1.introduction

Why choose BTC-LST?

With the birth of Babylon, it added additional benefits to BTC by providing a security service called timestamps.This restaking service protects protocols built on Babylon by increasing the cost of attacks, and makes staking of BTC possible through a time lock mechanism.

Although there is no actual pledge reward in the first phase, points are given, the potential of BTC income has inspired a wave of BTC liquidity re-staked tokens (BTC-LST), such as Lombard, babypie, FBTC and SolvBTC, etc..

Compared with packaged BTC that acts as native BTC cross-chain representations, BTC LST uses the Babylon protocol to introduce a profitable cross-chain BTC representation.

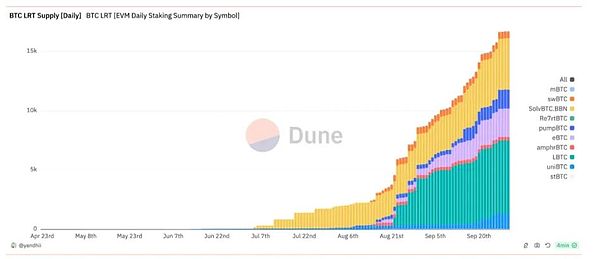

As of this writing, the BTC LST market has reached $1.07 billion (excluding the 9BWBTC assets on Ethereum).The market is dominated by SolvBTC and Lombard, with no sign of slowing growth.

Source: @yandhii , dune dashboard

On the other hand, many DeFi or restaking platforms on Ethereum (such as Symbiotic, Karak, etc.) have seen opportunities brought by the influx of earnings BTC assets and have begun to integrate these assets into their agreements to guide the overallLock value (TVL) and trading volume.

ThisThe phenomenon is extremely optimistic, because the inflow of assets can strengthen Ethereum’s position as the center of liquidity in the DeFi field and continue to create flows of economic activity.

As BTC is more accepted by institutions and the public, it can be observed from recent news such as BTC ETF and cbBTC, not to mention the dominance of BTC (about 58%), BTC adoption is expected to continue to grow until new innovations emerge.Therefore, it is necessary to have a clear understanding of the current BTC LST-fi pattern.

Source: Henry

This study aims to comprehensively sort out existing BTC-LRT, BTC wrappers, and DeFi protocols that follow the emerging trend of BTC insurgency on Ethereum to facilitate easier navigation in the future.

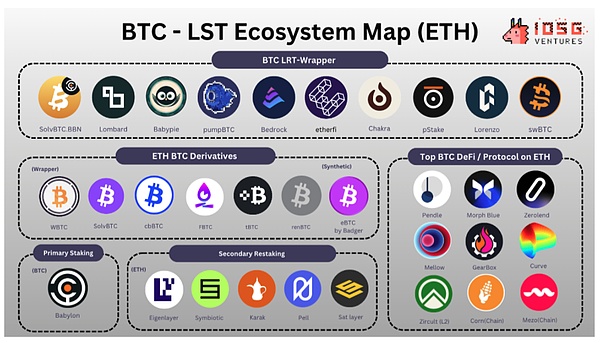

2.BTC-LST Ecology

Source: IOSG

Bitcoin LST Wrapper is a “new member” of this cycle, designed to unlock liquidity of tokens pledged in Babylon, the BTC re-staking protocol.

BTC flow packages usually come in three forms:

-

One is a one-way cross-chain wrapper, supported by BTC pledged by Babylon in the BTC main network at a 1:1 ratio.”Revenue-generating tokens” minted on ETH are used as receipts for pledging BTC.

Examples: LBTC, pumpBTC, babypie’s mBTC, etc.

-

Use LBTC or ordinary BTC (such as WBTC) as collateral and re-polize assets to wrappers on re-private platforms such as Symbiotic and Karak.On Ethereum, use LBTC or ordinary BTC (WBTC) as collateral and then re-private these assets to re-staking platforms such as Symbiotic and Karak.

Example: Etherfi’s eBTC, Swell’s swBTC

-

“Reverse mode”, using WBTC as collateral on ETH, and passing staking certificates to Bitgo through oracles, allowing BTC unlocked from Bitgo to be pledged into Babylon to generate profits.”Reverse Mode” users can use WBTC as collateral to unlock native BTC on the mainnet and pledge it to the Babylon platform.They pass the staking proof to Bitgo through oracles, which unlocks BTC and uses it to staking on Babylon for profit.

Example: Bedrock

While the first two types focus on bridging or unlocking more BTC assets from the BTC mainnet to the ETH ecosystem, the latter type extracts WBTC assets from ETH and pledges the assets “reversely” to the Babylon protocol.Architecturally speaking, one thing these wrappers have in common is that BTC is stored in a hosting party on the BTC mainnet (such as Cobo or Copper) to protect its assets, which is the cheapest and most convenient way.To show the entire BTC LST/LRT pattern more clearly, here is a summary of how some BTC LST/LRT works:

Source: Henry

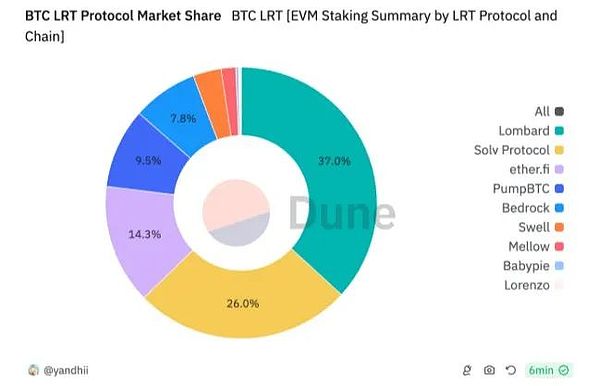

BTC LST market size

As of this writing, LBTC dominated with a market share of 37%, followed by 26% of solvBTC and 9.5% of pumpBTC.79.6% of BTC LSTs are on the Ethereum main network, while the remaining 21.4% are scattered on BNB chain, Arbitrum, Avalanche and other networks.

The two major players in the BTC LST market have taken different approaches.Lombard focuses on Ethereum, while SolvBTC adopts a multi-chain approach and opens up various networks including BNB, ARB, etc.

Source: @yandhii , dune dashboard

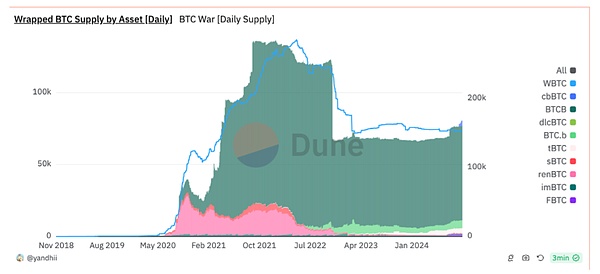

2.1 ETH BTC derivatives (Wrapper and synthetics)

ETH BTC derivatives are encapsulated BTCs that are bridged from the BTC main network to the ETH network, usually implemented through the custodian.These Wrappers are not competitors to BTC LST, but are used as key factors driving LST growth.

Unlike BTC LST, these derivatives are not pledged into the Babylon agreement and do not generate income inherently.Instead, they serve as a common manifestation of BTC on the ETH blockchain.Although not essentially profit-generating assets, ETH BTC derivatives have become a key component of today’s ETH DeFi landscape.

Most DeFi and restake platforms accept WBTC because:

-

They have been tested in practice

-

Occupy high market dominance in the 2024 cycle

As of this writing, bitgo’s WBTC has bridged from BTC to ETH’s assets of more than $9 billion since 2018.Of this, 21.5% (about US$1.9 billion) were deposited into Aave for loans, accounting for about 20% of Aave’s total assets in ETH.

Most DeFi and restake platforms accept WBTC because:

-

They have been tested in practice

-

It has maintained a high market dominance for many years

Source: @yandhii , dune dashboard

On the other hand, the new generation of Wrapper (E.g., FBTC) also accumulated more than $152 million on ETH, with monthly growth of 38% according to DeFillama.Another packager, SolvBTC, also attracted over $800 million in TVL on BSC and BTC L2 such as Merlin.

These figures not only demonstrate the importance of BTC assets in the ETH ecosystem, but also highlight the huge potential of ETH DeFi to capitalize on this opportunity.

As mentioned above, the main problem with WBTC is trust in the custodian.

Recently, there has been growing concerns about the WBTC relationship with Justin Sun, leading Sky (former Maker) to consider removing the WBTC variant from their vault.BA Lab outlines the main concerns, mainly around the argument that Justin Sun may have a significant impact or control over the joint ventures that manage WBTC.However, Justin Sun himself claims that he has no control over WBTC or its assets.This transfer should also be seen as a risk to WBTC.

2.2BTC re-pled

BTC re-private refers to assets related to BTC on ETH (in the form of encapsulated BTC or BTC LST) that have been re-private to generate income.

The following table shows each asset accepted on the staking platform and its respective TVL:

Source: Henry

Overall, about $150 million of BTC is being restaked on ETH, most of which belong to Symbiotic and some are deposited into SatLayer.Symbiotic alone holds $124 million worth of BTC products, including WBTC and tBTC, as well as a pledged BTC LST worth $10 million.Karak’s BTC assets are only about $100,000.Together, these BTC assets contributed 7% to Symbiotic’s TVL.

On the other hand, Pell Network has successfully attracted a large number of BTC LSTs to be restaked through various BTC layer 2 solutions such as Bitlayer and B2network.These assets will be used to provide shared security services and generate revenue, similar to the model adopted by Babylon Finance and Eigenlayer.

While BTC LST has already earned the first layer of income from Babylon, some protocols (such as EtherFi) leverage BTC-LST by re-staking the LST to other re-staking platforms (such as Eigenlayer, Symbiotic, and Karak) to generate the second layer of income.

Although this strategy allows stakeholders to enjoy leveraged returns and maximize capital efficiency of a single asset, they also face the same risk as ETH LST, i.e., being cut by multiple platforms at the same time (Babylon, Symbiotic).

Anti-Slashing policies can prevent some degree of cuts on ETH, but further information about Babylon is not clear.

2.2.1 BTC-DeFi

There is no doubt that DeFi has been one of the most important areas that drive blockchain economic activity.As the $9.5 billion BTC asset market on ETH grows, DeFi on ETH can benefit from the stability, institutional recognition and potential benefits provided by BTC.

In general, in addition to exchange, BTC/BTC-LST-related DeFi can be divided into two main areas:

-

Currency Market & Interest Rate Swap: Morph blue, Aave, Pendle, Zerolend, Curve

-

BTC staking/points strategy: Corn, Meso, Gearbox, Mellow

Source: IOSG

2.2.2 Money Market

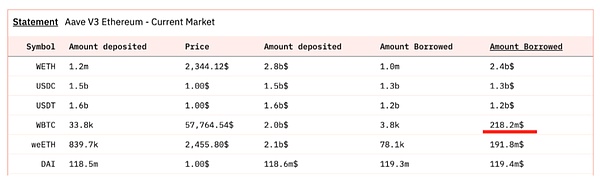

BTC, as the most “safe” asset, is commonly used as collateral in the ETH DeFi landscape.Aave is the oldest and most prestigious money market with over $2 billion in WBTC deposits, but only $218 million in borrowings, which is relatively utilizing relative to stablecoins (86.7%) or WETH (85%).Low (7.69%).

Source: @KARTOD, Dune dashboard

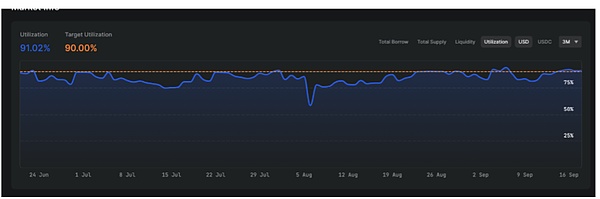

On the other hand, Morpho Blue achieves higher utilization rates despite its small deposit base (20% of Aave).The most popular market on Morpho Blue is WBTC/USDC, which has a utilization rate of up to 90%.

Source: WBTC/USDC Vault, Morphblue

So far, Aave and Morph only accept WBTC.To stand out in the highly competitive lending market, zeroland is the first market to target BTC LST tokens and support PT-eBTC.To date, they have $17 million worth of eBTC supply, with about $3.28 million being loaned out with a utilization rate of 20%.

In addition, Curve is not only a safe haven for stablecoin exchange, but also a popular destination for BTC-related assets to store assets.On Curve, BTC vendors can do two things: First, they can provide liquidity to the three pools.Second, they can borrow crvUSD using tBTC and WBTC as collateral.

As of this writing, approximately $50 million worth of BTC assets have been deposited for borrowing crvUSD.On the other hand, among the available pools, the tBTC-WBTC pool stands out with $25 million in assets and $2.24 million in daily trading volume.Unfortunately, although BTC-related assets are active on Curve, $CRV incentives have not been provided to attract users.

2.2.3 Interest Rate Swap (IRS) Exchange

In addition to the money market, Pendle offers interest rate swap (IRS) products, which are also one of the most popular places for BTC LST DeFi.

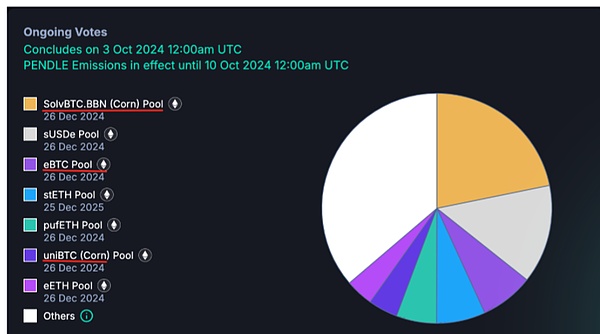

Pendle uses the future gains of BTC LST and speculation on points to create multiple dedicated markets: PT/YT for SolvBTC.BBN, LBTC and eBTC, etc.These markets attracted more than $136 million in total, up 150% month-on-month driven by points and incentives for agriculture.

A new round of voting incentives also marks an increasing interest in BTC LRT.For example, SolvVBTC in Corn was selected to attract the most Emission from Pendle.Therefore, the supply of BTC LRT assets is expected to continue to grow in the near future, taking into account emission incentives.

Source: Pendle Dashboard

2.2.4 TVL Bootstrapping Vault / Points Strategy

While Money Market and IRS products generate additional benefits for BTC assets based on BTC demand and supply on the ETH mainnet, TVL directs the vault to prioritize the use of BTC to boost TVL in their respective chains to promote ecosystem growth.Additionally, some vaults provide leveraged points farm strategies by recycling or borrowing BTC to maximize returns with the same capital.

Gearbox offers up to 27 times the lombard points borrowed into WBTC via leverage (up to 7 times).However, the service is not popular because the supply in gearbox is very limited (only about $3 million).

Source: gearbox.fi

In addition to the points strategy, some Layer 2 networks, such as Thesis’ Mezo and Binance Labs-backed Corn, are leveraging the value of BTC in return by allowing nodes to “stake” the bridged BTC LSTs as collateral, thus leveraging the value of BTC, which is in return for participating verification.The process earns $BTC fees, which is a good attempt to leverage BTC and guide TVL of these networks to promote future ecosystem growth.So far, mezo has attracted $121 million in BTC-related assets and $20 million in corn.

So far, it has been clear that most of the DeFi activities associated with BTC LSTs are primarily driven by incentives.While BTC adoption is growing, the actual demand for generating BTC LSTs will be highly dependent on Babylon’s earnings performance in the long run, which could make BTC LSTs a more attractive asset than ETH.

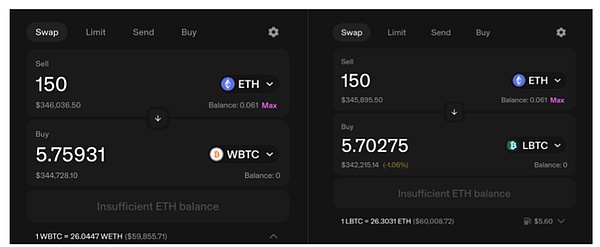

2.2.5 Liquidity issues

Despite having a $300 million TVL, the deepest pool has only about $10 million in liquidity in the Uni v3 pool (according to nansen).Swapping $345,000 ETH for LBTC will result in a 1.06% slippage, which is 4 times that of WBTC (about 0.4%).This difference reflects a key issue that BTC LSTs must overcome: liquidity issues when mass exit from LBTC positions.

Source: Uniswap

3. Summary

Bridged BTC can mainly take two forms: ordinary BTC, such as Wrapped BTC (WBTC), and BTC re-staking in Babylon, called BTC-LST.

The BTC LST/LRT-Fi landscape is still in its early stages, but shows healthy signs of bridging more TVL from BTC to the ETH DeFi ecosystem.

BTC adoption is expected to increase due to its growing recognition and market dominance in the current cycle.Opportunities to generate returns for BTC also create a market for speculative and trading activities on ETH.

WBTC remains one of the most widely adopted forms of BTC on ETH.However, tBTC or LBTC is expected to gain more adoption due to the recent challenges facing the association with Justin Sun.

It is increasingly common to see BTC re-staked tokens re-staked in Symbiotic or Karak for leveraged farming.While this may generate higher benefits, users must bear the risk of multiple cuts.

Money market and interest rate swaps are the most demanding BTC DeFi activity on ETH, and it is also interesting to try to use BTC as a fee during the verification process.

Currently, most of the DeFi activities related to BTC on ETH are mainly motivated by points or rewards.To generate actual demand, BTC LSTs need to create value (possibly in the form of income), which needs to be greater than ETH LSTs.

Custody risk, risk reduction and liquidity risk are the main concerns in the BTC LST landscape.