Author: arndxt; Source: X, @arndxt_xo; Compiler: Shaw Bitcoin Vision

I’m going to take a deep dive today and analyze the true state of our economy right now.If you have been paying attention to the previous macroeconomics, you should be able to get some hints from it.

At present, only artificial intelligence is still driving GDP forward, and other aspects such as the labor market, households, affordability, and asset acquisition are all declining.

Everyone is waiting for the “cycle reversal”.But there are no cycles at all.

The fact is:

-

The market now no longer trades based on fundamentals.

-

AI capex is actually a key factor in preventing technological decline.

-

There will be a wave of liquidity in 2026, and market consensus hasn’t even begun to price it in yet.

-

Inequality is a macro-resistance that restricts policymaking.

-

The bottleneck of artificial intelligence is not GPU computing power, but energy.

-

Cryptocurrency is becoming the only asset class with real upside potential for younger demographics, making it politically relevant.

Don’t misjudge the risks of this transformation and misallocate investments, thereby missing out on opportunities.

1. Market dynamics are not driven by fundamentals

Asset market prices have fluctuated over the past month without the release of new economic data, but have seen sharp swings in response to the Fed’s shift in attitude.

The probability of a rate cut dropped from 80% to 30%, and then back to 80%, just because of the remarks of individual Fed officials.This is consistent with market conditions in which systemic capital flows overwhelmingly exceed macro judgments.

Here is some microstructural evidence:

-

Volatility target funds mechanically deleverage when volatility spikes and re-leverage when volatility compresses.

These funds don’t care about “the economy” because they adjust their risk exposure based on only one variable: the level of market volatility.When volatility increases, they reduce their exposure → sell.When volatility falls, they increase exposure → buy.This will cause automatic selling when the market is weak and automatic buying when the market is strong, thereby amplifying two-way fluctuations.

-

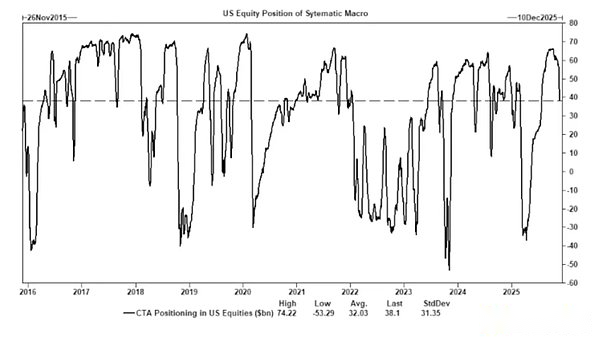

CTA switches long and short positions at preset trend levels, thereby generating forced capital flows.

CTAs (Commodity Trading Advisors) follow strict trend rules:

• If price breaks above a certain level → Buy.

• If price falls below a certain level → sell.

There is no “logic” behind this.It’s just mechanical.So when enough CTAs place stop-loss orders at the same price at the same time, a massive, coordinated buying or selling action occurs, despite no change in fundamentals.These flows can affect the entire index within days.

-

Share buyback window remains largest source of net equity demand.

Companies buying back their own stock are the largest net buyers in the stock market, larger than purchases by retail investors, hedge funds and pension funds.Companies are steadily pumping billions of dollars into the market every week during the share buyback window.

This would create: 1. a built-in uptrend during buyback season; 2. significant weakness as the window closes; and 3. a structural buying order that is not tied to macro data.This is why stocks can rise even when market sentiment is extremely negative.

-

The inversion of the VIX curve reflects short-term hedging imbalances, not “panic”.

Typically, long-term volatility (3-month VIX) is higher than short-term volatility (1-month VIX).When this reverses, with front-month options rising in price, one thinks of a “fear surge.”But today, VIX curve inversions are often caused by short-term hedging demand; options traders adjusting exposure; inflows into weekly options; and systematic strategies to hedge at the end of the month.This means: VIX surge ≠ panic.VIX surge = hedged capital flows.

This distinction is crucial as it shows that volatility is now driven by trading rather than market sentiment.

This has resulted in the current market environment being more sensitive to market sentiment and capital flows.Economic data has become a lagging indicator of asset prices, while Fed communications have become a major trigger of market volatility.

Liquidity, positioning and policy tone now drive price discovery more than fundamentals.

2. AI is preventing a full-scale recession

Artificial intelligence has begun to function as a macro stabilizer.

It effectively replaces cyclical hiring, supports corporate profitability and sustains GDP growth amid weak labor fundamentals.

This means the U.S. economy is far more reliant on AI capital spending than policymakers publicly acknowledge.

-

Artificial intelligence is suppressing demand from the least skilled and most replaceable third of the labor market.And this is often where cyclical economic downturns first appear.

-

Productivity gains masked overall deterioration in the labor market.Output remains stable because machines absorb jobs previously performed by entry-level labor.

-

Corporate profits rise due to fewer employees, while households bear the resulting socioeconomic burden.

-

This results in a shift of income from labor to capital—a classic recession dynamic that is masked by gains in productivity.

-

AI-related capital formation artificially maintains GDP resilience.Without capital expenditures in artificial intelligence, the overall GDP data will be significantly weaker.

Regulators and policymakers are bound to support AI capital spending through industrial policy, credit expansion, or strategic incentives, or else there will be an economic downturn.

3. Inequality has become a macro constraint

The backlash against Mike Green’s analysis (poverty line ≈ $130,000 to $150,000) shows how far-reaching the issue is.

Core facts:

-

Child care expenses>rent/mortgage;

-

Housing is structurally unaffordable;

-

Baby boomers dominate asset ownership;

-

The younger generation only has income and no capital;

-

Asset inflation is exacerbating this gap every year.

Inequality will force adjustments in fiscal policy, regulatory stance and asset market interventions.

Cryptocurrency is becoming a demographic tool, allowing younger generations to participate in capital appreciation.Policymakers will make corresponding adjustments accordingly.

4. The bottleneck of artificial intelligence expansion currently lies in energy rather than computing power.

Energy will become the new narrative theme.

The AI economy cannot thrive without a corresponding expansion of energy infrastructure.

The discussion around GPUs ignores a much larger bottleneck:

-

electricity

-

Grid capacity

-

Nuclear and natural gas construction

-

cooling infrastructure

-

Copper and critical minerals

-

Data center location restrictions

Energy is becoming a limiting factor in the development of artificial intelligence.

Energy, particularly nuclear energy, natural gas and grid modernization, will be one of the most impactful investment and policy areas over the next decade.

5. The two economies are rising, but the gap is widening

The U.S. economy is splitting into capital-driven artificial intelligence sectors and labor-intensive traditional sectors, with little overlap between the two.

The two systems increasingly operate with different incentives.

Artificial Intelligence Economy (Expansion)

-

High productivity

-

high profit

-

Low labor intensity

-

Strong strategic protection

-

Strong capital attraction

Real economy (shrinking)

-

Weak labor absorptive capacity

-

consumer pressure

-

reduced mobility

-

asset concentration

-

Inflationary pressure is high

The most valuable companies of the next decade will build solutions to bridge or exploit this structural gap.

6. My vision for the future

-

Artificial intelligence will be supported or else there will be a recession.

-

Liquidity led by the Ministry of Finance will replace quantitative easing as the main policy channel.

-

Cryptocurrency becomes a political asset class tied to intergenerational equity.

-

Energy will become the real bottleneck in the development of artificial intelligence, not computing power.

-

Over the next 12 to 18 months, markets will continue to be driven by sentiment and capital flows.

-

Inequality will increasingly shape policy decisions.