Author: Alex Weseley Source: Artemis Research Translation: Shan Ouba, Bit Chain Vision

Key points

-

Although so far, the existing $ billions of dollars of tokens and real financial assets are deployed on the public chain, but there are still many tasks to do it at the intersection of law and technology to rewrite the financial system on the public chain.Pipeline.

-

History tells us that the financial system has not provided support for the globalization and digital levels required today, but has become a wall garden built on outdated technology.Public blockchain has unique advantages and can improve these problems in a global and credible way.

-

Despite the challenge, Artemis believes that stocks, government bonds and other financial assets will be transferred to public blockchain because they are more efficient.As applications and users gather on the same underlying platform that supports programming and interoperable assets, this will release the network effect.

introduce

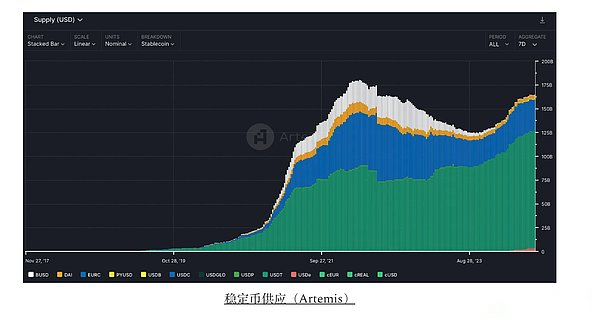

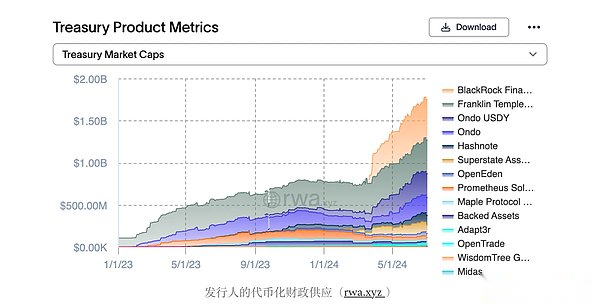

At present, the legal currency of token has exceeded 160 billion US dollars, the total amount of tokenization of U.S. Treasury and goods has reached US $ 2 billion, and the tokenization of real -world financial assets on public blockchain has begun.

>

>

Over the years, the financial industry has been curious about the potential of blockchain technology to subvert the traditional financial market infrastructure.The benefits of commitments include improving transparency, non -degeneration, accelerating settlement time, increasing capital efficiency, and reducing operating costs.This promise has contributed to the development of new financial instruments on the blockchain, such as innovative trading mechanisms, lending agreements and stablecoins.At present, decentralized finance (DEFI) has more than $ 100 billion in lock -up assets, indicating that people have a strong interest and investment in this field.Supporters of blockchain technology believe that its impact will exceed the creation of encrypted assets such as Bitcoin and Ethereum.They foresee that in the future, the global, constant and distributed ledger will strengthen the existing financial system, and the existing financial system is often limited by centralization and isolated ledger.The core of this vision is tokenization, even if the smart contract program called token is used to represent the process of traditional assets on the blockchain.

To understand the potential of this transformation, this article will first study the development and operation of traditional financial market infrastructure from the perspective of securities clearing and settlement.This review will include the review of historical development and the analysis of the current practice, and provide the necessary background for how to promote the next stage of financial innovation for the exploring the section of the blockchain.The Wall Street Documentation crisis in the 1960s will provide a key case study, highlighting the vulnerability and inefficiency in the existing system.This historical event will laid the foundation for the main participants of liquidation and settlement and the inherent challenges of the current delivery and payment (DVP) process.At the end of this article, it discusses how to provide unique solutions for these challenges without license, and may release greater value and efficiency in the global financial system.

Wall Street’s document work crisis and DTCC

Today’s financial system has been formed under high system pressure for decades.An event that is often underestimated explained why the settlement system operated so, that is, the document work crisis in the late 1960s, George S. Geis’s “Historical Background of Stock Settlement and Blockchain”The book describes it in detail.Looking back on the development of securities liquidation and settlement, it is essential to understand the current financial system and recognize the importance of tokenization.

Today, people can easily purchase securities through online agents.Of course, the situation is not always the case.From a historical point of view, stocks are issued to individuals who hold physical certificates representing stock ownership.In order to exchange stocks, the physical certificate must be transferred from the seller to the buyer.This includes handling the certificate to the transfer agent. The transfer agent will cancel the old certificate and issue a new certificate in the name of the buyer.Once the new certificate is delivered to the buyer, the payment payment is delivered to the seller, and the transaction can be considered to be settled.In the 19th and 20th centuries, more and more agents represented investors holding stock certificates, enabling them to clearly clear and settle their transactions with other brokers.This process is still mainly manual, and brokerage companies usually use 33 different documents to perform and record single securities transactions (SECs).Although it can be managed at the beginning, as the transaction volume increases, this process has become more and more cumbersome.In the 1960s, stock trading activities increased sharply, making physical delivery securities between brokers a task that was impossible.In the early 1960s, the system designed to handle 3 million transactions per day cannot handle 13 million shares of transaction volume (SEC) in the late 1960s.In order to allow the background office to complete the settlement time, the New York Stock Exchange shortened the trading day, extended the settlement time to T+5, and eventually prohibited on Wednesday.

>

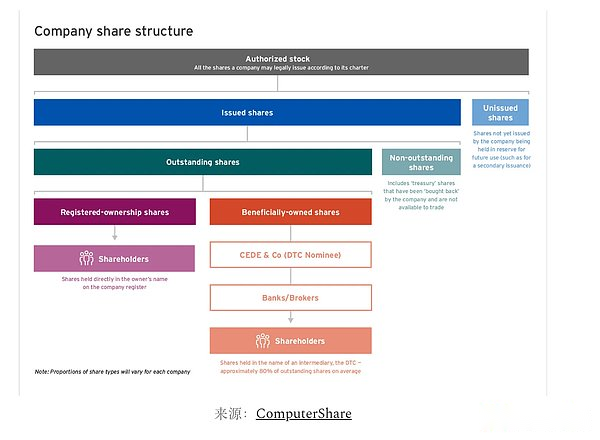

Since the establishment of the Central Certificate Services (CCS) in 1964, the New York Stock Exchange has been working hard to find a solution.CCS 的目标是成为所有股票证书的中央存管处,这意味着它将代表其成员(主要是经纪人)持有所有股票,而最终投资者则被授予以经纪人分类账中的账簿记录为Benefiting ownership of the representative.The progress of CCS was hindered by a series of regulations. Until 1969, all fifty states amended the law, approved the CCS concentrated certificate and transferred stock ownership.All stocks are transferred to CCS so that they can be stored in the so -called “fixed swap -can be available”.Because CCS holds all stocks in a fixed form, it records the balance of its members and agents in the internal accounts, and the member agent records the balance of the final investors they represent in their internal divisions.At present, stock settlement can be completed through account records instead of physical delivery.In 1973, CCS was renamed the depository trust company (“DTC”), and all stock certificates were transferred in the name of the subsidiary “CEDE & AMP; Co”.Today, DTC has become the name owner of almost all company stocks through CEDE.DTC itself is a subsidiary of the Storage Trust Trust and Settlement Company (DTCC). Other subsidiaries of DTCC include the National Securities Settlement Corporation (NSCC).DTC and NSCC are the two most important part of today’s securities systems.

The emergence of these intermediaries has changed the nature of stock ownership.In the past, shareholders held physical certificates; now, this ownership is represented by the book records in the book chain.With the development of the financial system, the increase in complexity has led to the emergence of more custodians and intermediaries. Each custodian and intermediary agencies must maintain their ownership records through account book records.The figure below simplifies the level of ownership:

>

Explanation of securities digitalization

Since the crisis of the document work, DTCC has stopped the practice of holding physical stocks in its vault. Therefore, the stock has changed from “fixing” to completely “non -physical”. Now almost all stocks are presented in the form of electronic account records.Nowadays, most securities are issued in non -physical form.As of 2020, DTCC estimates that 98% of securities have been non -lively, and the remaining 2% represents securities worth nearly 780 billion US dollars.

Introduction to traditional financial market infrastructure (FMI) entry

By understanding the financial market infrastructure (FMI), you can obtain a deeper structural background knowledge required to understand the potential of the blockchain, and the blockchain is preparing to subvert these entities.The financial market infrastructure is an important institution that constitutes the pillar of our financial system.The International Clearance Bank (BIS) and the International Securities Regulatory Commission (iOSCO) detailed the role of financial market infrastructure in the “Financial Market Infrastructure Principles” (PFMI).BIS and iOSCO’s key financial market infrastructure defined by the smooth operation of the global financial system includes::

-

Payment system (PS):Responsible for the system that safely transfer funds between participants.

-

Example: In the United States, Fedwire is a major interbank radio exchange system that provides real -time summary (RTGS) services.Globally, the SWIFT system has system importance because it provides a network for international capital transfer, but it is just a support system -it does not hold accounts or settlement payment.

-

Central Securities Stocking Institution (CSD):Its responsibilities are entities that provide securities accounts, central storage services, asset services, and play an important role in helping ensure the integrity of securities issuance.

-

For example: in the United States, it is DTC.In Europe, it is Euroclear or Clearstream.

-

Securities Settlement System (SSS):The securities settlement system allows securities to transfer and settlement through bookkeeping in accordance with a set of pre -determined multilateral rules.Such systems allow securities for free or paid.

-

For example: in the United States, it is DTC.In Europe, it is Euroclear or Clearstream.

-

Central opponent (CCP):Become a entity of the buyer of each seller and the seller of each buyer to ensure the performance of the unsuitable contract.CCP is achieved through debt renewal, and one contract between the buyer and the seller will be split into two contracts: one is between the buyer and the CCP, and the other is between the seller and the CCP, thereby absorbing the risk of the opponent.

-

For example: in the United States, National Securities Listing Company (NSCC).

-

Trading repository (TR):Maintain the entity of the transaction data set electronic records.

-

Example: DTCC operates global trading repository in North America, Europe and Asia.Mainly used for derivatives transactions.

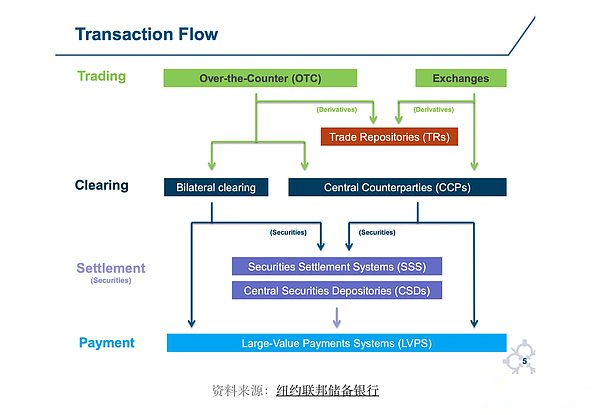

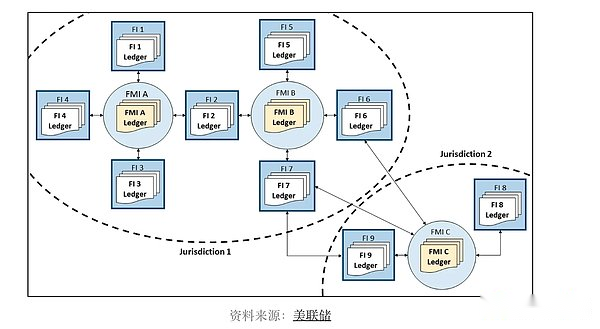

In the entire life cycle of affairs, the interaction of these systems is as follows:

>

Transfer usually uses FMI as the central hub and uses wheel spoke models. Among them, wheel spokes are other financial institutions, such as banks and brokerage self -business.These financial institutions may interact with multiple FMIs in different markets and jurisdictions, as shown in the figure below.

>

The isolation of this ledger means that the entity must trust each other to maintain the integrity of the ledger, communication and verification.There are some entities, processes and regulations, purely to promote this trust.The more complicated and global the financial system, the more exogenous power is needed to strengthen the trust and cooperation between financial institutions and financial market intermediaries.

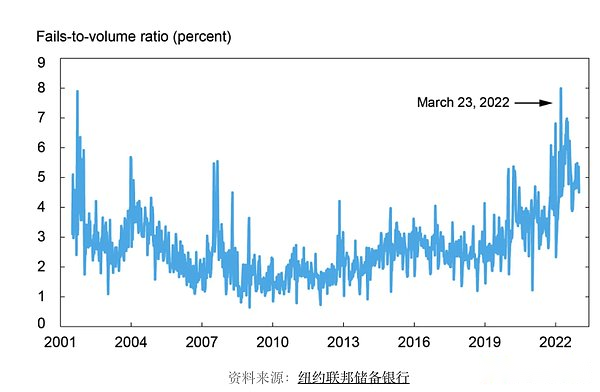

The following data on the failure of the company’s securities settlement highlight the current low efficiency of the financial market. The failure of these company securities settlement has recently increased to more than 5% of the total transaction volume.

>

Additional data provided by DTCC’s daily settlement of U.S. Treasury bonds shows that a transaction failure of 20 billion to 50 billion US dollars per day has failed.This accounts for about 1%of the DTCC liquidation transaction, and DTCC liquidates about $ 4 trillion in Treasury bonds (DTCC) per day.

>

The failure of settlement will have serious consequences, as securities buyers may have used it as a collateral in another transaction.This subsequent transaction will also face the situation that cannot be delivered, which may trigger the Domino card effect.

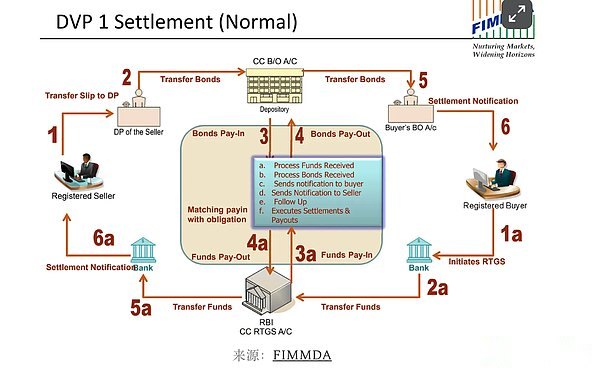

Securities settlement: payment delivery

The payment and settlement system committee said: “So far, the largest financial risk in securities liquidation and settlement occurs during the settlement process.”Securities can be transferred for free or paid transfer.Some markets adopt a mechanism, that is, securities transfer will only occur only when the corresponding capital transfer is successful -this mechanism is called “payment of payment” (DVP).Today, the delivery of securities and the payment of funds are carried out on two fundamental different tracks through different systems.One is performed through the payment system, and the other is through the securities settlement system, that is, the system mentioned in the previous section.In the United States, payment may be performed through Fedwire or ACH, and international payment may be used to communicate with SWIFT and settled through a bank network.On the other hand, the delivery of securities is carried out through the securities settlement system and the central securities depository office (such as DTC).These are different tracks and different ledger, which need to strengthen communication and trust between different intermediaries.

>

Blockchain and atom settlement in DVP

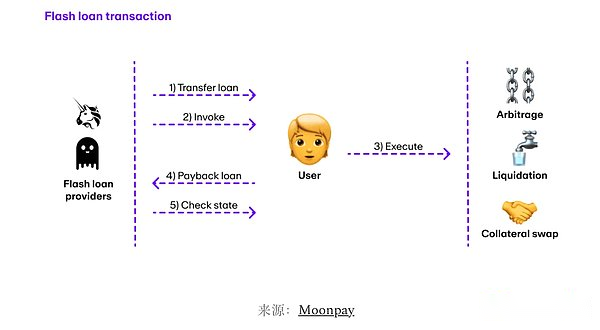

Due to the unique attribute of blockchain transactions, blockchain can reduce certain risks in the payment system, such as principal settlement risk.Blockchain trading itself can be composed of several different steps.For example, deliver securities and complete payment.The special feature of blockchain transactions is that all the steps of the transaction are either successful or all failed.This characteristic is called atomic, which makes Lightning Loan and other mechanisms possible. In a single transaction, users can borrow unsecured funds, as long as they return in the same transaction.This is possible, because if the user fails to repay the loan, transactions and loans will not be recorded.In the blockchain, the payment of goods can be completed through the atoms of smart contracts and transactions.This may reduce the risk of principal settlement, because one step of the transaction is unsuccessful, causing potential losses in all aspects.Blockchain has key characteristics that enable them to eliminate the role played by traditional securities settlement systems and payment systems in the payment settlement settlement.

>

Why is it a blockchain without permission?

In order to make the blockchain open and without license, anyone must be able to participate in verification transactions, generate blocks, and reach a consensus on the standard state of the ledger.In addition, anyone should be able to download the state of the blockchain and verify the effectiveness of all transactions.Examples of public blockchain include Bitcoin, Ethereum, and Solana. Anyone who connects the Internet can access the ledger and interact with it.The blockchain that meets this standard and large and decentralized is essentially a credible neutral global settlement layer.In other words, they are an unjust environment for transaction execution, verification and settlement.The transaction can be carried out between the use of smart contracts between the parties that do not know each other, so as to achieve the implementation of no trust and no intermediary, thereby incomplete changes to the global shared ledger.Although no entity can restrict individual access to the blockchain, a single application based on blockchain -based construction can implement permissions, such as white lists from KYC and compliance -related purposes.

Public blockchain can improve the efficiency of background operations, and improve capital efficiency by using the programmability of smart contracts and atomicity of blockchain transactions.These functions can also be implemented by licensed blockchain.So far, many enterprises and governments have explored blockchain through private and licensed blockchain.This means that network verifications must pass the KYC inspection to be allowed to join the network and run the consensus mechanism, transaction verification, and block production software of the ledger.The implementation of the license blockchain for institutions is not better than using private shared ledger between institutions.If the underlying technology is completely controlled by Morgan Chase, the banking alliance, and even the government, the financial system will no longer be non -prejudice and credible neutrality.Since 2016, enterprises and government agencies have been studying distributed ledger technology. Except for pilot projects and testing environments, we have not seen any major implementation of these systems.In the view of A16Z’s Chris Dixon, this part is because the blockchain allows developers to write a code to make a strong commitment, and companies do not need to make too much promises to themselves.In addition, the blockchain aims to imageLargeLike multiplayer games, not just multiplayer games like corporate blockchain.

Select the Standardization Case Study

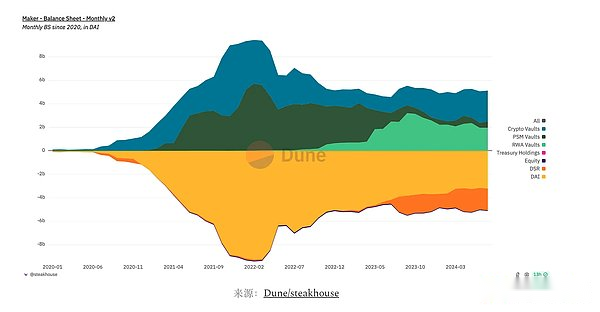

MakerThe use of real -world assets (RWA) has been added to guarantee the issuance of DAI.In the past, DAI was mainly supported by encrypted assets and stable currency.Today, a large part of the MAKER balance sheet (about 40%) is stored in the RWA vault investing in the US Treasury bonds, bringing considerable income to the agreement.These RWA vaults are managed by various entities, including BlockTower and Huntington Valley Bank.

>

BelideThe US dollar agency liquidity fund (BUIDL) was released on the Ethereum public chain in March 2024.Bellaide’s fund is invested in U.S. Treasury bonds, and investors are expressed in the fund ownership of the fund through ERC-20 tokens.In order to invest in the fund and issue additional shares, investors must first pass the Securitize through KYC.You can currently pay the shares through telegram or USDC.Although there are options for stable currency issuance and redemption shares, the actual settlement of the transaction will wait until the fund is successfully sold in the traditional financial market (under redemption).In addition, the transfer agent Securitize maintains a chain transaction and ownership registration book, which replaces the blockchain as a legal register.This shows that before the US Treasury bond itself can be issued on the chain, from a legal perspective, there are still many jobs to do so that they can make atom settlement through USDC payment.

ONDO FinanceIt is a fintech startup in the field of tokenization.They provide a variety of products, including OUSG and USDY, which are issued on multiple public blockchains in the form of token.Both products are secretly invested in U.S. Treasury bonds and provide income for holders.OUSG is available in the United States, but it is only for qualified buyers, and USDY is sold for anyone outside the United States (and restricted areas).An interesting point about USDY casting is that when the user wants to cast a USDY, they can remit USD or send USDC.For USDC deposits, when ONDO exchanges USDC to US dollars and remit the capital to its bank account, the transfer is regarded as “complete”.This is because of legal and accounting purpose, clearly stating that the lack of clear digital asset supervision framework hinders innovation.

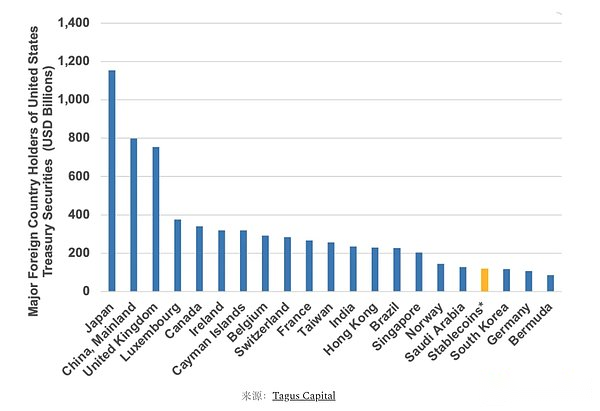

Stabilizing currency is the most successful case of the tokenization so far.More than 165 billion U.S. dollars, the legal currency exists in the form of stable currency, and the monthly transaction volume reaches trillions.Stable coins are becoming an increasingly important part of the financial market.The stable coin issuer is the 18th largest US debt holder in the world.

>

in conclusion

The financial system has gone through many growth troubles, including the crisis of documents, the global financial crisis, and even the GameStop incident.During these periods, the financial system was under pressure testing and shaped it into what it is today: a large number of intermediaries and isolation systems, relying on slow processes and regulations to establish trust and transactions.Public blockchain provides a better alternative solution through the establishment of anti -examination, credible neutrality, and programmable ledger.However, the blockchain is not perfect.Due to their distributed characteristics, they have technical characteristics, such as block restructuring, fork and delay related issues.To understand the settlement risks related to the public blockchain, see Natasha Vasan’s “Solving the Unexposed Issues”.In addition, although the security of smart contracts has improved, smart contracts are often invaded by hackers or through social engineering.During the congestion period, the blockchain will become expensive, and the ability to deal with the scale of scale required by the global financial system has not been displayed.Finally, in order to achieve the extensive labeling of real world assets, compliance and regulatory obstacles need to be overcome.

With the proper legal framework and the full improvement of underlying technology, the assets of assets on public blockchain are expected to release the network effect with the collection of assets, applications and users.As more and more assets, applications and users are introduced into the chain, the platform itself (blockchain) will become more valuable, which is more attractive to the builders, issuers and users, thereby forming a virtuous circle.The use of global sharing and credible neutrality will make new applications appear in the field of consumers and financial fields.Today, thousands of entrepreneurs, developers, and policy makers are building this public infrastructure to overcome obstacles and strive to achieve a more interconnected, efficient and fair financial system.

Future research issues

-

How does smart contract language affect tokenization?Compared with EVM -based smart contracts, is the MOVE object data model more suitable for financial assets securely on the chain?

-

To what extent finance should we keep and transparent?Zero knowledge proves how to achieve multi -chain/cross rollup financial infrastructure while protecting privacy when necessary?Is this better than using the license chain?

-

In the world where real financial assets exist on the chain, how should we look at the blockchain interoperability agreement?What is their role and how should they build?