Source: Galaxy; Compilation: Bitchain Vision

1. Background

On September 5, Hyperliquid, the leading decentralized on-chain perpetual contract exchange, announced a governance vote to grant the long-standing USDH code “Hyperliquid-first, aligned with Hyperliquid and compliant USD stablecoin.”This move breaks tradition.Hyperliquid’s code holding rights are usually sold every 31 hours in a Dutch auction, and the winner will destroy the network’s native token HYPE.At its peak, the HYPE value of these auctions was as high as $1 million, and now the settlement price is close to $20,000 to $40,000.

However, USDH is different.Since Hyperliquid already has a US$5.5 billion balance of USDC and more than US$200 million in external revenue flows to the stablecoin issuer, Circle, USDH represents a chance for the Hyperliquid network to regain this value.The vote winner will not automatically replace USDC as the dominant quote currency, but it will receive one of the most coveted digital properties on the network: the USDH name.

The statement sparked fierce competition among stablecoin issuers, with existing participants such as Ethena, Sky (formerly MakerDAO), Paxos, Agora, Frax Finance, Bastion and OpenEden, as well as newcomers such as Native Markets.This process itself sets a precedent.This is Hyperliquid’s first governance vote besides taking it off the shelves, and it is also a test of whether its network can guide decision-making in a decentralized way.

The ongoing governance process, the major proposals submitted, and the long-term impact of the vote are outlined below.

2. Voting process and timetable

This is the first major governance vote for Hyperliquid except for the removal of assets. The vote will be conducted entirely on the chain, and the voting rights of the verifier are proportional to the pledge weight.The USDH proposal was submitted at 10:00 UTC time on September 10 (6 pm Beijing time on September 10). Verifiers must declare their voting intention within 24 hours..Thereafter, users who have pledged HYPE can re-delegate the pledged HYPE to the verifier who meets their preferences.The final vote will be held from 10:00 to 11:00 UTC on September 14.

To be approved, the proposal must reach the quorum and receive at least two-thirds of the total pledge support.Currently, validators bound to the ecosystem manager Hyperliquid Foundation hold about 54% of the total stake.Therefore, Foundation validators will abstain until the quorum reaches, after which they will vote according to the wishes expressed by the community.Kinetiq, the ecosystem’s leading liquidity staking provider, also announced that it would abstain from the entitlement to the Foundation Verifier.Therefore, it is expected that approximately 63% of the total HYPE stake will not be directly involved, and the final decision will be left to the independent verifier.

For such an important vote, the timing was extremely tight.Multiple teams expressed concern that competitors don’t have enough time to propose a complete proposal, and voters don’t have enough time to digest all the proposals.Despite these objections, the Hyperliquid team has not extended the voting time.

3. Hyperliquid’s current stablecoin pattern

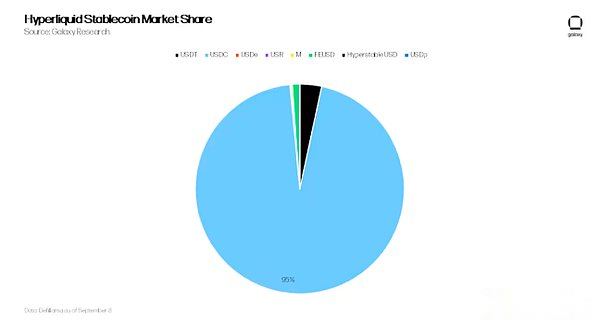

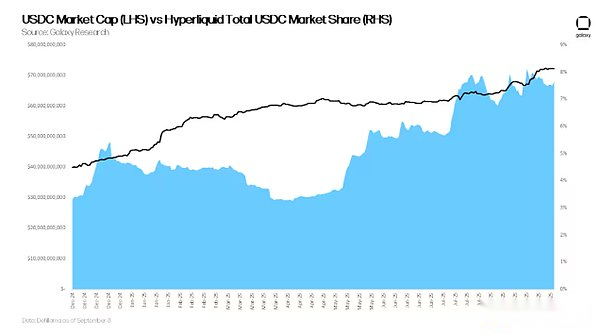

To date, Hyperliquid’s stablecoin market has been dominated by Circle’s USDC, the main margin, collateral and settlement currency for the Hyperliquid network.Circle issued approximately $5.5 billion in USDC on Hyperliquid, accounting for 95% of all Hyperliquid’s stablecoins.Unlike other blockchains directly cast by Circle,HUSDC on yperliquid is not natively issued, but is stored in the pool contract of the Ethereum layer 2 network Arbitrum.When users deposit USDC, their funds are added to the pool, and Hyperliquid’s back-end accounting system allocates the corresponding balance based on the participants’ share of USDC in the pool.Although Circle announced in July that it plans to issue native USDC on Hyperliquid through the upgraded Cross-chain Transfer Protocol (CCTP V2), it has not yet been implemented.The current reliance on bridging USDC raises security risks, as any vulnerability that affects collateral held by Arbitrum could directly compromise Hyperliquid’s transaction infrastructure.

Furthermore, although 8% of the total USDC issuance is present on Hyperliquid, the network does not gain any real value from such an arrangement.Worse, half of the USDC’s revenue generation is directed to Coinbase under the earnings share agreement with Circle, which undoubtedly provides value to Hyperliquid’s competitors.$5.5 billion worth of USDC, about $220 million in annual revenue flows to Circle and Coinbase.As a natively issued stablecoin, USDH can not only improve security and reduce dependency risks, but also redirect the benefits generated by the stablecoin balance to Hyperliquid.

Although Circle has stated that it will not submit a USDH proposal, it has not backed down.A few days after the announcement, Circle CEO Jeremy Allaire tweeted: “Don’t believe in the hype… We will make a big move into the HYPE ecosystem. We are committed to being a major player and contributor to the ecosystem.”

3. What rights does USDH have?

Clarify what are the key and what are not in USDH governance voting.Winning the vote does not mean that the team can control Hyperliquid’s stablecoins, nor does it mean that it automatically monopolizes transactions.In fact, there is only one vote: Issuing stablecoins with USDH as the code.

However, in a symbolic sense, the winner will also gain legitimacy and become the stablecoin issuer that best fits Hyperliquid values and governance.This recognition is crucial for integration, market maker support, and long-term adoption.

It is also important that the USDH code cannot guarantee anything.This does not mean that all USDC quote pairs on perpetual contracts or spot will suddenly migrate to USDH.Hyperliquid’s trading infrastructure is deeply rooted in USDC, and forced transfer of liquidity can damage the depth of transactions and user experience.

The code will not prevent competitors from going online either.In fact, many proposers have said they intend to deploy on Hyperliquid regardless of the vote.

In fact, USDH winners will gain strong brand influence and may take the default role in the new spot market launched under HIP-3 (this upgrade allows anyone, not just the Hyperliquid team, to launch the market with Hyperliquid’s infrastructure).However, whoever issues USDH must win adoption through liquidity, integration and execution.

Code is best understood as a consistent signal rather than a guarantee of dominance.Its true value will depend on how the issuer can effectively achieve market adoption.

4. The main contenders of USDH

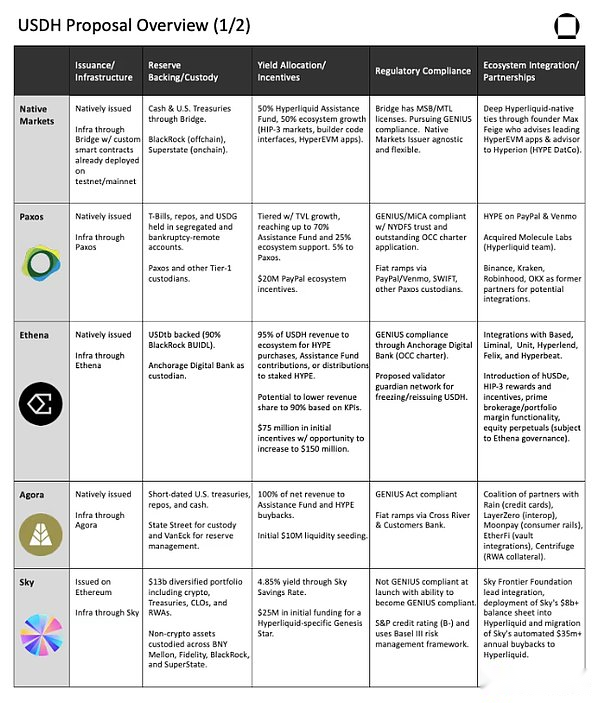

Here is an overview of the main proposals.Readers are also encouraged to read these proposals in full.These proposals are compared side by side in the appendix.

1. Native Markets

Native Markets is a newcomer to the stablecoin issuance field, but has been deeply rooted in the Hyperliquid ecosystem.Its founder Max Fiege was an early advocate of Hyperliquid and served as an advisor to several major applications on HyperEVM (network smart contract layer) and Hyperion, a listed treasury company that acquired HYPE.While Native Markets has no record of issuing stablecoins, it is the only team that has deployed and tested the circulation of tokens on the Hyperliquid testnet and the mainnet.

Native Markets, the first team to submit proposals, submitted proposals less than 90 minutes after posting the USDH announcement on Hyperliquid account X (formerly Twitter).The team submitted an extension proposal last Sunday as community feedback Native Markets’ initial proposal was too vague.The main contents of its proposal include:

-

Stablecoin Issuance and Infrastructure: USDH is issued natively on HyperEVM and can be combined on Hypercore, the network’s lightning-fast central limit order book.The infrastructure has been deployed and tested on the Hyperliquid testnet and mainnet; audits are currently underway.

-

Reserve support and custody: backed by cash and U.S. Treasury bonds.Off-chain reserves are managed by BlackRock, the world’s largest asset management company, and on-chain reserves are managed by Superstate through a service provider called Bridge.

-

Earnings Allocation and Incentives: 50% of reserve earnings will be used for Hyperliquid Assistance Fund; 50% will be dedicated to USDH growth, including collaboration with Builder Code Interfaces, HIP-3 Marketplaces and HyperEVM applications.

-

Regulatory Compliance and Fiatcoin Gateway: Regulatory Compliance is achieved through Bridge.Bridge is registered as a Money Services Enterprise (MSB) with the U.S. Treasury Department of Financial Crime Enforcement Network (FinCEN) and holds currency transfer licenses in multiple states, but has not yet obtained a license to fully comply with the recently passed GENIUS Act.The team is applying for more licenses to ensure future compliance with the GENIUS Act.

-

Ecosystem Integration and Partnership: Native Markets has deep ties to the Hyperliquid native market.As mentioned earlier, its founder, Max Fiege, was an early adopter and advocate for Hyperliquid.He serves as a consultant to several large HyperEVM applications and is also an advisor to Hyperion, a HYPE digital asset treasury company.

2. Paxos

Paxos is one of the oldest players in the stablecoin market, with products issued by it, such as BUSD (Binance White Label) and PYUSD (PayPal White Label), which have exceeded $160 billion.Paxos is known for its strict regulation and good cooperation with institutions and has a strong track record of expanding stablecoins with some of the world’s largest fintech companies.Paxos submitted its preliminary proposal on September 6, just 24 hours after Hyperliquid announced the USDH vote.On September 9, the team proposed a revision proposal based on community feedback.The main contents of this proposal include:

-

Stablecoin Issuance and Infrastructure: USDH is issued natively on HyperEVM and supports Hypercore combination functionality.Infrastructure utilizes Paxos’ proven technologies (e.g. PYUSD, BUSD, and USDP).Supports multi-chain interoperability.

-

Reserve support and custody: Reserves are kept in bankruptcy quarantine accounts and are backed by cash, US Treasury and reverse repurchase agreements.Hosting, regular audits, and monthly forensics are all in compliance with Paxos’ regulatory standards.

-

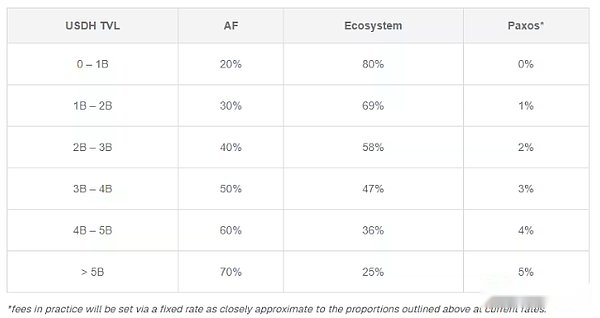

Earnings Allocation and Incentives: Paxos initially proposed to allocate 95% of reserve earnings to HYPE buybacks and redistribute them to protocols, validators and users, of which 5% are retained by Paxos for operations and reinvestment in USDH growth.In the revised proposal, Paxos introduced a new hierarchical allocation structure based on USDH total lock value (TVL) (see figure below).The team also added a $20 million incentive that its partner Paypal promises to provide to the HYPE ecosystem.

-

Regulatory Compliance and Fiatcoin Gateway: Passing Paxos is fully compliant with the U.S. GENIUS Act, EU MiCA regulations, and other global standards.Fiat currency in/out through global interbank information system SWIFT and custodial partners, as well as Venmo, Checkout and other export platforms.

-

Ecosystem integration and cooperation: It may be integrated with mainstream exchanges and wallets such as Binance, PayPal, Kraken, Robinhood, OKX, Anchorage, etc.The recent acquisition of Molecular Labs, the creator of the first HYPE liquid staking tokens and tokenized HLP products, strengthens its ties with Hyperliquid.In the revised proposal, Paxos said it will bring HYPE online in Paypal and Venmo and open the door to integration with Paypal’s 400 million users and 35 million merchants.Paxos also plans to build a revenue product that “embeds any consumer front-end with a simple API suite”, as well as a set of tokenized HLP products to drive the growth of HIP-3.

3. Ethena

Ethena Labs is the creator of USDe, currently the third largest stablecoin in the world with a total supply of over $13 billion.Ethena has been deployed on platforms such as Ethereum, Arbitrum, Binance BNB Chain, Optimism, Mantle, Kava and Linea, and has proven that it can be promoted on a large scale and is compatible with centralized and decentralized platforms.

Ethena submitted the USDH proposal on September 9 and was the last major issuer to submit it.The main contents of this proposal include:

-

Stablecoin Issuance and Infrastructure: USDH is issued natively on HyperEVM with Hypercore composability.

-

Reserve support and custody: Initially supported by Ethena’s USDtb (USDtb itself is 90% backed by BUIDL, a tokenized money market fund owned by BlackRock, whose collateral is escrowed at Bank of New York Mellon).In the future, you can choose to expand to Ethena’s other existing stablecoins, USDe, or the Hyperliquid native version hUSDe, with governance approval.

-

Earnings Allocation and Incentives: At least 95% of the initial reserve income will be used in the Hyperliquid ecosystem (Assistance Fund + HYPE repurchase).If key performance indicators (KPIs) are met (e.g., $5 billion supply, stable anchorage), it may be adjusted to 90%.Other possible incentives include Ethena points rewards, up to $150 million in HIP-3 front-end ecosystem grants, and liquidity loans and migration cost subsidies adopted by USDH.

-

Regulatory Compliance and Fiatcoin Gateway: Compliance is achieved through federally licensed crypto bank Anchorage Digital Bank.Supports GENIUS platform docking and realizes the inflow and outflow of global fiat currencies.

-

Ecosystem Integration and Cooperation: Potential integration of the Hyperliquid ecosystem includes: the launch of hUSDe, a synthetic dollar supported by uBTC and uETH (a tokenized version of the network that can be hedged through HyperCore); the introduction of HIP-3 reward mechanisms to reduce the perpetual transaction costs of using USDe margin; direct USDe hedging on Hyperliquid; and the expansion of margin support for major brokers and portfolios.Other initiatives include the use of Ethena to provide liquidity in stock perpetual contracts through collaboration with Unit (Hyperliquid’s tokenization layer), as well as extensive HyperEVM integrations such as LayerZero for interoperability, new earnings capabilities through Hyperlend, Felix and Hyperbeat, and Pendle earnings products enhanced by points incentives.

4. Agora

Agora positiones itself as an institutional-grade white label stablecoin infrastructure provider powered by traditional financial giants VanEck and State Street.The team’s model is centered on compliance, scale and partnerships and is directly connected to the global banking system.Agora’s flagship stablecoin, AUSD, has been issued $166 million and is available on more than 10 blockchains.Agora submitted its proposal on September 7.The main contents of this proposal include:

-

Stablecoin issuance and infrastructure: USDH is issued natively on HyperEVM, with the composability of HyperCore, and supports cross-chain interoperability through LayerZero.Agora’s white label stablecoin engine will provide fully collateralized Hyperliquid native products.

-

Reserve support and custody: Reserves include short-term U.S. Treasury bonds, overnight reverse repurchases and cash.These reserves will be managed by VanEck (with assets under management of over $130 billion) and custodial by State Street (with assets under management of over $49 trillion) and Chaos Labs will provide proof of on-chain reserves.

-

Earnings Allocation and Incentives: Agora invests 100% of net reserve income into the Hyperliquid ecosystem and distributes it to Assistance Fund and HYPE buybacks through quarterly governance votes.Additionally, Agora promises $10 million in liquidity seed funding on the first day.

-

Regulatory Compliance and Fiatcoin Gateway: Agora and its infrastructure are designed in compliance with the GENIUS Act and global regulations and will enable access/exit fiatcoin through cooperation with Cross River Bank and Customers Bank.

-

Ecosystem Integration and Partnership: Establish distribution partnerships through Rain (processing bank card payments for more than 2 billion users), Moonpay (ten millions of KYC-completed users), and EtherFi vaults.LayerZero interoperability supports liquidity access to dozens of blockchains.

5. Sky

Sky is the successor to MakerDAO, one of the oldest and most influential protocols in the DeFi field, which pioneered the decentralized stablecoins through DAI.Currently, Sky manages over $8 billion in circulating stablecoins (including DAI and newer USDS), and is backed by $13 billion in collateral.

Sky submitted its preliminary proposal on September 8 and provided more details the next day.The main contents of this proposal include:

-

Stablecoin issuance and infrastructure: issuance through the Sky protocol on Ethereum and bridged to Hyperliquid (technically the same as DAI/USDS).Implement native multi-chain through LayerZero.Integrated Sky’s anchored stability module (PSM), provides instant USD redemption liquidity worth $2.2 billion and can be exchanged with a revenue token called sUSDS to earn Sky savings rate (currently 4.75%).

-

Reserve Support and Custody: Powered by Sky’s $13 billion diversified portfolio, including cryptocurrency collateral, U.S. Treasury and Secured Loan Documents (CLOs).Provide transparency through the real-time dashboard on info.sky.money.

-

Earnings Distribution and Incentives: The yield rate of all USDHs is 4.85%, and all returns will be used for the Assistance Fund’s HYPE repurchase.Sky also promised $25 million to incubate Hyperliquid Genesis “Star”.This “Star” is based on Sky’s application module Spark and aims to promote the development of DeFi.

-

Regulatory Compliance and Fiatcoin Gateway: The Sky platform was not originally GENIUS compliant, but its modular design could open the door to USDH’s future customization to comply with GENIUS standards.Sky is the only stablecoin protocol that has received the official S&P Credit Rating (B-) and complies with the Basel III Collateral Risk Management Framework.

-

Ecosystem Integration and Cooperation: Leading the implementation of the Sky Frontier Foundation (Sky’s senior leaders and developers).Deploy Sky’s balance sheet of over $8 billion directly to Hyperliquid and migrate its $35 million annual repo system from Uniswap to Hyperliquid.In the future, USDH will be split into an independent “generator agent” to achieve complete autonomy, with autonomous governance, token mining on Hyperliquid, and customizable strategies (for example, to increase risk for competitive gains or regulatory priorities).

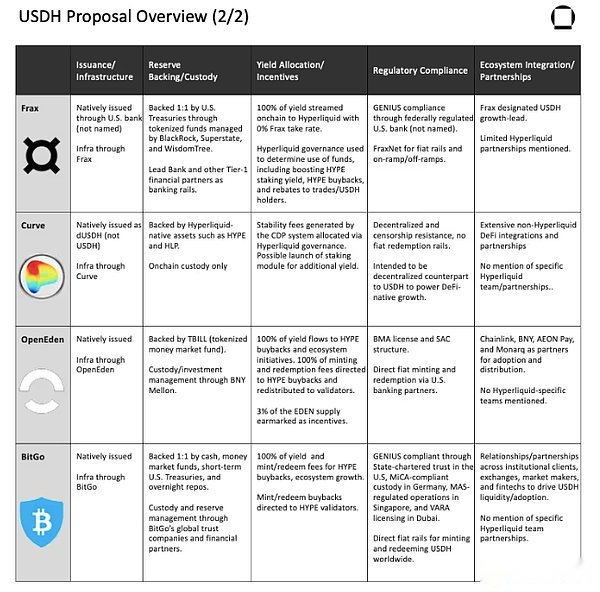

6. Frax

Frax Finance is known for its innovations in hybrid stablecoin design, with its products including FRAX, FraxLend and sfrxETH, reaching billions of dollars.Its flagship stablecoin FRXUSD has a market capitalization of $101 million.

Frax submitted a preliminary proposal on September 5 and revised comments on September 8.The main contents of its proposal include:

-

Stablecoin Issuance and Infrastructure: Frax initially proposed the issuance of non-native USDH, but later updated the proposal to issue Hyperliquid native stablecoins in partnership with a federally regulated bank issuer (name not published, pending signing agreements and legal review).The design uses FraxNet as the account layer to enable instant multi-chain connections across more than 20 chains, and is powered by LayerZero.

-

Reserve Support and Custody: Tokenized funds managed through BlackRock, Superstate and WisdomTree, powered by U.S. Treasury at a 1:1 ratio, and Fidelity will join soon.Lead Bank and other tier 1 financial partners, a fintech-focused institution, will provide banking support.

-

Earnings Allocation and Incentives: All base Treasury yields will be transferred to Hyperliquid in a programmatic manner, with Frax’s handling fee of 0%.Hyperliquid governance will determine how profits are used, such as increasing HYPE staking proceeds, targeted buybacks of HYPE for aid funds, or providing rebates to active traders/USDH holders.

-

Regulatory Compliance and Statutory Gateway: Issued by an undisclosed federally regulated Bank of America for a large-scale issuance of currencies that comply with GENIUS standards.The 1:1 minting/redeem between USDC, USDT and fiat currencies is powered by FraxNet, the team’s cross-chain interoperability infrastructure, providing institutional-level accessibility.

-

Ecosystem Integration and Partnerships: Frax did not include any major partnerships or integration plans in its proposal, but stated in a subsequent Q&A session that it will have a USDH growth lead with a focus on expansion/distribution.

7. Curve

Curve is best known for its stablecoin trading AMM design, launching one of the first decentralized exchanges optimized for stablecoin trading and pioneering the Voter Custody (veCRV) token governance model, which is now widely adopted in the DeFi space.In 2023, Curve launched crvUSD, a decentralized stablecoin with a circulation of US$231 million.What’s unique about its scheme is that it suggests that a second code dUSDH is reserved for a decentralized stablecoin built on the crvUSD collateralized bond warehouse (CDP) model.

Curve submitted its proposal on September 9.The main contents include:

-

Stablecoin Issuance and Infrastructure: The system will be powered by Curve’s LLAMMA architecture, which adopts continuous rebalancing rather than binary clearing, thereby increasing resilience during volatility.The governance of dUSDH will be under the responsibility of Hyperliquid, while Curve will provide the technology stack and operational support.

-

Reserve support and custody: dUSDH will be backed by hyperliquid native assets such as HYPE and HLP, thus directly linking the issuance of stablecoins with ecosystem development.dUSDH’s anchoring mechanism will be maintained through automatic exchange rate adjustments and Curve’s “pegkeeper” system, and uses Hyperliquid assets to stabilize the US dollar value.

-

Profit distribution and incentives: The stability fees generated by the CDP system will flow back to Hyperliquid governance, which will determine how to best allocate.The staking module can also provide stable annual interest rates for dUSDH holders while providing minters with a circular and leverage strategy.

-

Regulatory Compliance and Fiatcoin Gateway: Unlike other solutions, Curve’s dUSDH will be completely decentralized and censor-resistant.However, it does not provide fiat currency exchange channels or compliance coordination, so Curve positioned it as a supplement to the regulated USDH.

-

Ecosystem Integration and Partnership: By supporting minting for hype and high liquidity providers (HLPs), dUSDH will have a flywheel effect: users can borrow, trade and recycle in Hyperliquid, thereby enhancing the practicality of native tokens.This complements the regulated USDH path and gives Hyperliquid a dual stablecoin strategy: one for institutional adoption and the other for DeFi native leverage and growth.

8. OpenEden

OpenEden is an issuer of institutional-level tokenized real-world assets and the largest on-chain U.S. Treasury bond provider in Asia.Founded in 2022, the company has launched several products such as USDO, a stablecoin issued under a Bermuda regulatory license, and TBILL, a tokenized money market fund, which is one of the oldest funds in the industry.

OpenEden submitted its proposal on September 9.The main contents of its proposal include:

-

Stablecoin Issuance and Infrastructure: USDH will be issued through OpenEden Digital, a wholly-owned subsidiary of the Bermuda Financial Authority (BMA) that holds a Class M digital asset business license.USDH issuance adopts a bankruptcy segregation stand-alone account company (SAC) structure to ensure that USDH reserves are legally isolated from the issuer’s liabilities.The reserves will be supported by TBILL, creating a transparent and independent rating basis.

-

Reserve Support and Hosting: USDH will be powered by TBILL.TBILL is a tokenized money market fund that invests in short-term U.S. Treasury bonds and has an independent rating (Moody’s A, S&P AA+f/S1+).Custody and investment management are provided by Bank of New York Mellon.Chainlink oracles will be used for data feeding, proof of reserves, and cross-chain interoperability (CCIP through Chainlink’s cross-chain interoperability protocol).

-

Profit Allocation and Incentives: All coin and redemption fees will be used for HYPE repurchases and redistributed to validators.All underlying reserve earnings (approximately 4% from TBILL) will also be used for HYPE repurchase and ecosystem programs.In addition, 3% of the total supply of EDEN tokens will be used to incentivize USDH adoption on Hyperliquid.

-

Regulatory Compliance and Fiatcoin Gateway: OpenEden emphasizes its regulatory coverage through its BMA license and SAC architecture.USDH will support direct minting and exchange of fiat currencies through Bank of America partners, as well as exchanges through USDC.

-

Ecosystem Integration and Cooperation: In addition to Bank of New York Mellon, OpenEden also works with Chainlink to provide data, proof of reserves and cross-chain transfer support.These integrations are designed to ensure USDH is widely used in DeFi and institutional settlement systems.

9. BitGo

BitGo is one of the oldest custodians in the cryptocurrency space, founded in 2013 and currently manages over $90 billion in assets on the platform.The company operates six regulated trust entities around the world and provides custody services for major tokenized assets such as WBTC and USD1 (stablecoins launched by World Liberty Financial of the Trump family).BitGo submitted its proposal on September 10.The main contents of this proposal include:

-

Stablecoin Issuance and Infrastructure: USDH will be issued natively on Hyperliquid and deployed on HyperEVM and HyperCore, which can be exchanged for fiat, USDC and USDT 24/7 through integrated banking channels.BitGo emphasizes that USDH is not a wrapper, but is completely endorsed by equivalent dollars.Interoperability with other blockchains will be achieved through Chainlink’s CCIP.

-

Reserve Support and Custody: Each USDH token will be fully supported by cash, money market funds, short-term US Treasury bonds and overnight buybacks in a 1:1 ratio.Custody and reserve management will be responsible for BitGo’s global trusts and supplemented by financial institution partners in multiple jurisdictions.Transparency will be provided through a two-month third-party audit and will be validated on-chain through Chainlink’s proof of reserve service.

-

Earnings Allocation and Incentives: Reserve income will be used in a programmatic way to purchase and pledge HYPE, with a pledge cap of 20% per verifier to avoid centralized risks.The pledge reward will be distributed proportionally to USDH holders, a portion of which can be optionally assigned to the Assistance Fund by the Hyperliquid governance body.BitGo will charge a 30 basis point fee on reserve balances, citing the need to ensure sustainability even in low interest rates.

-

Regulatory Compliance and Fiatcoin Gateway: BitGo has an extensive global regulatory network, including U.S. state government chartered trusts, German MiCA-compliant custodians, Singapore’s MAS-regulated operating organizations, and Dubai’s VARA license.These networks combine with mature banking relationships to ensure unimpeded access to fiat currency direct minting and exchange USDH on a global scale.

-

Ecosystem Integration and Partnerships: BitGo plans to drive instant liquidity and application of USDH by leveraging its thousands of institutional clients and good relationships with exchanges, market makers and fintech companies.With its in-depth staking infrastructure in place, BitGo emphasizes its ability to quickly integrate USDH into its global institutional workflow.

10. Other proposers

-

Bastion

-

Ultra Sound Dollar on Hyperliquid (accessible via Discord only)

-

Konelia Team (accessible via Discord only)

5. Pre-voting (verifier statement) preferences

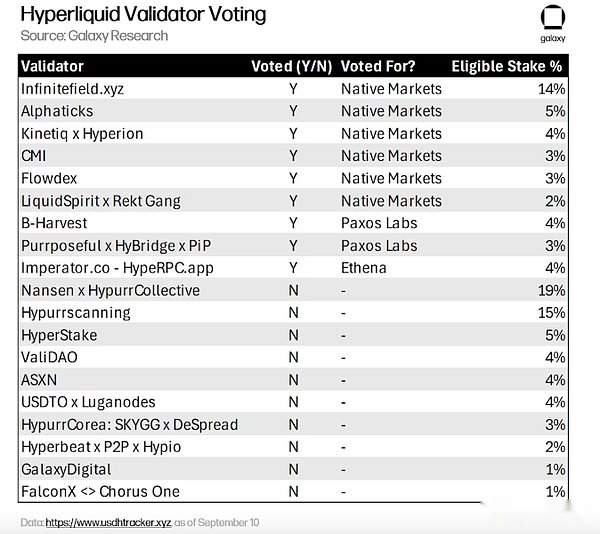

With the official proposal window closed, the focus has shifted to the validator statement, which will be released on Thursday at 10:00 UTC time.A total of 19 validators are eligible to participate in addition to Foundation Verifiers.As of Thursday morning, nine validators have declared, accounting for 43% of the qualified stake.These weights are still likely to change before the final vote on Sunday, as HYPE stakers may pledge them to validators that meet their preferences.

Early voting preference highlights several key trends:

Early voting preference highlights several key trends:

-

Hyperliquid alignment is crucial: To date, the vast majority of validator endorsements have placed Hyperliquid priority alignment first.Native Markets gains extensive validator support with its focus on Hyperliquid, without competing chains, tokens or external priorities.Supporters believe that this unique dedication is crucial to maintaining cyber sovereignty, in stark contrast to Native Markets’ large issuers who may have conflicts of interest with other stablecoin products, such as Paxos or Ethena.Even validators who ultimately support Paxos or Ethena recognize consistency as critical and position their choice to promote ecosystem development without compromising Hyperliquid independence.The general view is that while the compliance framework and technology stack can be replicated, the true Hyperliquid priority commitment cannot be commoditized.For many validators, this ecosystem loyalty is far superior to the resources and scale provided by experienced issuers.

-

Regulatory Compliance and Experience: Those who did not vote for Native Markets stressed that proven regulatory compliance and institutional track record are crucial.Paxos supporters noted that Native Markets’ history of New York Trust License, global licensing coverage and issuance of more than $160 billion stablecoins gives it a unique ability to issue USDH under the GENIUS Act and the MiCA in Europe.Ethena supporters stressed that the company is massive, able to safely manage billions of dollars in funding and can be deployed through Anchorage custody and BlackRock-backed reserves, providing infrastructure that is usually reserved for large stablecoins only.These validators believe that compliance and operational resilience are crucial for long-term survival, especially in response to crises and regulatory scrutiny.In addition, there are concerns about Native Markets’ dependence on third-party offerings such as Stripe, which has raised questions about its dependence on suppliers.The debate reflects that some people prioritize proven compliance, while others are willing to trust teams that are updated but aligned with the ecosystem, and they will catch up.

-

Promoting ecosystem growth through earnings sharing and incentives: The core motivation in the validator statement is how USDH earnings and incentives will drive Hyperliquid growth.Native Markets supporters emphasize their dual strategy of using reserve earnings to reinvest in HYPE buybacks and ecosystem expansion and define it as a sustainable flywheel.Ethena’s proposal attracted validators as it promises to provide at least 95% of its revenue, delivers up to $150 million in ecosystem grants, covers migration costs, and provides liquidity loans to market makers.Paxos supporters noted the $20 million incentive commitment it partnered with PayPal, and ultimately expanded to global consumer and business adoption.Validators generally believe that earnings sharing models, liquidity commitments and integration are key levers driving adoption, but there are differences in prioritizing short-term incentives or long-term reinvestment.

-

Strict evaluation process and community engagement: The last trend in validator communication is that they place great emphasis on presenting decisions as the product of strict transparent processes.Many validators refer to stakeholder consultation, AMA and proposal reviews, and often publicly share scoring frameworks or evaluation criteria.Validators emphasized independence.Verifiers, including Imperator, explicitly deny any financial relationship with the issuer to emphasize neutrality.Other validators, such as IMC and Infinite Field, emphasize that community engagement is at the heart of its deliberations, positioning themselves as managers rather than gatekeepers.HypurrCollective, the most staked validator, has not yet announced a vote, but it has even released a comprehensive framework for making decisions based on stakeholder preferences, Telegram and X polls, and the stance of its own team.USDH’s decisions are not just about selecting issuers, but also demonstrates Hyperliquid’s increasingly mature governance mechanism.

Ultimately, the situation is that on one side is idealistic support for Native Markets, the native leader of Hyperliquid, and on the other side is pragmatic support for existing companies like Paxos and Ethena that focus on compliance.However, one thing in common among all camps is optimism.Each validator urges cooperation at the end of the statement, regardless of the outcome.

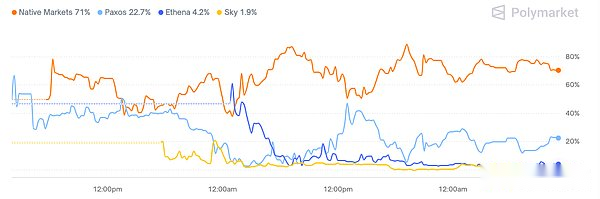

Polymarket’s forecasting market also clearly predicts the potential outcomes of the vote to some extent.Native Markets has remained ahead since the market went live, which is consistent with the current voting distribution.

6. Impact on Hyperliquid

Pay distribution fees

The competition from USDH highlights the shift in the stablecoin issuance landscape, and issuers must pay more and more issuance fees.A few days after the USDH issuance process started, Ethena reflected this trend, announcing that it will be launched on the Ethereum Layer-2 platform MegaETH, and the proceeds from its stablecoins will be used to pay for the cost of the sorter.The issuer no longer takes all his income to himself, but needs to reinvest the income into its issuance ecosystem, essentially gaining attractiveness through subsidy adoption.In this model, in addition to brand awareness, the most important factor is how much value the issuer is willing to return.Currently, Tether (the largest stablecoin issuer) is the main winner of stablecoins with its unparalleled coverage and ability to maintain its issuance without making such concessions.

Commitment and execution risks

A central question in the USDH competition is what happens if the winning team fails to fulfill its commitment.Building a secure, compliant, liquid and integrated stablecoin infrastructure is not easy, and the tight voting time has been the reason for repeated criticism throughout the process.The proposal looks good on paper, but the team has less than a week to develop, and the key details are not yet known, which amplifies execution risks.Therefore, many proposals are more like letters of intent than binding commitments.This raises the question: whether the governance process should postpone the voting until the team can submit a more specific, audited and executable proposal.This hasty approach could lead to priority speed over thorough due diligence, and also raise questions about what would happen if the team failed to deliver on its promises.

Regulatory compliance

While most proposals emphasize that the regulatory status of the U.S. and compliance with the GENIUS Act are its competitive advantage, it is questionable whether anchoring USDH to a U.S.-regulated issuer will really pose risks to Hyperliquid and its markets.RFI calls for a “compliant” stablecoin, but does not specify which type of compliance it is, and validators can choose to weigh whether binding USDH to an OCC charter or state charter entity will inadvertently create a U.S. connection that Hyperliquid does not need.This could unnecessarily expose the Hyperliquid market if U.S. authorities take a hostile stance on the agreement.That being said, issuers can build the issuance structure through offshore entities while still adopting the collateral quality and design of the GENIUS Act framework.Therefore, one question that validators may need to think about is whether regulatory ties with the United States represent stability and credibility or an avoidable source of potential risks.

Deployment and first-mover advantage

Another uncertainty is whether the winning team will lead the way.Several issuers, including Native Markets, Paxos, Agora, Sky and Ethena, said they could launch Hyperliquid native stablecoins regardless of the outcome.Native Markets said the stablecoin could be deployed as early as next week.If so, the “winner” of the voting may not be the first team to go public.This makes the considerations of validators and communities more complicated: Is the symbolic weight of the code more important than the speed and quality of actual deployment?

USDH as a governance precedent

This is the first time that Hyperliquid has run a governance process outside of the removal process.What other issues will the community vote on next?Validators need not only trade-offs on technical preparation, but also on value consistency, counterparty trust, and execution risks.Future votes on agreement revenue, upgrades or cross-ecosystem partnerships can emulate this strategy.USDH is both a test of Hyperliquid governance maturity and a test of stablecoin decision-making.

“Ethereum Alignment” comparison

Ethereum has been talking about “alignment” for years, but in reality, there is almost no largest protocol or Layer2 that returns meaningful value to ETH holders.Instead, they create value by expanding EVM coverage and promoting wider development of the Ethereum ecosystem.One of the most striking features of the USDH proposal is its value alignment with Hyperliquid, and each major USDH competitor promises to use 95% to 100% of the reserve income to add value to the Hyperliquid ecosystem.This is very different from Ethereum’s specification, which could be a decisive advantage of Hyperliquid if the model proves sustainable.That being said, there is also a potential negative impact on this alignment: It may undermine the need for users to hold USDH.Without some form of holder incentive, users may be more willing to hold their funds in earning alternatives and exchange them for USDH only when trading is required.This may limit USDH’s circulation and slow its popularity.

7. Conclusion: Hyperliquid will win anyway

Regardless of the USDH vote, one conclusion is clear: the real winner is Hyperliquid.This process forces some of the largest stablecoin players not only to compete for USDH code, but also openly promises to remain consistent with the Hyperliquid ecosystem as unprecedented.Issuers portray themselves as indispensable partners, but in reality, their demand for Hyperliquid is much greater than what Hyperliquid needs for them.What the issuer wants is distribution, liquidity of Hyperliquid, traders and narrative momentum.In fact, USDH forces issuers to compete for distribution within Hyperliquid, not the other way around.Whether through regulated fiat-backed models or decentralized designs, issuers are adjusting their economic conditions, partnerships and infrastructure to benefit Hyperliquid.The vote will determine who will use the USDH code, but Hyperliquid has gained the most important thing: being recognized as a network that is strong enough to reshape the cumulative landscape of stablecoin value.

8. Appendix