Author: Andrew Kang, co-founder of Mechanism Capital Source: X, @Rewkang Translation: Shan Oppa, Bitchain Vision

Bitcoin ETFs offer many new buyers the opportunity to include Bitcoin in their portfolios.In contrast, the impact of Ethereum ETF is still unclear.

When BlackRock filed a Bitcoin ETF application, I was bullish when the Bitcoin price was $25,000.Since then, Bitcoin price has risen 2.6 times, while Ethereum has risen 2.1 times.Starting from the bottom of the cycle, both Bitcoin and Ethereum have a return of 4.0 times.So, how much upside space can Ethereum ETF bring?I think,If Ethereum cannot find a powerful way to improve economic benefits, it has little room for upward trend.

Analysis of capital flows

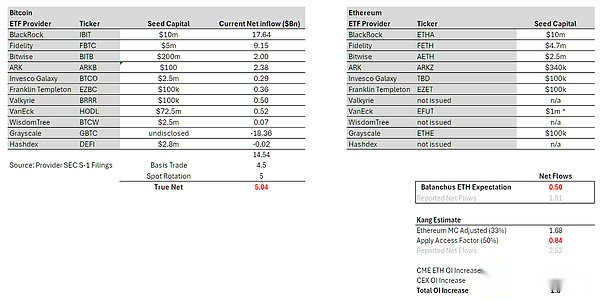

Overall, Bitcoin ETFs have accumulated $50 billion in asset management, which is an impressive number.However, if existing GBTC asset management scale and rotation are excluded, net inflows since launch are only $14.5 billion.These are not real inflows, as many neutral capital flows need to be considered, such as basis trading (selling futures, buying spot ETFs) and spot rotations.Based on CME data and analysis of ETF holders, I estimate that approximately $4.5 billion of net inflows can be attributed to basis trading.ETF experts believe that large holders such as BlockOne also convert spot Bitcoin into ETFs, which is about $5 billion.After deducting these traffic, we came up with a real net purchase of Bitcoin ETFs of $5 billion.

From here we can simply calculate the situation of Ethereum.@EricBalchunas estimates that Ethereum inflows may be 10% of Bitcoin.This means that the real net purchase in 6 months is $500 million, with the reported net inflow of $1.5 billion.Although Balchunas’s estimate of the odds of approval is incorrect, I think his lack of interest and pessimism in Ethereum ETFs are informative, reflecting the widespread interest of traditional finance in it.

Personal prediction

My benchmark is 15%.Starting with Bitcoin’s $5 billion real net buy, adjusting Ethereum’s market cap to 33% of Bitcoin and a 0.5 access factor*, we came up with a real net buy of $840 million and a reported net inflow of $25.2$100 million.There is a reasonable view that ETHE has a lower premium compared to GBTC, so I set the optimistic scenario at $1.5 billion true net buy and $4.5 billion reported net inflow.That’s about 30% of Bitcoin inflows.

In any case, true net buying is much lower than the derivatives flows before the ETF, which totaled $2.8 billion and excluded spot advance layout.This means that the impact of ETFs has been fully reflected by the price.

*The access factor adjusts the traffic brought by the ETF, which is significantly beneficial to more Bitcoin than Ethereum, considering the different holder bases of the two.For example, Bitcoin is a macro asset that is more attractive to institutions with access issues, such as macro funds, pensions, endowments, sovereign wealth funds, etc.Ethereum is more like a technology asset, more attractive to venture capital, crypto funds, tech experts, retail investors, etc., who do not have many restrictions on accessing cryptocurrencies.The 50% ratio is obtained by comparing the ratio of ETH to BTC of the CME open contract to market capitalization ratio.

Looking at the CME data, Ethereum has significantly fewer open contracts than it was before the launch of Bitcoin ETFs.Open contracts represent 0.30% of supply, while Bitcoin is 0.6%.At first I thought it was a “early” sign, but it could also be said to reflect a lack of interest in smart traditional financial funds in Ethereum ETFs.Traders in the market get good deals on Bitcoin, they usually have good information, and if they don’t repeat Ethereum transactions, there must be a good reason that could mean weak liquid intelligence.

How did $5 billion push Bitcoin from $40,000 to $65,000?

The short answer is, it doesn’t.There are many other buyers in the spot market.Bitcoin has become a globally recognized key investment asset with many structural accumulators, such as Michael Saylor, Tether, family offices, high net worth individuals, etc.Ethereum also has some structural accumulators, but I think its number is much lower than Bitcoin.

Remember that Bitcoin has reached a market capitalization of $69,000/$1.2 trillion before the ETF exists.Market participants/institutions have a large amount of spot cryptocurrencies.Coinbase hosted $193 billion, with $100 billion of that coming from its institutional plans.In 2021, Bitgo reported $60 billion hosting and Binance hosted more than $100 billion.Six months after the launch of the ETF, it hosted 4% of the total Bitcoin supply, which is important, but is only part of the demand equation.

Between MSTR and Tether, you already have billions of dollars in additional buys, but not only that, there are low-proportion ratios before the ETF launches.The view that ETFs were seen as selling news events/market tops was very popular during this time.Therefore, short-term to medium-term momentum selling requires repurchase (influence of 2 times the flow).In addition, once ETF inflows show significant impact, short positions also need to repurchase.Open positions actually dropped before launch – which was surprising.

The positioning of Ethereum ETFs is very different.Ethereum was 4 times the price before launch, while Bitcoin was 2.75 times the price.Cryptocurrency exchanges’ open interest increased by $2.1 billion, bringing it to an all-time high.The market is (semi) effective.Many cryptocurrency participants have seen the success of Bitcoin ETFs, expecting Ethereum to get the same results and make arrangements based on them.

I personally think that the expectations of cryptocurrency participants are overvalued, which is out of touch with the true preferences of traditional financial allocators.Those who are deeply involved in the crypto field have a relatively high sense of identity and willingness to buy Ethereum.However, in fact,For many large groups of non-cryptocurrency native capital, Ethereum has much lower recognition as a key portfolio allocation.

The prospects of Ethereum

One of the most common reasons to market Ethereum to traditional finance is to regard it as a “tech asset.”Global computers, Web3 application stores, decentralized financial settlement layer, etc.This is a good selling point, and I have believed it in the previous few cycles.But when you look at the actual numbers, it’s hard to convince.

In the last cycle, you could point out the rate of expense growth and point out that DeFi and NFTs will generate more expenses, cash flow, etc., making it a tech investment like tech stocks.But in this cycle, the quantification of expenses is counterproductive.Most charts show growth is flat or negative.Ethereum is a cash machine, but how can analysts explain this price to family offices or macro fund bosses under 30-day annualized revenue, 300 times price-to-sales ratio, and negative earnings/price-earnings ratio after inflation?

I even expect the “fake traffic” (neutral capital flow) to be less for the previous few weeks, for two reasons.First, approval was a surprise, with issuers having less time to market to large holders to convert their Ethereum into ETF form.Second, holders are less attractive in switching because they need to give up the benefits they get from pledging or farming or using Ethereum as collateral in DeFi.But please note that the pledge rate is only 25%.

Does this mean Ethereum will be reset to zero?Of course not, at a certain price, it will be considered a valuable asset.When Bitcoin rises in the future, it will be driven to a certain extent.Before the ETF launch, I expect Ethereum to trade between $3,000 and $3,800.After the ETF was launched, my expectations were $2,400 to $3,000.However, if Bitcoin rises to $100,000 in the end of 2024/First quarter of 2025, this could drive Ethereum to an all-time high, but the Ethereum/Bitcoin ratio will be lower.There are still many developments to look forward to in the long run, and you have to believe that Blackrock/Fink is doing a lot of work to build some financial tracks on the blockchain and tokenize more assets.How much value this will bring to Ethereum and on what timeline it is still uncertain.

I expect the Ethereum/Bitcoin ratio to continue to decline in the next year, ranging from 0.035 to 0.06.Despite the small sample size, we are seeing Ethereum/Bitcoin hit lower highs in each cycle, so this shouldn’t be surprising.