Original author: Ansgar Dietrich, Casparschwa, Ethereum Foundation

This article comes from the discussion of Ansgar Dietrichs and Casparschwa on the eth research forum on the Ethereum staking mechanism and ETH issuance model.Geek Web3 has sorted out and deleted this.These views were proposed in February 2024, and some data may be biased, but their analysis of the Ethereum staking economic model is still worth referring to, and some of the conclusions are still not outdated.

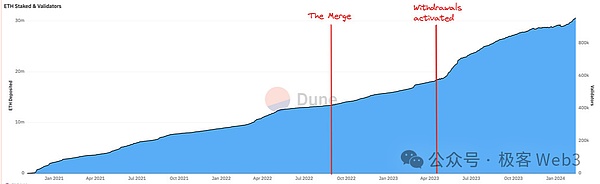

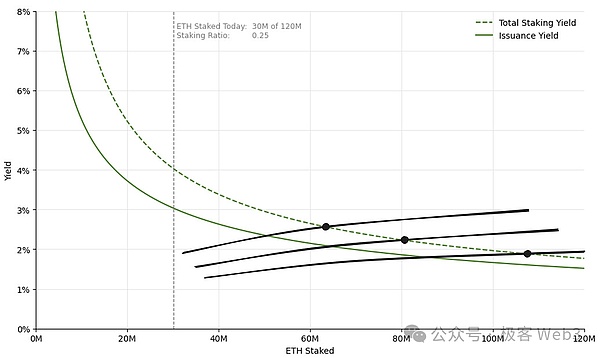

text:at presentETH pledged on Ethereum has reached 30 million, accounting for 1/4 of the total (this is the data from February this year)This ratio is quite considerable and is still rising, with no signs of slowing down.The figure below shows the change in the ETH pledge volume over time, and it can be clearly seen that it is showing a continuous growth trend, and this trend will continue for a long time.

future,A large proportion of the new stakes of ETH will be affected by LST (liquid staked tokens), such as stETH.This will gradually increase the usage rate and monetary attributes of LST, but this may have negative effects.

First of all, LST has a network effect. Larger LST projects will erode all liquidity in the track and eventually form a winner-takes-all, which will intensify the competitive landscape of the LST track.In addition, if LST surpasses ETH and becomes the mainstream currency on Ethereum except Gas Token, users will face the risk of counterparty brought by LST.Currencies on Ethereum should be as trust-free as possible in order to truly achieve economic scalability.

(“Opposite risk” refers to the other party’s possible default/unable to fulfill its obligations. In the LST scenario, the “Opposite risk” mainly includes theft of user assets, the slippage of LST price, and the depreciation)

At present, there is no hard and upper limit for ETH pledge, and in theory all ETH can be pledged to obtain profits.LST has significantly changed the cost structure of pledge, and almost all ETH may be pledged.thereforeWe believe that Ethereum’s economic model and pledge model should include dynamic adjustment policies to allow the pledge ratio to be adjusted within a certain range.In this way, Ethereum can ensure security at a controllable cost scale and avoid the occurrence of negative externalities.

In this article, we propose some urgent issues to be solved for Ethereum’s economic model.

Current status and future trends of ETH token issuance strategy

Before the discussion begins,Let’s first explore which long-term pledge models are feasible under the current ETH token issuance policy.Ethereum’s security relies on a certain proportion of token staking, which can be summarized as POS Ethereum itself has “demand to attract staking”.The demand for pledge is clearly stipulated in Ethereum’s monetary policy. According to the actual pledge weight, the agreement will adjust the additional ETH issuance accordingly and increase the pledge rewards for individual nodes.

However, the pledge intentions of ETH holders are diverse and complex. We can only make reasonable inferences based on existing information and roughly estimate the long-term impact of changes in pledge intentions on the participation of pledgers.

The supply and demand relationship curve of ETH pledge: exchange additional ETH for security guarantee

Validator node staking ETH will allow the protocol to obtain security guarantees, and the protocol will distribute token rewards to ETH stakeholders, which is a win-win mechanism.(For space limitations, this article will not discuss specific issues such as “What level of security needs to be achieved”. If you want to know more, please refer to the article Paths toward single-slot finality) The benefits of Validator mainly come from two parts:

Part One:The reward issued by the agreement based on a fixed income curve; (that is the reward assigned to pledge participants through additional ETH every year)

Part 2:The MEV benefits obtained by Validator during the block production process.

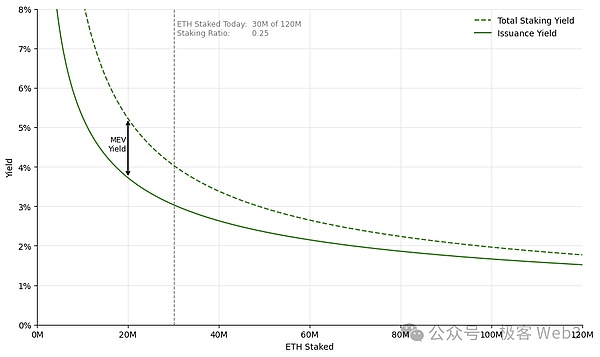

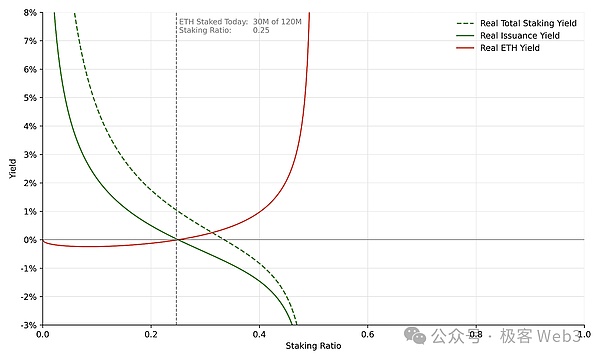

(The horizontal axis of this figure shows the pledge participation degree of ETH, and the vertical axis is the pledge yield rate, which describes the pledge income that the Ethereum protocol is willing to provide to meet different pledge rates. We can regard the Ethereum protocol as the buyer pledgee.For sellers)

Note: To understand the following, readers may need to have a simple understanding of the supply and demand relationship curve in economics.

ETH increase yield curve (green solid line):As can be seen from this curve, the staking rewards provided by Ethereum to a single node will gradually decrease as the number of stakers increases.When the participation of ETH staking is low, the system needs more rewards to encourage more people to pledge ETH; when more and more people participate in pledge, the marginal contribution of a single verifier to network security will be reduced, and the rewards for pledge will be rewarded.The demand also decreased.

Total pledge income curve (green dotted line):The fixed additional issuance income of ETH plus the MEV income constitutes the total pledge income of the pledger.It should be noted here that the calculation method of MEV yield is: the total MEV yield (about 300,000 ETH last year) divided by the total pledged ETH.

Since the total MEV returns are basically fixed, as the number of validators increases, the MEV returns will drop rapidly, which ultimately causes the pledge yield to approach the simple ETH issuance rate.It is worth noting that Ethereum’s MEV returns have been quite stable over the past period of time (see MEV-Boost Dashboard), and while this may change in the future, it is temporarily considered fixed to simplify our discussion scenario.

From the above curve, we can read two key messages:

-

In order to avoid too low staking participation, Ethereum has set high returns when staking participation is low to attract more stakingers.

-

The marginal utility of each stakeholder decreases, that is, as the staking participation increases, the additional issuance rate of ETH tokens gradually decreases.

However, the above-mentioned pledge yield curve fails to ideally adjust pledge participation.First, this curve cannot effectively limit the threshold of the pledge ratio. Even if all ETH is pledged, the pledge incentive will remain at about 2%.In other words, at the incentive design level, Ethereum does not accurately control the final staking ratio.Overall,In addition to using high incentives to ensure the system has the lowest security guarantee in the initial stage, the agreement does not guide the pledge level to a specific range.

It should be noted that the above mentioned only has nominal returns and does not consider the dilution effect brought about by the additional issuance of ETH itself.As more ETH is issued, the dilution effect will become more significant.In this regard, we temporarily ignore the influence of the dilution effect and will be discussed in detail later.

Supply-side analysis of ETH staking

The above article discusses the demand curve for pledge, which is the pledge income that the Ethereum protocol is willing to provide to meet different pledge ratios.Now we turn our attention to the supply curve.The pledge supply curve demonstrates the pledge willingness of ETH holders at different rates of return and reveals the conditions required for different pledge participation levels.

Generally, the curve will tilt in the upper right, which means that the network needs higher incentives to achieve higher staking participation.However, since pledge intention cannot be directly observed or accurately measured, the shape of the supply curve cannot be specifically depicted, and we can only infer through qualitative analysis.

In addition, the supply curve is not static, and we will explore the changes in staking costs over time and how this change affects the pledge decisions of ETH holders.in other words,Changes in pledge costs will lead to displacement of the supply curve, causing ETH holders to change their demand for pledge incentives.

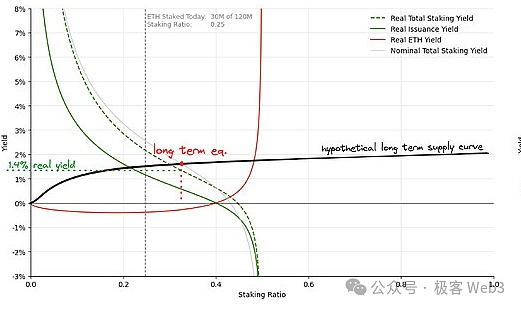

We can only fit historically observable pledge levels into an approximate pledge supply curve, and the intersection of the demand curve and supply curve at each specific time point reflects the historically truly achieved pledge participation rate.

The horizontal axis of this figure is still the ETH pledge participation degree, and the vertical axis is the pledge yield.As shown in the figure,Since the launch of the Ethereum beacon chain, the total amount of pledged ETH has continued to increase, and the supply curve of pledged volume has moved downward.Even under lower pledge proceeds, ETH holders’ pledge willingness will increase.Judging from the historical trend, it is a reasonable expectation that the supply curve will continue to move downward in the short term.However, what is worth discussing in depth is the issue of long-term pledge balance, and we need to carefully analyze the composition of the supply side.

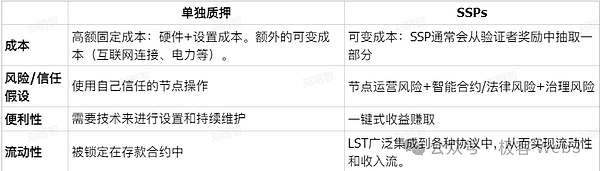

When deciding whether to pledge, any ETH holder usually considers two main factors: the benefits of pledge and the costs required.Overall, the pledge income of unit assets in the hands of the verifier is the same.However, different types of stakeholders have significant differences in cost structure.The following will provide an in-depth comparison of the differences between independent stakeholders and staking service providers (SSPs).

Independent stakeholder vs stake service provider

SSPs accept users’ ETH and complete pledge operations on behalf of users, charging a certain service fee.Normally, they will provide users with LST as pledge credentials, and users can use LST for secondary market transactions (such as stETH).For LST holders, the liquidity of these tokens depends on the overall usage of LST and the support rate of third-party agreements for it.

What we want to focus on is SSPs such as Lido that issue LST.As for those SSPs that do not issue LST, they can be regarded as a special case where the LST liquidity value is zero and will not be discussed in this article.

For most people,Individual pledge does not require trust in third parties, but the participation threshold is high and the operation is cumbersome; in contrast, LST requires a certain degree of trust, but it has significant simplicity and liquidity advantages.

After comparing these two pledge methods, we can draw two important conclusions:

1.There are obvious differences in the cost structure of independent pledges among different ETH holders.The level of technical content, different hardware conditions and operation and maintenance costs, and confidence in hosting security have made the supply curve of independent stakeholders steeper.This means that if the number of independent stakeholders is to be significantly increased, either significantly increase the staking income or improve UX for staking operations.

2.In contrast, the cost structure of users who use SSPs pledge is basically the same.The main differences are only reflected in the assessment of SSP operational risks and concerns about redemption slippage between LST and ETH.Therefore, the supply curve of SSP is relatively flat.This means that to attract more ETH holders to perform LSD liquidity staking, the required rate of return increase is relatively small, which can smoothly expand the pledge participation rate.

In addition, the cost of independent pledge is not affected by pledge participation, while the cost of holding LST may gradually decrease over time and the increase in SSP usage, for the following reasons:

1. LST’s “monetary attribute” enhancement:When the popularity of a certain LST increases, we can expect it to be supported by more and more projects, surpassing the use scenarios of native ETH, such as more DeFi protocols integrating LST, and the second-tier network uses bridged ETH by default.Liquid pledge, etc.When the ETH pledge ratio is high enough, LST may even surpass the unstaked ETH in terms of liquidity, reversing the liquidity gap between the two.

2. Reduce the risk of smart contracts:Over time, LST’s smart contracts will undergo a lot of practical tests and further reduce risks through formal verification and other methods.

3. Improvement of the robustness of the governance system:As the usage rate increases, LST-related governance mechanisms will become more mature and robust. For example, the LDO + stETH dual governance proposal reflects the progress of the LST governance system.

4. Reduced expectations for large-scale risk:When a certain LST takes up a large enough proportion of the overall market, it may be considered an existence that is “too big to fall”.Therefore, users believe that various forces in the market will promptly remedy problems when SPPs occur.

5. LSD service provider profit balance:When the usage rate of LST is high enough to make its liquidity good enough, SSPs can reduce unit service fees to maintain profitability and attract more users to participate.

Overall, the existence of SSPs and LSTs has significantly flattened the staking supply curve, which means that there is no need to continue to increase the staking incentives, which can promote the increase in the total amount of Ethereum staking.From this we can infer thatLSD will continue to play an important role in promoting the growth of pledges.However, in this way,In the long-term time dimension, pledge incentives are not a shackle for the growth of ETH staking. So how large can ETH staking reach?

Long-term equilibrium point of pledge rate

Taking into account factors such as demand and supply, we can infer the long-term equilibrium state that ETH staking can maintain.We mentioned earlier,When the pledge participation rate is low, the demand curve shows a clear tendency, but there is no clear conclusion on the specific pledge ratio that may be achieved in the long run.

We then explained that as the pledge costs and risks decrease, the supply curve will gradually decline over time, making more and more people willing to participate in pledge, and LST plays the main role.However, the shape of the supply curve itself cannot be quantitatively analyzed, and it is not clear whether it is steep enough to make a reasonable adjustment to pledge participation.

Therefore, the equilibrium point of the overall pledge ratio cannot be accurately calculated, and there are broad possibilities, which may even be close to 100%.The figure below reflects that even if the supply curve varies in the long term, it may cause displacement of the equilibrium point of the pledge ratio.

In fact, the most important thing is not how high the pledge participation rate will reach, but that once this high pledge rate occurs, it will bring a series of hidden dangers.This article proposes some policy adjustment suggestions to prevent this from happening.

Analysis of pledge ratio: Under what circumstances is the better if the pledge rate is small

The pledge rate can be defined as the ratio of the ETH pledge volume to the total ETH supply. The current total supply of ETH is about 120 million, of which about 30 million are pledged, with a pledge rate of about 25%.Before exploring the potential problems caused by high staking rates, we must first figure out a standard:

What level of staking rate can ensure the security of Ethereum.According to a previous discussion record by the Ethereum Foundation, we can know that the current staking level is enough to ensure the economic security of Ethereum.

This brings up a problem-If the current staking rate can already ensure network security, is it necessary to pursue a higher staking rate and achieve “over-security”?In our opinion, although high staking rates can enhance network security, they may bring about some negative externalities, affecting the operation of ETH holders, independent stakeholders, and even the entire Ethereum protocol.

Network Effects of LST Currency Attributes (LST): Refusing to Take Risk

LSTs are competing fiercely for the issue of monetary attributes.Due to the existence of network effects, this competition often presents a “winner-takes-all” situation.As the application field of LST continues to expand, its practicality will increase accordingly, and its market share will gradually increase. The monetary attributes of LST will be strengthened in many aspects, such as on-chain and off-chain integration, liquidity, and resistance.Ability to manage attacks, etc.

In a high staking rate environment, if a single SSP controls most of the staking ratio, it is likely to be considered “big and not overwhelming”.If most ETH is pledged to the SSP, it is difficult to have a way to effectively punish it.If a dominant SSP penetrates into the core of Ethereum protocol governance, but does not have to bear corresponding responsibilities to users, this centralized governance risk will undoubtedly have a profound impact on Ethereum’s decentralization.

If most ETH participates in liquidity staking, in fact, in most scenarios except Gas Token, the real currency will be LST.However, LSTs issued by ETFs, CEXs, or on-chain staking pools are accompanied by different trust assumptions and are at significant risks.Ultimately, users will inevitably bear additional risks from operators, governance, laws, and smart contracts, which is obviously not an ideal state.

In addition, although LST boasts that it can restore the liquidity of pledged ETH, its effect as a collateral in DeFi is definitely not as good as native ETH.If the Ethereum network wants to achieve true economic scalability, its currency must be as trustworthy as possible, preferably using ETH itself.

Minimum feasible circulation – serving user experience

Ethereum’s minimum issuance MVI is the minimum issuance required by the Ethereum network under the premise of maintaining its security and functionality. It aims to balance the security and ETH inflation rate of the network.According to the MVI principle, it is necessary to ensure that there is sufficient pledge participation to ensure the security of the agreement, but the amount of pledge should not be too much.

When the pledge level reaches a certain critical point, the security of the protocol is sufficiently stable. At this time, the marginal utility brought by the additional pledge will gradually decrease, and negative effects may even occur (for example, increasing network load and diluting the rights and interests of ETH holders).wait).also,Pledge is the basic service required by an agreement. The agreement should pay reasonable compensation for pledge to attract users to participate, rather than force users to participate due to asset dilution pressure.

If the ETH issuance continues to increase, it will cause all ETH holders and stakeholders to face greater dilution risks, but SSP will not be negatively affected.Because the ownership of pledged ETH does not belong to the SSP, SSP only obtains income by charging service fees, and dilution of ETH value has nothing to do with it.Not only that, if more people participate in LSD pledge to hedge inflation, the service fees collected by SSPs will increase.

Assume a situation:The participation rate of Ethereum pledge is 90%, the annual yield of pledge is 2%, the liquid pledge accounts for 90% of the total pledge value, and the average SSP fee is 10%. In terms of conversion, there will be a fee equivalent to 0.16% of the market value of Ethereum every year.Paying to SSP is about 200,000 ETH, which is about 530 million US dollars at the current price.This $530 million is actually an invisible tax on all ETH holders.

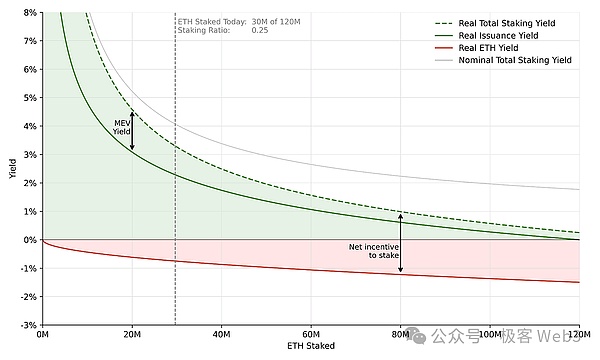

Real rate of return: Nominal rate of return – dilution effect

Similar to the nominal interest rate and real interest rate in finance, the actual rate of return is the real rate of return obtained after excluding the dilution effect in the nominal pledge income of ETH.As more and more people participate in staking and Ethereum inflation, the nominal income brought by ETH staking will be gradually diluted, and the actual income can more clearly reflect the real incentives of staking, while the pledge income we discussed earlierAll curves are nominal returns curves.

The above figure reflects the impact of dilution effect on the income of pledgers and non-pled ETH holders, respectively.For ETH holders who do not pledge (shown in the red line in the figure), their real returns are obviously negative because their nominal balance remains unchanged but suffers from the dilution effect of inflation.To clearly describe this effect, we can divide the pledge ratio “S” into two situations for analysis.

When the pledge ratio is low (the part on the left side of the curve), the actual return curve (green solid line) is closer to the nominal return curve (gray solid line).This is because there are fewer pledges and fewer rewards distributed by the agreement through additional issuance of ETH, so the ETH inflation rate is very low and the dilution effect is light.In this case, the main incentive for pledge comes from positive returns, that is, the green area in the graph.

When the pledge ratio is high (the part on the right side of the curve), the gap between the actual income and the nominal income curve gradually increases.As more and more pledgers participate, the increase in ETH issuance increases and the dilution effect becomes more obvious.In addition to the reduction in actual returns, part of the incentives for pledgeers come from “dilution protection”, that is, hedging inflation through pledge.In extreme cases, when the pledge ratio is close to 100%, the actual pledge income will only be composed of MEV income. At this time, the inflation rate of Ethereum will be very high because additional tokens are required to reward the pledger.

To sum up,The biggest difference between high and low pledge ratio is the difference in the composition of pledge income.Under the low pledge ratio, users will obtain actual positive returns. After the pledge ratio increases, due to the high inflation rate, users can only obtain less returns to offset the dilution effect, that is, “dilution protection”.The higher the pledge ratio of Ethereum, the more newly issued ETH, and the higher the nominal income of the pledged users. However, high nominal income does not mean high actual income.

It should be emphasized that this change in profit composition will not reduce the incentive effect of pledge.If you only look at the results, dilution protection and positive returns from real money are also attractive to users.However, two different natures of benefits have very different meanings for users:When the pledge ratio is low, pledge is a profitable service paid for by the Ethereum agreement; on the contrary, when the pledge ratio increases, pledge becomes a helpless move to hedge inflation.

therefore,If the pledge ratio moves to the highest right, we may fall into a worst situation: the actual gain provided by the pledge is extremely limited and also poses a threat to asset dilution to those who are reluctant to accept LST.

Under the same pledge policy, any pledger will definitely choose a strategy that has higher actual returns for him.However, in Ethereum’s protocol design, users cannot choose at all, because the issuance curve of the protocol determines the final equilibrium state of the pledge (when the long-term pledge supply curve is fixed). For profit considerations, any user can only choose to participate in pledge.A strategy.

Poor feasibility of independent pledge

The cost of SSP is fixed, the more pledges, the lower the unit cost, and it is born with the advantage of economies of scale.As the number of ETH managed by SSPs increases, its marginal efficiency will also be improved, which can reduce costs and charge lower service fees, attract more users, and achieve higher profits.Based on these advantages, successful SSPs may be seen as “big and undefeated” existence, which reduces the tail risks it faces and further strengthens the scale effect.

(Tail risk: risk of extreme events. The probability of these events is extremely low, but once it occurs, it often leads to huge losses)

On the contrary, independent pledgee needs to bear all costs on its own. The cost will not decrease due to the increase in the pledge amount, but will increase due to the increase in network load.This is one of the reasons why Ethereum passed the EIP-7514 proposal.

According to the previous analysis, as more and more pledge returns are used to hedge inflation rather than obtain actual returns, the pledger’s actual returns are increasingly dependent on MEV, and MEV returns are highly volatile and will allow independent pledges.The total income of the user fluctuates.In contrast, SSP can distribute the total MEV revenue proportionally to all Validator verification nodes it manages, effectively reducing the impact of staking income fluctuations on its overall operational effect.

With the increase in the use rate of LST and the enhancement of monetary attributes, the gap between independent pledge and LSD pledge will further widen.In other words, as the pledge rate increases, the competitive disadvantage of independent pledge over LSD pledge becomes more and more significant.

In many jurisdictions, governments tax pledged income on nominal income rather than actual income adjusted for dilution effects.Through certain structural designs, LSTs can provide holders with some protection from this tax impact, which independent pledges usually cannot do.As the gap between nominal and actual returns becomes larger, the income level of independent pledgers is further left behind by LSD pledgers.

Based on this, we propose the following point:

1. Holding native ETH should be economically feasible, ensure a good user experience, and avoid value dilution problems caused by security risks, so as to better protect the interests of ETH holders.

2. To achieve true economic scalability, Ethereum’s general currency should be as trust-free/trust-free as possible.Only in this way can the robustness and wide applicability of the entire system be ensured.

3. The dilution protection of asset value has become the main incentive component of pledge, which is not ideal for pledgeers and ETH holders.Relying on dilution protection as an incentive may bring about unnecessary market fluctuations, weakening the original intention of the pledge mechanism.

4. High staking participation rate will further aggravate the competitive disadvantage of independent stakeholders in the market, which may make more users tend to use SSP for staking, resulting in centralization of staking, which is not conducive to the decentralization and security of the network.

The pledge ratio that Ethereum can achieve in the future is still uncertain. We need to take the initiative to determine an optimal pledge ratio to prevent negative impacts from being too high.Even if a high pledge ratio may be beneficial to some people, this choice should be made after careful consideration, rather than randomly affected by external factors in the market.

The ultimate goal of pledge participation ratio

I think,Ethereum’s pledge policy should be based on the pledge ratio, rather than the pledge amount of ETH.The supply of ETH fluctuates due to the influence of EIP-1559 and the issuance mechanism, and the pledge ratio can adapt to this supply change.Although the supply of ETH is currently changing very slowly, with a decrease of about 0.3% per year since The Merge, its long-term impact cannot be ignored.Establishing a policy based on the pledge ratio can maintain stability for a longer period of time without frequent adjustments.

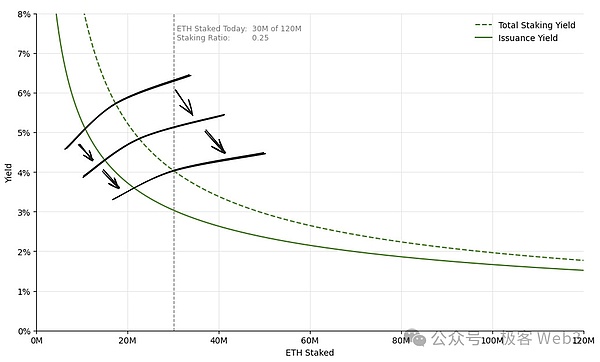

As mentioned above, although the current issuance curve ensures the lowest pledge level, it lacks a mechanism to limit the upper limit of the pledge ratio, which may lead to an excessively high pledge ratio.We believe thatA complete token issuance policy should set upper and lower limits of the pledge ratio to ensure network security and maintain reasonable participation..Specifically, the policy should strive to maintain the pledge ratio within an “optimal range that ensures both network security and avoids negative external effects.”

To this end, Ethereum can set super high rewards for too low staking ratios, and ultra low rewards or even negative rewards for too high staking ratios to adjust the staking ratio.In this way, Ethereum can regulate staking participation.The curve of this policy design can be referred to the example proposed by Vitalik, which shows how rewards can be adjusted at different pledge ratios to guide pledge behavior.

As shown in the issuance curve in the figure, rewards are generous when staking participation is low, consistent with the current policy.As the degree of pledge participation increases, pledge income gradually decreases until it turns to a negative value.In other words, the benefits of pledge will eventually be reduced to no longer be attractive, thereby inhibiting pledge behavior.However, this negative income state will not last for a long time, and the pledge participation will gradually decrease due to the regulation of this mechanism and reach an equilibrium at a certain appropriate level.therefore,A model that presents this return curve law can ensure that the pledge ratio remains within a reasonable range.

In fact, to achieve a reasonable pledge ratio range, there is no need to choose a curve where the income quickly turns negative. Those curves that only control pledge rewards to zero or near zero after a critical point may be enough to achieve the same.The effect can not only suppress excessive pledge, but also maintain system stability.

Impact of determining the reasonable pledge ratio range

The advantage of determining a reasonable pledge ratio is that it can effectively avoid various negative effects caused by high pledge ratios.However, this strategy is not without its shortcomings, and an obvious example is that the rewards faced by independent pledges in this case are volatile.Similar to the environment with high pledge rate,Under the strategy of determining a reasonable pledge ratio, a large part of the incentive source is MEV returns, which will strengthen its volatility.

therefore,Although there are many advantages of determining the pledge ratio range, it may also exacerbate the already existing returns volatility.MEV risks can be solved by introducing mechanisms such as Execution Tickets or MEV Burn, or setting pledge fees to balance the volatility of returns to a certain extent.There are also some people who object to determining the pledge ratio within a certain range. One of the representative views is that doing so may reduce the overall equilibrium return, thereby increasing the competition between independent stakeholders and SSPs, as well as competition between different SSPs..

The logic of opponents is that the reduction in overall equilibrium returns leads to insufficient fund supply. The staking form adopted by some SPPs may be more beneficial to the Ethereum protocol, but due to the lack of competitiveness of their projects, it is difficult to survive continuously and make profits, resulting in the overall EthereumLower utility.To deal with this problem, we must still distinguish between nominal and actual returns.

Although strategies to determine the pledge ratio range may reduce nominal returns, actual returns may not be affected.The following diagram further illustrates this.

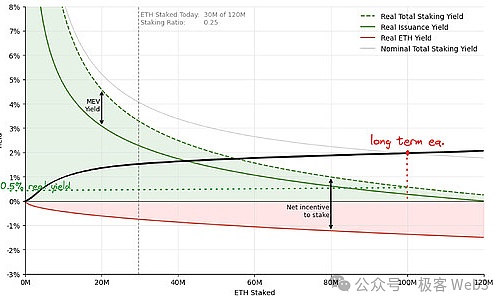

The above figure shows the situation where the system reaches long-term equilibrium when a certain pledge ratio range is adopted, while the following figure roughly shows the situation under the current Ethereum token issuance curve.Both examples are based on the same assumption: about 100 million ETH participate in staking, that is, the long-term pledge supply remains consistent, and this comparison is only meaningful.

In the figure below, most of the pledge incentives are used for dilution protection, so the actual rate of return is only maintained at about 0.5%.In the case of the left figure, the system will reach a lower nominal rate of return equilibrium point, but due to the low inflation rate, the real rate of return will increase to about 1.4%.

This example clearly illustrates,Determining the pledge ratio range will reasonably increase the actual rate of return and can alleviate the competitive pressure between pledgers.In addition, this also benefits ETH holders who do not participate in the pledge, as dilution risk is minimized.

Open question

The strategy proposed in this article is to determine a reasonable pledge ratio.However, there are some problems that need to be solved urgently.

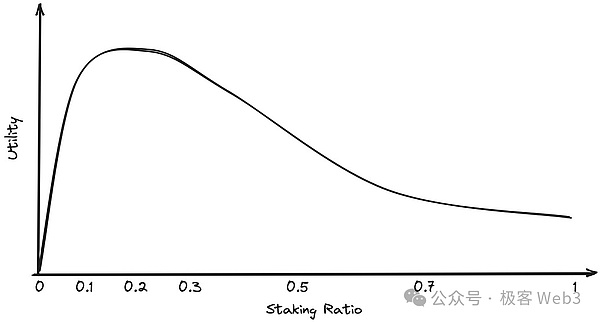

1. What is the ideal range of the pledge ratio?

Regarding the pledge ratio, we have discussed the unsatisfactory range, but have not clearly proposed an ideal pledge ratio range.In fact, this issue is quite complicated and needs to be discussed in depth within the community, and we will refer to some opinions from Vitalik and Justin.

The core of this problem is the trade-off – low staking participation increases the risk of a protocol being attacked, while excessive staking participation may have negative external effects.In order to better determine the pledge range, we can model the utility under different pledge ratios.One possible utility curve is as follows:

2. How to choose the appropriate pledge income curve to achieve the target range?

After determining a reasonable pledge ratio, the designer must also choose the appropriate pledge curve to achieve balanced participation in Ethereum pledge.Designers should carefully evaluate the advantages and disadvantages of different curves and choose the most suitable solution.At the same time, designers can continue to explore other mechanisms, such as feedback control systems similar to EIP-1559, to dynamically adjust the staking issuance curve according to network conditions to ensure that the matching degree between the curve and network requirements is optimal.

3. How to ensure incentive compatibility in near zero or negative issuance?

Incentive compatibility was proposed by Nobel Prize winner Leonid Hurwicz, which is an important principle of mechanism design. SpecificallyIf a mechanism can unify the personal interests within the system with the overall interests of the system, the system is incentive-compatible.

The original intention of Ethereum PoS is to attract validators to participate in consensus through economic incentives. However, under certain staking participation rates, issuance income may approach zero, or even negative.Although in this case, the verifier may continue to pledge for MEV income, if the conventional staking reward is lacking, the verification node may lack sufficient motivation during block production and verification, that is, when the staking issuance volume is too low, the consensus mechanism issuance mechanism.May be at risk of failure.

To solve this problem, the Ethereum protocol can charge a certain fee to all validators and redistribute the validators based on whether they are competent and re-establish incentive compatibility.However, the implementation of such a solution will increase the complexity of the protocol and therefore further exploration of its feasibility and effectiveness is required.

4. How to set the target range in a relative (staking ratio) rather than an absolute (fixed ETH quantity) way?

In fact, the pledge issuance level can also be set to an absolute number of ETH, such as 30 million or 40 million ETH. However, in order to make the issuance policy more forward-looking and adaptable, it is best to directly use the pledge ratio as an assessment parameter.In order for the issuance policy to target a specific pledge ratio, the agreement needs to control the amount of ETH pledge and supply.

5. When the pledge participation rate exceeds the target range, how to restore it to the target value?

If the current pledge participation rate is within the target range, it is of course the ideal situation, but if it exceeds this range, certain measures must be taken to reduce the pledge participation, so that some pledgeeers will lose their income and then withdraw from the pledge.Even if we use the mildest means to reduce participation, this process can have an adverse impact on some pledges.How to minimize this impact is still a problem that needs to be solved.

in conclusion

We discussed the current Ethereum staking incentive policy and token issuance plan, explained in detail the negative externalities of the issuance plan, and discussed a new policy that can solve the problem, which is to set the staking ratio within a target range..

However, given some unresolved issues, especially in the absence of validator fee mechanisms and on-chain MEV capture mechanisms, it will take some time to achieve this policy.We propose that during this period, the current ETH staking and token issuance policies will be reformed as a key step towards the target policy.

To this end, in the upcoming Electra upgrade, we have proposed a proposal to reform the pledge issuance policy (for related content, please refer to the article Electra: Issuance Curve Adjustment Proposal).