Author: danny; Source: X, @agintender

Nvidia announced its Q3 financial report on November 19. Although it cannot be said that the results are outstanding, it can also be said that it exceeded expectations.The problem is that with such a report card, the market did not pay for it and began to fall sharply after rising by 5%.Many friends in the currency circle are confused.This article attempts to summarize, interpret and analyze the hidden aspects of this seemingly “too good to be true” financial report from the perspective of a short-seller.

In addition, there are too many articles about singing more, so I won’t go into details here.

If you are too lazy to read a long article, here are some of the core empty-talking views, please take them away without any thanks:

-

Revolving Financing Manufacturing Revenue: Nvidia has built a closed loop of capital return by investing in customers such as xAI, converting investment funds into its own book income, and lacks substantial cash delivery.

-

Abnormal surge in accounts receivable: The balance of accounts receivable reached US$33.4 billion, with a growth rate that far exceeded revenue, and the calculation of turnover days was suspected of concealment, implying serious “channel congestion” and back-end loading.

-

Inventory and Narrative Divergence: Under the narrative of “supply exceeds demand”, the inventory of finished goods unexpectedly doubled, prompting potential customers to delay delivery or the risk of unsalable products.

-

cash flow inversion: Operating cash flow is significantly lower than net profit, which proves that the company’s profits mainly remain in the books and have not been converted into real money.

This article does not constitute any investment advice.This article is just a collection of opinions.

1. Recurring revenue and supplier financing models

1.1 Closed-loop mechanism of capital flow

Background: In November 2025, Elon Musk’s xAI completed a US$20 billion financing round, in which Nvidia directly participated in an equity investment of approximately US$2 billion, but this is not a simple “investment behavior.”Follow the logic step by step:

Capital outflow (investment side): Nvidia transferred cash (approximately $2 billion) from its balance sheet and recorded it as “Purchases of non-marketable equity securities” as an equity injection into xAI or related SPVs.This outflow is reflected in the cash flow statement under “Investing Activities.”

Capital conversion (client): xAI receives this fund as a down payment or capital expenditure budget to purchase a GPU cluster (i.e., the Colossus 2 project, involving 100,000 H100/H200 and Blackwell chips).

Capital repatriation (revenue side): xAI immediately issued a purchase order to Nvidia.Nvidia ships and recognizes “data center revenue.”

Financial results: Nvidia actually converted the “cash” assets on its balance sheet into “revenue” and “net profit” on the income statement through the intermediary of xAI.

Although this kind of operation is usually allowed under accounting standards (GAAP) (as long as it is evaluated), it is actually a kind of “low-quality revenue” (IFRS is dissatisfied here and just wants a fight?)

This is also criticized by short sellers such as Michael Burry, because this model of “almost all customers being funded by their suppliers” is a typical feature of the late bubble period.When a company’s revenue growth relies on its own balance sheet expansion, its revenue growth will dry up once it stops investing outside the country.(Does it feel like a nesting doll in a currency trap?)

1.2 Leverage effect and risk isolation of SPV

If you think the recurring revenue model is a bit surprising, the special purpose vehicle (SPV) structure involved in the deal may be an eye-opener.

According to news reports, xAI’s financing includes equity and debt. The debt part is structured through an SPV, which is mainly used to purchase Nvidia processors and lease them to xAI.

The operating logic of SPV: As a legally independent entity, SPV holds GPU assets.Nvidia is not only a seller of GPUs, but also an equity investor in the SPV (First-loss capital provider).This means Nvidia has dual roles in the deal: supplier and underwriter.

Circular arbitrage model of revenue recognition: By selling hardware to the SPV, Nvidia can immediately recognize the full amount of hardware sales revenue.However, for the end user xAI, this is essentially a long-term lease (Operating Lease), and its cash outflow is carried out in installments (such as 5 years).

Risk Concealment: This structure converts long-term credit risk (whether xAI can pay rent in the future) into immediate revenue recognition.If the price of AI computing power collapses in the future, or xAI cannot generate enough cash flow to pay rent, the SPV will face default, and Nvidia, as an equity holder of the SPV, will face the risk of asset writedowns.But in the current earnings season, it all shows up in the form of glossy Genesis revenue

1.3 The shadow of supplier financing during the Internet bubble period

The current business model is somewhat similar to the Internet bubble in 2000.At the time, Lucent was lending billions of dollars to customers to buy its own equipment.When Internet traffic grew less than expected and these startups defaulted, Lucent was forced to write off huge bad debts and its stock price crashed 99%.

Nvidia’s current exposure (direct investment + SPV debt support) is estimated to be over $110 billion, accounting for a significant proportion of its annual revenue.Although Nvidia does not currently list it directly as “customer loans” on its balance sheet, its material risk exposure is consistent through holding customer equity and SPV interests.

2. Doubts about accounts receivable

2.1 The proportion of accounts receivable has grown rapidly

According to the Q3 FY2026 financial report, Nvidia’s accounts receivable balance reached $33.4 billion

The year-over-year growth rate of accounts receivable (224%) is 3.6 times the revenue growth rate (62%).In normal business logic, accounts receivable should keep pace with revenue growth, especially since Nvidia is so “strong.”When accounts receivable grow far faster than revenue, this usually means two possibilities:

a. Decline in revenue quality: The company relaxed credit terms and allowed customers to defer payments to stimulate sales.

b. Channel stuffing: The company rushes shipments to channel dealers at the end of the quarter to recognize revenue, but these products have not really been digested by the end market.(This will be discussed later)

2.2 Algorithm of DSO (days of accounts receivable turnover)

DSO for the quarter was 53 days, down slightly from 54 days in the previous quarter.So what is the actual situation?

First, the standard DSO calculation formula: DSO = (Accounts Receivable/Total Credit Sales) x Number of Days in the Period

Beginning AR (end of Q2): $23.065 billion

Ending AR (end of Q3): US$33.391 billion

Average AR: US$28.228 billion ((Q2+Q3)/2)

Quarterly revenue: $57.006 billion

Number of days: 90 days

The standard DSO is approximately 282.28 / 570.06 *90 = 44.566 (days)

However, the reported DSO is 53 days.It stands to reason that from the perspective of “whitewashing” the report, a more “radical” number would usually be reported, but here it is conservative?This implies that Nvidia may be using the end-of-period accounts receivable as the numerator, or its calculation logic is more inclined to reflect the capital occupation at the end of the period.

If calculated using ending balance:

333.91 / 570.06 *90 = 52.717 (days)

This number is consistent with the report.But what does this mean?This means that the accounts receivable balance at the end of the quarter is extremely high relative to sales for the entire quarter.This hints at the back-end loading phenomenon, where a large amount of sales occur in the last month or even the last week of the quarter.

If sales were evenly distributed, ending accounts receivable should only include the last month’s sales (approximately $19 billion).But the balance now stands at $33.4 billion, which means nearly 58% of quarterly revenue did not receive cash.

Under the so-called “seller’s market” and “supply exceeds demand” narrative, Nvidia should have strong bargaining power and even require advance payment.However, the reality is that not only did Nvidia not receive the advance payment, but it instead provided customers with an account period of nearly two months?!This doesn’t seem to be consistent with the “rush buying” narrative?!

3. Inventory puzzle: the paradox of insufficient supply and overstocked inventory

When Jensen shouted “Blackwell demand is crazy (Off the charts)”, Nvidia’s inventory data seemed to tell a different story.

3.1 Reasons for doubling inventory

Total inventory in Q3 FY2026 reached US$19.8 billion, almost double from US$10 billion at the beginning of the year, and an increase of 32% from US$15 billion in the previous quarter.

What’s more critical is the composition of the inventory:

Raw Materials: $4.2 billion

Work in Process (WIP): $8.7 billion

Finished Goods: $6.8 billion

In a word, finished goods inventories surged.At the beginning of 2025, finished goods inventory was only $3.2 billion.It has now surged to $6.8 billion.Especially when Lao Huang is shouting that the demand is crazy and explosive, under the assumption that there is a shortage of chips and customers are queuing up to wait for the goods, the finished products should be “shipped as soon as they are produced” and the inventory level should be kept at an extremely low level.

Why is this?Do you want to wait until the Chinese New Year to collect the bill?

3.2 US$50 billion in procurement commitments

In addition to the inventory on its balance sheet, Nvidia also disclosed supply-related commitments (Purchase Commitments) of up to $50.3 billion.This is the future purchase amount Nvidia has committed to suppliers such as TSMC and Micron.

This is a huge “hidden danger”.If AI demand slows or weakens in any way in the coming quarters, Nvidia will face a double whammy:

-

Inventory impairment: Existing inventories of $19.8 billion may lose value.

-

Default or compulsory purchase: A US$50 billion purchase contract will lead to more inventory backlogs or the payment of huge liquidated damages.

The emergence of this “heavy asset” characteristic indicates that Nvidia is no longer the asset-light chip designer, but more and more like a hardware manufacturer carrying a heavy supply chain burden.

Production capacity is running ahead, and inventory is chasing behind. Is this really out of control?

4. Profit increases, but cash flow decreases?

4.1 The inversion between operating cash flow (OCF) and net profit

Normally, a healthy technology company’s operating cash flow should be higher than net income (because depreciation, amortization and stock-based compensation are non-cash expenses and will be added back).However, Nvidia’s data shows the opposite trend.

Q3 Net Income: US$31.9 billion

Working Capital Changes:

Cash outflow due to increase in accounts receivable: -$5.58 billion

Cash outflow due to inventory buildup: -$4.82 billion

Q3 operating cash flow (OCF): approximately US$23.75 billion

Conclusion: Q3 operating cash flow was significantly lower than net profit.For every dollar of profit, only about $0.74 is actually converted into cash inflow, and the rest becomes chips in the warehouse (inventory) and IOUs (accounts receivable) from customers.

Of course, this phenomenon of OCF < Net Income depends on how you interpret it. It can mean that the company’s profits are confirmed by accounting standards, rather than supported by real money in bank accounts; it can also mean that the company is developing at a high speed.

4.2 Cash bleeding from investment activities

Purchases of non-marketable equity securities — commonly known as investments: $3.7 billion in outflows this quarter.

This US$3.7 billion is flowing to “ecosystem partners” such as xAI, CoreWeave, and Hugging Face.That compares with just $473 million in the same period last year.Nvidia is ramping up its buyout of the ecosystem at the pace of SpaceX.

From the xAI model, the investment process may be as follows:

-

Nvidia accumulates cash through debt issuance or previous profits

-

Invest cash in startups (cash outflow)

-

The startup uses the money to buy chips (recognized as revenue)

-

Nvidia’s book profits increase, its stock price rises, it attracts talents through equity incentives, and then raises funds through debt issuance or additional issuance (does it feel like a currency trap?)

If it is really this mode, it will feel a bit like musical chairs. Of course, as long as the music does not stop, the game can continue to be played.But once the financing environment tightens (such as interest rates rising or the AI bubble bursting), the game may stop instantly.

5. Nvidia’s dominance is not sacrosanct

In the 10-Q filing, Nvidia disclosed a very high customer concentration ratio, of which “Customer A” accounted for 22%.Although not named, there are only a few wealthy companies on this planet, and it is almost certain, 100% certain, that it is Microsoft.

There is another layer of “related party transaction” risk hidden here.Microsoft is OpenAI’s largest financier, and Nvidia has also invested in OpenAI.When Microsoft purchases Nvidia chips, a large part of them should be used by OpenAI.Both of them are shareholders, so the share of the share is unknown?Does anyone know if there is any special clause?

Also, what if Microsoft gives up and doesn’t buy it today?

In addition, the existence of Customer B (15%), C (13%), and D (11%) means that the top four customers control Nvidia’s lifeblood.This concentration makes Nvidia less dominant in pricing negotiations than outsiders imagine.On the contrary, these giants are using their huge purchasing volume to force Nvidia to make concessions in supply chain allocation, customized chip design, etc., and are even accelerating the development of self-developed chips (such as Google TPU, AWS Trainium, Meta MTIA) to get rid of dependence on Nvidia.This can also be seen from the increase in accounts receivable.

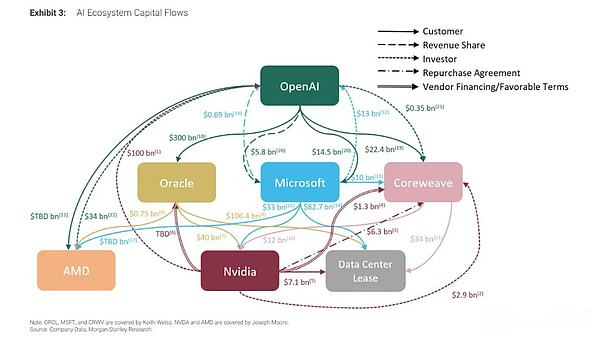

The picture below gives you a visual representation of the complex structure of the OPEN AI cluster. I would like to ask you, can you understand the calculation?

Postscript

Why write this article?First of all, I haven’t written a long report research article of this type for a long time, and I wanted to revisit the feeling of reading a report.

Secondly, there is a voice or logic in the market. The encryption market looks at the US stock market, the US stock market looks at the AI revolution, and AI looks at NVIDIA’s performance. Although NVIDIA’s financial report exceeded expectations, there are still many bearish views.

Compared with other specious bearish views, it is of empirical significance to look for clues from the financial reports.

It’s been a long time since I’ve written a similar statement analysis report. Quandang will provide you with another perspective on the current market environment.