Liquity Protocol Overview -Core Concept

Ponzi scam metaphor in traditional finance

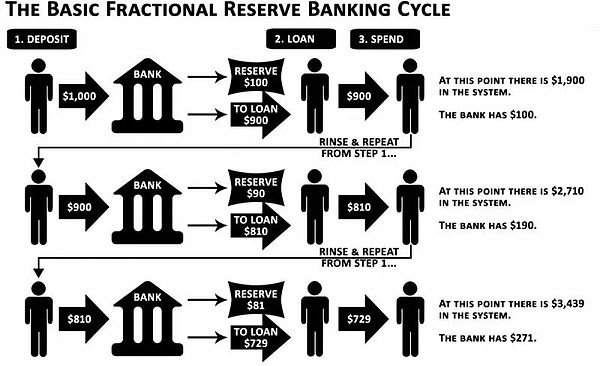

Ponzi scheme, which is commonly used to describe cryptocurrencies in traditional finance (Tradfi).People in the traditional financial circle are proud of their investment in “safe” and “stable” monetary system.However, they may not know that since the beginning of the 19th century, banks have actually been a manifestation of a naked Ponzi scheme.Let’s take a look at this little-known system-some reserve bank system (Fractional-Reserve Banking, that is, “partial reserve system”).

>

Analysis of part of the reserve system

Part of the reserve system is a system that allows bank loans to lend far exceeding its actual holding reserve.The reserve ratio is the lowest percentage of customer deposits that banks must retain, and the remaining parts can be used for loan lending.This system enables banks to create currencies through loans, because new loans will generate new deposits and expand the supply of currencies.So, how does this system become a Ponzi scheme?In fact, this system depends on the continuously increasing new deposits to maintain operation. Similar to the Ponzi scheme, when the bank does not have enough deposits to inflow (the new deposit cannot pay the withdrawal demand), the system collapses and the bank crowding will occur.

The reserve ratio (set by the Federal Reserve) is usually 10%, but it turned out to be 0%when writing this article (mid -March 2023).This means that in theory, banks can create unlimited currencies by only $ 1 deposit.Although this system is important to the global economy (because it stimulates demand), it pose a variety of threats to the stable currency we know and use.

USDT, USDC, BUSD, TUSD, and USDP -These are the centralized stable currency in the head in the encryption field. Their total market value is about 123 billion US dollars, accounting for about 10%of the global cryptocurrency market value.Most of these stable currencies come from the US dollar stored in a bank account.Come on?The keyword is “bank account”, which meansThese deposits are also subject to some reserve systems that may crash at any time.Recently (March 10, 2023), Silicon Valley Bank (SVB) closed down. This is the second largest bank closure in the United States, causing huge shocks in the encryption market.Because the issuer of the USDC stabilized coin, Circle had about 8% of the reserve of SVB, causing USDC to fall to $ 0.88, which is 12% lower than the US dollar.

If it is not the involvement of FDIC (federal deposit insurance company), the USDC 8% reserve will disappear out of thin air, which will lead to the real price of USDC to $ 0.92.What serious consequences of retail investors) have caused.When you read this, you might think, “But isn’t there many decentralized stablecoins that can replace USDC? For example, FRAX and DAI.”The problem is that these so -called “decentralized” stablecoins are not so decentralized because most of their reserve comes from centralized stablecoins.For example, MakerDao’s DAI stabilization currency is supported by USDC, and a large part of the FRAX stablecoin in circulation is also supported by USDC.

IGNAS | Defi Research pointed out on Twitter: “We found that $ USDC’s endorsement is cash held by banks, but … banks actually do not hold these cash.”/ Twitter

>

When we mention DEFI, we usually think that it is a completely parallel financial system.But since the goal of the encrypted industry is to completely get rid of the traditional financial system (Tradfi), why does DEFI still rely on this system that it wants to break away?

>

Introduction to the liquity protocol -decentralized stable currency solution

The liquity agreement came into being. It is a real decentralized stable coin issuer, which is not affected by any bank risk.The protocol uses Ethereum’s security to use $ ETH as a mortgage as a mortgage to cast a stable currency on the Ethereum blockchain $ LUSD (linked to the US dollar).This means that $ LUSD is completely supported by $ ETH, and $ ETH can be said to be one of the highest quality mortgages in cryptocurrencies.

In addition to providing decentralized stablecoins, the liquity protocol also providesComplete interest -free loan, high capital efficiencyAnd the generous income of its stable currencyEssence

The tokens of the liquity protocol -in -depth analysis

>

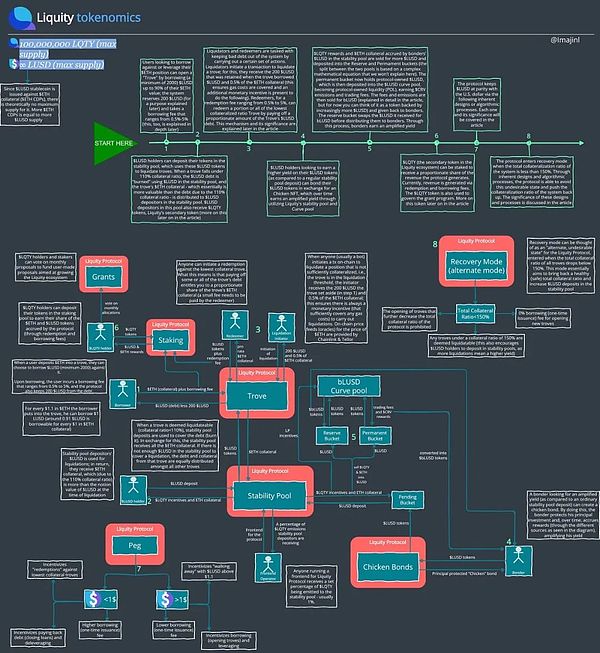

Liquity protocol adoptionDouble -generation currency economic modelThe$ LusdIt is a native stabil (Native Stablecoin) issued by the protocol, and$ LqtyIt is used to motivate the tokens adopted by certain functions of the protocol, and it is also the value capture tokens in the ecosystem.We will introduce these two tokens in detail later.

Liquity protocol: parsing TROVE and Stable Ponds

TROVE is the core component of the liquity protocol.They promote the creation of mortgage debt positions (CDPS).Simply put, users can deposit the $ ETH token as a collateral and cast a stable coin $ LUSD of liquity.You can understand Trove as the MakerDao vault of the Liquity version, but there are some subtle differences.

>

First of all, Liquity’s TROVE only accepts $ ETH as a mortgage.This is because the main goal of the agreement is:

-

Keep the price stable 稳

-

Keep decentralization

-

Maintain anti -censorship ability

-

Sacrifice price stability,Because the mortgage may fluctuate high and low on the chain, it increases the risk of forming bad debts.Due to insufficient liquidity, liquidation may not be executed, or due to the sudden decline in prices, liquidation no longer has economic feasibility.

-

Sacrifice the decentralization,Because some underlying mortgages may have centralized characteristics (for example, if the mortgage is USDC or USDT).Therefore, these protocols usually need to increase the minimum mortgage rate (maintaining the health level of the mortgage to prevent the sudden decline in prices and provides sufficient time for liquidation), which reduces their capital efficiency.In contrast, Liquity’s TROVE only accepts $ ETH as a mortgage, which can reduce the mortgage rate to 110%(because $ ETH has less volatility compared to most other DEFI tokens and sufficient liquidity on the chain).

-

The holders of $ lusd stablecoin can choose to deposit their $ LUSD token in the pool.

-

When any TROVE mortgage rate drops below 110%, anyone can initiate a transaction to liquidate the TROVE and get itTrue0.5% $ ETH mortgage and user openingTrueSet at 200 $ LUSD.

-

The minimum $ LUSD debt is 2000, which has made many small retail investors discourage

-

The secondary clearing model and recovery mode may allow some users to be cautious about the agreement

-

Accept $ ETH as a collateral (this may be the biggest problem with liquity scalability)

$ ETH is an ideal mortgage in these aspects.

Other main stable coins issuers, such as MakerDao, Abracadabra Money, Inverse Finance and QIDAOProvide a variety of mortgage options, which allows them to expand scale (issuing more stablecoins), but it also brings some problems accordingly:

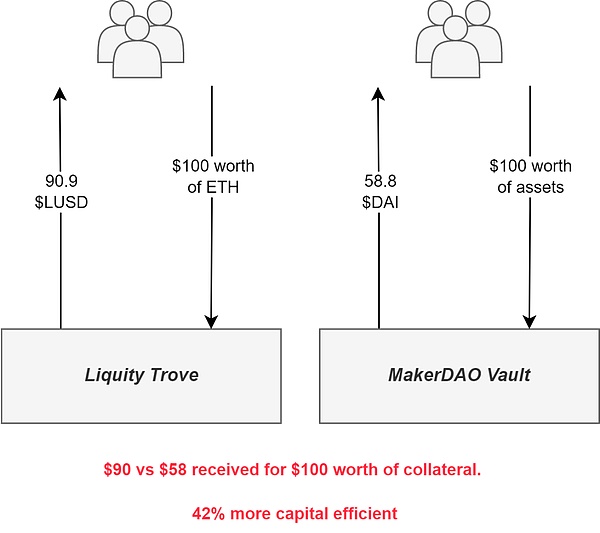

In short, this means that each ETH tokens worth $ 1.1 are used as mortgages, and 1 LUSD can be borrowed.This makes Trove have extremely high capital efficiency, because you can use less mortgage to bear more debt.

To better understand this, we can see MakerDao.The minimum mortgage rate of most MakerDao vaults is about 170%, which means that each mortgage of $ 1.7 can only be cast (borrowed) 1 $ DAI stablecoin.

>

Second, it may also be the most important point. TROVE of the liquity protocol allows interest -free lending, that is, you can use your $ ETH tokens as mortgage without paying any interest.

Most stable currency issuers (as mentioned earlier) usually collect debtsFloating interest rateThe range from several percentage points to higher, which reduces the attraction of opening debt positions.Not only has interest rates itself deterred, but its variability makes interest rates unpredictable.

This interest rate willCompound interest(Quickly accumulated over time), this is alsoIncrease the risk of liquidation(It usually leads to a few percentage points of net loss of mortgages because it is necessary to pay the clearing fine to the liquidator), because the value of your debt relative to the mortgage is increased (assuming that your mortgage price is relatively stable or completely stable).

However, the liquity protocol will indeed receive itOne -time borrowing feeThe rate floats between 0.5% and 5%.Although the cost is usually 0.5%, the article will explain why the cost will change later.

This one -time borrowing fee will be added to the debt when the TROVE is opened, and paid is paid when the user closes Trove.It is worth noting that the main stable currency issuers, including Abracadabra Money and Qidao, also use this cost structure.For users who want to open debt positions, this is a better choice, because it is a one -time fee, and the cost is significantly lower than the floating interest rate in the long run.

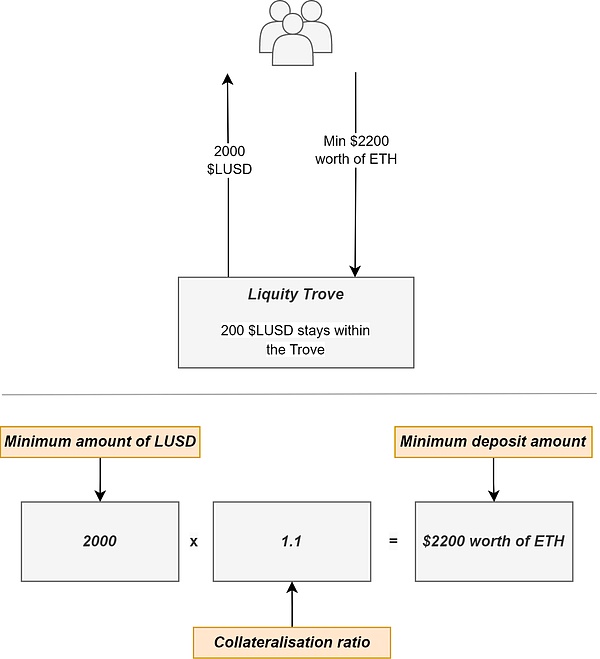

thirdPerhaps the only main disadvantage of Liquity’s lending mechanism is that the minimum amount of $ LUSD (that is, debt) borrowed is 2000 $ LUSD.

>

This means at least $ ETH mortgage worth $ 2,200 to the agreement.In addition, the agreement reserves 200 $ LUSD from the debt it undertaken (the reason will be explained behind the article), and it will be returned only when the user closes Trove.

>

Finally, the liquity agreement is not under DAO, and its smart contracts are completely unchanged.

What is the relationship with TROVE?In a system like MakerDao, $ MKR (Maker’s auxiliary token) is used for governance protocols and can be used to vote for key matters, such as changing key parameters such as interest rates, minimum mortgage rates, and new mortgage types.

What are the disadvantages of this system?first,It is not always decentralized.Some “giant whales” may accumulate a large amount of governance power to affect decision -making, which will benefit them (rather than vote in the best interests of the agreement), and the participation rate of governance voting is usually very low.Secondly,These systems may be manipulated by lightning loans.at last,These governance proposals usually need to be developed, discussed and finalized for a long time.also,It may not be efficient to rely on a system that requires artificial governance, because they may not be able to master all the information required for making wise decisions.

In contrast, the protocols such as LIquity are completely governed by algorithms -these algorithms are not manipulated, after actual combat testing, the protocol is most appropriately adjusted using transparent blockchain data.Specifically, the expenses related to TROVE are adjusted by these algorithms according to market conditions (there will be more introductions in the article later); secondly, the unsatisfactory of the agreement means that it cannot introduce any interest rate or new mortgage type, the minimum mortgage rateIt cannot be changed.Although such a system may be the best in decentralization, it may pay some costs in terms of security and scalability.Since the LIquity’s smart contract is immutable, any vulnerability or defect in the code cannot be changed.At the same time, users’ growing preferences for mortgage debt positions may not be satisfied, which hinders the possible innovation that may have occurred.If the system is variable, it may better adapt to these changes.

One of the contents you just read may make you impressed:Very low minimum mortgage rate.You may think, “110% of the mortgage rate is definitely not safe, which will greatly increase the risk of bad debts” (which leads to the unstable price of $ LUSD stablecoins).

>

This worry may be applicable to other stable currency issuers using traditional clearing systems.

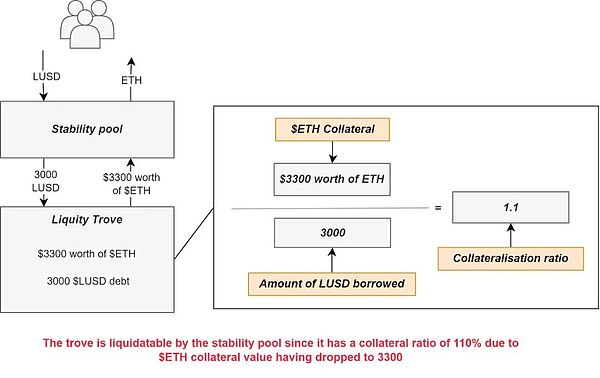

But Liquity uses an innovative concept-Stable pool, Achieve the most advanced clearing system.

It works like this:

This ensures that the liquidation process is always economic incentive.This is very important, because if the value of the collateral is lower than the debt, the user does not have the power to repay debt and obtain the equivalent mortgage and liquidation rewards.

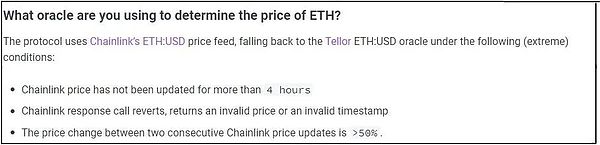

How does the liquidation person know when Trove is insufficient mortgageIntersectionLiquity uses the chain price prophecy to determine the price of $ ETH, so as to determine which TROVE can be liquidated.These prophecy machines are mainly provided by ChainLink, and the spare prediction machine is provided by Tellor.The picture below (from the liquity document) describes the use of the Tellor prediction machine to provide $ ETH price information.

>

Now you know how the liquidation is started.But what will the debt be dealt with?After the liquidation starts, TROVE’s undertaking debt is actually offset (destroyed) by the $ LUSD deposit in the stable pool.The mortgage was then confiscated and returned to the stable pool.In this way, the stable pool depositors obtain the $ ETH mortgage of the Trove Trove in proportion.To the $ 0.5%$ ETH mortgage to the liquidator, the calculation results were 9.45%, but because the volatility of $ ETH was 9%).This means that depositing $ LUSD into the stable pond is always favorable, because TROVE will always maintain excess mortgage status.

>

It is worth noting,The stabilization pool is also further incentive by the auxiliary tokens of liquity $ lqty.Make the deposit to the stabilization pool more attractive.

Overall, the incentive mechanism that stores LUSD into the stabilization pool is mainly a very competitive stable currency yield (annualized interest rate, APR).composition.

butWhat if the $ LUSD in the stable pool is not enough to pay off the debt of a borrowing position?Don’t worry, developers have considered this situation.In this case, debt and mortgage are evenly distributed to all other unreasonable borrowing positions.Although at first glance, this seems to be unfavorable for users who have unreasonable positions, but in fact, other positions will get net income when liquidation (of course, over time, the price of $ ETH may fall, and the situation may be at that time.No more).

The picture below is taken from the liquity document, which shows the re -assignment of debt and mortgage between all other true.

>

However, because the deposit in the stable pool is sufficient enough, the agreement has never been used in this secondaryLiquidation modeAnd I think that in the future, the situation of the use of this sub -clearing mode will not occur often.It is just a spare mechanism set up to cope with the worst situation.

>

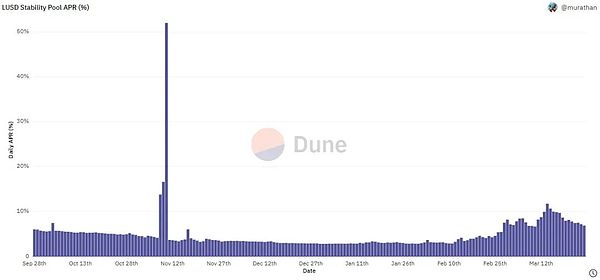

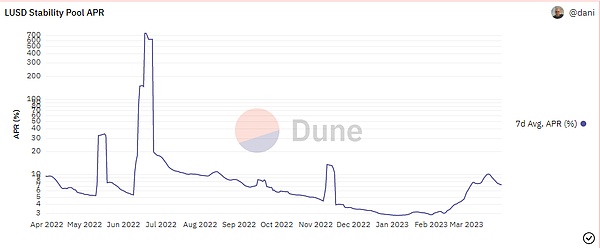

As shown above,Most (about 65%when writing this article) $ LUSD Stable Coins are stored in the stable pool, because this is the most important case of $ LUSD at presentEssenceThis can be attributed to the annual interest rate of the stable pool deposit (see the figure below), with an average month of about 7.9%and an average annual an average of about 22%.Such a stable currency yield is very rare.

>

Even when the $ lqty incentives issued to the stable pond start to reduce and eventually exhausted, TROVE will still have additional $ ETH collaterals when liquidated (when the mortgage rate & lt; 110%)Essence

If this is not enough to inspire users to deposit $ LUSD (such as APR deposited in a stable pool may be lower than other opportunities to earn $ lusd earnings), robots using Lightning Loan (deposit in a block of $ lusd to cancel the debt, to cancel the debt.And take out $ eth) can always provide $ lusd liquidity to clear Trove.In this way,The system does not need to rely on users to save $ lusd into the stable pool,It does not need to rely on the secondary liquidation mechanism (that is, the distribution of debt and mortgage between all other unrelated borrowing positions) to complete the liquidation.

As you can see here, not only have bad debts never appeared in the agreement, but all liquidation is seamless. It happens when it should occur (when Trove’s mortgage rate is reduced to less than 110%).In contrast, MakerDao, Abracadabra and many other stable currency issuers have encountered liquidation problems in the past, often leading to bad debts and non -debt.Some protocols such as MakerDao will cast and sell their $ MKR tokens to make up for these bad debts, but you can see that this is a system that is far less than liquity.

>

However,The clearing model used by liquity also has a potential risk: Chainlink’s feeding price (you remember, the liquity protocol uses these for liquidation) is controlled by a 4/9 multi -signature and may be manipulated.However, as mentioned earlier, if Chainlink’s price is suspicious, Tellor will be used as a backup.Although this reduces some of the risks brought by using ChainLink, it does leave a potential attack vector (if Chainlink and Tellor are manipulated at the same time, it may be due to regulatory pressure).This risk cannot be completely eliminated due to the non -variability of the liquity contract.

Liquity protocol: analytical recovery mode

The recovery mode can be regarded as a “alternative and unsatisfactory state” of the liquity protocol. When the total mortgage rate of all borrowing positions is less than 150%, it will enter this model.The main goal of the recovery model is to restore the total mortgage rate of the agreement to the level of health (safety) by repaying debts or supplementary mortgages, and increase the $ LUSD deposit in the stable pool.

How is the agreement realized thisWhat about point?First of all, the agreement banned any users who could not increase the total mortgage rate of the system to open a new borrowing position.Secondly, in order to encourage users to open a new borrowing position to increase the total mortgage rate of the system, the agreement will be exempted from the loan fee.Third, any borrowing positions with a mortgage rate of less than 150% will be considered clearing, which will also inspire $ LUSD holders to deposit funds into a stable pool because more liquidation means higher returns.Through these measures, the agreement can simultaneously increase the total mortgage rate and increase the deposit of the stable pool.

Although this mechanism is important during the market or agreement turbulence, it is just a short -term operation mode. Once triggered, it usually only lasts a short time (in fact, this model has only been started once, and it lasted only a few minutes for a few minutes.To.In addition, the probability of the protocol triggering the mode itself can effectively prevent the system from entering this state.

It is worth mentioning,Recovery modelThe clearing mechanism under the formula is different from the normal mode,But you don’t need to understand this part of the details.If you are interested, you can read the detailed introduction to the recovery mode in the official document of liquity.

Liquity protocol: Maintain the $ lusd anchor mechanism

So far, we mainly discuss the liquity agreement.Now, let’s combine these new knowledge,Understand how the internal protocol design and algorithms of liquity are kept $ LUSD stable at the ideal $ 1 anchor (equivalent).

Before continuing, first introduce a simple mechanism in the agreement called “redemption”.In this process,Anyone (usually a robot) can convert $ LUSD to $ ETH from the lending position with the lowest mortgage rate.This means that the redemption is essentially another way to repay part or all $ LUSD debts. Retain has the right to obtain the $ ETH mortgage of the corresponding proportion in the borrowing position.By 5%, adjust according to the anchor situation of $ LUSD; please refer to the relevant content for more information), and these costs are paid to the agreement.

For example, assuming that the borrowing position with the lowest mortgage rate has a debt of 400 $ LUSD, the current $ ETH price (for simple reasons) is $ 1.In this case, we set the redemption fee of 1%.Anyone can now use a $ 396 $ ETH tokens worth $ 396.So, where did $ ETH worth $ 4?This is a 1% redemption fee paid to the agreement.Why is someone willing to redeem from the borrowing position with the lowest mortgage rate?We will explain this problem in the next few paragraphs.

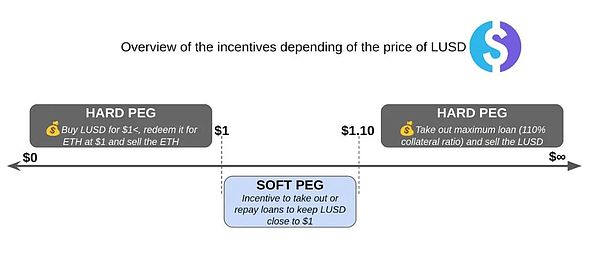

Now, let’s talk about the anchor.

Scenario 1: The price of $ LUSD is higher than $ 1.How to reduce the price?

1) Reduce the cost of one -time borrowing

2) Inspire users to borrow (open borrowing positions) and increase $ ETH for leverage operation

3) When the price of $ LUSD is higher than $ 1.1, the user is inspired to open the borrowing position and “cash out the venue”, that is, after borrowing the $ LUSD, which is profitable by selling or redeeming other assets, and then exiting the operation.

Let us analyze these strategies one by one.

1) The protocol use algorithm to determine the one -time loan fee.If the anchoring price of $ lusd is higher than $ 1, the borrowing fee is usually reduced, encouraging users to open a borrowing position, because this is lower for them (this is why the borrowing fee range mentioned earlier from 0.5% to 5%between).More borrowing positions will be opened to increase the supply of $ LUSD, thereby lowering the price; although the supply of $ LUSD will not directly reduce the price, this will prompt more people to sell their newly cast $ LUSD, which brings brings to bringThe price fell.

2) When the price of $ LUSD is higher than $ 1, users will be automatically motivated to open borrowing positions and sell their newly cast $ LUSD.In this way, they can use $ LUSD for more other stablecoins, and then turn off their positions when the price of $ LUSD is restored to $ 1, and earns the difference between the sale of $ LUSD.In addition, users who watched $ ETH (therefore want to increase leverage) can take action when $ LUSD is higher than $ 1: they can open borrowing positions, generate $ LUSD, and sell these $ LUSDs (thereby reducing its price) in exchange for more $ETH (because the price of $ LUSD is higher than expected, they can get more $ ETH), and then store these $ ETHs into the position again (increase the maximum amount of borrowing, because the mortgage increases), and then repeat this process.

3) When the price of $ LUSD is higher than 1.1 US dollars, economically, users will tend to generate $ LUSD at the minimum mortgage rate (110%) at the minimum mortgage rate (110%), and profit by selling these $ LUSDs (thereby low prices)Essence

Scenario 2: The price of $ LUSD is lower than $ 1.How to increase the price?

1) Improve the cost of one -time loan

2) Inspire users to repay the debt (close the borrowing position) and reduce the $ ETH leverage

3) Inspire users to redeem the borrowing position with the lowest mortgage rate

Let us analyze these strategies one by one.

1) If the price of $ LUSD is lower than $ 1, the borrowing fee is usually raised (please remember, the borrowing fee is dynamic, up to 5%), so that users can restore the new borrowing position because the cost has become higher.The opening of the new lending position will ensure that fewer $ LUSDs are cast and sold, and the price of $ LUSD will be further deviated from the anchor value.

2) When the price of $ LUSD is lower than $ 1, users will be automatically motivated to close the borrowing position.Those users who have already opened a loan position but keep their debts in other stablecoins or other investment will be inspired to repurchase $ LUSD (promoting $ lusd price rebate) and repay the debt because this is lower for them.In addition, users who use leveraged operations can repurchase $ LUSD (promoting $ lusd price rebate) and repaying debts to solve the leverage because the cost is lower.

3) When the price of $ LUSD is lower than $ 1, anyone can redeem $ ETH from the lending position with the lowest mortgage rate, which is economical.Anyone can buy $ LUSD (pushing the price rebound) and redeem the position of the minimum mortgage rate to earn a difference, because the $ ETH value of the redemption is higher than the $ lUSD they purchased lower than the anchor value.

The following is a concise icon, which shows two scenes that are lower than and higher than the anchor value.If you want to understand the anchoring mechanism of $ LUSD more deeply, I recommend reading, “How to make,” and “The Premium OF Resiliation Lisd’s PEG and LIQU Idity Strategy “, these twoarticle.

>

Now, there is another key variable that needs to be discussed.Lobricity.

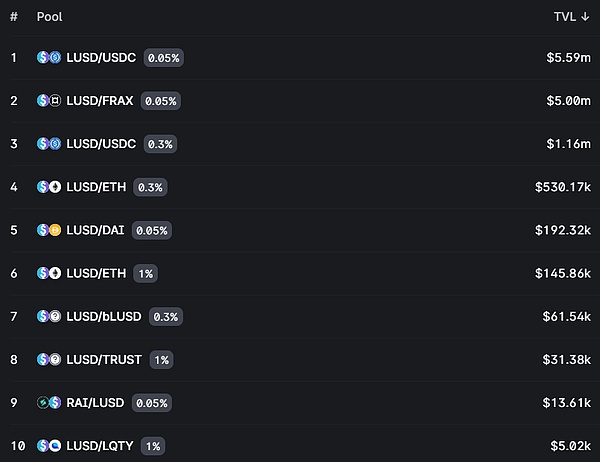

For stable currency like $ lusd,Deep liquidity (powerful market depth)It is essential for improving user experience.A sufficient liquidity can ensure that users enjoy lower price sliding points and market impacts when transaction stabilization coins, and at the same time help keep the price of stable coins at the $ 1 anchor value that is close to the ideal.

>

As shown above, the $ LUSD pool on the CURVE (leading stabilization coin automatically) has a liquidity of about $ 25 million, and the proportion of the pool is very healthy (the pool is not mainly composed of $ LUSD token).

>

In addition, the UNISWAP V3 (another leading stabilization coin automatically as a market business) also has a lot of $ LUSD liquidity pools.

In addition to the Ethereum chain, $ LUSD also has millions of dollars on other chains (through cross -chain bridges like Celer, you can cross the chain to Ethereum L2 solution), such as Arbitrum and OptimismEssenceYou can check all the $ LUSD markets here.

Now you have learned about the powerful algorithm, protocol design and other related factors of $ 1 anchor.

Finally, we summarized this part of the content by viewing the performance of $ LUSD this year (2023).

>

As you can see, the transaction price of $ LUSD has been kept in a narrow range close to the anchor value. Although there are some fluctuations during the $ USDC anchor incident, it is worth noting that it has not seriously taken off the anchor.About 100 basis points (about 1%).

Liquity protocol: pledge mechanism and Grant plan

As you already know, the agreement will charge all the borrowings and redemption fees generated (the loan fee is denominated at $ lusd, and the redemption fee is priced at $ ETH).Then, the agreement distributed these fees to the holder of the pledged $ LQty tokens in the original form. Therefore, the pledgers will get the rewards of $ LUSD and $ ETH according to their proportion in the pledge pool.

If you want to know how to pledge $ LQty tokens, you can watch the step -by -step tutorial “How To Stake Lqty” on YouTube.

In addition, the agreement also set up a Grant project called Liquifrns, which aims to promote the development of the liquity ecosystem.$ Lqty holders govern the plan, and they actually determine which proposal can be funded.

Liquity protocol: front -end operation analysis

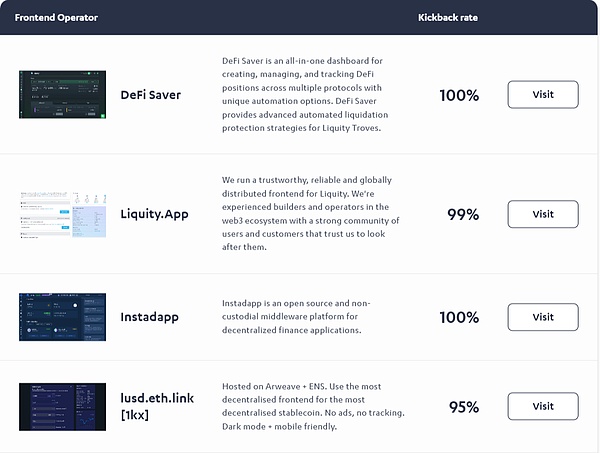

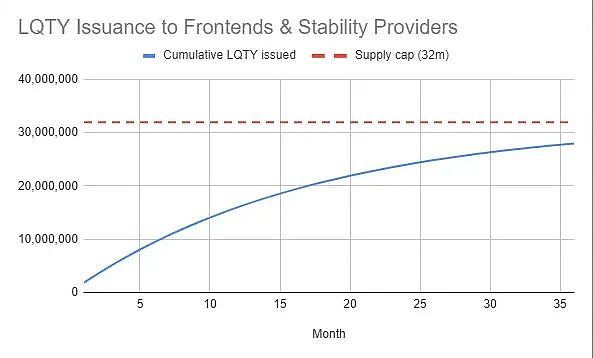

Another key difference between liquity and other decentralized applications (DAPPS) is that liquity is not running the front end.Instead, liquity outsourced this job to any interesting participants.

Remember that users who deposit in the stable pool will receive additional $ lqty incentives (tokens issuance)?Anyone who runs the front -end interface for Liquity can get a certain percentage of rewards from it; this ratio is determined by the “feedback rate”.For example, if the feedback rate of a front -end operator is 99%, through their front -end, every 100 $ LQty tokens obtain a stable pool user, the operator will get 1 $ LQty tokens.

>

The picture above shows some popular front -end operators.At present, a total of 64 front -end is running for the liquity protocol.What if the server of a country is closed?no problem.Government regulations prohibit these front -end operations in another country?No problem.This is the benefit of distributed the system to multiple front -end.

What is the best thing?Some front -end operators are very selfless and do not charge any fees (the feedback rate is 100%), which means that as a depositer of a stable pond, you can get the maximum $ lqty income.

The token distribution and unlocking mechanism of the liquity protocol

The $ LUSD tokens do not have the highest supply limit, because these tokens are issued based on the $ ETH mortgage, and the protocol does not set the “upper limit” of the $ ETH mortgage to cast $ LUSD.

However, the auxiliary tokens $ LQty has a fixed maximum supply, set at 100 million (100,000,000) tokens.This means that after the issuance of the $ LQty tokens, token holders will not face the risk of dilution.

The issuance of $ LQty tokens starts from the date of the agreement (April 5, 2021).

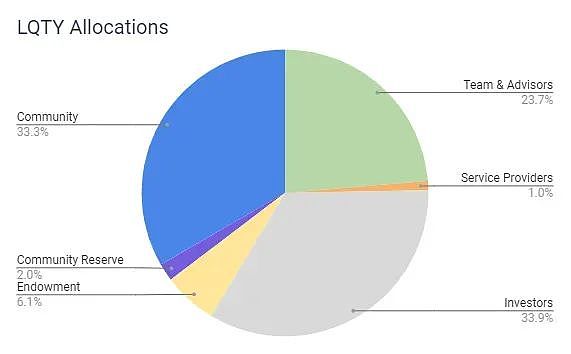

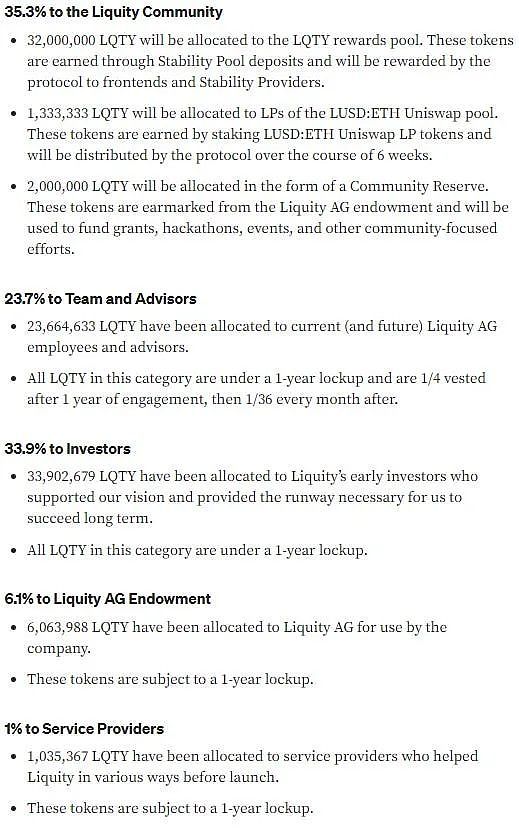

The distribution of the $ lqty tokens is displayed below.

>

>

It can be seen from the figure above that the $ 57.6% of the $ LQty supply is distributed to investors, teams and consultants (essentially inside personnel), which is much higher than industry standards.

6.1% of the supply was reserved to the Liquity AG Foundation (legal entity).This part of the $ lqty distribution is currently incorporated in the stable pool.The allocation and its income provides financial support for the previously mentioned LIQUIFRENS funding plan.Bleak

>

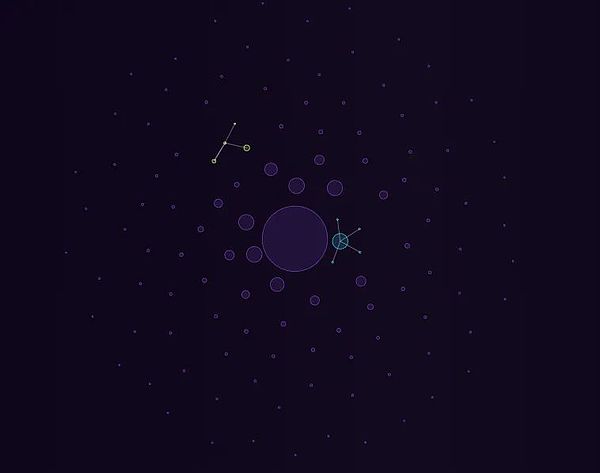

As shown in the BubbleMaps above (you can learn more about the platform and these bubbles), many external accounts (eoas, basically wallets) hold a large number of $ LQty tokens (giant whales), this is this, thisIncreases the possibility of market selling and price manipulation.One of the giant whales even held 10%of the $ LQty supply in circulation.

>

At present, the belonging and locking of the distribution of $ lqty is not very important, because as shown above, the amount of circulation of $ lqty is already very high, close to 92%.At present, only a small number of team unlocks and the tokens of the stable pool have not yet entered the market; these issuance will gradually end around March 2024, as shown in the figure below.

>

This is good news for the holders and pledges of $ lqty, because they will not be further diluted, and they also have a positive impact on the price trend, because the remaining $ lqty supply that has not entered the market is very small.

Liquity value creation and capture mechanism

For the entire DEFI field, Liquity has created value through its decentralization, resistance review, and strong toughness, while avoiding banking risks.When writing this article, liquity is the closest to the stablecoin items that are currently closest to truly decentralization and anti -review.

This feature has attracted the attention of some decentralized autonomous organizations (DAOS). For example, Olympusdao, which holds a large amount of reserves assets, has caused DAOs like Olympus to start using $ LUSD as credible asset support, as shown in the figure below.

>

In addition, Liquity has created value through a completely decentralized agreement, allowing DEFI users to open high capital efficiency and interest -free loan. These loans are guaranteed by the stabilization pool. At present, this may be the best clearing system in DEFI.Essence

These loans are seamless, instant, and no need to license. Users can use $ ETH mortgage borrowing to increase leverage or obtain an openness of other encrypted assets, participate in income agriculture, enjoy tax incentives (compared with the sale of $ ETH) and other opportunities.Essence

Liquity also creates value for those DEFI users who want to earn stable coins through stable pools -this forms a symbiotic relationship between the agreement and the user.The safety of all funds (mortgages).

>

LIquity’s $ LUSD stable coins play a role played by its DEFI ecosystem in Ethereum, Optimism, and Arbitrum, to further create value for users.At present, users can earn $ LUSD into the Yearn vault earning automatic compound profit income as a collateral on Angle, borrowing on AAVE and Silo, or amplifying the income on Gearbox, and there are many other applications.As $ LUSD is integrated into more DEFI platforms, more functions are constantly emerging.

Next talk about the value of the agreement.

As mentioned earlier, the agreement will charge a one -time loan and redemption fee, which are priced at $ LUSD and $ ETH, respectively, and the cost range is between 0.5% and 5% (usually close to the low range).The 100% of these costs are owned by the liquity protocol, and all are allocated to the $ LQty pledker, so the $ LQty tokens become the value of the agreement to capture the tokens.

>

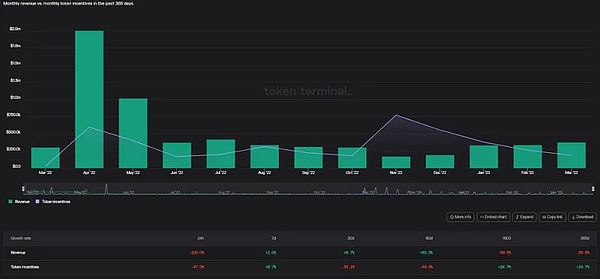

Liquity income vs token incentives

As shown in the figure above, even during the severe encrypted bear market in 2022, Liquity continued to generate income and assigned it to $ LQty pledges.In addition, with the opening of 2023, the income of the agreement has increased, which may be attributed to the recovery of the encrypted market we are currently undergoing.

However, the operation of the agreement is not smooth.It can be seen from the above figure that in the past year, the $ LQty tokens issued by the agreement per month mostly exceeded the income of the agreement, and the amount of issuance in some months has even reached 10 times the income.

Compared with other stable currency issuers, Liquity has not performed well in terms of efficiency, and relying on more tokens (incentives) has brought less income.

This also shows that in the long run, there may be potential problems in the sustainability of the agreement, because liquity cannot generate income without affecting the token holders, and issuing tokens will cause dilution effects and potential prices to fall.In addition, if the tokens are not issued, the agreement may not have considerable income at all (this will be further discussed at the end of the article).

>

MakerDao’s income vs tokens incentive

As shown in the figure above, in the past year, MakerDao has generated all income without issuing any $ MKR token incentives.

>

Abracadabra Money

Although Abracadabra is far less efficient than MakerDao, its income in most months is still higher than its tokens (incentives).

>

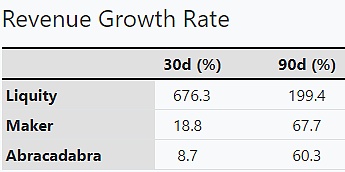

Data source: tokenterminal

However, as shown in the figure above, the income growth rate of liquity in the past 30 days and 90 days is the highest, reaching 676.3%and 199.4%, respectively. In contrast67.7%(90 days), while Abracadabra’s growth rate was 8.7%(30 days) and 60.3%(90 days).

Finally, it is necessary to understand that the income of liquity is not instantly, because the borrowing fee is only paid to the agreement when the user closes the borrowing position, which takes time.Only the redemption fee is received immediately.These two expenses (as mentioned earlier) are distributed in their original forms ($ ETH and $ LUSD) instead of being used to repurchase and distribute $ lqty to pledges.Can fully capture value.

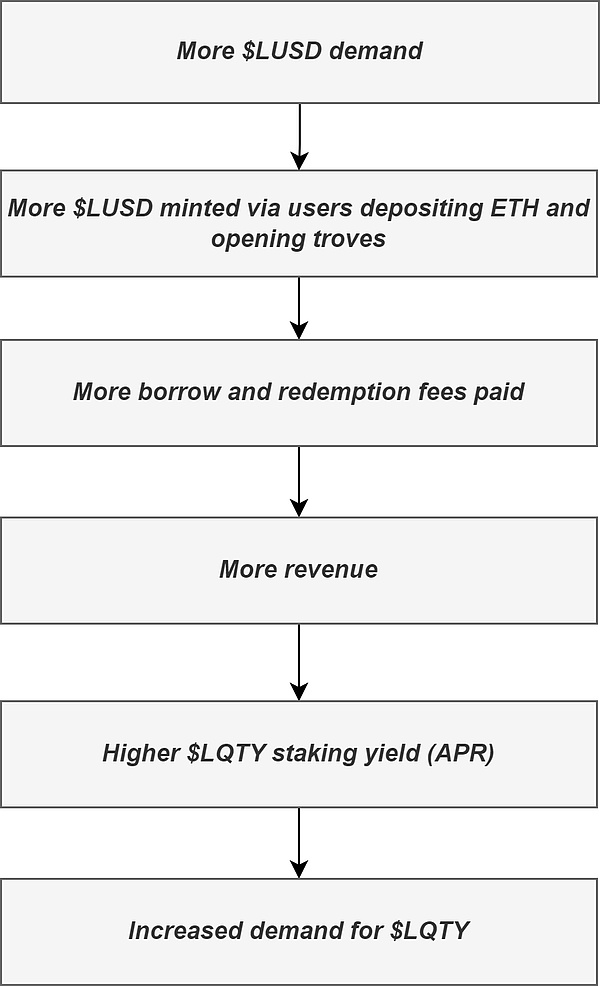

Analyze the demand of $ lqty driving factor

The demand for $ lqty is highly related to the demand for casting $ lusd.

>

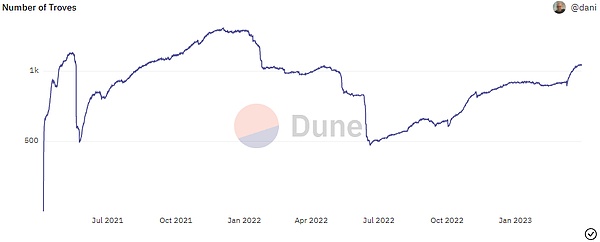

As shown in the figure below, the number of open borrowing positions has increased steadily since the middle of last year (2022).

>

However, this trend may be temporary, because some of the design options of the protocol (these designs make it anchored stable and decentralized) may hinder the scalability of the protocol, which will affect the demand of $ lqty.

Main problems include:

Given that we are in the recovery period of the encrypted market (“encrypted spring”), this stage is usually accompanied by extreme fluctuations, we can expect more liquidation events to bring higher stable pool returns, which will be transformed into more to moreThe demand for $ LUSD, then promotes the above -mentioned cycle to restart, resulting in an increase in demand for $ lqty.

>

At present, the annual average yield (APR) of pledge $ LQty is 7.33%, and the annualized return rate of the last month is 8%(APR), which is a considerable amount of income (compared to the pledge returns of other DEFI token to tokensRest), especially considering that these income comes from the income generated by the agreement.

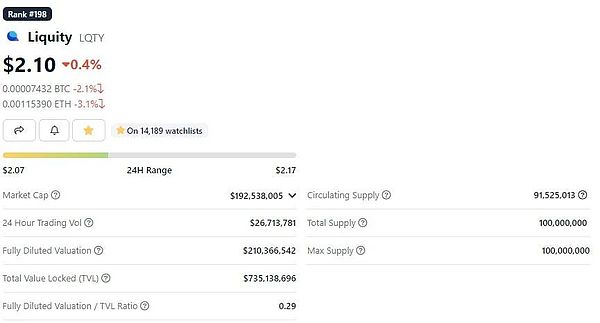

When writing this article, the market value of $ lqty is also 3.19 times lower than $ MKR, showing that its future growth space is huge.

In the end, although the impact is small, the governance of the Grant plan is also a demand driving factor for the $ LQty tokens.

About Liquity Agreement and the final thinking of its future

Overall, although Liquity has created an impressive product and realized the decentralization level that has not yet reached other stabilized currency agreements, due to the non -muttering of its contract, the agreement may gradually evolve into a only existenceCode library, because innovation or introduction of new products.

In my opinion, this is a survival risk of the liquity protocol, because projects such as Raft Finance are using liquity code (therefore called the “code library”), and developed products that can be expanded (mayThe decentralization level) continues to innovate and expand the product scope by expanding the types of mortgage products (such as the introduction of $ ETH and $ STETH) to surpass the ability of Liquity itself.The Liquity team does not intend to make these extensions and innovations.

In addition, stablecoins are still anchored to the US dollar (due to inflation), which appears with products like FRAX’s FPI (linked to CPI and anti -inflation).It may gradually disappear.

Insiders have also received a large amount of supply of $ lqty.Although this will not lead to centralization (because $ lqty is not governance tokens), it does make the $ LQTy circulation supply part of the minority giant whale wallets increase the risk of market selling and price manipulation.

Finally, there is a sustainable problem with $ lqty tokens, because the maximum use of $ LUSD is currently deposited in a stable pond, and when the tokens of $ lqty are exhausted, only the excess $ ETH mortgage of liquidation will be distributed to the distribution of the extra $ ETH mortgage to be distributed to the distribution of the liquidation.For those who stabilize the deposit, the reduction of income may suppress the demand for deposit, thereby reducing the demand of $ LUSD and $ lqty.

Personally, although I think the liquity protocol is a model of stabilizing currency decentralization and anchor stability, I am worried about its future because it may gradually be outdated.On the other hand, the underlying technology of Liquity will be improved and promoted in future DEFI, and the prospects of Defi seem to be very bright.

Original: Tokenomics 101: UndersTanding Liquity Protocol $ LUSD & Amp; $ lqty cover: ChatGPT

>