Author: Francesco, Castle Capital; Translation: 0xxz@作 作 作 作 作 作

The mortgage seems to be considered one of the main narratives of 2024 by many people.

However, although many people talk about the way and their benefits of re -mortgage, the situation is not all optimistic.

This article aims to take a step back, pledge from a higher level of analysis, emphasize risks and answer such questions: Is it really worth it?

Let us first introduce this theme first:

What is again pledged?

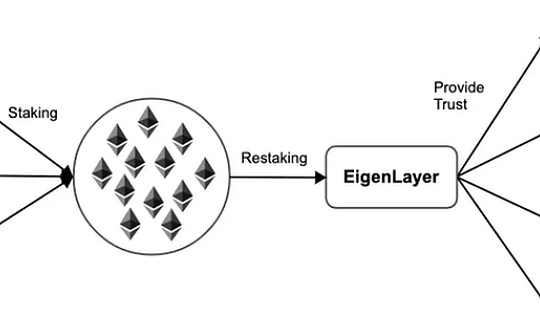

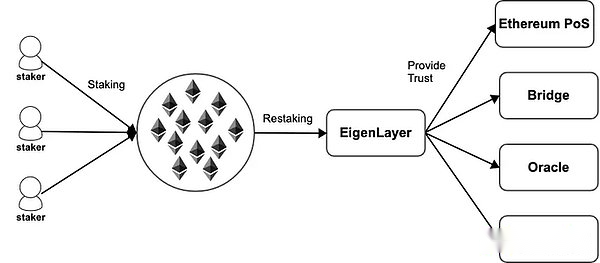

Ethereum’s equity certificate (POS) is a decentralized trust mechanism, and participants can promise its pledge to protect the security of the Ethereum network.

The idea of re -mortgage is that the same pledge used to protect the Ethereum POS can now be used to protect many other networks.

EIGENLAYER is decentralizing the decentralization of Ethereum in Ethereum so that AVS (Actively Validated Services) can use it without launching its authentication set, which effectively reduces the threshold for entering the market.

EIGENLAYER is decentralizing the decentralization of Ethereum in Ethereum so that AVS (Actively Validated Services) can use it without launching its authentication set, which effectively reduces the threshold for entering the market.

Generally, such modules need to actively verify services, which have their own distributed verification semantics to verify.Generally, these active verification services (“AVs”) are either protected by their own native token or permitted in essence.

Why are people pledged again?

Simply put, it is because of economic incentives and returns.If Ethereum pledge yield hovers around 5% each year, pledge may bring attractive additional benefits.

However, this will bring additional risks to the pledges.

In addition to using the inherent risks of ETH pledged, when users choose to re -pledge your tokens, they are essentially entrusted to punish their pledged power under the circumstances that Eigenlayer contracts have errors and dual signatures on any AVS they protect.

Therefore, the mortgage increases a layer of risks, because the re -mortgagers may be punished on ETH, re -mortgage, or two.

Is the additional income worth pledge?

R (ISK) -Pet pledged-another pledge added some significant risks

• ETH must be pledged (or LST -therefore not liquidity)

• Eigenlayer smart contract risk

• Specific punishment conditions of the agreement

• Liquidity risk

• Concentration risk

In the words of ChainLinkgod, “a liquidity re -mortgage token supports liquidity mortgage to tokens stored in the recycling protocol.Add another layer of liquidity and risk here? I think we are not enough. “

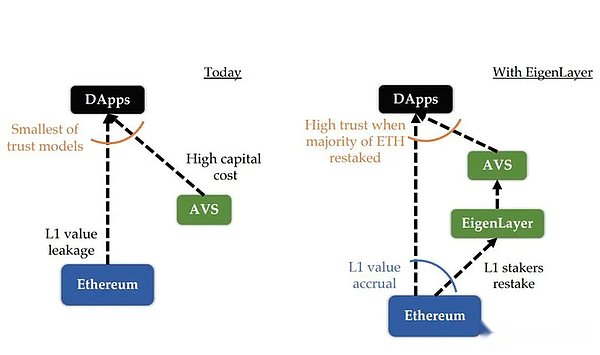

In fact, by re -mortgage, users are using tokens that have been exposed to risks (due to mortgage), and add additional risks above it, which eventually leads to stratified risks, as shown below:

In addition, any additional primary development will increase more complexity and additional risks.

In addition, any additional primary development will increase more complexity and additional risks.

In addition to the personal risk of the re -pledges, the Ethereum developer community also puts forward the issue of re -pledge, especially in the famous Vitalik’s article on “Do not overload the Ethereum Consensus”.

The problem with pledge is that it has opened up new risk ways to protect Ethereum pledged in the main network. It is destined that some of them will protect other chains (chose to join by pledges).

Therefore, if they have improper behavior according to other protocol rules (there may be errors or weak security), their deposits will be punished.

The debate is very practical. Developers and Eigenlayer try to find a method of coordination and ensure that Ethereum will not be punished by these technological progress.

The most important “layer” of protecting Ethereum security is really not easy.In addition, a key aspect of this is to allow the level of risk management of re -pledges.

Many re -pledge projects handed the AVS’s white list process to their DAO.

However, as a re -pledker, I hope to review and decide which AVS to be pledged to avoid the possibility of being attacked by malicious networks and reducing the possibility of a new attack medium!

All in all, the mortgage is an interesting new original.

Nevertheless, the concerns of Vitalik and others cannot be ignored.When talking about re -mortgage, it is important to remember how this will affect the security model of Ethereum main network: in fact, it is fairof.

Finally, it is a personal choice if it is worth pledge.

Institution re -pledge

Perhaps it is surprising that many institutions have expressed their interest in re -mortgage and get additional rewards other than pledge.

Considering the risks emphasized before, whether the maximum interest rate of re -mortgaging depends on the retail or institution, it will be very interesting.

Except for the additional income except the native ETH pledge is very attractive to those who have participated, but considering risks, this is not a change of life for Dege.

This has opened up new use cases for Ethereum as a financial instrument.

A particularly interesting comparison can be compared with the “corporate bonds” with “corporate bonds”.

The new network hopes to obtain L1 security, similar to how companies or national countries use their financial systems to create bonds and protect their assets.

In the field of cryptocurrencies, Ethereum is the widest and most liquid network, and it may be the only network that can maintain such a market -from a similar perspective of countries in the Tradfi economy, it is also the safest network.

Nevertheless, most of the interests of the current mortgaging seem to be driven by Eigenlayer airdrops, Eigenlayer airdrops may be the largest airdrop in the history of cryptocurrencies.

How will the dynamic dynamics change after airdrop?

Perhaps the actual R/R analysis may push some people to other ways that may be more effective.

I even think that a large part of the capital deposit -re -mortgaged capital is hired capital, and these capitals may leave after airdrops.

The separation speculative section is essential for evaluating users’ true interest in this new primitive.

Personally, forgive me, the mortgage statement is a bit exaggerated, and you must carefully evaluate the current risk.

What can we do to reduce these risks?

Some solutions that reduce the risk of re -mortgage include optimizing and re -mortgage parameters (tvL upper limit, punishment amount, cost distribution, minimum TVL, etc.) and ensure the diversification of funds between AVS.

One of the direct steps that can be considered by the mortgage agreement is to allow users to choose different risk conditions when the deposit is repaired.

Ideally, each user should be able to evaluate and choose AVS to be re -mortgaged without entrusting the process to DAO.

This is a product that requires AVS and Eigenlayer to work together to ensure that there is a roadmap that can minimize these risks.

The EIGENLAYER team has cooperated with the Ethereum Foundation to further coordinate and ensure that the re -mortgage will not give Ethereum, Liquid Stake tokens or use its AVS to increase system risks.