Author: Ekko an, Ryan Yoon, Source: Tiger Research, Compiler: Shaw Bitcoin Vision

Key takeaways

-

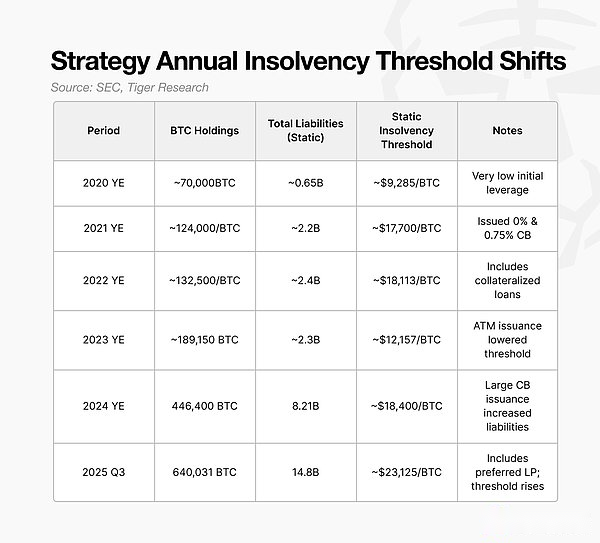

Strategy’s static bankruptcy threshold is expected to be around $23,000 in 2025, nearly double the $12,000 level in 2023.

-

The company will change its financing model from simple cash and small convertible bonds to a diversified portfolio of convertible bonds, preferred shares and ATM issuance in 2024.

-

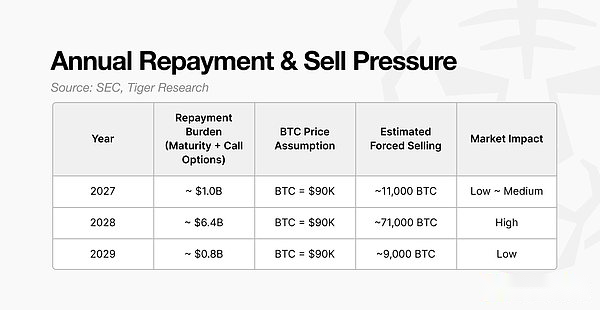

Call options held by investors allow them to redeem them early before expiration.If Bitcoin prices fall, investors are likely to exercise this option, making 2028 a critical risk window.

-

If the refinancing fails in 2028, Strategy may need to sell approximately 71,000 Bitcoins, assuming a Bitcoin price of $90,000.This is equivalent to 20% to 30% of the average daily trading volume and will cause significant pressure on the market.

1. Questions about Strategy stability

Bitcoin’s recent decline has caused DAT’s stock price to fall by approximately 50%.This raises a core question in the market: With both the stock price and the company’s core assets falling, does Strategy’s stability still exist?The concerns were heightened after JPMorgan noted that Strategy could be removed from the MSCI index.

It’s not just the stock that people are paying attention to.Strategy holds a huge amount of Bitcoin, which is enough to influence the broader market, far exceeding the scale of ordinary whales..This raises two key questions.

-

At what level does the Bitcoin price reach before Strategy’s balance sheet collapses?

-

When and under what conditions can the company have an impact on the market?

This report examines U.S. Securities and Exchange Commission (SEC) filings to determine Strategy’s effective bankruptcy threshold, periods of increased risk, and the potential impact that could have on the market if a stress scenario were to occur.

2. Strategy at Risk: $23,000 Threshold

Before launching our analysis, we first clarify the concept of static bankruptcy.Static bankruptcy is a situation in which a company is unable to repay its debts even if all of its assets are liquidated.

Simply put, static bankruptcy is a situation where assets are less than liabilities.For example, if Echo Company owns a property worth 1 billion won and 100 million won in cash, but has 1.2 billion won in debt, then from the balance sheet point of view, the company is already insolvent.DAT companies are facing the same situation.If the price of Bitcoin falls below a certain level, book equity becomes negative and the company becomes unable to repay its debt.This level is known as the static bankruptcy threshold.

To determine Strategy’s static bankruptcy threshold, we first examine how the company accumulated its Bitcoin holdings.

Strategy has held Bitcoin as a strategic asset since 2020, but its accumulation pattern has changed after 2023.Until then, the company had relied primarily on cash reserves and small convertible bonds to buy Bitcoin.Its holdings remain below 100,000 Bitcoins, and its refinancing needs are also relatively limited.

Starting from 2024, Strategy’s financing method will change.The company raised leverage to finance the purchase of more Bitcoin through a combination of preferred stock issuances, ATM stock plans and large-scale convertible debt.

This resulted in the accumulation of Bitcoins rapidly accelerating.This structure creates a cycle: the higher the price of Bitcoin, the greater the company’s market capitalization and greater leverage, supporting more buying.

The goals remain the same, but the funding structure and risk profile have changed.This structural shift is now at the heart of exacerbating Strategy’s risk of bankruptcy.

Strategy expects a static bankruptcy threshold level of approximately $23,000 in 2025.Below that level, the value of its Bitcoin holdings would be less than its liabilities, rendering the company insolvent on its balance sheet.

The key is that this threshold keeps rising.In 2023, the company can sustain a Bitcoin price of around $12,000.This threshold rises to $18,000 in 2024 and $23,000 in 2025.This critical level also increased as Strategy increased its holdings on Bitcoin.

Therefore, the $23,000 threshold represents the minimum price required for Bitcoin to operate stably.This means that Bitcoin would need to fall approximately 73% from current levels to trigger bankruptcy risk.

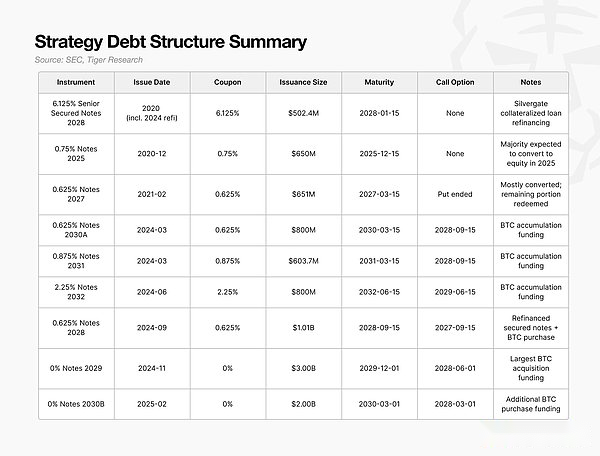

3. Convertible bonds: The issue is the holder’s put right, not the maturity date

As mentioned earlier, Strategy’s static bankruptcy threshold was raised to $23,000 as liabilities grew faster than Bitcoin holdings.The next question is how these debts are structured.

Between 2024 and 2025, Strategy adopts a new financing model that combines convertible bonds, preferred stock and an ATM stock plan.Among these instruments, convertible bonds account for the largest proportion and have the most significant impact on the market.

The key is not the size or maturity of the convertible bond, but the timing of the holder’s exercise of the put option.

This clause allows investors to request early repayment, which the company cannot refuse.Most of the large convertible bonds issued in 2024-2025 have holder redemption dates around 2028, so 2028 is a key year for Strategy to prove its ability to refinance.

If Bitcoin prices approach the bankruptcy threshold in 2028 or market conditions worsen, investors are likely to exercise put options rather than wait for expiration.A wave of put option exercises would require Strategy to raise billions of dollars in cash immediately.

The problem is that almost all of the money raised through these convertible bonds is used to buy Bitcoin.If these funds are invested in productive assets that generate cash flow, the company will naturally have a source of repayment funds.However, the focus on accumulating Bitcoin has left little cash available for redemption.

Therefore, debt repayments will need to be achieved through the sale of assets.If Bitcoin prices are low when the options window opens, Strategy could face an immediate liquidity shortage.Forced selling would further depress prices, raise bankruptcy thresholds and potentially trigger a vicious cycle.

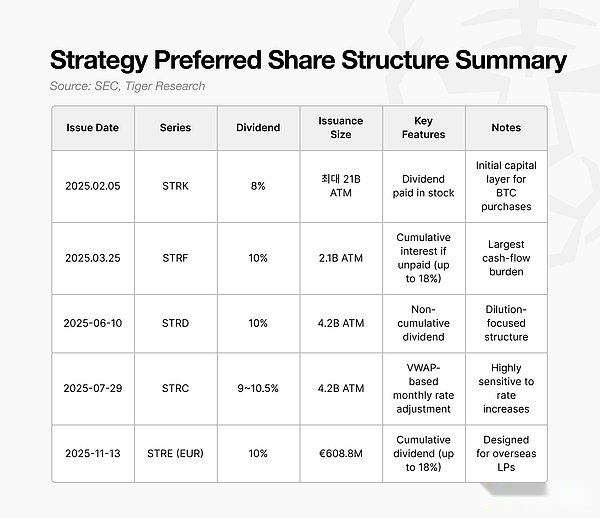

4. Preferred shares: Why choose a 10% dividend load?

Starting in 2025, Strategy will shift from issuing nearly zero-coupon convertible bonds to issuing preferred shares with a dividend yield of about 10%.At first glance, this may seem like a more costly option.

However, the decision reflects growing refinancing pressures in 2027-2028.A large number of bondholders choosing to sell back bonds in 2028 will significantly increase medium-term repayment risks.Any continued cash outflows during this period will increase the risk of bankruptcy.

The key feature of preferred shares is that dividends do not need to be paid in cash.Strategy issuance is designed so that dividends can be paid in shares when needed.This allows the company to raise capital without an immediate cash drain and meet its dividend payment obligations without using cash.In effect, the preferred shares help Strategy avoid selling Bitcoin during the critical 2027-2028 period.

While a 10% dividend yield seems high, paying dividends in the form of shares makes it a tool to preserve liquidity and prevent short-term cash shortages.

However, this structure also brings new challenges.Paying dividends in the form of stock continues to dilute common shareholders.Strategy itself is facing possible equity dilution caused by future convertible bond conversions, and preferred shares have added another aspect of equity pressure.

Preferred shares also enjoy priority repayment rights.If the company faces pressure on debt repayment and operating costs at the same time, preferred stockholders must be paid in priority over common stockholders.Although preferred stock does not have a fixed maturity date, its dividend obligations constitute a structural fixed cost and affect the company’s actual bankruptcy threshold.

By 2024-2025, Strategy has moved from a model based on low-cost convertible bonds to a hybrid structure that combines convertible bonds, preferred shares and ATM issuances.This shift allowed Bitcoin holdings to expand rapidly in the short term.

5. What happens if Strategy fails?

If Strategy is unable to refinance in 2028, its impact on the market can be estimated by its repayment obligations.

A large number of convertible bonds issued in 2024-2025 will generate potential repayments of approximately $6.4 billion in 2028.If market conditions deteriorate and the preferred stock issuance, ATM issuance and new convertible debt cannot proceed, the company will have no choice but to sell Bitcoin.

Assuming a Bitcoin price of $90,000, Strategy would need to sell approximately 71,000 Bitcoins to meet these obligations.This is not comparable to the size of a typical institutional sale.

The current average daily trading volume in the spot market is US$20 billion to US$30 billion.The sale of 71,000 Bitcoins for $90,000 is equivalent to about $6.4 billion and accounts for about 20% to 30% of daily trading volume.Such a massive sell-off in a short period of time would almost certainly put price pressure on the market.

What’s even more worrying is that this type of sell-off is not a one-time event.As Bitcoin prices fall, Strategy’s assets immediately shrink in value, weakening its financial ratios.This will further limit its ability to raise funds and may force it to sell more Bitcoin.

The result is a vicious cycle: failed refinancings lead to forced sales, forced sales lead to falling prices, falling prices reduce asset values, and the company is forced to sell further assets.A few quarters of this dynamic could worsen balance sheets beyond recovery.

Therefore, Strategy’s structural risk is concentrated in 2028.Outside of this window, the leverage model appears manageable, but a failure to refinance in 2028 could trigger selling pressure large enough to affect the entire Bitcoin market.

Therefore, 2028 will be critical not only for Strategy’s survival, but also for potential volatility in the entire Bitcoin ecosystem.

6. Strategy is relatively stable, but late entrants face higher risks

The market narrative often reduces DAT risk to a simple question: can a company survive every decline in Bitcoin.However, this analysis shows that the key to a company’s survival is not short-term price swings or stock volatility, but the design of a company’s balance sheet and its capital structure.

Therefore, evaluating DAT companies requires more than just looking at the decline in its stock price or the price of Bitcoin.Key indicators include the position of its static insolvency threshold, the timing of cash repayment pressures and the tools it has in place to bridge funding gaps.These factors help us understand its structural resilience rather than short-term fluctuations.

Not all risks can be predicted.ETF capital flows, macroeconomic conditions and regulatory policy changes may reshape the market environment at any time.Even so, the most reliable benchmarks are the bankruptcy thresholds implied by the financial data and the company’s underlying cash flow mechanics.

Strategy is unique in this regard.The company entered the Bitcoin market in 2020, withstood the downturn in 2022, and accelerated accumulation through leveraged financing in 2024.Its mix of convertible debt and preferred stock creates a multi-layered buffer.

Therefore, Strategy has a relatively stable foundation.New entrants have not yet established a mature DAT framework, and their ability to withstand sharp price drops is far less stable.