Author:0xcoconutt

Preface

Did you know?Less than 5% of neobanks are profitable?

The new banks have an attractive pitch: fully digital banking services, lower fees and a better user experience.However, it turns out that theseThe economics of digital banking are fundamentally weak.

This article will delve into why many traditional newTypeThe bank’s income mainly depends onTypeBank income will also fall.

1. Overreliance on interchange fees

Neobanks rely primarily on transaction fees, a small fee charged by banks each time a user swipes a debit card.

This approach only works when scale is high, profit margins are high, and consumption is high.However, in practical applications, most of the time this model has poor economic benefits and is very fragile.

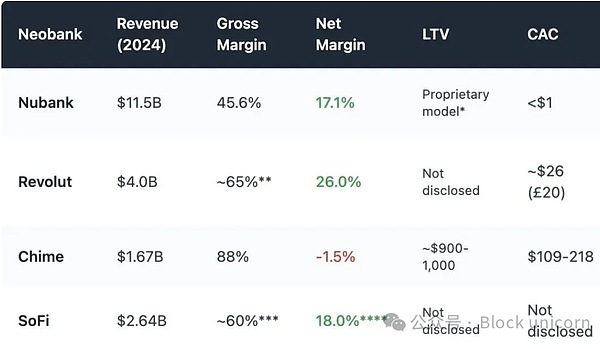

Chime is a US-based digital bank that does not have a banking license itself and can only rely on partner banks to hold deposits and issue bank cards, which is very similar to the operation model of cryptocurrency digital banks.Its business model is entirely focused on bank card transactions.It is expected that by 2024, approximately 80% of its total revenue will come from transaction fees.

However, regulators in many regions have capped interchange rates:

-

EU: 0.2% per transaction

-

United States (Durbin Amendment): Approximately $0.21 per swipe + 0.05% fee

-

Chime works with smaller banks and charges up to about $0.44 per swipe.

But this legal arbitrage opportunity is under pressure, and profit margins are already narrow for new banks that rely on transaction fees as a sustainable business model.

In addition, transaction fee income is also highly sensitive to consumer spending cycles.During an economic downturn, if people spend less with their cards, new banks’ revenue will also fall.

2. Idle capital: no lending, no interest income

The core of banking business income is interest income from lending, not interest income from payment.

Traditional banks convert deposits into loans, earning interest on mortgages, lines of credit, and business financing.

Even those new banks with banking licenses have mostly failed to establish this core functionality.

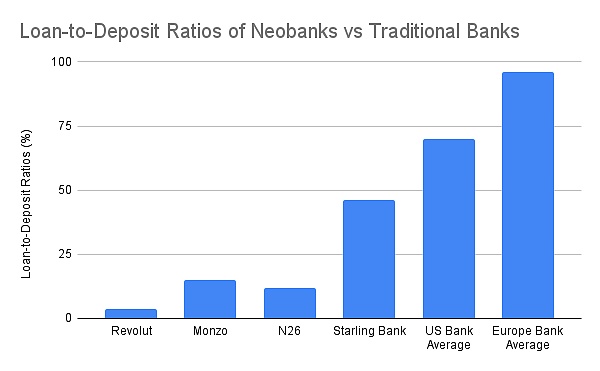

traditional bank60% to 65% of revenue comes from net interest income, and the loan-to-deposit ratio is 55% to 65%, with global averages even higher.However, most neobanks have underperformed in this major revenue stream, with only Starling Bank standing out with its acquired mortgage portfolio.

Crypto neobanks using a self-custody model cannot earn interest income from deposits.They cannot use user funds to generate revenue.At best, they forward deposits to DeFi protocols like Aave or Lido and take a small percentage of the proceeds as commission.However, these integrations lack an underwriting mechanism, no real control, and have their own risks, such as protocol hacking, stablecoin de-anchoring, etc.

In the fintech and cryptocurrency models, the same paradox keeps recurring: deposits accumulate but cannot be liquidated.

In essence, many neobanks, including cryptocurrency neobanks, are nothing more than expensive deposit storage units.

3. High customer acquisition costs and maintenance costs

Unlike traditional banks that rely on historical accumulation or organic growth of branch networks, new banks must win every customer through marketing and referrals in a highly competitive digital market.This results in high customer acquisition costs (CAC), severely squeezing their profit margins.

Due to the high registration threshold and the need for user education, the customer acquisition cost of cryptocurrency new banks will only be higher.Not to mention, most crypto neobanks employ high annualized yields and token incentives to entice users to deposit within the app.This amounts to deferred debt that the company needs to repay and significantly increases customer acquisition costs.

Cryptocurrency neobanks also have a worse cost-to-income ratio than traditional neobanks:

-

Stablecoin-based payment methods compress foreign exchange and transaction fees, triggering a vicious cycle of competing to drive down prices amid increasingly fierce competition.

-

Even with a self-hosted model, regulatory obligations include know-your-customer (KYC), redemption controls, and card program compliance.If card purchases are found to be fraudulent, refunds and penalties will be borne by the cryptocurrency neobank.They may even be at risk of being suspended from services by centralized card issuers.

-

The majority of users are small retail users (deposits less than $1,000), while after-sales, fraud, and infrastructure costs remain the same.

4. Reinventing the model: winning with embedded DeFi

Crypto neobanks cannot succeed by imitating Chime or Monzo because their business models have very different roots given their self-custodial nature.I don’t think cryptocurrency neobanks have any advantages over traditional neobanks, but cryptocurrencies can help neobanks increase profitability through embedded DeFi.

1. Trading activities as the main source of income

Transaction revenue has become an effective way for traditional new banks and crypto wallets to obtain high-margin revenue.

-

Revolut wealth division (including cryptocurrencies, 2024): £506m (16.3% of total revenue), up 298% year-on-year, driven primarily by customer speculation in cryptocurrencies rather than traditional banking services.

-

Phantom Wallet (2025 forecast): $79 million in wallet transaction volume

Embedded trading capabilities are considered industry standard.Applications need to provide rich asset types, trading pairs, MEV protection, fast execution and other functions to stand out and ensure that users get the best trading experience.

2. Structured income and on-chain wealth products

Rather than lending directly, neobanks will package complex DeFi products into wealth products that are easy for retail users to understand and invest in.

-

Self-issued stablecoins earn income from government bonds by guiding users to exchange them for new bank stablecoins.

-

Selected Yield Vaults and Retail Savings Agreements

-

On-chain ETF/Real World Assets (RWA)

-

insurance

I haven’t seen many Western emerging banks able to replicate the success of Alipay’s wealth product portfolio.

Screenshot provided by Alipay wealth product

Crypto neobanks have the advantage of offering a broad range of wealth management products that simplify DeFi and make high-yield financial products more accessible to a wider audience.

Embedded DeFi can help enrich neobanks’ wealth management product portfolios.

Conclusion: Don’t build banks, build decentralized finance (DeFi) tracks

Profit margins for neobanks have always been thin.Even if new cryptocurrency banks have DeFi-native tools, they face more severe challenges: lower stablecoin payment fees, higher compliance costs, stricter customer admission processes, and more intense competition once traditional new banks move into the cryptocurrency field.

As Revolut and Nubank begin to offer stablecoins, cryptocurrency trading, and on-chain yields on top of existing infrastructure, new crypto-first banks will struggle to compete for user mindshare.

The winning opportunity lies not in building another nascent bank, but in providing rails: yield routers, stablecoin FX layers, DeFi wrappers or curators that can plug into existing bank distribution networks.It will be difficult to compete with Shinsei banks that have already accumulated a large user base, but we should strive to supplement and increase their profitability with cryptocurrencies.

The way to win is not to build a new bank, but to provide supporting facilities: revenue routing, stablecoin FX trading layer, DeFi wrapper or curation platform that interfaces with existing bank distribution channels.It will be difficult to compete with neobanks that have already amassed large user bases, but we should strive to use cryptocurrencies to supplement and enhance their profitability.