these protocols to change the value evaluation criteria for points in actual dilution or hard currency payments.By gaining enough bargaining power through higher commitment capital, they can decide not to give any monetary value at all, realizing the 0-based cost of capital.

Prior to this, the market’s expected pricing for points was within the range of about 40%.Using our earlier framework, this suggests that in order for ROAR to be safely greater than 1, AVS should be able to generate a return on equity equivalent to at least 40% of its native token.For low-margin crypto services, especially if asset efficiency is less than 100%, i.e. underutilized TVL to leave a reserve of loss, the only way for service operators to move forward is through a higher leverage balance sheet.

Who are AVS customers?

Many AVS can be considered to provide value-added services to other infrastructure providers (such as roll-up).In this sense, AVS can be regarded as a B2B (business to business) service, not a B2C (business to consumer) service.

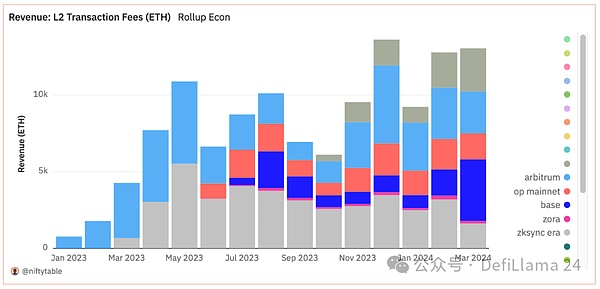

The market potential of AVS serving Rollups today will be limited by Rollups’ revenue.The 12.8k ETH Gas fee generated by top Ethereum L2 in February means that Rollups revenue runs at 153.6k ETH.Let’s assume that all Rollups revenue can be redistributed to AVS services.Currently, Eigenlayer has 3.535M re-staked ETH.This means that in the most generous situation where all L2 revenue can be redirected to AVS, the re-stakeholder will receive an annualized return of 153.6k/3.535m = 4.3%.We note that this annualized earnings do not take into account any considerations of cutting risks and “default losses”, which we will explain in the next section.

Source: Dune. (@niftytable), https://tinyurl.com/2dbs87do

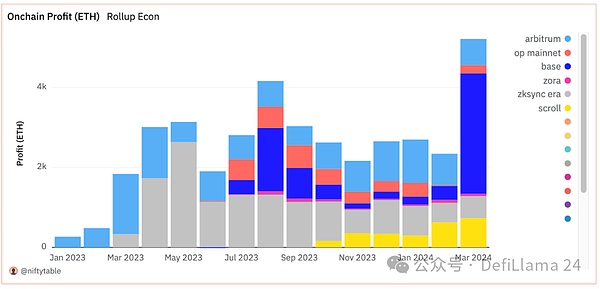

If we limit market opportunities to sequencer profits (i.e. Rollups revenue minus Ethereum call data cost), the number will shrink to an annualized return of 54k/3.535m = 1.5%.

Source: Dune. (@niftytable), https://tinyurl.com/2dbs87do

In fact, our suspicion is that most Rollups will try to protect their serializer profits and choose to provide cost savings (e.g., EigenDA provides cheaper data availability than Ethereum) or address real technology gaps (e.g., interoperability)service.Therefore, in the early stages of AVS launch, most of the staking income is required to be paid for AVS’s native token issuance.As we mentioned in the trust cost formula we came up with above, issuing in native tokens instead of ETH will increase the trust cost of AVS.

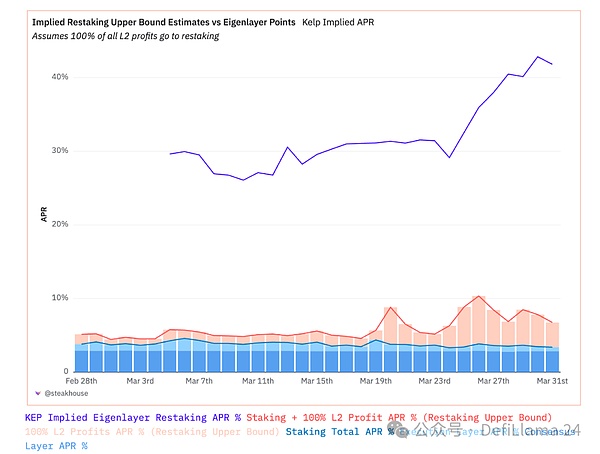

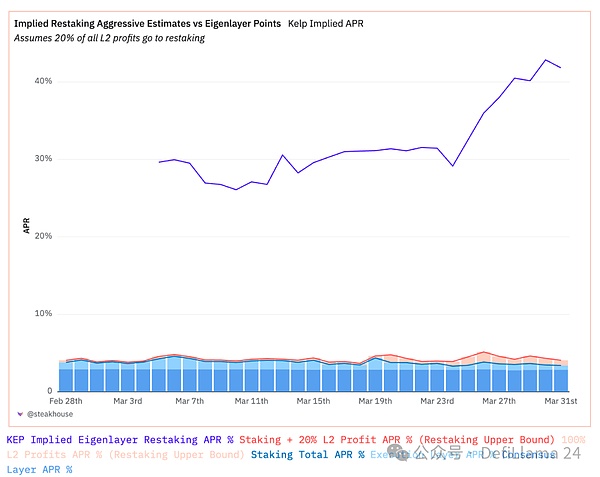

Market dynamics may change interestingly, as the annualized percentage of restaking of +40% market expectations (embodied by points) competes with the reality of AVS monomer economics and scale.This expectation is more challenging when compared to a lower share of profits that L2 may provide re-staking proceeds.

Source: Dune. (@steakhouse), https://tinyurl.com/233kr6qj

Source: Dune. (@steakhouse), https://tinyurl.com/233kr6qj

Assuming that all Tier 2 profits are paid to the reprivator for sharing security—which is at best an impossible upper limit estimate—we leave the reprivator with approximately 1.5%±0.5% reprivator gains.If that profit share reaches a more reasonable but still aggressive level, i.e. 20% of all Tier 2 profits are attributed to the repants, then our earnings are about 10%.The rate of return on replenishment is 0.75%±0.25%.This is at least related to an estimate from the emerging liquidity resolidated token (from Jason Vranek of Puffer Finance), which recently estimated that the resolidated yield of about 0.5% is “good”.

Losses of default: cuts and other risks

The risk of re-staking must be considered with caution, as user collateral is actually re-staking to support multiple major verification services.This means that the re-stakinger’s collateral is likely to be cut under completely new conditions, depending on many special factors beyond crypto-economic verification activities.

EigenLayer’s risk document confirms very clearly and convincingly that it will not pledge the pledged token again.However, there is the concept of leverage, as tokens are reused many times, which may be more similar to leverage in the sense of bank multiplier.

The risk of re-staking ETH starts with the reduction of pledge ETH or operational risks.In the earnings management study for Lido DAO, we found that large risk reduction (one operator offline for more than 7 days) would have an effect of approximately 0.01% on all stETHs.Operational risks are more destructive in tail risk events such as Prysm errors and massive withdrawal queues (0.315%).

These risks are superimposed with the risk of replenishment.When restakingers promise their ETH to protect AVS, ETH is “at risk” in a way similar to Ethereum staking.The node operators entrusted to perform verification activities must operate correctly to avoid user collateral being cut.There is no final version of the cut conditions that will affect the restakeholder, so we can only guess how likely this is.Priority is to keep simple and easy to operate and not change node requirements to prevent high corruption costs.

We don’t think these risks are completely impossible.Underwriting AVS will likely prove very similar to the credits of underwriting ordinary commercial loans, and capital now at risk is somewhat affected by operational and commercial risks, not just pure consensus algorithmic math.It is also worth mentioning that there is also a moral hazard effect, as the AVS that cannot afford local L1 to protect its activities will be incentivized to seek rental capital at a lower cost, similar to the moral hazard underwriting of insurance.

We can qualitatively frame the impact of losses, including cuts, as default losses, similar to traditional financial analogies.Default Loss Captures the additional risk of ETH holders opting in:

•For non-pled persons, the default loss rate is 0

•For local stakeholders, the default loss rate is divided by the probability of cut * the loss rate and additional special risks, depending on the pledge method chosen.

•For reprivators, default losses include the previous content and add portfolio default losses for reprivate services: some text

○ Special losses from cuts or other operational errors

○ Related losses between a cut or loss event on an AVS and another

○ Related losses between Ethereum staking and AVS

In other words, we can only guess what the source of the loss of re-staking is.

This means that the default loss actually increases with the number of re-pending of the ETH collateral.The more chances of correlation occur, the greater the possibility of a loss of income events.

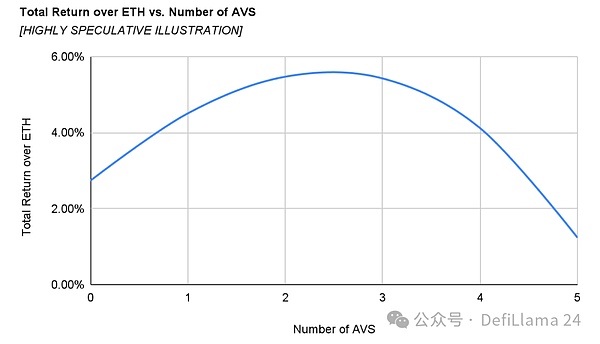

That is, there are various mitigation measures that can mitigate potential losses that may result from cuts or operational errors.The maximum loss of stakers on Ethereum is basically limited to 50% of each validator’s collateral.Similarly, we can expect that there will be an upper limit on the correlation between AVS and between AVS activity and Ethereum staking.We expect that the final optimization curve selected by the AVS will produce a decreasing return due to the default loss rate, thus possibly having an optimal maximum number of AVS allocations.

The curve below assumes that each AVS in the set is the same and the average resolution fee is about 5%, which is the maximum estimated upper limit possible for Rollups revenue.

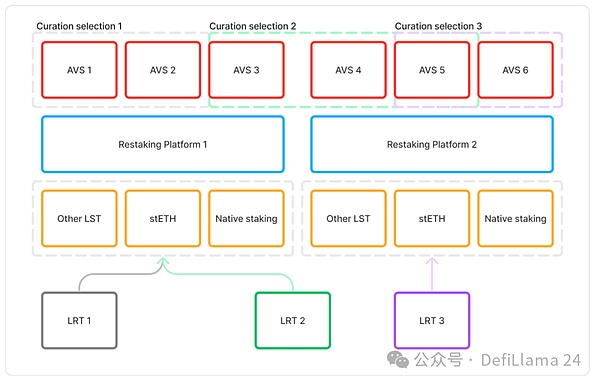

Liquidity re-pled agreement

The Liquidity Re-Staking Agreement (LRT) introduces new dimensions of aggregation and liquidity.When considering the balance sheet, unlike the current pledged tokens (LSTs), LRT’s asset allocation strategy involves more diversified risks and returns.Although the management of node operators is a key feature of LST, they tend to be generally consistent in similar dimensions and compete fiercely in price and performance.

The evolution of LRT as an LST may find that the final product does not match the user’s expectations of the underlying assets.When mapped into the familiar fiat financial system, LST plays the role of a monetary policy transmission tool, similar to a core bank deposit or government debt instrument.Where stETH is the underlying asset, LRT is fund management, i.e. more similar to structured products or bond funds.

The so-called benefit brought by LRT is AVS management, that is, by incurring AVS re-staking fees, to maximize the returns of re-staking ETH, while minimizing default losses.The improvement of this decision space must be operated in a limited profit margin to be shared among more participants.

If the returns are insufficient, meaningful differentiation cannot be reflected, and LRTs may be forced to take more risks by allocating to AVSs with higher balance sheet leverage, or simply and elegantly failing or competing with LST by default.

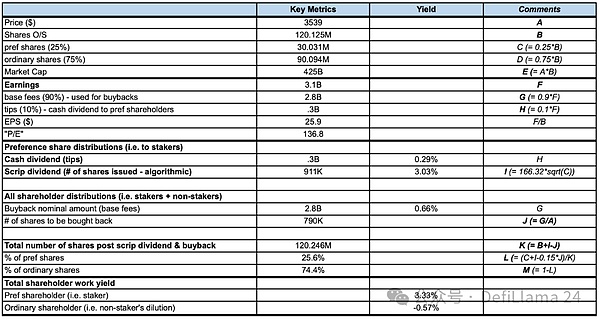

Appendix: Job benefits

We use hypothetical numbers and familiar equity analogies to illustrate Ethereum’s concept of “work gains”.Ethereum’s “Capital Return Policy” setting for its token holders is as follows:

The pledger is a preferred shareholder and is entitled to cash dividends (i.e. user tips and MEVs) + stock dividends (i.e. new token issuance).These two constitute the total reward of the validator.

The non-pled person is a common shareholder.

All shareholders can benefit from stock buybacks (i.e., user Gas burn).

As shown below, pledgers gain higher returns at the cost of non-pledgers.Specifically:

The pledger’s work earnings are 3.33%, which consists of 0.29% cash dividend earnings and 3.03% “stock dividend” earnings.

The non-pledger’s work income is -0.57%, which is caused by the dilution of the “stock dividend” (i.e., the issuance of new tokens) to the pledger.

In short, cryptocurrencies provide a uniform price return for all token holders, but offer different levels of “work gains” depending on the type of token holders.This means that people who provide jobs may have a different view of the “fair value” of tokens than people who do not.

Job Return Model Overview, April 2, 2024, Reference: https://dune.com/steakhouse/eth-decomposition