Author: qw & amp; chloexyg, alliancedao; Translation: Bitchain Vision Xiaozou

In AllianceDao, we receive about 3,000 encrypted entrepreneurial accelerators every year.We will collect a lot of data to understand what the underlying chain of these projects is, what types of their products, where their base camps are, and so on.Because the sample scale is huge and relatively speaking, we are not affected by these factors, so we can form a unique opinion on the development direction of the industry.

1Public chain

(1.L1

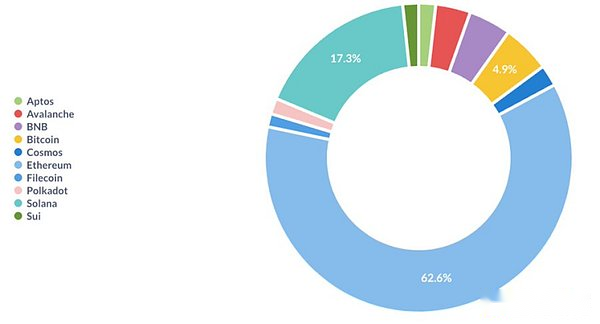

Ethereum is still a dominant ecosystem.Solana was reappearing after the bottom of 2022 bottomed out.FTX also collapsed in the second half of 2022, which may not be a coincidence.Along with the strong interest of REDinals, Runes and Bitcoin L2, Bitcoin is undergoing revival.

>

>

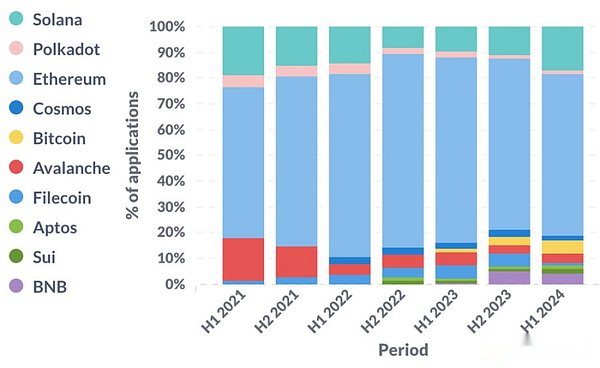

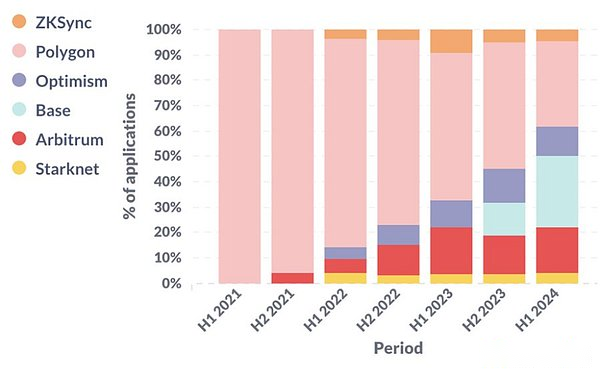

(2) EthereumL2

Look at Ethereum L2 (and side chain).Over the past three years, Optimistic Rollup’s attention has remained high.It is worth noting that in the first half of 2024, more than a quarter of the startups based on Ethereum L2 chose Base.

>

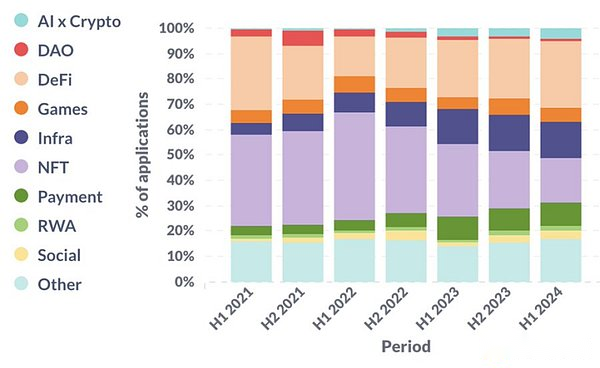

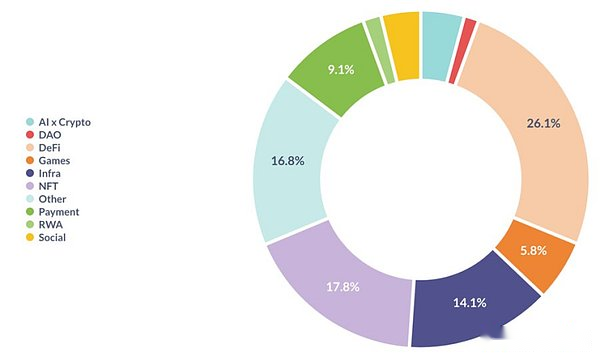

2. Product

More and more startups are building infrastructure, DEFI, payment, and AI X Crypto.Among them, infrastructure and AI are aligned with public discourse.But the rise of Defi and payment fields may surprise most people because the public is almost not very interested in them.Coincidentally, in our opinion, they are still the real PMF (product market compliance) discovered by the encrypted world only two vertical fields.

>

>

Please note that this is not a perfect classification of the product, and it is clear that these categories overlap a certain degree.For example, a startup may operate two categories: games and NFT at the same time. In this case, we will allocate the weight of 0.5 for each game and NFT.

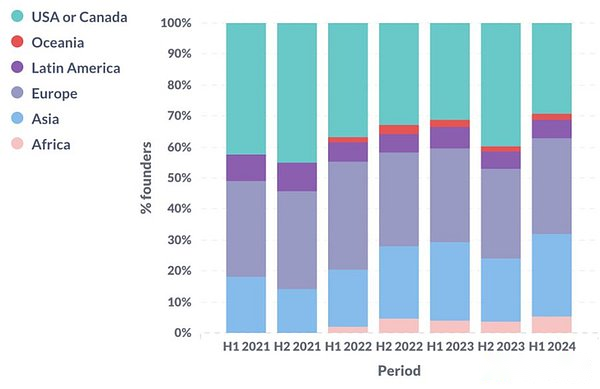

3, Geographical distribution

In the first half of 2024, we saw that the proportion of startups in the United States and Canada was the lowest in history, and the proportion of startups in Asia and Africa was the highest in history.This may be due to the uncertainty of the United States and more and more practical applications in emerging markets.

In general, North America, Europe, and Asia are still the first three major crypto startups, and the number of startups in various regions accounted for 1/4 to 1/3 of the total.

>

>

4Founder background

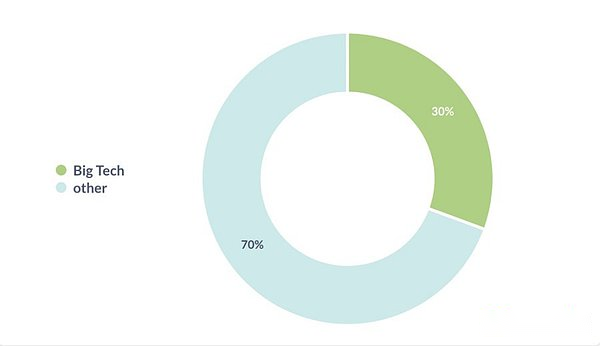

(1) Large -scale technology company

The proportion of founders from the “large technology company” background reached its peak in 2021, currently 30%.The large technology company mentioned here refers to the technology company in the S & P 500 index.Specific definitions are not important. The important thing is the trend of development over time.

>

>

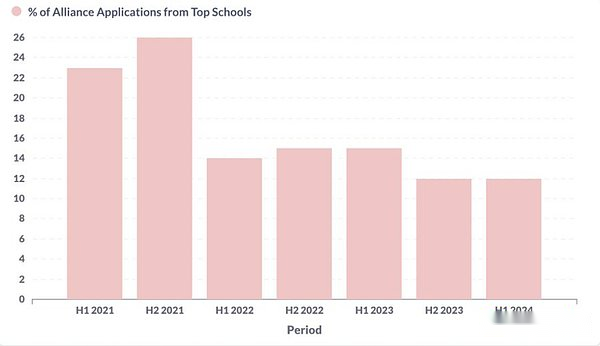

(2) Top famous school

Similarly, the proportion of founders who graduated from the “top famous school” reached its peak in 2021.We define the top universities as the top 100 universities in QS.

>

>

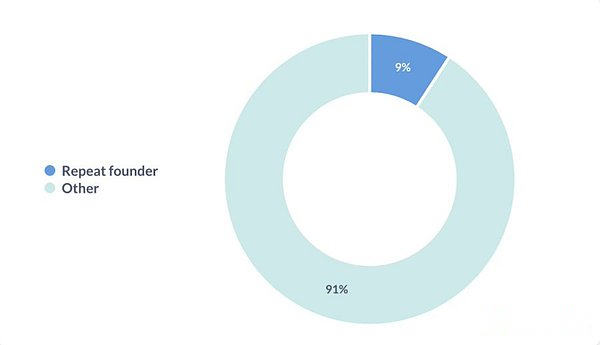

(3) Multiple entrepreneurs

About one -tenth of the entrepreneurs have previously founded a startup company.

>

5, Team composition

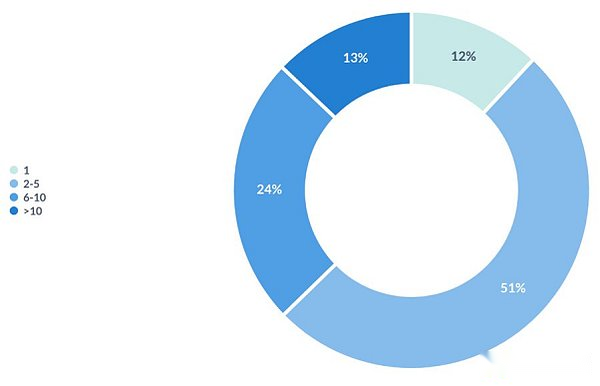

(1) Team scale

More than half of the startup companies are only 2 to 5 people.We also happen to believe that this is the best scale of startups at the PRE-PMF (before PMF).

>

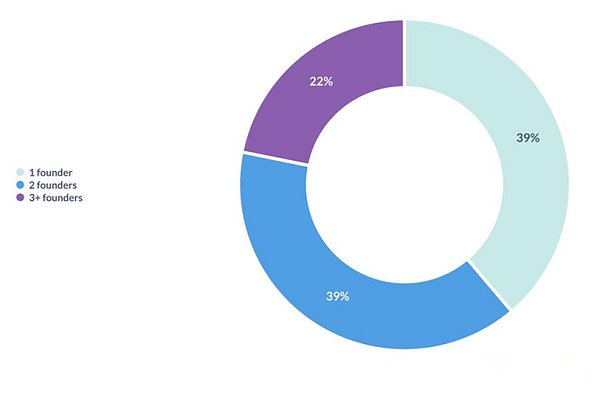

(2) Co -founder

Less than 40%of startups were founded by a single founder.Each study shows that 20-30%of unicorn companies are founded by a single founder.

>

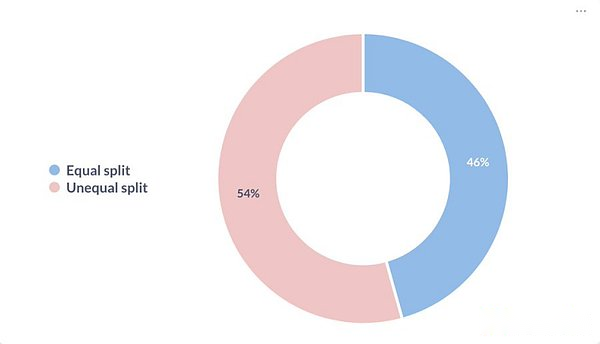

(3) Equity division

Of the startups with two or more co -founders, about half of the companies choose to distribute the equity average.

>

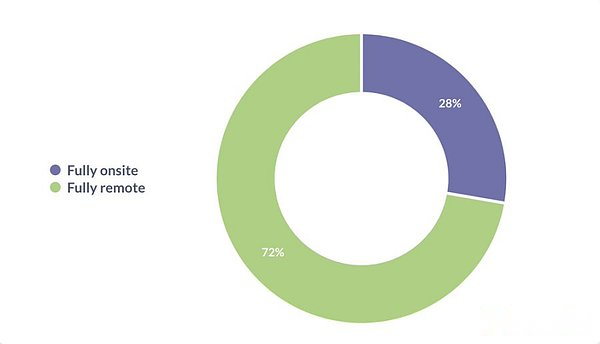

(4) Remote work

Nearly 3/4 startups adopt a completely remote work model.

>