Author: Shigeru Satou

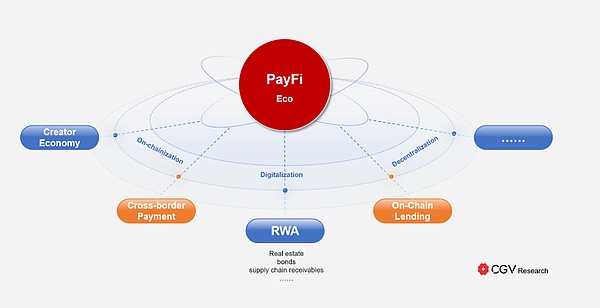

Payfi, that is, Payment Finance refers to an innovative technology and application model combining payment functions with financial services in the field of blockchain and cryptocurrency.

The core of Payfi is to the process of sending, receiving and settlement of cryptocurrencies, not trading behavior.This model not only covers the payment and transactions of cryptocurrencies, but also includes a variety of financial activities such as borrowing, financial management, and cross -border payment.By decentralized technology, PayFi makes financial activities faster and secure, and reduces friction and cost in traditional financial systems, thereby promoting seamless value transfer and financial inclusive globally.

Payfi was first proposed by the EthCC conference at the EthCC conference in July 2024 at the EthCC conference in July 2024.In her opinion, Payfi represents a new way of building a financial market, creating a financial primitive and product experience around the time value of currency (TVM).These are difficult or unrealized in traditional and even Web2 finance.

Payfi’s vision is to use blockchain technology to innovate the payment system, realize more efficient and low -cost transactions, and provide a new financial experience, create more complex financial products and application scenarios, create a integrated value chain, and form a new new value chain to form a new new value chain to form a newFinancial cluster.

The CGV Research team believes that with the development of high -performance blockchain technology, the real value of Payfi will expand and scale quickly in this environment.This expansion can accelerate the integration of payment and financial services, making cryptocurrencies more practical and efficient in daily transactions and more complex financial operations.In the future financial ecology, PayFi will become a key driving force.

Payfi: Inheritance and expand the Payment Vision of Bitcoin

The birth of Bitcoin originated from the “decentralized payment” concept proposed in its revolutionary white paper “Bitcoin: A Peer-To-TOER Electronic Cash System.”This concept not only introduces a new form of currency -Bitcoin, but more importantly, it imagines a global payment system that does not require an intermediary, which can bypass the restrictions of traditional financial institutions and achieve more efficient and transparent value valueTransfer.Nakamoto’s vision aims to completely reform the existing payment system to eliminate high fees, lengthy settlement time and financial exclusion.

However,Although Bitcoin successfully led the cryptocurrency revolution, the original intention of the daily payment medium failed to fully realize it.Bitcoin is more regarded as a means of storage, not currency for daily transactions.

Over time, the emergence of stablecoins fills this gap.By stabilizing the value of the legal currency to the blockchain, a bridge is set up between the financial systems of cryptocurrencies and the real world, which has promoted the first actual application scenario of blockchain payment.Since 2014, the growth of stablecoins has expanded, proved the strong demand for the market for blockchain payment.The stable currency users can avoid the risks brought by the fluctuations of cryptocurrency prices while enjoying the transparency and decentralized advantages brought by blockchain technology.Up to now, stabilization coins have supported about $ 2 trillion per year, close to the annual payment processing of VISA.

However, although stablecoin has promoted the development of blockchain payment, blockchain payment still faces many challenges, such as poor user experience, delay in transaction, high cost and compliance.These challenges have limited the extensive application of blockchain payment as the mainstream payment medium.

The further expansion of payment ecosystems depends on the promotion of financial instruments and financing mechanisms.In the traditional financial system, tools such as credit cards, trade financing and cross -border payment have greatly promoted global payment applications by providing liquidity and financing options.

As an emerging industry, blockchain does not necessarily need to completely rebuild a market. Instead, it can provide more valuable products and solutions through blockchain technology on the basis of the existing market.It is in this context that Payfi came into being.

By using the high performance and low -cost transaction characteristics of advanced public chains, PayFi will not only make the blockchain payment system is expected to surpass the traditional financial mechanism, but also create a global financial market with more liquidity and adaptability.This evolution is not only the return of Bitcoin’s original intention, but also a major innovation based on Bitcoin.Through PayFi, the blockchain payment system will truly release its potential and promote the global financial system to a more efficient and tolerant future.

Payfi core concept: capital value (TVM)

“Time is more valuable than money, you can get more money, but you can’t get more time.”

Time value of Money (TVM) is a core concept in finance, emphasizing the difference in value of funds at different time points.The basic principle of TVM is: the current value of a funds is usually higher than the same amount of funds in the future.This is because the currently held funds can be used immediately for investment, which generates benefits, or for consumption, thereby bringing instant effectiveness.

To put it simply, the important concept behind the value of funds is “opportunity cost”.If the person holding funds does not use the fund immediately, he will lose potential investment opportunities and cannot get potential returns.Therefore, the current value of funds must reflect these opportunities to be abandoned.For example:

——The loans and mortgages:In the bank loan, the interest rate is based on TVM. The interest paid by the borrower is actually compensation for the right to use the funds provided by the bank;

——Entering Evaluation:When assessing investment such as stocks, bonds or real estate, investors will consider the present value of future income to determine the attractiveness of investment;

——Ductory budget:When conducting capital budgets, the company will evaluate the future cash flow of different projects, and calculate its current value through discounts to help management make the most favorable investment decisions.

Payfi allows users to achieve the time value of funds in a very low cost and efficient way through blockchain technology; by using smart contracts and decentralized platforms, PayFi users can manage and invest without intermediaries without intermediaries.Fund to maximize the efficiency of fund utilization.This new model not only significantly reduces the cost of transaction, but also shortens the transaction time, enabling funds to quickly enter the market for reinvestment or other uses.

In addition, PayFi’s infrastructure provides possibilities for developing more complicated chain financial products, such as the chain on the credit market, installment payment system, and automated investment strategies based on smart contracts, which will expand to more complex financial products and application scenarios.Create an integrated value chain to form a new “financial cluster”.

Blind RWA + DEFI: Build a new financial cluster with PayFi as the core

In the financial system, real -world assets (RWA) and decentralized finance (DEFI) have unique advantages, but they also face their own challenges: RWA has a huge market size and stable value, but the liquidity is relatively low.There are also insufficient transparency and transaction efficiency; DEFI has efficient trading mechanisms and global liquidity, but mainly depends on crypto assets and lacks direct connection with the real economy.

Unlike the industry’s point of view: “Payfi is a subdivision of the RWA track”, CGV Research believes that RWA is part of the Payfi ecosystem.In addition to RWA, PayFi also involves wider crypto assets, smart contract -driven financial services, and decentralized payment and settlement systems.With the help of Defi to promote the introduction and application of RWA, Payfi is an important part of its core function.

RWA needs DEFI to improve liquidity and transaction efficiency. It achieves rapid and low -cost global financing through the digitalization and smart contracts of the blockchain, and enhances transaction transparency and security.At the same time, DEFI has introduced RWA’s rich asset category to reduce volatility risks, provides stable sources of benefits, connects the real economy, and promotes its actual application and development globally.

>

Through PayFi, RWA and DEFI are no longer the financial system developed independently, but the organic whole of interdependence and complementarity, realizing the integration and innovation of real assets and financial services on the chain.

——D digitalization and chain:Import RWA into the blockchain.The PayFi platform first digitizes RWA through smart contracts so that it can be expressed and traded on the blockchain.This process ensures the value and security of RWA’s value and ownership on the chain.In this way, the traditional RWA assets can be divided into small units to facilitate trading and investment globally.

——Smark contract and payment system:Realize efficient transactions and settlement.Once the RWA is digitized, the PayFi platform uses smart contracts to come from dynamic transactions and settlement processes.This not only speeds up the transaction speed, reduces costs, but also ensures the transparency and security of transactions.In addition, the PayFi chain payment system makes the transfer and payment of these assets simpler and more efficient, solving the problem of settlement delay and high handling fees common in traditional finance.

——Lloid pool and financing channels:Provide fund support for RWA.Payfi’s liquidity pool provides sufficient financial support for RWA, so that these assets can receive financing of global investors.By using RWA as a mortgage, Payfi allows investors to participate in financing activities on the DEFI platform, and at the same time provides stable sources of funds for RWA.This model not only increases the liquidity of RWA, but also brings diverse investment opportunities to Defi investors.

——Re risk management and transparency:Enhance market trust.Through blockchain technology, Payfi ensures the transparency and verification of all RWA transactions, reducing information asymmetry and operating risk.The automatic execution of smart contracts reduces the risk of artificial intervention. At the same time, the non -tampering of the blockchain ensures the security of transaction records.All this has enhanced the trust of the market and promoted the further integration of RWA and DEFI.

In the future, PayFi will play an increasingly important role in promoting global asset liquidity, reducing transaction costs, and enhancing market transparency.In Lily Liu’s view,Payfi introduces RWA and institutional finance into the liquidity pool on the chain to create a integrated value chain to form a “new financial cluster”, which may be the largest theme in the cycle of the encryption market.

Why does Payfi happen on solana?

Why does PayFi happen on Solana instead of other L1 public chains or L2 solutions?The answer given by Lily Liu is: “Solana has the three major advantages of high -performance public chain, capital liquidity and talent liquidity.” These advantages constitute the threshold for other competitors at this stage.

First, high -performance public chain.The core technical advantage of Solana is its unique Proof of History (POH) consensus mechanism, so that it can handle more than 65,000 transactions per second (TPS), and the transaction confirmation time is usually about 400 milliseconds.This performance far exceeds the 10-15 TPS and long confirmation time of Ethereum. Even the L2 solution on Ethereum, such as Optimistic Rollups, is difficult to match solana in terms of delay and throughput.Although VISA claims that its server can handle up to 56,000 TPS, in actual use, VISA has only handled 1,700 transactions per second.In contrast, Solana can fully meet the actual payment needs.

Second, capital liquidity.As of August 30, 2024, the total lock value (TVL) of the Solana ecosystem has exceeded $ 10 billion, and has attracted major investment in top venture capital funds such as Andreessen Horowitz (A16Z), Polychain Capital, Alameda Research.This capital liquidity provides strong financial support for the expansion of PayFi.

Finally, talent liquidity.The Solana Foundation actively promotes the construction of the developer community and organizes more than 500 hackers pine and developer education projects worldwide.As of 2024, more than 5,000 active developers in the Solana ecosystem have become one of the fastest growing blockchain developer communities in the world.The powerful talent pool supports the development of various innovative projects, and continues to attract new technologies and financial talents to join the ecology, laying a solid foundation for the development of Payfi.

Payfi uses programmable payment to open up the traditional world and blockchain world. Through smart contracts, the large -scale expansion of credit finance will be expanded into possible.Solana’s advantage not only supports the development of Payfi, but also allows it to have strong competitiveness in future global payment and financial markets.

Taking Pyusd as an example, PayPal chose Solana as a new public chain paid by Pyusd. It mainly values the fast settlement capacity, low transaction costs, and strong developer ecosystems provided by Solana.Solana’s token extension, including confidential transfers, transfers, and memo fields, provides necessary flexibility and commercial practicality for PYUSD.

As PayPal said: “These functions are not optional. If you want PYUSD to play a role in a wider range of business, it must be provided to the merchant.” Today, Solana has become the main platform of PYUSD, accounting for 64% of the market.The share, and Ethereum only accounts for 36%.In addition, as early as September 2023, VISA has expanded USDC’s settlement function from Ethereum to Solana.

Payfi application scenarios and typical projects

The essence of Payfi is to use advanced encryption technology to reshape and upgrade the traditional financial system. Therefore, all financial scenarios can be replaced with PayFi

1. Cross -border payment and trade

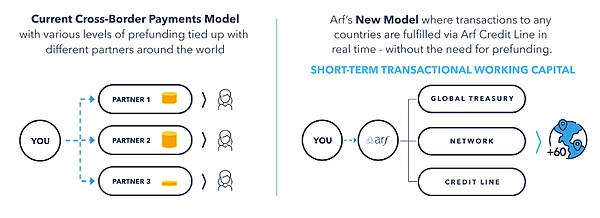

The traditional cross -border payment problem is mainly due to the isolation problem in the centralized sovereign monetary system. Due to the impact of national monetary policy such as foreign exchange control and capital circulation, cross -border payment has always been cumbersome, time -consuming, and cost -effective.At first, everyone believed that cryptocurrency payment to replace traditional cross -border payment was an excellent solution, but there were still many shortcomings for enterprises.

Today, the cross -border payment industry is still seriously relying on prepaid funds to achieve the settlement of the day.At present, the funds that have been claimed in the prepaid funds account are more than $ 4 trillion, which is a huge and hidden cost for financial institutions and global payment industries.Payfi can optimize this and use traditional credit finance to leverage the encryption service.

>

The current cross -border payment model is compared with the ARF improvement model

(From: ARF)

ARF (@Arf_one):The world’s first short -term liquidity solution to support cross -border payment, regulatory, and transparently.Headquartered in Switzerland.By providing digital asset -based operating funds and settlement services for digital assets, as well as local imports and export capabilities, it is used to eliminate the capital -intensive business model institutions of the cross -border payment industry.ARF provides a unified liquid network for cross -border payment and trade, eliminates the demand of Prefunding, and provides 24X7 transparent compliance services.As of now, the trading volume on the ARF chain has recently exceeded 1.6 billion US dollars, and no default has occurred, which has become one of the fastest -growing stable currency cases.

2. Supply chain finance

Supply chain finance combines financial services with supply chain management. Based on the trade relationship and transactions in the supply chain, through the control and management of supply chain information flow, logistics, and capital flow, it provides a systematicFinancial products and services.Traditional supply chain finance is subject to tedious contracts and legal work, and it is difficult to automate the evaluation. The financing process is slow, which seriously affects the financing turnover of small and medium -sized enterprises.Payfi greatly simplifies the process of receivables and other businesses, alleviating the problems of corporate financing difficulties.

>

Global companies are rejected due to the limitations of traditional financial institutions due to the limitations of traditional financial institutions.

(From: isle Finance)

Isle Finance (@isle_finance):The first project to provide the RWA PayFi network for the supply chain payment will introduce the current web3 liquidity into supply chain finance and provide a competitive income with A -level quality to liquidity providers.Through ISLE, the supply chain payment is combined with real -time settlement and liquidity management of blockchain technology, so that the supply chain participants can handle payment and settlement faster and improve the efficiency of capital utilization;You can anchor the stability of high credit buyers and share the advance payment discounts provided by the buyer with the buyer.The main customers of ISLE include: High Pure Personal Personal (HNWIS), encrypted native users, DAO inventory, asset manager and family office, etc., and allow ordinary users to mortgage the ISLE tokens to obtain liquidity mining rewards.

3. Consumer finance

Payfi facing C -end users may be more interested in users, mainly in the field of consumer finance. This is also part of Lily Liu’s emphasis on Payfi sharing, “Buy Now, Pay Never”.Users can cover the current expenditure by promising future returns, and the mandatory execution part will be implemented by the smart contract on the chain.In consumer finance, the key to Payfi is to open up a service provider to open up merchant networks in the middle, so that consumers can obtain sufficient consumer scenarios.

>

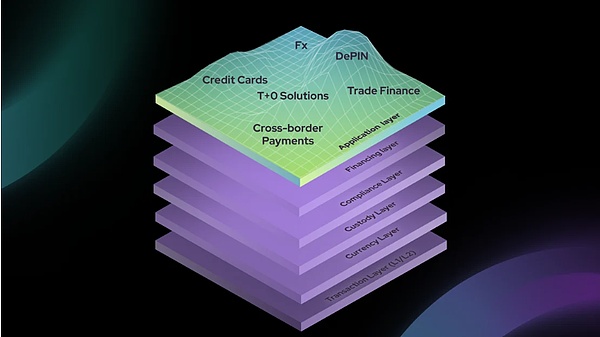

Payfi Stack’s open stack of compliance payment financing solutions

(From: Huma Finance)

Huma Finance (@Humafinance):In the industry, the Payfi Stack was first proposed, a open stack aimed at building a compliance payment financing solution, and advocating industry leaders to optimize solutions to meet the unique needs of Payfi.Initial stacks include the following levels: transactions, currency, custody, financing, compliance and application.Taking the financing layer as an example, including: from credit rating, underwriting to RWA prophecy machines, etc.As a representative project of the financing layer, HUMA focuses on short -term financing commonly used in the payment field. As of August 26, 2024, the total amount of financing of HUMA (single -caliber) exceeded 280m, and the default rate was 0.

Credipay (@credix_finance):Through seamless and risk -free credit services, it helps companies increase sales and improve cash flow efficiency.The seller provides buyers with flexible payment conditions and collects prepaid.We manage and protect customers from any credit and fraud risks, so that they only pay attention to the most important things: increasing sales and profitability.The current Credix’s services are mainly concentrated in Latin America, such as account receivables.

Payfi opportunities and challenges

1. Market growth space

The core goal of Payfi is to introduce the time value of the currency into the chain, and reconstruct the financial system in a more programmable, sub -custody, and decentralized manner.With the rapid increase in the number of global stable currency and the continuous improvement of cryptocurrency infrastructure, Payfi is expected to become an important force to transform traditional finance.

According to Statista data, the total global digital payment transaction in 2023 is expected to reach about 9.46 trillion US dollars, and this number is expected to continue to grow, and it may reach $ 14 trillion by 2027.At the same time, data from Mordorintelligence shows that the DEFI market size is estimated to be US $ 46.61 billion in 2024, and it is expected to reach US $ 78.47 billion by 2029, with a forecast of a compound annual growth rate of 10.98%.

The calculation of the CGV Research team shows that assuming PayFi can account for 10%of the total global digital payment transaction (conservative estimation),By 2030, the PayFi market size (expected to be US $ 180 billion) will be 20 times that of the DEFI market size ($ 87 billion).This means that PayFi has huge market potential and is expected to occupy an important position in the global digital payment field.

2. Supervision and compliance challenges

With the continuous increase in the amount of stable currency issuance, central banks of various countries have gradually eased the attitude towards stablecoins.In a broad sense, the stable currency that anchored in the fiat currency can be regarded as the number of fiat currency.Payfi mainly involves the payment business of stable currency as the medium, which is actually subject to the supervision of the sovereign monetary system.

On the one hand, the current PayFi project focuses on compliance, usually only allows licensed institutions to participate, and individual users need to go through strict KYC processes and review.On the other hand, a large number of PayFi projects tend to expand the business of the third world countries. Because local regulations are usually insufficient and regulatory obstacles are low, the risk of compliance is relatively small.

3. Technology and security risks

After years of Defi development, although the security issues have not been completely eliminated, a large amount of security vulnerabilities have been found, and after rigorous auditing, the security of Payfi on the chain has basically equivalent to the security of traditional DEFI.

However, technical challenges mainly exist under the chain.Because PayFi needs to access a large number of real -world assets to ensure that the enforcement of the logic under the chain is still a problem to be solved.The current solution is usually to handle the alignment and the chain under a intermediary entity, but this solution still needs to be further improved.

Conclusion

Payfi, as a new wave of payment of finance, is reshaping the global financial ecology with its unique charm.It not only inherits the vision of Bitcoin’s payment, but also improves the efficiency and inclusiveness of financial services to a new height through the innovation of blockchain technology.With the blessing of high -performance public chains such as Solana, the market size of Payfi is expected to achieve index growth, becoming the main driving force for the future financial market.

As Lily Li foresees it, Payfi closely combines RWA and DEFI to build a integrated value chain, forming a new financial cluster.This revolutionary innovation will promote the development of the global financial system in a more efficient and tolerant direction.