Author: Prathik Desai, Source: Token Dispatch, Compiled by: Saoirse

Seven years ago, Apple completed a financial feat that surpassed even the company’s best products.In April 2017, Apple launched the $5 billion Apple Park campus in Cupertino, California; a year later, in May 2018, the company announced a $100 billion stock buyback program—a 20 times the amount it invested in the 360-acre headquarters park called the “spacecraft.”This sends Apple’s core signal to the world: besides the iPhone, it has another “product” that is no less important than (or perhaps even surpasses) the iPhone.

This was the largest stock buyback program in the world at that time and part of Apple’s decade-long buyback boom—— During this period, Apple spent more than US$725 billion to buy back its own shares.Full six years later, in May 2024, the iPhone maker once again broke the record by announcing a $110 billion buyback program.This operation proves that Apple not only knows how to create scarcity in hardware devices, but also knows this well at the stock level operations.

Today, the cryptocurrency industry is adopting similar strategies, with faster pace and larger scale.

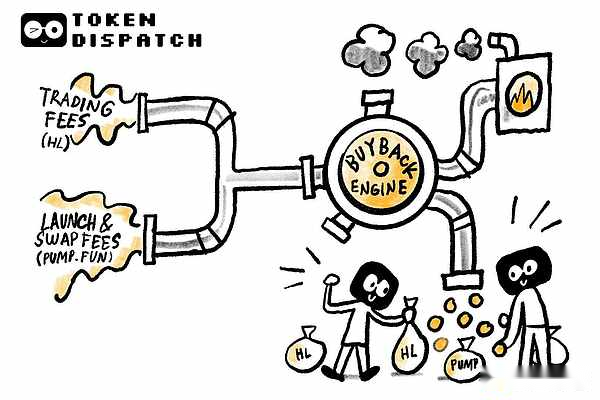

The two major “revenue engines” in the industry –Perpetual Futures Exchange Hyperliquid and Meme Coin Issuing Platform Pump.fun—— Almost every transaction fee income is being used to repurchase your own tokens.

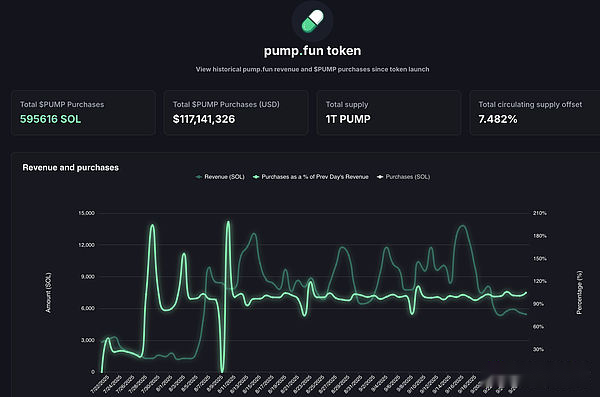

Hyperliquid set a record of $106 million in fees in August 2025, with more than 90% of which are used to buy back HYPE tokens on the open market.Meanwhile, Pump.fun’s daily income briefly exceeded Hyperliquid – on September 2025, the platform’s single-day income reached US$3.38 million.Where does this income eventually flow?The answer is 100% used to repurchase PUMP tokens.In fact, this repurchase model has lasted for more than two months.

This operation allows crypto tokens to gradually possess the attributes of “shareholder equity agents”——This is rare in the cryptocurrency field, after all, tokens in this field are often sold to investors whenever they have the opportunity.

The logic behind this is that cryptocurrency projects are trying to replicate the long-standing success path of Wall Street’s “dividend aristocrats” (such as Apple, Procter & Gamble, and Coca-Cola): These companies spend huge sums of money to return shareholders through stable cash dividends or stock buybacks..Take Apple as an example. In 2024, its stock repurchase amount reached US$104 billion, accounting for about 3%-4% of its market value at that time;The “circulation offset ratio” achieved by Hyperliquid through repurchase is as high as 9%.

Even by traditional stock market standards, such numbers are amazing; it is unprecedented in the cryptocurrency field.

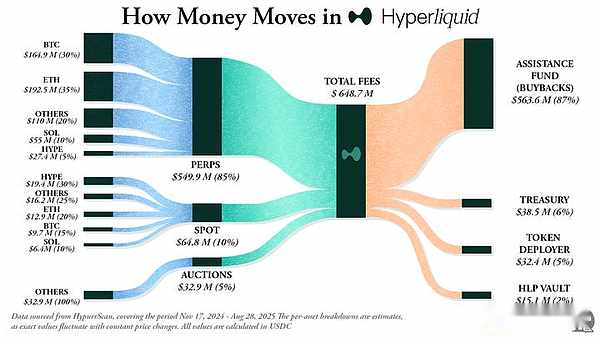

Hyperliquid has a clear positioning: it creates a decentralized perpetual futures exchange with the smooth experience of a centralized exchange (such as Binance), but it is completely based on the on-chain operation.The platform supports zero Gas fees, high leverage trading, and is a Layer1 with a perpetual contract as the core.As of mid-2025, its monthly trading volume has exceeded US$400 billion, accounting for approximately 70% of the DeFi perpetual contract market.

What really makes Hyperliquid stand out is its way of using its funds.

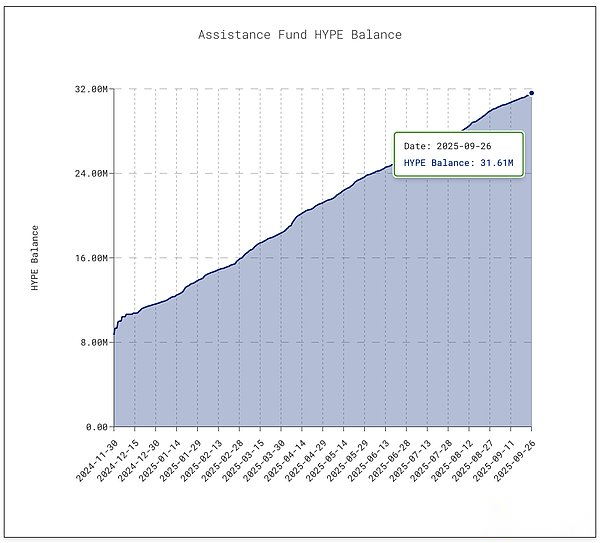

The platform transfers more than 90% of its fee income to the “Aid Fund” every day, and this fund will be used directly to purchase HYPE tokens on the open market.

As of the time of writing, the fund has held over 31.61 million HYPE tokens worth approximately US$1.4 billion — a 10-fold increase from 3 million in January 2025.

The buyback boom reduced the supply of HYPE circulation by about 9%, driving the token price to climb to its $60 peak in mid-September 2025.

at the same time,Pump.fun has reduced PUMP token circulation by about 7.5% through repos.

With extremely low handling fees, this platform transforms the “Meme coin boom” into a sustainable business model: anyone can issue tokens on the platform and build a “binding curve” to allow market popularity to ferment freely.This platform, which was originally just a “joking tool”, has now become a “production factory” of speculative assets.

But hidden dangers also exist.

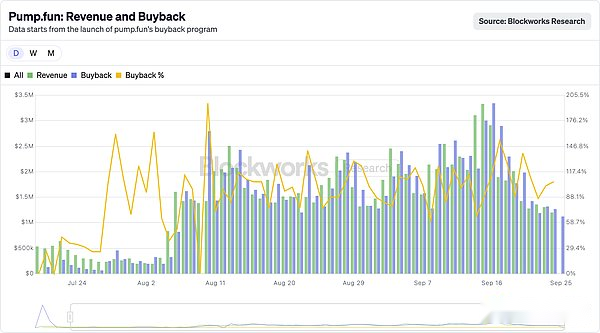

Pump.fun’s revenue is obviously cyclical – because its revenue is directly linked to the popularity of Meme coins issuance..In July 2025, the platform’s revenue fell to US$17.11 million, the lowest level since April 2024, and the repurchase scale also shrank; by August, monthly revenue rebounded to more than US$41.05 million.

However,“Sustainability” remains an open question.When the “Meme Season” cools down (which has happened in the past and will inevitably happen in the future), token repurchases will also shrink.Even more serious, the platform is facing a lawsuit worth up to $5.5 billion, with plaintiffs accusing its business of “similar to illegal gambling.”

The core that supports Hyperliquid and Pump.fun is their willingness to “give back the income to the community.”

Apple once returned nearly 90% of its profits to shareholders through repurchases and dividends in some years, but these decisions were mostly phased “batch announcements”; while Hyperliquid and Pump.fun continued to give back almost 100% of their revenue to token holders every day – this model is continuous.

certainly,There are still essential differences between the two: cash dividends are “earnings” and although taxes are required, they are highly stable; while repurchases are at most just “price support tools” – once income declines, or the amount of token unlocks far exceeds the amount of repurchases, the repurchases will be invalid..Hyperliquid is facing the upcoming “unlocking shock”, while Pump.fun needs to deal with the risk of “Meme coin popularity transfer”.Compared with Johnson & Johnson’s record of “continuously increasing dividends in 63 years”, or Apple’s long-term and stable repurchase strategy,The operation of these two encryption platforms is more like “walking tightropes at high altitude”.

But perhaps, this is no longer easy in the crypto industry.

Cryptocurrencies are still in a mature stage of development and have not yet formed a stable business model, but they have shown an astonishing “development speed”.The repurchase strategy happens to have the elements that drive the industry to accelerate: flexibility, tax efficiency, deflationary attributes – these characteristics are highly consistent with the “speculation-driven” crypto market.Up to now, this strategy has built two completely different projects into the industry’s top “revenue machines”.

Whether this model can last for a long time is still uncertain.But it’s obvious that itFor the first time, cryptocurrencies have been freed from the label of “casino chips”, closer to “company stocks that can generate returns for holders” – the speed of returns may even put Apple in a stressful way.

I think there is a deeper inspiration behind this: Apple realized long before the emergence of cryptocurrencies, that it sells not only iPhones, but also its own stocks.Since 2012, Apple has accumulated nearly $1 trillion in repurchase spending (more than GDP in most countries), and stock circulation has decreased by more than 40%.

Today, Apple’s market value remains above $3.8 trillion, partly because it regards stocks as “a product that needs to be marketed, polished, and maintained scarcity.”Apple does not need to raise funds through additional stock issuances – its assets and liabilities are abundant, so the stock itself becomes a “product” and shareholders become “customers”.

This logic is gradually permeating the cryptocurrency field.

The success of Hyperliquid and Pump.fun is that instead of reinvesting or hoarding the cash generated by their business, they convert it into “the purchasing power that drives up the demand for their own tokens.”

This has also changed investors’ perception of crypto assets.

iPhone sales are important, but investors who are optimistic about Apple know that the stock has another “engine”:Scarcity.Nowadays, traders have begun to develop similar perceptions about HYPE and PUMP tokens – there is a clear commitment behind these assets in their eyes: every consumption or transaction based on the token has a more than 95% chance of being converted into “market repurchase and destruction.”

But Apple’s case also reveals another side:The strength of repurchase will always depend on the strength of the cash flow behind it..What happens if revenues decline?When iPhone and MacBook sales slowed, Apple’s strong balance sheet allowed it to fulfill its buyback commitments by issuing bonds;And Hyperliquid and Pump.fun do not have such “cushioning”——Once transaction volume shrinks, repurchases will also stagnate.More importantly, Apple can turn to dividends, service businesses or new products to deal with the crisis, and these encryption protocols currently have no “alternative solutions”.

For cryptocurrencies, there is also the risk of “token dilution”.

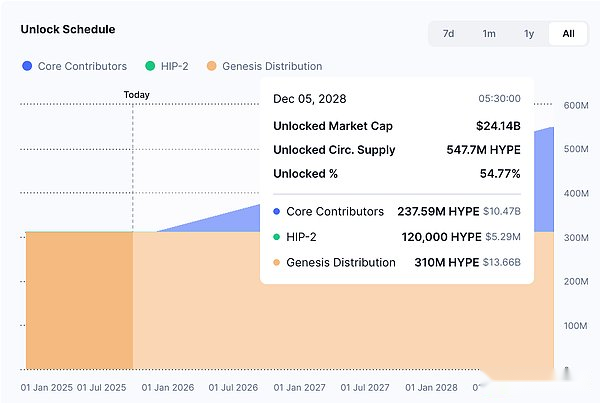

Apple doesn’t need to worry about “200 million new shares flowing into the market overnight,” but Hyperliquid faces this problem: Starting in November 2025, nearly $12 billion worth of HYPE tokens will be unlocked to internal staff, which is far beyond the daily repurchase volume.

Apple can independently control stock circulation, but the encryption protocol is subject to the token unlocking schedule that was “dead in black and white” many years ago.

Even so, investors still see the value and are eager to participate.Apple’s strategy is obvious, especially for those familiar with its decades of development — Apple has cultivated shareholder loyalty by converting stocks into “financial products.”Today, Hyperliquid and Pump.fun are trying to replicate this path in the encryption field, but the pace is faster, the momentum is stronger, and the risks are higher.