Author: Prathik Desai, Source: Token Dispatch, Compiler: Shaw Bitcoin Vision

Over the past week, I analyzed two very different Bitcoin business models.One is to purchase Bitcoin through debt and equity financing, and the other is to consume energy for mining.The former Strategy is the largest corporate reserve holder of Bitcoin, while the latter Marathon is the largest Bitcoin miner.

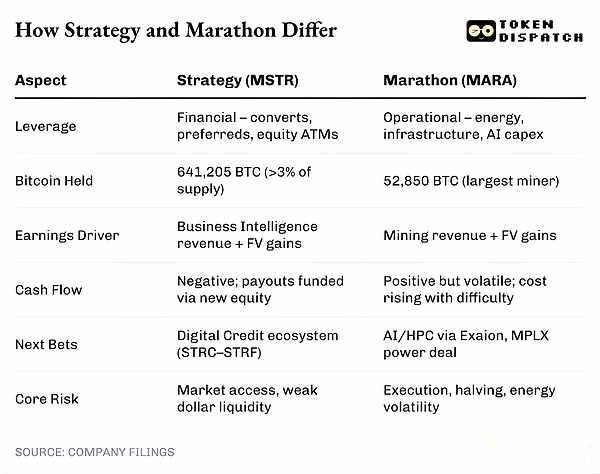

My understanding is that Strategy and Marathon Digital are like the yin and yang of the enterprise cryptocurrency space.While they both claim to be “always bullish on Bitcoin,” this mantra is very different in their respective business practices.

One side is using financial products that are less than five years old to realize the financialization of its beliefs, while the other side is using mechanisms that have been tested in the 16 years since Bitcoin was born to realize the industrialization of its beliefs.However, both parties have made billions of dollars (on paper), operated with different forms of leverage, and both have found ways to make holding Bitcoin attractive to investors with their business models.

This all got me thinking, what happens when your income depends on a currency that you have no control over?Are you running a business or a fiercely loyal religious organization?

In this article, I will analyze the earnings of two public companies that have built huge business empires based on the same cryptocurrency and explore their similarities and differences.

Two houses, the same token

In West Texas, the heat from mining machines rolls in; in Virginia, it’s the glow of Bloomberg terminals.Both places are betting on the same asset – Bitcoin.

Michael Saylor’s Strategy and Fred Thiel’s Marathon top the list of corporate Bitcoin reserves, with a combined holding of more than 690,000 Bitcoins.That’s more than Starbucks’ coffee sales in 2023 and 2024 combined.

What’s more interesting is how these two companies got to this point and what they do with their Bitcoin holdings.

Thaler’s company issued bonds and then used the money raised to buy Bitcoin, hoarding it much like a central bank hoards gold.Thiel’s energy company walks the line between two realms – it mines Bitcoin like any other commodity, but uses computers instead of traditional mining equipment; then, like Strategy, it buys more Bitcoin from the market.

They both profit from the same token, although not always in the form of cash.

Strategy reported operating income of $3.9 billion and net profit of $2.8 billion.However, all of the gains came from an accounting method that allows Strategy to book the unrealized appreciation of its Bitcoin holdings after applying a fair value measurement.The company has never sold a single Bitcoin since it began hoarding in 2020.

Strategy currently holds 641,205 Bitcoins, accounting for more than 3% of the total Bitcoin issuance, and the average purchase cost of each Bitcoin is approximately US$74,000.Whenever the price of Bitcoin rises above this level, Strategy makes a paper profit by marking the market cap of its Bitcoin holdings.

Strategy’s net profit has moved almost in lockstep with Bitcoin since it adopted fair value accounting in January.

The company suffered losses when the price of Bitcoin fell below $85,000 in March; it subsequently turned a profit in the second and third quarters, with Bitcoin closing above $107,000 and $114,000 on June 30 and September 30, respectively.Today, the company operates in perfect sync with Bitcoin’s price cycle, constantly buying but never selling.

borrow belief

In keeping with its philosophy of never selling, Strategy supports its Bitcoin buying strategy with a financing model.

It raises money by issuing low- or no-interest convertible bonds and preferred shares that pay steady dividends rather than pursue growth.Investors continue to buy, convinced that as long as the price of Bitcoin rises, the equity gains embedded in it will far exceed the coupons they give up.

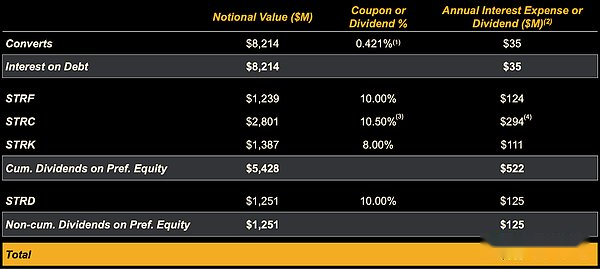

As of October 24, Strategy had raised $8.2 billion in low-interest convertible bonds with an earliest maturity date of 2028, which is just enough to maintain its “buy more Bitcoin” strategy.

In addition to convertible bonds, Strategy relies on what it calls a “digital credit ecosystem.”Through this system, it offers a range of perpetual preferred shares (STRC, STRF, STRK and STRD), allowing investors to choose their preferred type of Bitcoin exposure through dividend categories.

As of Oct. 24, Strategy had raised $6.7 billion in perpetual preferred stock.

Overall, the cost of the convertible debt and equity would require Strategy to pay approximately $689 million in interest and dividends annually.

So where does it get the money to pay for these expenses?The answer: from new investors.Strategy continues to raise capital by issuing shares at market prices, selling new shares when investor enthusiasm builds.

All of these financial models form a cycle: raising funds to continually buy Bitcoin, which helps achieve dollar-cost averaging.With every increase in the price of Bitcoin, companies reassess the value of their Bitcoin holdings and show profits.These proceeds are then used in earnings reports to gain trust and issue more shares.Then the whole process repeats again.

The whole loop works fine until something goes wrong.

Although Strategy holds approximately $65 billion worth of Bitcoin reserves, the company currently does not receive any revenue from hoarding the cryptocurrency.At least not yet.Its legacy business, which includes selling business intelligence product licenses and subscription services, generated $128.6 million in revenue and $90.6 million in gross profit during the quarter.Revenue rose 10% year over year, beating analysts’ expectations but not nearly enough to cover its $689 million in dividend and interest expenses.

After Strategy released its financial report, its stock price rose 8%, hitting a high of $276 per share during the session, but has since given up all gains, closing at $255 on November 5.

As of September 30, Strategy had a cash balance of approximately $56 million.

All in all, these are red flags that investors need to be aware of.

Last week, S&P Global downgraded Strategy’s credit rating to junk status “B-” for the first time.Although S&P Global gave the company a stable outlook, it also pointed out the above-mentioned problems of the company: excessive Bitcoin holdings, low risk-adjusted capital adequacy, and insufficient U.S. dollar liquidity.

Operating cash flow was negative in the first half.That means its strategy of using new capital to finance current spending could fail if capital markets turn risk-averse.

Industrialization of Bitcoin

Strategy proudly claims to be the world’s largest Bitcoin treasury company, while Marathon Digital (MRAR) made it clear in its quarterly shareholder letter ending September 30, 2025 that “we are not a Bitcoin treasury company.”This is despite the fact that the company operates the largest public Bitcoin mining farm in the world and holds more Bitcoins than any other miner.

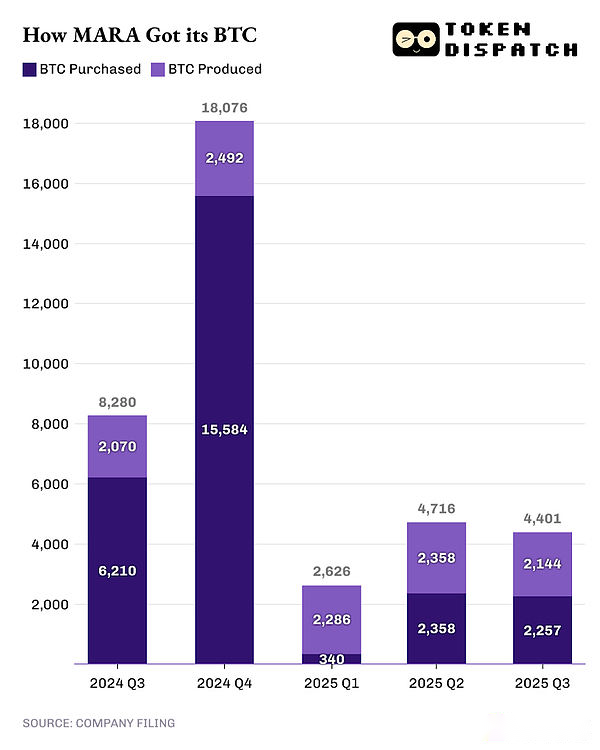

Unlike Strategy, Marathon acquires Bitcoin through two methods: mining and open market purchases.In Q3 2025, Marathon mined 2,144 Bitcoins and purchased 2,257 Bitcoins from the market.

Marathon also differs from Strategy in how it deploys its Bitcoin assets to achieve sustained profitability.

About one-third of the 52,850 Bitcoins held by Marathon have been loaned, pledged or used in other investment strategies.In the third quarter of 2025, Marathon earned $9.6 million in interest income from lending 10,377 Bitcoins.That’s a significant amount of cash flow for a company whose net income, excluding paper profits, is negative.

This is another reason why Marathon should expand its business focus beyond purely Bitcoin mining, buying, and holding.

Diversify risk and reward

Marathon’s recent business activity hints at how the company plans to expand its revenue streams in different business areas by doubling down on its computing power.

In August, Marathon signed an agreement to acquire 64% of Exaion for $168 million.Exaion develops and operates high-performance computing (HPC) data centers and provides secure cloud and artificial intelligence infrastructure.The deal will expand MARA’s presence in Europe’s enterprise artificial intelligence cloud business, an industry expected to be worth a trillion dollars by 2031.

On November 4, Marathon also signed a letter of intent with energy infrastructure and logistics asset provider MPLX LP.Under the agreement, MPLX will supply natural gas to Marathon’s new 400-megawatt power plant and data center campus in West Texas.

I view these announcements as a precaution against the unique volatility and risks faced by businesses that are only betting on Bitcoin.While Strategy’s approach to acquiring Bitcoin at a lower acquisition cost worked, Marathon and other businesses buying Bitcoin did not have this advantage.This puts them at greater risk of liquidation and the risk of losing investor confidence if the price of Bitcoin falls below the purchase cost.

For Marathon, these business expansions are both critical and timely given its current financial situation.

Although Marathon’s third-quarter revenue increased 92% year-on-year to US$252 million, and net profit soared 200% to US$123 million, these figures include a US$343 million fair value gain generated by marking its Bitcoin positions at market value.The company reported earnings of $0.27 per share, well ahead of its previous forecast of a loss of $0.10 per share.However, since the earnings release, its stock price has fallen from $17.81 to $17.13.

Against this backdrop, Marathon’s transformation from a Bitcoin mining company into a vertically integrated energy-to-artificial intelligence conglomerate became inevitable.

Faith and fair value profits

There’s an interesting paradox in telling stories with numbers.Although the world believes that numbers are objective and fair, different narrators may interpret the same set of numbers differently.

Financial statements are a prime example of a business using the same set of numbers to tell a variety of different stories.For example, both Strategy and Marathon’s financial statements show strong paper profits, indicating that both companies are in financial health.However, these numbers mask underlying challenges that, if ignored, could lead to the failure of both companies and their strategies.

Strategy calls Bitcoin “digital capital” and uses it to issue perpetual preferred shares similar to interest-bearing Bitcoin bonds.Marathon not only uses its computing infrastructure to mine and profit from it, but also expands its revenue sources into artificial intelligence and enterprise cloud businesses.

Both will ultimately face different challenges if they rely too much on Bitcoin.If interest rates rise or liquidity tightens, Strategy may become less attractive to investors.If energy prices rise or network difficulty grows faster than computing power gains, Marathon’s profit margins could be squeezed.In addition, the inevitability of the block reward halving in 2028 cannot be ignored.

One company is betting that the value of Bitcoin will always be higher than its debt, while another hopes that the cost of mining Bitcoin will always be lower than its market value.

Currently, both Strategy’s “spreadsheet” and Marathon’s “server” are keeping pace with Bitcoin’s movements.It will be interesting to see how their business develops once Bitcoin prices begin to move adversely for an extended period of time.