Original title:Why did Bitcoin’s largest buyers suddenly stop accumulating?

Source: CryptoQuant; Compiled by: Bitchain Vision

For much of 2025, Bitcoin’s bottom looked impregnable, bolstered by an unlikely alliance between corporate treasuries and ETFs.

Companies issued stocks and convertible bonds to buy Bitcoin, and inflows of ETF funds quietly absorbed the new supply.Together, these factors have created a durable demand base that has helped Bitcoin weather increasingly tightening financial conditions.

Now, that foundation is shifting.

On November 3, Charles Edwards, the founder of Capriole Investments, published an article on X saying that as the pace of institutional accumulation slowed down, his optimistic expectations for the market have weakened.

He noted: “For the first time in seven months, institutional net buying fell below daily mining supply. It’s not good.”

Bitcoin institutional buying volume (Source: Capriole Investments)

According to Edwards, this is a key metric that keeps him optimistic even if other assets are outperforming Bitcoin.

However, he noted that as it stands, there are approximately 188 corporate treasury holdings of significant amounts of Bitcoin, many of which have business models limited to their exposure to the token.

Bitcoin treasury buying slows

No company typifies enterprise Bitcoin trading more than MicroStrategy, which recently shortened its name to Strategy.

The software maker, led by Michael Saylor, has transformed into a Bitcoin treasury company and now holds more than 674,000 Bitcoins, solidifying its position as the largest single corporate holder.

However, the pace of its purchases has slowed significantly in recent months.

For reference, Strategy accumulated approximately 43,000 Bitcoins in the third quarter, which was the company’s lowest quarterly purchase volume so far this year.This number is not surprising considering that some of the company’s Bitcoin purchases during this period plummeted to just a few hundred coins.

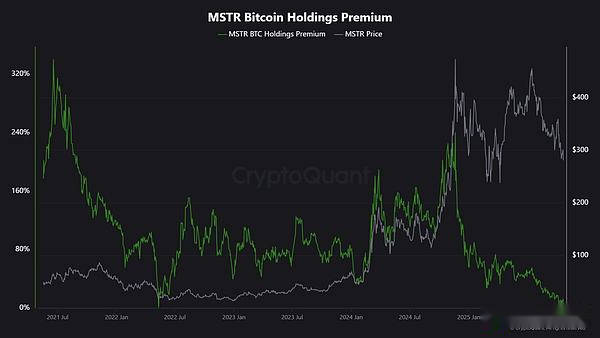

CryptoQuant analyst JA Maarturn explained that this slowdown may be related to the strategy’s declining net asset value.

He said investors used to pay a high “net value premium” for every dollar of Bitcoin on Strategy’s balance sheet, effectively allowing shareholders to share in the gains from Bitcoin’s rise through leverage.But that premium has narrowed since mid-year.

With fewer valuation tailwinds, issuing new shares to buy Bitcoin is no longer as value-adding as it once was, reducing the incentive to raise capital.

“Raising capital is more difficult. Equity issue premiums have fallen from 208% to 4%,” Maarturn noted.

MicroStrategy’s stock premium (Source: CryptoQuant)

Meanwhile, the cooling wave isn’t limited to MicroStrategy.

Metaplanet, a Tokyo-listed company modeled after U.S. Bitcoin pioneer MicroStrategy, recently saw its share price fall below the market value of its own Bitcoin holdings after experiencing a sharp decline.

In response, the company approved a stock buyback plan while issuing new financing guidelines to expand its Bitcoin reserves.The move shows the company’s confidence in its balance sheet, but also highlights waning investor enthusiasm for the “digital asset reserve” business model.

In fact, the slowdown in Bitcoin treasury acquisitions has led to mergers between some of these companies.

Last month, asset management company Strive announced the acquisition of smaller Bitcoin reserve company Semler Scientific.The deal will allow the companies to hold nearly 11,000 Bitcoins at a premium, with Bitcoin increasingly becoming a scarce resource in the industry.

These examples reflect structural constraints rather than a loss of faith.When equity or convertible bond issuance no longer enjoys a market premium, capital inflows will dry up and corporate capital accumulation will naturally slow down.

What is the flow of funds in ETFs?

Spot Bitcoin ETFs, long viewed as automatic absorbers of new supply, are showing similar signs of weakness.

These financial investment vehicles dominated net demand for much of 2025, with creations continuing to outpace redemptions, especially during Bitcoin’s surge to all-time highs.

But by late October, financial flows began to become erratic.Inflows turned negative in some weeks as portfolio managers adjusted positions and risk desks cut investment exposures in response to changing interest rate expectations.

This volatility marks a new phase in Bitcoin ETF behavior.

The macroeconomic environment has tightened and market expectations for rapid interest rate cuts have faded; real yields have risen and liquidity conditions have cooled.

Still, demand for Bitcoin remains strong, but now it comes in bursts rather than consistent waves.

SoSoValue’s data confirms this shift.Digital asset investment products attracted nearly $6 billion in inflows in the first two weeks of October.

By the end of the month, however, some of the gains were reversed as redemptions increased to more than $2 billion.

Bitcoin ETF weekly fund flows (Source: SoSoValue)

This pattern shows that Bitcoin ETFs have developed into a true two-sided market.They still provide ample liquidity and access to institutional investors, but are no longer vehicles for one-way accumulation.

When macroeconomic signals fluctuate, ETF investors can sell as quickly as they bought in.

Market Impact on Bitcoin

This changing situation doesn’t necessarily mean a recession, but it does mean greater volatility.As corporate and ETF absorption weakens, Bitcoin’s price action will become increasingly influenced by short-term traders and macroeconomic sentiment.

Edwards believes that in this case, new catalysts such as monetary easing, regulatory clarity or a return to stock market risk appetite may reignite the buying enthusiasm of institutional investors.

However, as marginal buyers currently appear more cautious, this makes price discovery more sensitive to global liquidity cycles.

So the impact is twofold.

First, the structural bids that once provided support are weakening.

During periods of insufficient supply and demand, intraday price fluctuations may intensify as fewer stable buyers reduce the ability to suppress fluctuations.Although the April 2024 halving policy mechanically reduces new supply, scarcity itself does not guarantee price increases without sustained demand.

Second, Bitcoin’s correlation is changing.As balance sheet expansion slows, Bitcoin may once again align itself with the broader liquidity cycle.Rising real yields and a stronger dollar are likely to weigh on prices, while looser market conditions could put it back on top amid rising risk appetite.

In essence, Bitcoin is re-entering a macro-reflexive phase, behaving less and less like digital gold and more like a high-beta risk asset.

At the same time, none of this negates Bitcoin’s long-term prospects as a scarce, programmable asset.

Rather, it reflects the growing influence of institutional factors that once insulated Bitcoin from retail price swings.The same mechanisms that propelled Bitcoin into mainstream investment portfolios are now making it more closely tied to the gravitational pull of capital markets.

The next few months will test whether the asset can maintain its store-of-value appeal without automatic corporate or ETF inflows.

If history is any guide, Bitcoin tends to adapt: when one demand channel slows, another tends to emerge—whether from sovereign reserves, fintech consolidation, or a renewed increase in retail participation during macro easing cycles.