Important points

-

The interest rate cut was 25 basis points, Milan opposed it, believing that it should be reduced by 50, but Cook did not object.

-

There is not much information about the table reduction schedule.

-

There was almost no particularly unexpected part of the meeting, and the market experienced some medium-level volatility.

-

The US dollar is the winner, gold is the loser, and 10y US bonds rebounded after breaking downwards through the 4% level.

-

In terms of the impression of the press conference, Powell looked very chessy and felt in poor condition.

-

The reporter’s questions focus on employment data, tariffs and independence issues.

-

On the issue of independence,Powell’s words are tough, he is shy about talking about Trump faction and looks a little disdainful.He mentionedIndependence is rooted in the Fed culture and is a gene.

-

It is normal for the remarks about risk balance to have a higher tendency toward employment risks, because the data is not favorable recently. Overall, the tone is neutral, and there are a little hawkish.

FOMC Statement

Recent indicators show that economic activity growth slowed down in the first half of this year.Employment growth slowed down, and the unemployment rate rose slightly but remained at a low level.Inflation has risen and remains at a high level.

The Commission strives to maximize employment and inflation of 2% over the long term.The uncertainty of the economic outlook remains high.The Committee is concerned about the risks of its dual mission,It is also believed that the downward risk of employment has increased.

To support its goals and in view of changes in the risk balance, the Commission decided to lower the target range of the federal funds rate by 1/4 percentage point (25bp) to 4% to 4-1/4%.When considering additional adjustments to the federal funds rate target range, the committee will carefully evaluate the upcoming data, evolving prospects, and risk balance.The Commission will continue to reduce its holdings of Treasury bills, institutional debt and institutional mortgage-backed securities.The Commission is firmly committed to supporting the goal of maximizing employment and returning inflation to 2%.

In evaluating appropriate positions in monetary policy, the Commission will continue to monitor the impact of upcoming information on the economic outlook.If risks arise that may hinder the achievement of the Commission’s goals, the Commission will be prepared to adjust its monetary policy position, as appropriate.The Commission’s assessment will consider a wide range of information, including labour market conditions, inflationary pressures and inflation expectations, as well as financial and international developments.

Members who voted for the monetary policy action include: Chairman Jerome H. Powell; Vice Chairman John C. Williams; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Ostan D. Goulsby; Philip N. Jefferson; Alberto G. Mousalem; Jeffrey R. Schmid; and Christopher J. Waller.Stephen I. Milan votes against the action, he tends to cut the federal funds target range by 1/2 percentage points at this meeting.

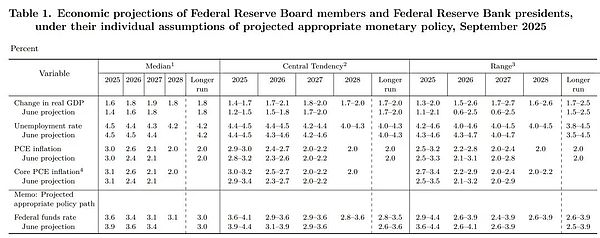

Economic Forecast

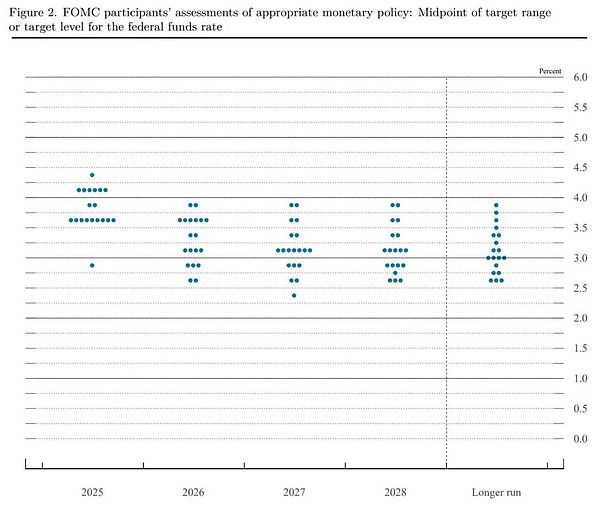

Dot map

Powell press conference record

Powell:

good afternoon.My colleagues and I remain completely focused on achieving our dual mission goal of maximizing employment and stabilizing prices for the American people.Although the unemployment rate is still low, it has risen.Employment growth has slowed down.The downside risk faced by employment has increased.at the same time,Inflation has risen recently and remains slightly higher.To support our goals,And considering the changes in risk balanceToday, the Federal Open Market Committee (FOMC) decided to lower our policy rate by 0.25 percentage points.We also decided to continue to reduce our holdings in our securities.After a brief review of economic development, I will talk more about monetary policy.

Recent indicators show that GDP growth rate in the first half of this year was about 1.5%, lower than 2.5% last year.The slowdown in growth mainly reflects the slowdown in consumer spending.In contrast, investment in commercial equipment and intangible assets has accelerated compared to last year.Activity in the real estate market remains weak.In our Summary of Economic Forecasts (SEP), the median forecast for participants is 1.6% GDP growth this year and 1.8% next year, which is slightly stronger than the June forecast.

On the labor market, the unemployment rate rose slightly to 4.3% in August, but has changed little in the past year and is still at a relatively low level.The growth of non-farm employment has slowed significantly to an average of only 29,000 per month in the past three months.This slowdown may largely reflect a decline in labor force growth due to reduced immigration and reduced labor force participation.Even so, labor demand has softened and the recent rate of employment creation seems to be lower than the “break-even” level needed to maintain unemployment rate stability.In addition, wage growth continues to slow, but still exceeds inflation.

Overall, the market conditions in which labor supply and demand slowed simultaneously is unusual.In this less vibrant and slightly weak labor market, the downside risk of employment seems to have risen.In our SEP, the median forecast for the unemployment rate at the end of this year is 4.5%, which will drop slightly after that.

Inflation has fallen significantly from its mid-2022 highs, but remains slightly higher than our 2% long-term target.Estimates based on the Consumer Price Index (CPI) and other data show that overall personal consumption expenditure (PCE) prices rose by 2.7% in the 12 months to August; core PCE prices rose by 2.9% after excluding the volatile food and energy categories.These readings are higher than earlier this year,Because commodity inflation rebounded.By comparison,Inflation in the service industry appears to be continuing to decline.

Affected by the tariff news,Recent inflation expectations indicators have generally risen this year, which is reflected in both market and survey-based indicators.However, after the next year or so, most long-term expectations indicators remain in line with our 2% inflation target.The median forecast for overall PCE inflation in SEP is 3.0% this year, down to 2.6% in 2026 and to 2.1% by (2028).

Our monetary policy actions are guided by the dual mission of promoting the American people to maximize employment and stabilize prices.At today’s meeting, the committee decided to lower the target range of federal funds rate by 0.25 percentage points to 4% to 4.25%, and continue to reduce our balance sheet.Changes in government policies are still evolving, and their impact on the economy remains uncertain.Higher tariffs have begun to push up prices in certain commodity categories, but the overall impact of its on economic activity and inflation remains to be seen.A reasonable benchmark scenario is,Its impact on inflation will be relatively short-term and a one-time price level change.butIt is also possible that the inflation effect will be more persistent, a risk that needs to be evaluated and managed..Our responsibility is to ensure that one-time price increases do not evolve into persistent inflation problems.

In the short term,Inflation risks tend to rise, while employment risks tend to fall, which is a challenging situation.When our goals are contradictory like this, our framework requires us to balance two aspects of our dual mission.As employment downward risks increase, the balance of risks has changed.Therefore, we believe that further measures are appropriate to take at this meeting to move towards a more neutral policy stance.

Through today’s decision, we are still in a good position to respond to potential economic development in a timely manner.We will continue to determine appropriate monetary policy positions based on future data, changing outlooks and balance of risks.In our SEP, FOMC participants wrote their personal assessment of the appropriate path to federal funds rate based on their respective judgments on the economic most likely scenario.The median forecast for participants is that the appropriate level of federal funds rate will be 3.6% by the end of this year, 3.4% by the end of 2026 and 3.1% by the end of 2027.This path is 0.25 percentage points lower than the June forecast.As always, there is uncertainty in these individual predictions, and they are not a plan or decision of the committee.Policy is not set on a preset track.

The Fed has been given two monetary policy goals: maximizing employment and stabilizing prices.We remain committed to supporting maximizing employment, bringing inflation sustainably back to our 2% target, and keeping long-term inflation expectations stable.Whether we can successfully achieve these goals is crucial to all Americans.We understand that our actions affect communities, families and businesses across the country.Everything we do is to serve our public mission and we at the Federal Reserve will do everything we can to achieve our goal of maximizing employment and price stability.Thanks.I look forward to our discussion.

Asked by reporter:

Thanks.I am Chris Regaber of the Associated Press.As you know, Fed Director Stephen Milan retained his position in the White House while joining the Fed Council.I believeThis is the first time in decades that the Fed Council has had an executive connection.Will this damage the Fed’s independence in daily politics?Relatedly, in this dynamic, how do you maintain the public’s view on the Fed’s political independence?Thanks.

Powell:

We do indeed welcome a new committee member today as usual, which remains united in pursuing our dual mission goals.We are firmly committed to safeguarding our independence,I really don’t have anything to share.

Asked by reporter:

You and other Fed officials have talked extensively about the impact of tariffs on inflation, although many companies seem to be digesting the cost of tariffs, which may be affecting the labor market and other parts of the economy, rather than inflation.Do you think this is a possible outcome, that tariffs are the reason we see a slowdown (especially in the labor market rather than inflation)?

Powell:

This is certainly possible.You know, we’ve started to see that rising commodity prices have been transmitted to higher inflation, in fact,Most, perhaps even all, of the rise in inflation this year is caused by rising commodity prices.These impacts are not very big at the moment, and we do expect the rest of this year and next year,These effects will continue to accumulate.And, you know, it may also have an impact on employment, but…I want to say, if you are exploring the reasons for the current situation of the job market,That’s more about the changes in immigration.So the supply of workers has obviously dropped significantly.The supply of workers has almost no growth, or even no.at the same time,The demand for workers has also dropped so dramatically that we see what I’ve called a curious balance.Usually when we say things are in equilibrium it sounds good, but in this case the balance is because both supply and demand are down sharply.Demand is falling a little more severe now because we are now seeing a slight increase in unemployment.

Asked by reporter:

Nick Timilaos of The Wall Street Journal.Chairman Powell,Is the economic situation and risk balance no longer a restrictive policy setting?

Powell:

I don’t think we can say that.What we can say is that we have maintained our policy at a restrictive level this year.People have different opinions, but I would say it is a clear level of limitation.The reason we can do this this year is because the labor market conditions are very stable, job creation is strong, and so on.I think if you go back to April and look at the revised employment creation data for May, June, July and August, I can’t say that anymore.This means that risks were previously evident in inflation.I would say they’re moving towards equality.Maybe they are not fully balanced.We don’t need to know this.But we do know that they have made meaningful movements in a more balanced direction, the risk between the two goals.This shows that we should move in the neutral direction.That’s what we do today.

Asked by reporter:

Under what circumstances is a reasonable rate cut of more than 25 basis points?How serious were you to consider this option at this week’s meeting?

Powell:

There is no widespread support for a 50 basis point cut today.I think we’ve done very large rate hikes and cuts over the past five years, and you usually do it when you feel that the policy has fallen out and need to adjust to the new position quickly.This is not what I feel right now.I think our policy has been done right so far this year.I think it is right for us to wait and see how tariffs, inflation and the labor market evolve.I think we are now responding to other evidence of a sharp decline in employment creation levels and weaker labor markets, and these risks may not be fully balanced, but are moving towards a balanced direction, so this requires policy change.

Asked by reporter:

Under what circumstances is a reasonable rate cut of more than 25 basis points?How serious were you to consider this option at this week’s meeting?

Powell:

There wasn’t widespread support at all for a 50 basis point cut today.I think we’ve done very large rate hikes and cuts over the past five years, and you usually do it when you feel that the policy has fallen out and need to adjust to the new position quickly.This is not what I feel right now.I think our policy has been done right so far this year.I think it is right for us to wait and see how tariffs, inflation and the labor market evolve.I think we are now responding to other evidence of a sharp decline in employment creation levels and weaker labor markets, and those risks may not be fully balanced, but are moving towards a balanced direction, so that requires policy changes.

Asked by reporter:

Colby Smith of The New York Times.Should we view today’s interest rate cuts as some kind of insurance measure taken by the Commission to prevent the potential weakening of the labor market, or should the Commission believe that the dynamics of the recession have been formed?I just wanted to figure out why the rate forecasts have turned to more rate cuts than three months ago, while the unemployment forecasts haven’t changed?

Powell:

Yes,I think you could think of this in a way as a risk management cut, because if you look at the Economic Forecast Overview (SEP), the growth forecast for this year and next year is actually slightly raised, and inflation and unemployment have not changed much.So what’s the difference now?The difference is that you see a completely different picture of labor market risks.You know, at the last meeting, we were seeing 150,000 jobs a month, and now we saw the revised data and new data, I don’t want to overemphasize non-farm job creation,But this is just one sign that the labor market is indeed cooling down, which tells us it is time to take this into account in our policies.

Asked by reporter:

The SEP once again showed that participants’ median forecasts believed that inflation at the end of the year would be higher than previous expectations.The SEP predicts that the Fed will not return to its 2% target until 2028.So I wonder, starting a series of rate cuts at this point, how do you describe its risk to price pressure?

Powell:

Yes, so I’ll see it like that.We fully understand and recognize that we need to continue to be fully committed to sustainable recovery of inflation to 2%, and we will.At the same time, we have to weigh the risks of two goals.I would say since April, really since April, the risks of higher and more persistent inflation have probably become a little less.thisPartly because the labor market has been weak and GDP growth has slowed.So I will just say that the risk there is less than people think.In terms of the labor market, we are seeing that the unemployment rate is still very low, and it is still a relatively low level, but we are seeing a lot of unemployment.We see downside risks.

Asked by reporter:

Michael McGee of Bloomberg.I’m a little confused about your explanation of the rate cut due to unemployment.If you think most of the happening in the employment sector is about immigration and your rate cuts don’t solve this problem, how do you think it’s more important than inflation?Inflation is almost a full percentage point higher than your target.

Powell:

Well, I mean what’s going on in the labour market is more about immigration than about tariffs.That’s the question I’m answering.So I wouldn’t say that everything that happens in the labor market is due to tariffs.I mean, you obviously have immigration slowdowns.You obviously have demand slowed, and now it may exceed supply slowdowns, and we know that because the unemployment rate has risen.So that’s the case.This is what I mean.

Asked by reporter:

I’ll ask.Since 2015, the SEP each year has predicted that you will reach your target in two years.And this year’s SEP says you will reach your goal in two years.2% seems out of reach.Does this indicate that the 2% goal is actually unattainable?If you never get to the goal and tell people you will do it, will this cause you any credibility issues?

Powell:

Well, I mean, you’re right.It does say we will reach 2% inflation by the end of 2028.But that’s how you make predictions.You write down an interest rate path that aims to create 2% inflation and maximize employment within the SEP timeframe.That’s all.You know, no one really knows what the economy will look like in three years.But the essence of this prediction is to write down a policy you think will return to the 2% target at least by the end.

Asked by reporter:

Thank you so much.Elizabeth Schultz of ABC News.Prices in many households, including groceries, are still rising, the latest inflation report shows.What will the Fed do if prices rise further?

Powell:

So our expectations, you can see that this year has been like this, inflation will rise this year, but basically because of the impact of tariffs on commodity prices.But these will prove to be one-time price increases, rather than creating an inflationary process.This is almost every prediction of our view.But we can’t just assume that this will happen, right?Our job is to make sure that this does happen and that we will do the job well.What we are now is that we are seeing inflation and we continue to expect it to rise, perhaps not as high as we expected a few months ago.Tariffs are transmitted to inflation more slowly and less.The labor market has been weak.Therefore, the possibility of a continuous outbreak of inflation has decreased.Therefore, we think it is time to acknowledge that the risk of another task has increased and we should move in a neutral direction.So what will we do?We will do what we need to do, but we have two tasks and we try to balance them.For a long time, our framework said that when our two goals conflict, it is a very unusual situation, how do we decide what to do?Because our tools can’t do two things at the same time.What we do is, we ask which one is further away from the goal and how long it is expected to take to reach it.So, then we think about these things, we see,As I mentioned, our policies have indeed been inclined toward inflation for a long time.Now we see that there is a clear downside risk in the labor market, so we are moving towards a more neutral policy direction.

Asked by reporter:

How worried are you about the slowdown in the job market for domestic families, especially young Americans who have difficulty finding a job?

Powell:

This is an interesting labor market, and obviously we think it is appropriate to lower interest rates to make policies more neutral, which is probably better for the labor market.You see those on the edge,For example, newly graduated college students, young people and minorities are finding it difficult to find a job.The overall job search success rate is very, very low.However, the layoff rate is also very low.So you are in a low-sack, low-recruitment environment, and it is worrying that if layoffs start to occur, the people who are laid off will not find many recruitment opportunities, which is one of the main concerns.This may soon translate into higher unemployment rates.In a healthier economy, healthier labor market, those people will have jobs.But now the hiring rate is very, very low.So over the past few months, this has become a growing concern.This is one of the reasons why we think it is appropriate to start shifting policy priorities to a more balanced position.

Asked by reporter:

Steve Lesman of CNBC.Mr. Chairman, you have used the word “recalibration” when you cut interest rates in the past.I wonder if you intentionally didn’t use it this time.In fact, when you say “policy is not set on a preset track”, do you mean the opposite of “recalibration”?Are we in a state of decision-making in meetings and data points?Are we back to neutral?Thanks.

Powell:

So I think we are in a situation where we make decisions in a row.We will focus on the data.You know, let me talk about SEP here.We often point this out.SEP is a collection of 19 individual predictions that show what they consider the most likely economic path at a specific point in time and, therefore, the most appropriate monetary policy path.As you know, we do not debate or try to agree on this.We just write them down and put them together.We sometimes discuss them.So we always say we don’t have a preset path, we are serious.The decisions we actually make will be based on the latest data when making the decision, changing outlooks and risk balance.So you’ll see that 10 of the 19 participants wrote down interest rate cuts twice or more for the rest of the year, while 9 wrote down interest rate cuts less, and in fact, in many cases, there were no more interest rate cuts.So, rather than looking at it that way, I encourage everyone to look at SEP from a probability perspective as usual.So there are different possible outcomes and possibilities, rather than this being certain, that will not happen.That’s what I want to say.

Asked by reporter:

Thank you for answering my question.Do the differences in the outlook heralds the uncertainty of policy in future meetings?Thanks.

Powell:

You know, this is a very unusual situation.Typically, inflation is low when the labor market is weak.And when the labor market is very strong, you need to be careful of inflation.So our current situation is,We have two-way risk, which means there is no risk-free path.(So we have a situation where we have two-sided risk, and that means there’s no risk-free path)So this is a pretty difficult situation for policy makers.I’m not surprised at all when you see that there are all kinds of opinions.It’s not entirely about having a different view of the economic path, in part.But it is also partly… about what is the right way to do it under the tension between the two goals.How do you weigh them?How much are you more worried about one than the other?So this is very natural.I think it would be surprising in such extremely unusual circumstances without a fairly broad view, and we do have it.But we got together, we talked, we had a good discussion, and then we decided what to do and acted on.But you’re right, the opinions are very different, and I think that in the current situation, it’s understandable and natural.

Asked by reporter:

Victoria Jeddah of Politico.You’ve talked a lot about the Fed’s independence and its importance over the years, but as the market questions about President Trump’s exact intentions about the Fed, what things would you point to what they should focus on to make sure the Fed is still making decisions based on economic prospects rather than political considerations?

Powell:

look,Working on the latest data, never taking into account any other factors, is deeply rooted in our culture.(it’s deeply in our culture to do our work based on the incoming data and never consider anything else. That’s just, everybody who’s at the Fed really feels strongly about that way.So, you know, you know through the way we talk about what we are doing, through the speeches people give, through the decisions we make.You’ll know we’ll still do that.We only do this.We simply do not construct or view these issues from the perspective of political outcomes.I think when you get to another part of Washington, everything is viewed through whether it helps or damages the perspective of this party, this politician, and that’s their framework.I think it’s hard for people to believe that this is not the way we think about problems at the Fed.We take a longer-term perspective.We try to do our best to serve the American people.So I think you will be able to judge that I believe we will never get to that point.I would say that we are doing our work exactly as usual, people are making their arguments, and we are having a very good discussion around these challenging issues.

Asked by reporter:

Do you think the court case surrounding Lisa Cook is related to the issue of independence?

Powell:

I think this is a court case and I should not comment on it.

Asked by reporter:

Thank you, Mr. Chairman.Edward Lawrence of Fox Business News.We have seen a preliminary benchmark correction downgraded by 911,000. The June correction is the first negative correction we have seen since December 2020.How can the Fed build important decisions about interest rates and the direction of interest rates on what you used to call “noisy”?

Powell:

Regarding the QCEW (Quarterly Employment and Wage Census), the corrections we have seen are almost exactly what we expect.Surprisingly, it is very close to expectations.The reason is that there has been almost a predictable overreport in the past few quarters.I think the Bureau of Labor Statistics does understand this and they are working to fix it.Of course, this has to do with low response rates, but it also has to do with the so-called “life and death model” because a large portion of employment creation happens around startups, how many companies go bankrupt and how many companies are founded.This is really hard.You can’t understand through investigation.You have to have a model to predict.This is very difficult, especially when the economy is undergoing huge changes.They have been working hard and making progress.But the data we get is still good enough to allow us to do our work.As for the problems we are currently facing in terms of data, the main thing is the low response rate.This happens everywhere, really.The response rate to surveys is now lower, both inside and outside the government.It’s no big secret, you know, we want higher response rates, and we need these to get less volatile data.And the way to get a higher response rate is to ensure that the organization that collects data has enough resources to drive higher response rates.This is not a complicated issue, but that’s what you need.This is not a mystery.That’s what you need.Edward, another thing I want to say is, in terms of employment creation,The first month’s response rate is quite low, or even lower.But by the second or third month, you are still collecting responses from the previous month.By then, the data became more reliable in the second month, and of course the third month.So it’s not that we can’t get the data, it’s just that we get it later.

Asked by reporter:

So for benchmark data, if this number is true, it means that 51% of the positions we think exist do not actually exist.This shows that the job market was weaker than expected at the beginning of the year.If you had this information at the time, would it change your opinion on where interest rates should be?Should interest rates be cut earlier?

Powell:

You know,We have to look forward, not backward.All I can tell you is, we see where we are now, we take the proper action, and we take that proper action today.

Asked by reporter:

Thank you, Howard Schneider of Reuters.As you mentioned just now, some edge indicators in the job market indicate that the decline has occurred.The black unemployment rate exceeded 7% in August.Work weeks have been shortened, college graduates have difficulty finding jobs, and youth unemployment has risen.Why do you think that a 0.25 percentage point rate cut can stop this now?

Powell:

Well, I haven’t said that I think 0.25 percentage points will have a huge impact on the economy, but you have to look at the whole interest rate path, right?The market has digested expectations.I mean, our market operates through expectations, right?So I think our policy path is really important.I think what’s important is… when we do see signs like that, we use our tools to support the labor market.I did mention this.You see the rise in the unemployment rate among minorities.You see young people, those who are more economically vulnerable and more susceptible to economic cycles.This is one of the reasons why the labor market is weakening marginally besides the overall lower non-farm employment creation.I also want to point out the labor force participation rate.The significant decline in labor force participation in the past year may be partly due to periodicity, not just the usual aging process.So we put all of this together and we see that the labor market is weakening, we don’t need it to be weaker, and we don’t want it to be like that.So we use our tool, which starts with a 25 basis point cut, but the market is also pricing an interest rate path.I am not acknowledging the market’s approach at all.I just said, it is not static.It’s just an action.

Asked by reporter:

As a follow-up to this…the current growth portfolio seems to be very focused on investment and consumer spending for high-income groups.Do you think this is an unsustainable combination for the future of the economy?

Powell:

I won’t say that.I mean, you’re right.These are two—We are gaining an unusually large amount of economic activity from artificial intelligence construction and corporate investment.I don’t know how long this will last.No one knows.In terms of spending, you see consumer spending data that is much higher than expected, which is likely to be biased towards high-income consumers.There is a lot of anecdotal evidence to suggest this.Still, it’s still a expense.So, I mean, I think the economy is moving forward.Economic growth will reach 1.5% or higher this year, perhaps a little better.As you can see, the forecast has been upwards.So, the labor market, the unemployment rate is very low, but, you know, there is a downside risk, but it is still a low unemployment rate.So, that’s how we see it.

Asked by reporter:

Hello Stephanie Ruhr of MSNBC.Treasury Secretary Scott Besent once said the Fed had problems with “deviation from mission” and “bloated institutions”.He now calls for an independent review.Will you support independent review, or are you open to any form of reform in any area of the Fed?

Powell:

I certainly would not comment on anything the minister or any other official said.So, as far as Fed reforms are concerned, you know, we just went through a long and I think it’s very successful process of updating our monetary policy framework.I would say that there is a lot of work behind the scenes in terms of the assets of the Fed system, the Fed system and the Council.Are they of the right size?We are actually doing 10% reductions in the entire Fed, including the Council and all Reserve Banks.After the cuts are over, the Fed will have basically the same number of employees as it was more than a decade ago.So, when we finish, we will have over a decade of zero job growth.And I think we might do more.So I think we are certainly open to constructive criticism and ways to improve the way we work.

Asked by reporter:

Not an independent review?

Powell:

Of course we are always willing to work hard to do better.

Asked by reporter:

Mr. Chairman, Neil Irving of Axios.Recently, there have been some debates about whether artificial intelligence has begun to affect the labor market, which are reflected in lower labor demand and increased productivity.Do you agree with this view?If this is true, how does this affect monetary policy setting?

Powell:

There is great uncertainty in this regard.I think my point, while a bit speculative, is widely accepted, that is, you do see some influence, but it is not the main driver.Special attention is paid to young people who have just graduated, yes, there may be some situations there.It may be companies or other institutions that have been hiring college graduates that can now use AI more than in the past.This may be part of the story.But the other part of the story is that wider employment creation has slowed down.The economy has slowed down.So this may be caused by a variety of factors.But yes, that could be a factor.It’s hard to say how big it is.

Asked by reporter:

Thank you, Mr. Chairman.What evidence do you see when tariffs appear in inflation?

Powell:

Well, you can look at the product, which is the broad product category.Commodity inflation was negative last year.If you go back 25 years, that is the typical situation, that commodity prices usually fall, even if the quality is adjusted.Of course, this is not the case during the epidemic.Commodity inflation has become very high, but we have basically returned to zero or slightly negative inflation.Now, I think commodity inflation in the past year is 1.2%, which doesn’t sound like a lot, but it’s a big change.So we think, I mean, analysts have different opinions, but we think it contributes about 0.3 or 0.4 percentage points to the current 2.9% core PCE inflation reading.So it contributes.What seems to be happening is, you know, the tariffs are mostly not paid by exporters.Most of this is paid by companies that are between exporters and consumers.So if you buy something and sell it to a retailer, or you use it to make a product, you may bear most of these costs and can’t be passed on to the consumer completely.That’s the case now.This seems to be what we see.All these middle companies and entities, they will tell you that they are completely planning to pass on these costs in the future, but they are not doing so now.For consumers, the transmission has always been very small.It is slower and smaller than we thought.But the evidence is very clear and there is some transmission.

Asked by reporter:

I also want to ask if you can share with us under what conditions you might consider leaving the Fed in May.

Powell:

I don’t have any new news about this to tell you today.(I have nothing new on that for you today.)

Asked by reporter:

Hello, Caterina Sariva of Bloomberg.I just wanted to follow up with one of your answers a few minutes ago.We often hear you talk about how you and your colleagues don’t think about politics.This won’t go into the conference room.But one of your new colleagues does come from this world, right, where everything is seen through a framework of politics and which party benefits.And that person is still employed by the White House.How do the market and the public interpret it, for example, some of his speeches, and some of the predictions we see today?I mean, the median forecast for this year has been moved because of the introduction of his forecast.I’m talking about the expected number of interest rate cuts this year.What do you have to say about…the market and the public that is trying to interpret what you said?

Powell:

There were 19 participants, 12 of whom voted in a rotational manner.So there is no voter, you knowThe only way to really change things is to be extremely persuasive.And in the context of our work, the only way to do this is to make very strong arguments based on data and one’s understanding of the economy.This is what really matters.And that’s how things work.I think that’s how this institution isIt is rooted in the DNA of this institution.This will not change.

Asked by reporter:

Then I want to ask a Gallup poll that shows that Americans now have more confidence in the president than they have in the Fed when it comes to doing the right thing for the economy.Why do you think this is?What is your response?What information do you have for the public?

Powell:

Our response is.We will do everything we can to use our tools to achieve the goals that Congress has given us, and we will not be distracted by anything.So I think that’s what we’re going to do.We just keep doing our work.

Asked by reporter:

Claire Jones of the Financial Times.Given the scope of opinions expressed before the meeting,I think there are much less disagreements today than many people expected.It’s nice to know what you think is the driver of such a strong consensus at the meeting, and on the other hand, explain why the dot map is so scattered among different people, from someone even expecting higher interest rates at the end of the year to five rate cuts.I mean, what kind of scope of view do you hear, on the one hand, why there is so much support for rate cuts today, and on the other hand, why are there such a big disagreement about what will happen next?

Powell:

So I think there is a pretty broad response, a broad assessment that the situation has changed about the labor market.Although we can and did say at our July meeting that the labor market is solid, we can point to 150,000 jobs and many other things per month.But I think the new data we get, not just non-farm employment data, but other data, suggests that there is indeed meaningful downside risk.I said at the time that there was a downside risk, but I think that downside risk has become a reality now and obviously there are more downside risks.So I think this is widely accepted.This means different things for different people.Some people, written down, almost everyone wrote down, supporting this rate cut, some supporting more rate cuts, and some not, as you can see from the dot map.That’s the situation.I mean, people have a lot of experience with it.I think that’s the case.I think that’s it, that’s it.I think you have some people taking the job very seriously and keep thinking, doing their jobs, discussing with our colleagues.We talk about this endlessly between us, and then we have a meeting and put everything on the table, and that’s what you get.you’re right.There are all kinds of perspectives in the dot map, and I think, as I said, it is no surprise, given the rather unusual, historically unusual nature of the challenges we face.But let’s remember that the unemployment rate is 4.3%.The economic growth rate is 1.5%.So it’s not a bad economy or something like that.We’ve seen more challenging economic times.But from a policy perspective, from a goal we are trying to accomplish, it is challenging to know what to do.As I mentioned before, there is no risk-free path now.What to do is not very obvious.So we have to pay close attention to inflation.At the same time, we cannot ignore and must pay close attention to maximizing employment.This is our two equal goals, and you will see a range of perspectives on what to do.Nevertheless, we came together at the conference today and acted with a high degree of solidarity.

Asked by reporter:

Thank you, Archie Hall of The Economist.You mentioned earlier that job creation is lower than your guess about its “break-even” rate.I’m curious to know more about it. Where do you think the “break-even” rate is?

Powell:

You know, there are many different calculation methods, none of which are perfect.But you know, it has obviously dropped significantly.You can say it is between zero and 50,000, you may be right or wrong.I mean, there are a lot of different ways.So no matter where it was a few months ago, 150,000, 200,000, it has dropped a lot, and it is noticeably because there are very few people joining the labor force.The labor force has really not grown much now, and this is the main source of labor supply in the past two or three years.So we don’t have that now.Our demand is also much lower.You know, interestingly, supply and demand have really dropped together so far, except now we do have inflation, sorry, it’s the unemployment rate that has risen, just a little bit higher than it’s in the year.4.3% is still a low level, but…you know, I think supply and demand are down so rapidly, it certainly caught everyone’s attention.

Asked by reporter:

You mentioned a lot about downside risks in employment, but it’s striking that the third quarter activity and output indicators we have seem to be quite strong.The Atlanta Fed’s GDPNow model is very strong, and you also mentioned strong PCE data.How do you coordinate these things?If those activity indicators are correct, is there a possibility of upside risk in the labor market?

Powell:

Well, that’s great.We are happy to see it happen.So I don’t know if you’re seeing a big contradiction there, but it’s gratifying to see economic activity remain stable.This comes largely from consumption.It looks like consumption is stronger than expected, and that’s the data we got earlier this week, I think so.Moreover, we have a rather narrow industry that is generating a lot of economic activity, namely artificial intelligence construction and commercial investment.So we focus on all of this, and I want to say we did go up.Between June and September SEPs, the median growth this year has actually been raised, while inflation and the labor market have not changed much.What really became the focus of today’s decision is the labor market risks we see.

Asked by reporter:

Hello, Nicole Goodkind of Barron’s.Thank you for accepting my question.Given the cumulative impact of high interest rates on the real estate industry, I wonder how worried you are that current interest rate levels are exacerbating housing affordability issues and may hinder the formation of households and wealth accumulation of a portion of the population.

Powell:

You know, housing is an interest rate sensitive activity, so it is at the heart of monetary policy.When the pandemic hit and we lowered interest rates to zero, real estate companies were very grateful and they really said that was the only thing that allowed them to continue, that we cut rates so aggressively and provide things like credit and they were able to finance because we did that.On the other hand, when inflation gets higher and we raise interest rates, you’re right, it really puts a burden on the real estate industry.So the interest rates have dropped a little bit, and as this happens, we don’t set mortgage rates, but our policy rate changes do affect mortgage rates, and that’s happening, which of course increases demand and lowering the borrowing rate of the builder will help, you know, help builders supply, so some of them should happen.I think most analysts think that interest rates need to change considerably to have a big impact on the housing industry, and, you know, the other thing is that by maximizing employment and price stability, it’s a strong economy and a good economy for housing.Finally, I want to say that there is a deeper problem here, not a cyclical problem that the Federal Reserve can solve, that is, a housing shortage nationwide, or in many places across the country, there is not enough housing for people.And, you know, all the areas around metropolitan areas like Washington are built very densely.So you have to build further and further.That’s the situation.

Asked by reporter:

Just a quick follow-up question, and in the last SEP press conference, you seemed to suggest a lack of confidence in their predictions.I wonder if you still feel that way now.

Powell:

You know, prediction is very difficult, even during periods of calm.As I mentioned before, predictors are a group of humble people, and there is a lot to be humble.So I think it is a particularly challenging time, more uncertain than usual.So I don’t know any predictor anywhere, really.Ask any forecaster if they now have great confidence in their predictions.I think they will honestly say no.

Asked by reporter:

Thank you, Chairman Powell.Jennifer Seanberg of Yahoo Finance.If you are cutting interest rates, why continue to reduce your balance sheet and then pause your balance sheet?

Powell:

Well, I think we, you know, are very limited in scale now to shrink the balance sheet.As you know, with regard to the balance sheet, we are still in a state of ample reserves, and we said we will stop at a level slightly above ample reserves.That’s what we are now.And we,You know, we are approaching that level.We are monitoring very carefully.We do not think this has any significant macroeconomic impact.These are pretty small numbers moving inside a huge economy.You know, the reduction level is not very large.So I won’t attribute the macroeconomic consequences to this.

Asked by reporter:

In his recent confirmation hearing, Stephen Milan mentioned that the Fed actually has three tasks assigned by Congress, not only employment and stable prices, but also moderate long-term interest rates.So what does Congress mean by “moderate long-term interest rates”?How should we understand when we see changes in the yield on 10-year Treasury bonds?How do you consider this part of the task when policy choices like rate cuts or balance sheets affect the long end of the yield curve?

Powell:

We have always believed that this is a dual task, maximizing employment and price stability, which has been like this for a long time, because we believe that modest long-term interest rates are the result of stable inflation, low and stable inflation, and maximizing employment.So for a long time,We do not see it as the third task that requires independent action.That’s the situation.And, in my case, we have not considered it in some different way.

Asked by reporter:

Thank you, Chairman Powell.Matt Egan of CNN.We recently learned that the average FICO credit score fell by two points this year, the largest decline since the Great Recession in 2009, with high default rates for auto loans, personal loans, and credit cards.How worried are you about the health of your consumer’s financials, if any?Do you expect the rate cut today to help?

Powell:

So, you know, we realize that.I think the default rate has been rising and we are really paying attention.They haven’t reached a level yet, and I don’t think they’re at a level that’s generally very worrying, but that’s something we’re focusing on.You know, lower interest rates should support economic activity.I don’t know if a rate cut will have a visible impact on this, but over time, you know, a strong economy with a strong labor market is what we are pursuing, and there are stable prices, so that should help.

Asked by reporter:

First, the rate cut occurred during a period when the stock market was at or near an all-time high and some valuation indicators were at a historical high.Is there a risk that interest rate cuts may overheat financial markets and may fuel bubbles?

Powell:

We focus closely on our goals, our goal is to maximize employment and price stability.So the actions we take are all focused on these goals.So we did what we did today.In addition, we monitor financial stability very, very carefully.And, you know, I would say it’s a mixed picture, but the family is in good condition.The bank is in good condition.Overall, the family is still in good condition overall.I know people at the low end of the income spectrum are clearly under pressure.But from the perspective of financial stability, we monitor the entire picture.We do not believe that there is a right or wrong future level of asset prices.We do not think there is a right or wrong price level of a specific financial asset, but we monitor the entire picture and really look for structural loopholes. I want to say those are not high now.

Asked by reporter:

Hello, Chairman Powell.Jan Yang of M&I Market News.I want to ask questions about inflation expectations.You said the Fed cannot take the stability of inflation expectations for granted.You mentioned that they have risen in the short term.I wonder if you can talk about this.Then there’s the long term, I wonder, do you see evidence that debates about Fed independence and growing deficits are putting pressure on inflation expectations?

Powell:

As you said, short-term inflation expectations tend to react to near-term inflation.So if inflation rises, inflation expectations predict it will take a little while to fall back.Unfortunately, throughout this period, long-term inflation expectations, whether it is break-even inflation in the market or almost all long-term surveys, the University of Michigan survey has been somewhat exceptionally lately, and has been very stable at a level consistent with long-term 2% inflation.So we don’t take this for granted.We actually assume that our actions have a practical impact on this, and we need to constantly show and mention and discuss our commitment to 2% inflation.So you’ll hear us do it.But as I mentioned, this is a difficult situation because the risks we face affect both the labor market and inflation.These are our two goals.So we have to balance.This is indeed what we are working on.Part of your question is about independence.I don’t see market participants, I don’t see them now taking this as a factor when setting interest rates.