Author: Alex xu, Lawrence Lee

introduction

As one of the oldest tracks in the encryption field, the Defi track is not satisfactory in this round of bull market. The overall increase of the Defi sector in the past year (41.3%) not only lags far behind the average level (91%), Even behind Ethereum (75.8%).

>

Data Source: Artemis

And if you only look at the data in 2024, the performance of the DEFI sector is also difficult to say, and the overall declines 11.2%.

>

Data Source: Artemis

However, in my opinion, in the background of BTC’s once -setting of the new high cottage coins, the DEFI sector, especially the head projects, may usher in the best layout time since its birth.

Through this article, the author hopes to clarify the view of the current DEFI value through the discussion of the following issues:

-

The reasons for the large -scale losing BTC and Ethereum in this round of cottage

-

Why is it the best time to pay attention to DEFI?

-

Some of the DEFI projects worthy of attention, and their value sources and risks

This article does not include DEFI with investment value in the market. The DEFI project mentioned in the article is only used as an example analysis, not investment advice.

This article is the phased thinking of the author as of the time when the publication. It may change in the future, and the viewpoints have strong subjectivity. There may also be errors in facts, data, and reasoning logic. Welcome the criticism and further discussion of interbank and readers.

The following is part of the text.

The mystery of the price of cottage is sharply sliding down

In the author’s opinion, the price performance of the cottage in this round is not as good as expected. There are three main reasons for the encryption industry:

-

Insufficient growth of demand: lack of attractive new business models, most of the tracks of the tracks of PMF (Product Market Fit)

-

The supply side of excessive growth: further improvement of industry infrastructure, further reduction of entrepreneurial thresholds, excessive issuance of new projects

-

The tide of lifting the ban continues: the tokens of the low -circulation and high FDV project continue to unlock, bringing a heavy throwing pressure

Let’s look at the background of these three reasons.

Insufficient growth in demand: The first round of bull market lacks innovative narrative

In the article “Preparing for the Bull Market Shenglang, I am thinking about the stage of the bull market, I think about the stage of this round of the period” mentioned in the article mentioned that the lack of commercial innovation and narrative of this round of bull market as the 21 -year DEFI and 17 -year ICO, so strategy, so strategyIt should be over -equipped with BTC and ETH (benefiting incremental funds brought by ETF) to control the configuration ratio of cottage.

As of now, this view is very correct.

Without a new business story, the inflow of entrepreneurs, industrial investment, users, and funds has been greatly reduced, and it is more important to suppress the overall expectations of investors to the development of the industry.When the market has not seen on the market for a long time, such as “DEFI will devour traditional finance”, “ICO is a new innovation and financing paradigm” and “NFT subversion content industry ecology”, investors will naturally vote on new stories with their feet.Local, such as AI.

Of course, the author does not support too pessimistic arguments.Although this round has not yet seen attractive innovation, the infrastructure is constantly improving:

-

The cost of block space has dropped sharply, and the L1 to L2 is the same

-

Cross -chain communication solutions are gradually complete and have a rich optional list

-

User -friendly wallet experience upgrades, such as Coinbase’s smart wallet supports selfless keys to quickly create and restore, directly call CEX balance, no need to recharge GAS, etc., allowing users to approach Web2’s product experience

-

The Actions and Blinks functions launched by Solana can publish the interaction on the chain with Solana to any common Internet environment and further shorten the user’s use path

The above infrastructure is like hydropower coal and highway in the real world. They are not the result of innovation, but they are the soil of innovation.

Supply -side growth: the number of projects exceeds + high market value tokens continuously unlock

In fact, from a different perspective, although the price of many cottage coins has reached a new year, the total market value of Congzhaner has not fallen miserable compared to BTC.

>

data: trading view, 2024.6.25

So far, the price of BTC has fallen by about 18.4% from high, and the total market value of Congzhaner (TRADING VIEW system is displayed in TOTAL3, indicating that the total encrypted market value deducts the value after BTC and ETH) only fell -25.5%Essence

>

data: trading view, 2024.6.25

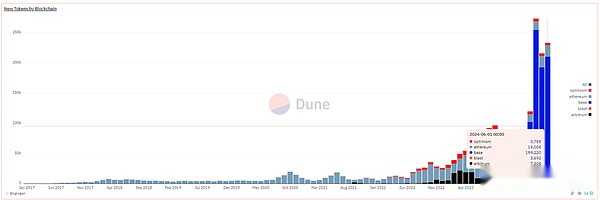

The limited decline in the total market value of the cottage is based on the large increase in the total amount and market value of the new Yamada currency. From the figure below, we can intuitively see that the increase in the number of tokens in this round of bull markets is the fastest year in history.Essence

>

new tokens by blockchain, data source: https: //dune.com/queries/3729319/6272382

It should be noted that the above data only counts the EVM chain’s tokens issuance data, and more than 90% of them are issued on the base chain. In fact, more new token is contributed by Solana.Most of the currency are Meme.

Among them, the high market value of the new market value in this round of bull markets is:

-

Dogwifhat: 2.04 billion

-

Brett: 166 billion

-

Notcoin: 1.61 billion

-

DOG • Go • THE • Moon: 630 million

-

Mog coin: 560 million million

-

POPCAT: 470 million

-

Maga: 410 million

In addition to Meme, a large number of infrastructure tokens are also or will be issued this year, such as:

The second layer of networks are:

-

Starknet: 930 million circulation, FDV7.17 billion

-

ZKSYNC: The market value of circulation is 610 million, FDV3.51 billion

-

Manta Network: The market value of 330 million, FDV10 billion

-

Taiko:; The market value of circulation is 120 million, FDV19 million

-

BLAST: The market value of circulation is 480 million, FDV2.81 billion

Cross -chain communication services include:

-

Wormhole: The market value of circulation is 630 million, FDV3.48 billion

-

Layer0: The market value of circulation is 680 million, FDV2.73 billion

-

ZetAChain: The market value of circulation is 230 million, FDV1.78 billion

-

Omni Network: The market value of 147 million, FDV1.42 billion

The chain service is:

-

Altlayer: The market value of circulation is 290 million, FDV1.87 billion

-

Dymension: The market value of 300 million, FDV1.59 billion

-

SAGA: The market value of circulation is 140 million, FDV1.5 billion

* The above market value data sources are coingecko, with 2024.6.28

In addition, there are a large number of tokens that have already been on a large number of unlocks. Their common features are low circulation ratio, high FDV, and early institutional wheel financing, and the cost of tokens of the institutional wheel is very low.

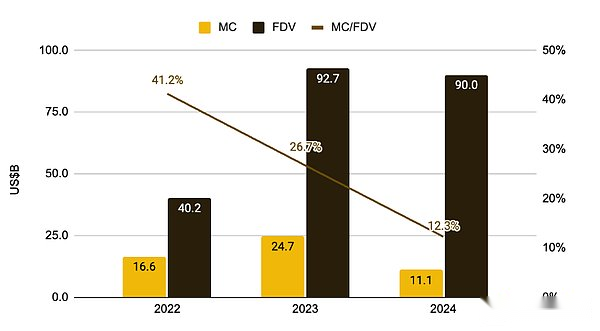

And the weakness of this round of demand and narrative, the excess issuance of superimposed asset supply side is the first time in the encryption cycle, although the project party tries to further reduce the tokens during the listing (from 41.2% in 2022 to 12.3%) To maintain valuation and gradually sell them to second -level investors, but the resonance of the two finally led to the overall downward movement of these encrypted project valuation hub. In 2024Few sections maintain positive returns.

>

The ratio of the ratio of Singapore Coin MC and FDV, picture source: "Low Float & amp; High FDV: How did we get here?", Binance Research

However, in the author’s opinion, the collapse of this high -market VC currency valuation center is a normal response to various encrypted strange phenomena in the market:

-

Create a ghost city Rollup in batches, only TVL and robots but no users

-

By renovating noun financing, it actually provides a similar solution, such as a large number of cross -chain communication services

-

Facing hot spots rather than actual user needs starting a business, such as a large number of AI+Web3 projects

-

Can’t find or simply don’t find a profit model, tokens have no value capture

The decline of these cottage valuation centers is the result of the market self -repair, the benign process of breaking the bubble, and self -rescue behavior of voting with funds and clearing the market.

The actual situation is that most VC coins are not worthless. They are just too expensive, and the market finally allows them to return to their due position.

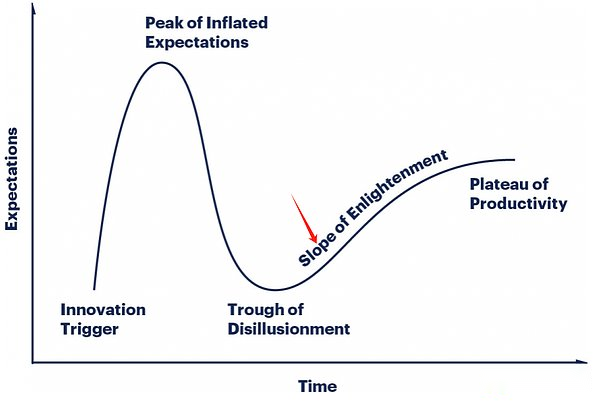

Follow DEFI at the time: PMF products, get out of the bubble period

Since 2020, DEFI has officially become a category in the cottage cluster.In the first half of 2021, the most DEFI project was the DEFI project in the TOP100 list of the encrypted market value. At that time, the category was dazzling, and he vowed to redesign all the existing business models in traditional finance on the chain.

In that year, Defi was the infrastructure of the public chain. DEX, borrowing, stabilization, and derivatives were 4 sets of sets of hands that must be made after the new public chain.

However, with the super hair of homogeneous projects, a large number of hacking attacks (adventure self -theft), the TVL of the TVL of the Ponzi model relying on the left foot has collapsed rapidly, and the spiral token price of the spiral ascension is zero.

Entering the bull market cycle, the price performance of most of the DEFI projects that has survived so far is not satisfactory, and fewer and fewer investment in the DEFI field is getting less and less.At the beginning of any round of bull market, investors’ favorite is the new story of this round of cycle, and DEFI does not belong to this category.

But this is also the case. The DEFI project coming out of the bubble has begun to appear more attractive than other alcohol currency projects. Specifically:

Business side: Have mature business models and profit models, head projects have moat

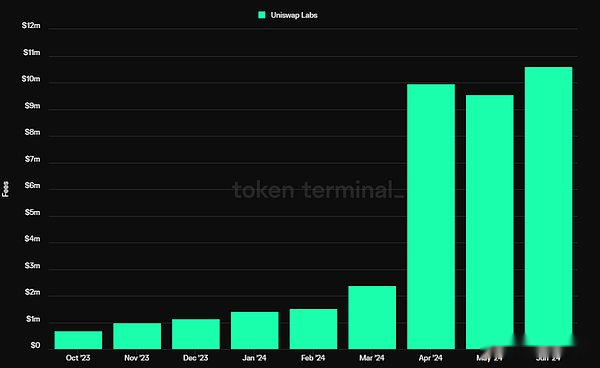

DEX and derivatives earn trading fees, loan charging interest rate difference income, stablecoin items to charge stable fees (interest), and Staking services to charge pledge service fees. The profit model is clear.The user needs of the head projects of each track are organic, basically through the user subsidy stage, and some projects still achieve positive cash flow after deducting tokens.

>

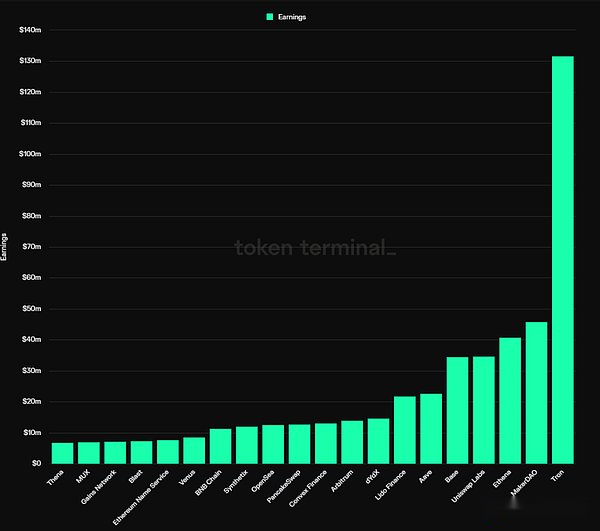

The profit ranking of encryption projects, Source: tokenterminal

According to statistics from Tokentermial, among the top 20 protocols with the highest profit in 2024, 12 are DEFI projects. The classification is:

-

Stablecoin: MakerDao, Ethena

-

Borrowing: AAVE, Venus

-

Pledge service: lido

-

DEX: Uniswap Labs, Pancakeswap, THANA (income from the front -end handling fee)

-

Derivatives: DYDX, Synthetix, MUX

-

Income aggregation: Convex Finance

The moats of these projects are diverse, some of which are derived from the multilateral or bilateral network effects of the service, some come from user habits and brands, and some stem from special ecological resources.However, from the results, the head projects of Defi showed some commonality in their respective tracks: market share tended to stabilize, later competitors decreased, and had certain service pricing power.

As for the moat of the specific DEFI project, we will detail the project part of the third section.

Supply: low emissions, high circulation ratio, small scale to be resolved to the ban tokens

In the previous section, we mentioned that one of the main reasons for the continuous collapse of the cottage valuation in this round is that a large number of projects based on high -valuation -based high emissions, and the current negative expectations brought by the income of tokens to enter the market.

Due to the early launch time, most of the DEFI projects on the head have passed the peak period of token emissions. The tokens of the institution have basically been released, and the future pressure is extremely low.For example, AAVE’s current token circulation ratio is 91%, the LIDO token circulation ratio is 89%, Uniswap token circulation ratio is 75.3%, MakerDao circulation ratio is 95%, and the circulation ratio of Convex is 81.9%.

This aspect shows that the small pressure in the future also means that no matter who wants to obtain the control of these projects, basically can only purchase tokens from the market.

Valuation: Market attention and business data are deviated, and the valuation level falls into the historic low range

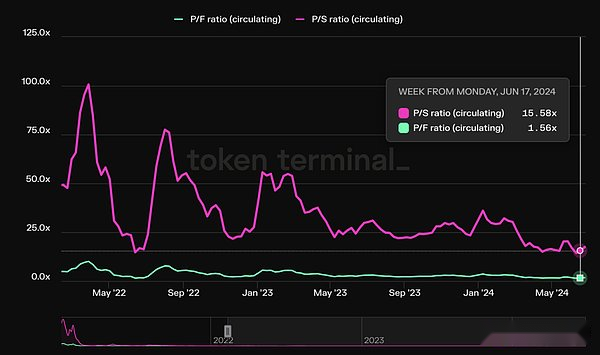

Compared to new concepts such as Meme, AI, DEPIN, ROLLUP service, etc., Defi has always been very thin in this round of bull market, and the price performance is mediocre, but on the other handThe profit level has continued to grow, forming the departure of prices and business, which is specifically reflected in the valuation level of some head DEFI.

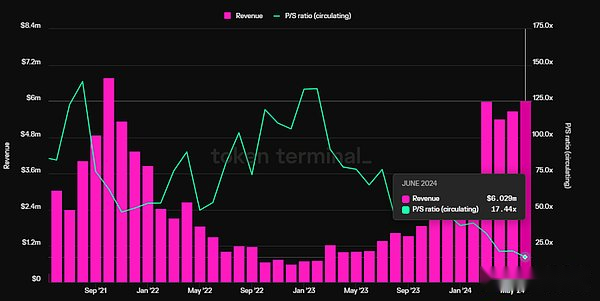

Taking the lending agreement AAVE as an example, in its quarterly income (referring to net income, non -overall agreement charges) has surpassed the high point of the previous cycle and set a record high, its PS (circulating market value/ annualized income) createdIt has a record low, currently only 17.4 times.

>

Data Source: Tokenterminal

Policy: The FIT21 Act is conducive to the DEFI industry compliance and may cause potential mergers and acquisitions

FIT21, that is, the “Financial Innovation and Technology for The 21st Center Act” (Financial Innovation and Technology for The 21st Century Act “.Leading position in the digital asset market.The bill was proposed in May 23rd that it was approved in the House of Representatives on May 22 this year.Because the bill clarifies the rules of regulatory framework and market participants, after the bill is officially passed, whether it is entrepreneurial or traditional finance to invest in DEFI projects, it will become more convenient.Considering that traditional financial institutions represented by Bellaide have embraced encrypted assets in recent years (promoting the listing of ETFs and issuing national debt assets on Ethereum), DEFI is a high probability that they will be the focus of the area in the next few years.In the end, mergers and acquisitions may be one of the most convenient options, and any related signs, even if it is only the intention of mergers and acquisitions, will trigger the value of the DEFI leading project.

Next, the author will take some DEFI projects as an example to analyze its business situation, moat, and valuation.

Considering that there are many DEFI projects, the author will analyze projects with good business development, wider moat, and more attractive valuation.

Defacious DEFI project

1. Borrowing: AAVE

AAVE is one of the oldest DEFI projects in history. After completing financing in 2017, it completed the transition from point -to -point borrowing (at that time the project was also called Lend).Compound of the head project of the same track, whether it is a market share or a market value, is the first place in the loan track.

AAVE’s main business model is to earn the interest rate difference of borrowing.In addition, AAVE launched its own stable currency GHO last year, and GHO will create interest income for AAVE.Of course, operating GHO also means new cost item, such as promotion costs, liquidity incentives, and so on.

1.1 business situation

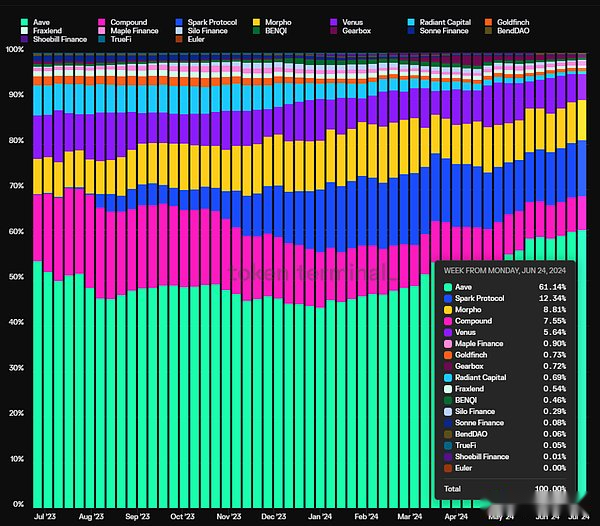

For the lending agreement, the most critical indicator is the scale of active loans, which is the main source of revenue of borrowing projects.

The figure below shows the market share of AAVE’s active loan scale in the past year. In the past six months, AAVE’s active loan share has continued to increase, and it has reached 61.1%.Repeat statistics on the loan of the income optimization module on AAVE and Compound.

>

Data Source: Tokenterminal

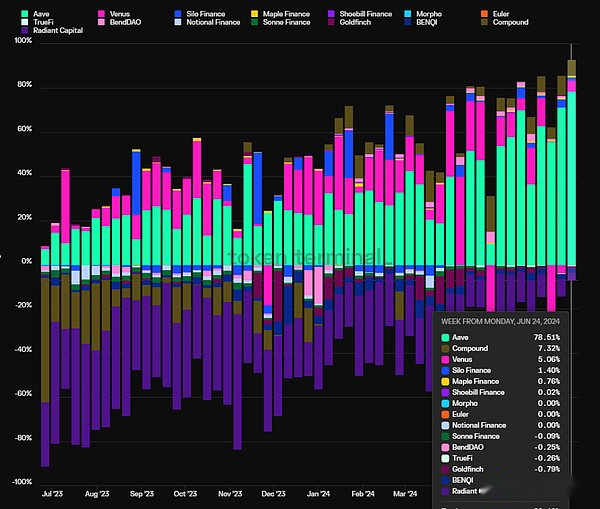

Another key indicator is the profitability of the agreement, the level of profit.Profit in this article = Agreement Revenue -tokens incentives.As can be seen from the figure below, the profit profit of the AAVE agreement has been opened a lot from other borrowing agreements, and it has early rid of the Ponzi model that stimulates the business through the token (Radiant in the figure below, which is represented by the purple part).

>

Data Source: Tokenterminal

1.2 moat

AAVE’s moat mainly has the following 4 points:

1. Continuous accumulation of security credit: Most new lending agreements will have a security accident within one year of launch. Since the operation of AAVE, there has been no security accident at the smart contract level.And a platform’s risk -free and stable operation of security credit is often the most priority element of DEFI users when choosing a borrowing platform, especially giant whale users with a large amount of funds. For example, Sun Yuchen is a long -term user of AAVE.

2. Bilateral network effects: Like many Internet platforms, Defi borrowing is a typical bilateral market. Deposits and borrowing users are both ends of supply and demand. The increase in unilateral size of deposit and loan will stimulate the business volume of the other side.Competitors are more difficult to catch up.In addition, the more abundant liquidity of the platform, the smoother the liquidity of both parties to the deposit and loan, and the more likely it is favored by large funding users. Such users in turn stimulate the growth of the platform business.

3. Excellent DAO management level: The AAVE protocol has fully implemented DAO -based management. Compared with the team’s centralized management model, DAO -based management has more full information disclosure, and community discussions with more sufficient decision -making.In addition, AAVE DAO’s community is active in a group of highly governance professional institutions, including head VC, college blockchain club, city merchant, risk management service provider, third -party development team, financial consulting team, etc.It is rich and diverse, and the participation of governance is relatively positive.From the perspective of the project’s operation results, AAVE, as the later partner of the borrowing service of the pond, has better considered growth and security in product development and asset expansion, and realized the transcendence of the elder brother Compound. In this process, DAO’s DAOGovernance plays a key role.

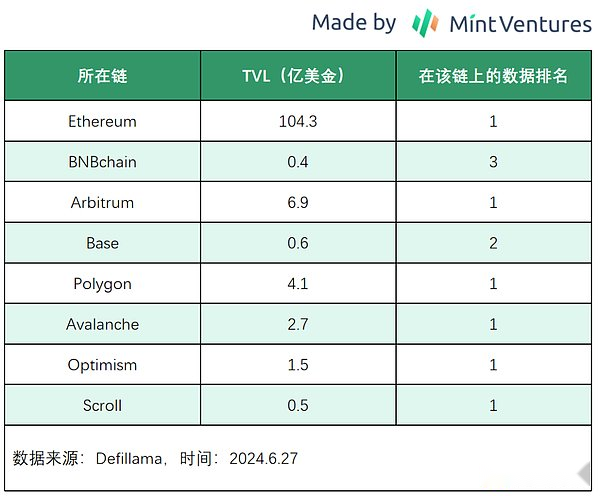

4. Multi -chain ecosystem occupies: AAVE is deployed almost all EVM L1 \ L2, and TVL is basically in the head in each chain. In the V4 version under the development of AAVE, multi -chain liquidity will be achievedThe advantages of cross -chain liquidity will be more obvious.See the details below:

>

In addition to the EVM public chain, AAVE is also evaluating Solana and APTOS, which will be possible to deploy on the network in the future.

1.3 valuation level

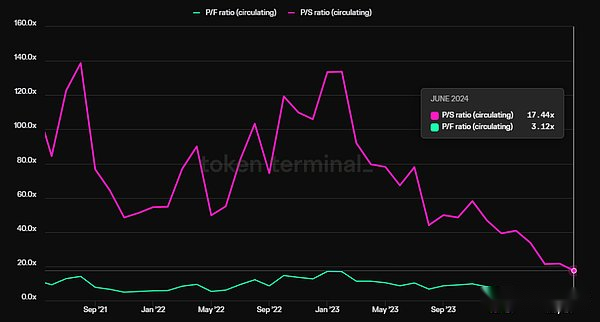

According to the tokensminal data, AAVE has continued to rise due to the continuous recovery of agreement costs and income, and the currency price is still hovering at a low level.New low, PS bit 17.44 times, PF is 3.1 times.

>

Data Source: Tokenterminal

1.4 risk and challenge

Although AAVE’s share in the borrowing market continues to rise, a new competitor is worth noting that it is the modular borrowing platform of Morpho Blue.MORPHO BLUE provides a modular agreement for third parties that intend to build a loan market. You can freely choose different mortgage, borrowing assets, prophecy machines and risk parameters to build a custom borrowing market.

This modular method allows more market participants to enter the field of lending and start to provide loan services. For example, AAVE’s once risk service provider GAUNLET, would rather interrupt the service relationship with AAVE, and launch its own loan market in Morpho BlueEssence

>

Image source: https://app.morpho.org/? Network = mainnet

>

Data Source: https://morpho.blockanalitica.com/

Morpho Blue has grown rapidly for more than half a year, and has become the fourth largest borrowing platform for TVL second only to AAVE, Spark (MakerDao) and Compound.

Its growth rate on Base is even faster. Less than two months before the launch, TVL has reached 27 million US dollars, and AAVE’s TVL in Base is about 59 million.

>

Data Source: https://morpho.blockanalitica.com/

2.Dexs: Uniswap & amp; raydium

Uniswap and Raydium are divided into EVM ecology and Solana ecosystem of Ethereum camp.UNISWAP launched the V1 version deployed on the Ethereum main network as early as 2018, but what really made Uniswap fire was the V2 version launched in May 2020.Raydium was launched in Solana in 2021.

The reason why we must recommend two different targets on the DEXS track is because they are divided into the two ecosystems with the largest number of web3 users, that isSolana ecology, and the two projects have their own advantages and problems.Next we interpret these two projects.

2.1 UNISWAP

2.1.1 Business status

Since the V2 version has been launched, the UNISWAP has been almost the largest DEX in Ethereum main network and most EVM chain transaction volume.In terms of business, we mainly pay attention to two indicators, namely transaction volume and handling fees.

The figure below is the monthly monthly transaction volume share of the UNISWAP V2 version.

>

Data Source: Tokenterminal

Since the V2 version in May 2020, UNISWAP’s market share has bottomed out from 78.4%in August 2020 to 36.8%at the peak period of DEXS War in November 2021, and has risen to 56.7%now. It can be said that experience experienceAfter the cruel competition test, he has established a foothold.

>

Data Source: Tokenterminal

UNISWAP’s market share in the transaction fee also showed this trend. Its market share was bottomed in November 2021 (36.7%), and then rose all the way, currently 57.6%.

What is even more valuable is that Uniswap except for a few months in just a few months of 2020 (Ethereum main network) and at the end of 2022 (OP main network), token subsidies for tokens.Most DEXS has not stopped subsidies for liquidity so far.

The figure below shows the proportion of the amount of incentives at the end of the major DEXS. You can see that Sushiswap, Curve, Pancakeswap, and the current VE (3,3) project on the Base Aerodrome, they were the projects with the largest subsidy amount during the same period, butNone of the market share higher than Uniswap.

>

Data Source: Tokenterminal

However, UNISWAP’s most criticized point is that although there is no token inspirational expenditure, the tokens are also valuable to capture, and the agreement has not opened the cost switch so far.

However, at the end of February 2024, Erin Koen, a developer of UNISWAP and the head of the foundation governance, issued a proposal in the community to upgrade the Uniswap protocol, so that the charging mechanism can reward the UNI token holder who has authorized and custody its token to token.The proposal caused a lot of discussions at the community level. It was originally scheduled to conduct formal voting on May 31. However, it is still delayed and has not yet been formally voted.Nevertheless, the Uniswap protocol has taken the first step in the work of opening fees and empowerment UNI tokens. The contract to be upgraded has completed development and auditing. In the visible future, Uniswap will have a separate agreement income.

In addition, UNISWAP LABS actually opened up charges for users who used the UNISWAP official webpage and Uniswap wallets as early as October 2023. The ratio was 0.15%of the transaction amount., USDT, DAI, WBTC, Ageur, GUSD, LUSD, EUROC, XSGD, but stable currency transactions and WETH \ ETH swaps are not charged.

And just the charging of the front end of Uniswap has made Uniswap Labs one of the highest income teams in the entire Web3 field.

It can be imagined that when the cost of the Uniswap protocol layer was opened, the annualized cost of UNISWAP in the first half of 2024 was about 1.13 billion US dollars.Billion dollars.

After the subsequent Uniswap X and V4 of Uniswap launched in the second half of this year, it is expected to further expand its market share of its transaction volume and transaction costs.

2.1.2 moat

UNISWAP’s moat mainly comes from the following three aspects:

1. User’s habit: At the beginning of the front -end charging of UNISWAP last year, many people thought that this was not a good idea. Soon users’ trading behavior would switch from the front end of Uniswap to a transaction polymercost.However, since the front -end opening charging, the revenue from the front end has always been rising, and its growth rate even exceeds the cost growth rate of the entire UNISWAP agreement.

>

Data Source: Tokenterminal

This data strongly illustrates the power of UNISWAP’s user habits. A large number of users do not care about the expenditure of this 0.15% transaction fee, but choose to maintain their own trading habits.

2. Bilateral network effects: UNISWAP, as a trading platform is a typical bilateral market, for the “bilateral” understanding of its business model, one angle is the two sides of the market are buyers (Trader) and the marketor (LP). Where is it?The more more the transaction, the more active, the more LP is inclined to provide liquidity to strengthen each other.On the other angle on the bilateral side is: one on one side of the market is a trader, and on the other hand is the project party deploying the initial liquidity of the token.In order to make your tokens more easily found and traded by the public, the project party tends to be the initial liquidity of DEX deployment in more users and more well -known to the public, instead of choosing a relatively unpopular second and third -line DEX. The project party’s this oneThe behavior has further strengthened the user’s habitual behavior in the transaction -the new token is prioritized to the UNISWAP transactions, which forms the mutual enhancement of the bilateral markets of “project parties” and “trading users”.

3. Multi -chain deployment: Similar to AAVE, UNISWAP is quite active in the expansion of multi -chain. The EVM chain with a large transaction volume can be seen in the UNISWAP figure, and its transaction volume is basically the top of the DEX ranking of the chain.

>

Follow -up, with the support of multi -chain transactions after Uniswap X lasted, Uniswap’s comprehensive advantages in multi -chain liquidity will be further enlarged.

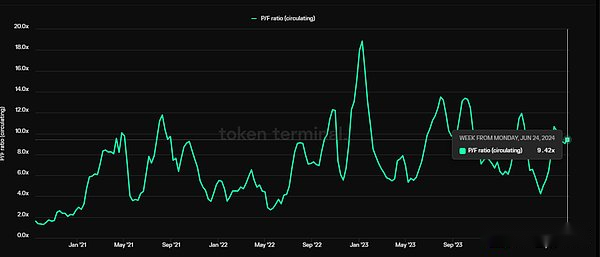

2.1.3 valuation

We take the ratio of the market value of Uniswap’s circulation and its annualized costs, that is, PF as the main valuation standard, and we will find that the current UNI token valuation is in a highly percentage range in history. This may be due to its upcoming coming.The cost switch upgrade has been reflected at the market value level in advance.

>

Data Source: Tokenterminal

In terms of market value, UNISWAP currently has a market value of nearly 6 billion, and the full diluted market value is as high as 9.3 billion, which is also not low.

2.1.4 risk and challenge

Policy risk: In April this year, Uniswap received Wells Notice from SEC, which means that subsequent SECs will take law enforcement operations on Uniswap.Of course, with the gradual advancement of the FIT21 Act, the Defi projects such as the subsequent Uniswap are expected to obtain a more transparent and expected regulatory framework. However, considering that the voting and landing of the bill will still beStress the business and token prices of the project.

Ecological location: DEXS is the basic layer of liquidity. Previously, it was a trading polymer. Trading polymers such as 1Inch, COWSWAP, and Paraswap can provide users with full -chain fluidity comparison and find the optimal transaction path. This model to a certain extent to a certain extentThe upstream DEX has the ability to charge and pricing the user’s transaction behavior.With the development of the industry, the wallet of the built -in trading function has become a higher upstream infrastructure. In the future, with the introduction of the intent mode, the DEX as the source of the underlying liquidity will become the one that users cannot perceive.Further dissolve users’ habits directly using Uniswap to enter a complete “price -comparison mode”.It is also realizing this that Uniswap is trying to march towards the ecological upstream, such as vigorously promoting the Uniswap wallet and release of the aggregation layer of the Uniswap X into the transaction to improve its ecological location.

2.2 raydium

2.2.1 Business status

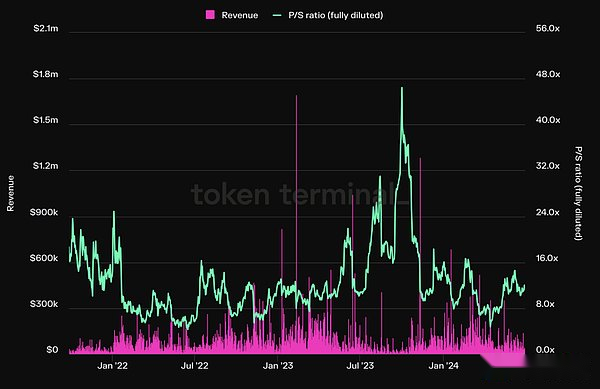

We will also focus on the transaction volume and fees of Raydium, and a better point of Raydium than Uniswap is that it starts the agreement charges very early and has a good cash flow. Thereforeitem.

Let’s look at the Raydium’s transaction volume. Thanks to the prosperity of the ecology of Solana in this round, its transaction volume began to take off from October last year. Its March transaction volume once reached 47.5 billion US dollars, about 52.7%of the UNISWAP transaction value in the month.

>

Data Source: FlipSide

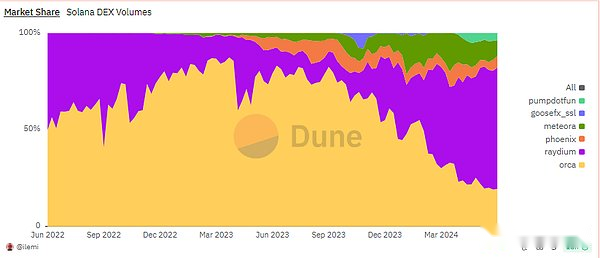

From the perspective of market share, Raydium’s transaction volume on the Solana chain has been increasing since September last year, currently accounting for 62.8%of Solana’s ecological transaction volume.Location.

>

Data Source: Dune

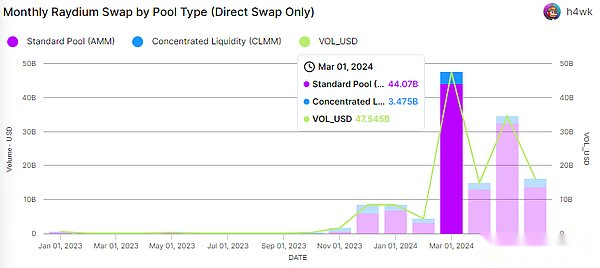

The reason why Raydium’s market share is less than 10% from the low tide period to more than 60% of currently, mainly due to the MEME trend that has continued to this round of the bull market cycle.Raydium uses two ways of liquidity pools. It is divided into standard AMM and CPMM. The former is similar to UNI V2, which is uniformly distributed in liquidity, suitable for high volatility assets.Lleapability provider can customize the interval of liquidity, which is more flexible, but more complicated.

And Raydium’s competitors ORCA choose a concentrated liquid pool model that fully embraces the UNI V3 type.For the MEME project party who needs to produce a large number of production and configure liquidity in large quantities, Raydium’s standard AMM model is more suitable, so Raydium has become the preferred liquid place for the MEME tokens.

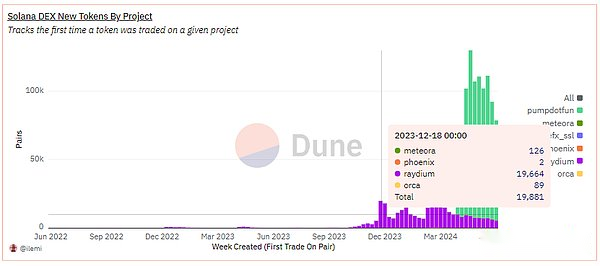

As the biggest MEME incubation base in this round of bull market, Solana has been born every hundred or even tens of thousands of new Memes since November this year. MEME is also the core driving factor of the ecological prosperity of Solana in this round, becoming the burning agent of Raydium’s take -off.

>

Data Source: Dune

As can be seen from the above figure, in December 23, Raydium’s new token number was 19664 a week, while the ORCA was only 89 in the same period.Although theoretically, the centralized liquidity mechanism of ORCA can also choose to “fully configure” liquidity to obtain similar effects to traditional AMM, but this is still not as simple and direct as the Raydium standard pool.

In fact, Raydium’s transaction volume data also proves this. The transaction amount from the standard pool accounted for 94.3%. Most of these transactions were contributed by the MEME tokens.

In addition, Raydium, as a bilateral market, is the same as UNISWAP and serves the bilateral market of the project party and users. The more retail investors on Raydium, the more the MEME project party is inclined to arrange the initial liquidity in Raydium.And service users (such as various types of dog TG BOT) choose Raydium to trade, this self -enhancement cycle further opened the gap between Raydium and ORCA.

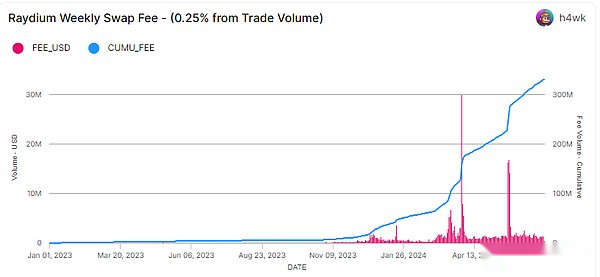

From the perspective of the transaction fee, the transaction fee created by Raydium in the first half of 2024 was about 300 million US dollars. This value was 9.3 times the Raydium transaction fee in 2023.

>

Data Source: FlipSide

The Raydium standard AMM pool feed rate is 0.25% of the transaction volume, of which 0.22% are attributed to LP and 0.03% are used to repurchase the tokens Ray.The cost of CPMM can be freely set to 1%, 0.25%, 0.05%, and 0.01%. LP will obtain 84% of the transaction fee, 12% of the remaining 16% are used to repurchase RAY, and 4% are deposited into the state treasury.

>

Data Source: FlipSide

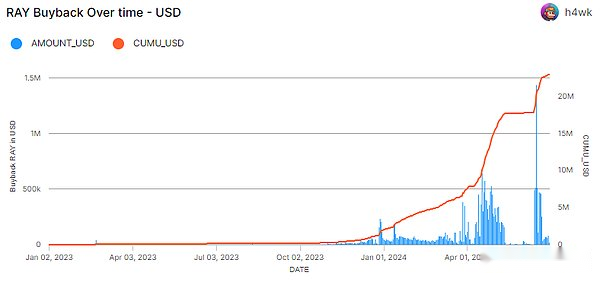

Raydium’s agreement revenue used to repurchase Ray in the first half of 2024 was about $ 20.98 million. This value was 10.5 times the amount of repurchase of the RAY agreement in 2023.

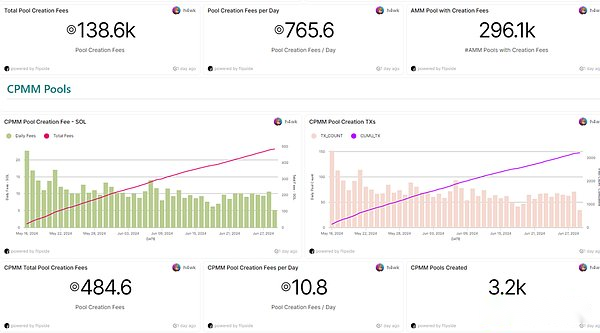

In addition to the income of the handling fee part, Raydium will also charge the newly created pool. At present, the CPMM pool charging is 0.15 SOL based on the AMM standard pool.(Based on the price of 6.30 SOL, it is about 108,000 US dollars. However, this part of the cost is not returned to the treasury, nor is it used for Ray’s repurchase. Instead, it is used for the development and maintenance of the agreement. It can be understood as team income.

>

Data Source: FlipSide

Like most DEX, Raydium still has incentives for DEX liquidity. Although the author has not found data that continues to track its incentive amount, we can from the official liquidity interface to the incentives of the current incentive liquidity pool that is currently incentive liquidity poolValue is generally statistics.

>

According to current Raydium’s incentives for liquidity, there are about 48,000 US dollars per week in motivation expenditure, which is mainly based on the RAY token.), The agreement is in a state of positive cash flow.

2.2.2 moat

Raydium is the largest market transaction volume on Solana. Compared with competing products, its main advantage is from the current bilateral network effects, similar to Uniswap.The project party and the trading users have enhanced each other.This network effect is particularly prominent in the MEME asset category.

2.2.3 valuation

Due to the lack of historical data 23 years ago, the author only compared Raydium’s valuation data in the first half of this year with the valuation data in 2023.

>

With the rise of transactions this year, although RAY’s currency price has risen, compared to the valuation of the valuation significantly compared with last year, its PF and UNISWAP DEX are also at a lower level.

2.2.4 Risk and challenge

Although Raydium’s transaction volume and revenue performed strongly in the past half of the year, its future development still has many uncertainty and challenges. Specifically:

Ecological location: Raydium is also facing the problem of ecological positions like UNISWAP, and in the Solana ecology, the polymer represented by Jupiter has a greater influence, and its transaction volume far exceeds Raydium (June Jupiter’s total transaction volume is 282100 million, Raydium is 16.8 billion).In addition, the MEME platform represented by Pump.fun has gradually replaced the scene of the project initiated by Raydium. More Memes start through pump.fun instead of Raydium, although the two parties are currently cooperative relationships.The Pump.fun platform gradually replaced the influence of Radyium on the project side, and Jupiter also surpassed Raydium’s influence on traders on the user side.If this situation is not improved for a long time, if the ecological upstream Pump.fun or Jupiter built DEX or turns to competitors, it will have a significant impact on Raydium.

Market wind direction change: Before the this round of SOLANA scratched MEME whirlwind, the market share of ORCA transaction volume was 7 times that of Raydium. This round of Raydium’s standard pool made Raydium regain the share.But how long can the MEME style of Solana last? Whether the future chain is still the world of earth dogs. It is difficult to predict. When the type of market transaction variety has shifted, Raydium’s market share may face challenges.

Token emissions: Raydium’s tokens currently circulate 47.2%. Compared with most DEFI projects, it is not high. In the future, the selling pressure after the unlocking tokens may cause price pressure.However, considering that the project already has a good cash flow, it is not the only choice for selling coins, and the team may also destroy the unbroken tokens to dispel investors’ concerns.

Higher centralization: At present, Raydium has not opened the Ray -based governance procedure. The project development is completely controlled by the project party, which may cause the profit of the coinkeeper to be unable to transmit it, such as RAY, which is repurchased by the agreement,How to distribute tokens has been suspended so far.

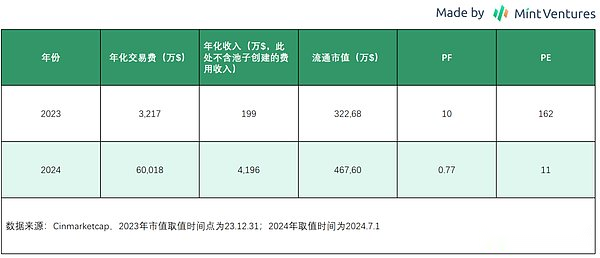

3. Staking: lido

LiDO is the leading liquid pledge agreement of Ethereum network.At the end of 2020, the launch chain was launched, marking that Ethereum’s process of turning from POW to POS officially started.Since the recovery function of the pledged assets was not yet launched, the ETH of the pledged ETH will lose liquidity.In fact, the upgrade of Shapella, which allows the assets of the assets of the letter, took place in April 2023, which means that the earliest users who entered ETH pledge could not obtain liquidity for two and a half years.

Lido pioneered this track of liquidity.The ETH of the user in the Lido will get the STETH voucher issued by Lido. Lido inspires the deep STETH-ETH LP on CURVE, thereby providing users with a stable “participating in ETH pledge to obtain benefits, and you can return it at any time at any time.ETH’s “service has begun to develop rapidly, and has gradually developed into the leader of the Ethereum pledged track.

In terms of business model, LIDO obtains 10% of its pledge income, of which 5% are allocated to pledged service providers and 5% are managed by DAO.

3.1 Business situation

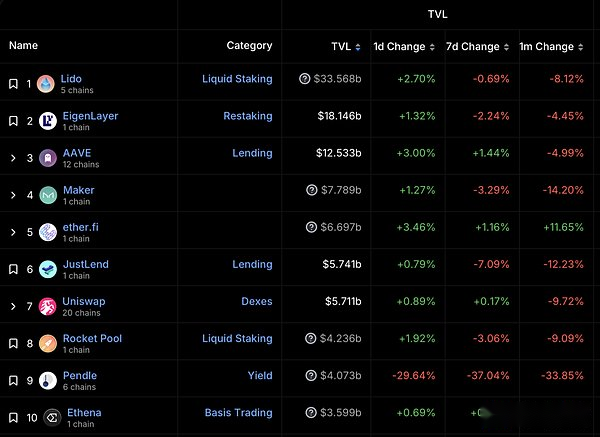

LIDO’s current main business is ETH liquidity service.Earlier, Lido was also the largest liquidity pledged service provider of Terra network and the second largest liquidity pledge service provider of Solana networks. It also actively expanded other chains such as COSMOS and Polygon, but later LidoWishingly contracted strategic shrinkage, and shifted the focus to the pledge service of the ETH network.At present, LIDO is the leader of the ETH pledge market and the highest DEFI protocol in TVL.

>

Source: DEFILLAMA

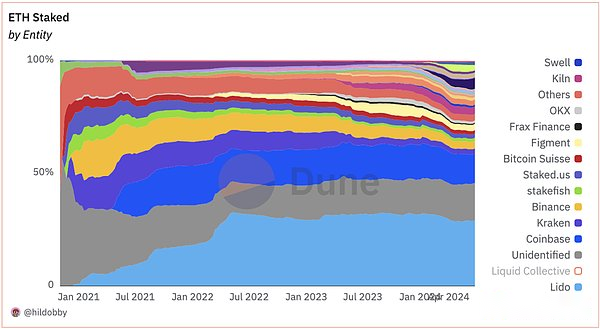

With the deep STETH-ETH liquidity of $ LDO incentives, and investment support from institutions such as Paradigm and Dragonfly in April 2021, Lido surpassed the main competitors at the end of 2021 (Kraken and Coinbase), Become the leader of Ethereum pledged track.

>

Lido spent about 280 million US dollars in 2021-2022 to motivate STETH-ETH's liquidity source: dune

However, the discussion of “whether the Lido family will affect the decentralization of Ethereum” appeared later. The Ethereum Foundation is also discussing whether it is necessary to limit the pledge share of a single entity.After touching the 32.6% high in May 2022, it began to fluctuate between 28% -32%.

>

ETH pledge market share historical situation (at the bottom light blue block is lido) source DUNE

3.2 moat

The moat of the lido business is mainly at 2 points:

-

The stable expectations brought by the long -term market leading position make Lido the first choice for giant whales and institutions to enter ETH pledge.Sun Yuchen, Mantle before the release of LST, and many giant whales are lido users.

-

The network effect brought by STETH widely used case.STETH has been fully supported by the head DEFI protocol as early as 2022. The newly developed DEFI protocol will be able to attract STETH (such as the LSTFI project that has been popular in 2023, as well as Pendle, and various LRT projectsTo.STETH is relatively stable as the basic income asset of Ethereum network.

3.3 valuation level

Although the market share of LIDO has declined slightly, the pledge scale of Lido has increased with the increase in ETH’s pledge ratio.In terms of valuation indicators, Lido’s PS and PF have recently reached a record low.

>

Source: Token Terminal

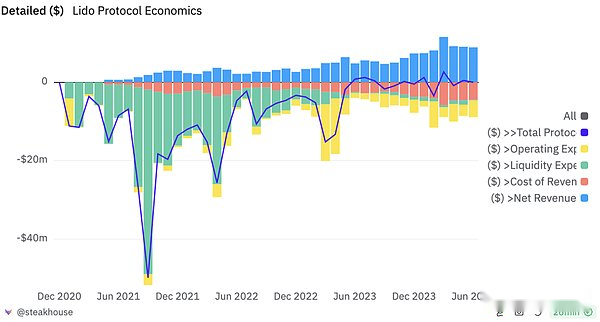

With the successful upgrade of Shapella, the market position of LIDO is stable, and the profit index of reflecting the “income -tokens incentives” indicators has also performed well. In the past year, a total of 36.35 million US dollars in profits.

>

Source: Token Terminal

This has also triggered the community’s expectations for adjustment of the $ LDO economic model.However, Lido’s actual helm Hasu once said more than once. Compared with Lido’s current expenditure, the current revenue of community vaults cannot maintain the total expenditure of LIDO DAO for a long time, and the income distribution is too early.

3.4 risk and challenge

Lido is facing the following risks and challenges:

Competition of new comers.Since the release of Eigenlayer, Lido’s market share has been declining.Any new project with sufficient token marketing budget will become competitors such as LIDO with leading advantages but tokens are close to the full circulation projects.

Some members of the Ethereum community, including the Ethereum Foundation, have a long -term question of the LIDO market share of the pledge market. Earlier, Vitalik also wrote a special article discussing this problem and sorting out various solutions.The obvious tendency of the scheme (about this issue, Mint Ventures has been analyzed in November last year, and interested readers can go to view).

SEC clearly defines LST as securities in the allegations of Consensys on June 28, 2024. The behavior of users casting and purchasing STETH is “Lido is issuing and selling unleaded securities by SEC.”The service to LIDO is also suspected of “issuance and sale of securities that have not been registered with SEC.”

4. Sustainable contract exchange: GMX

GMX is a permanent contract trading platform. It was officially launched on Arbitrum in September 2021 and launched Avalanche in January 2022.Its business is a bilateral market: one end is a trader, which can perform up to 100 times leveraged transactions; one end is a liquidity provider. They transfer their assets to traders ‘transactions and serve as traders’ opponents.

In terms of business models, transaction fees ranging from 0.05% to 0.1% of traders, as well as capital fees and borrowing fees constitute GMX income.GMX allocates 70% of the total income to liquidity providers, and the other 30% is assigned to GMX pledges.

4.1 Business situation

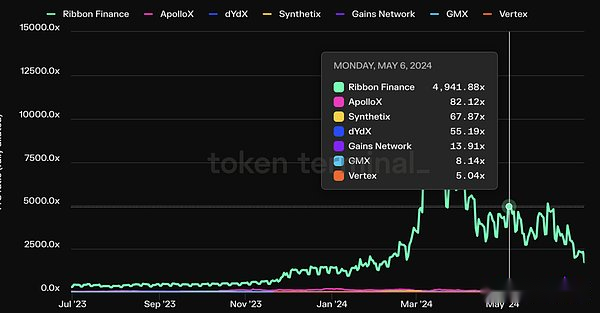

In the field of permanent contract trading platform, the new projects that indicate the traceable airdrops are frequent (such as AEVO, Hyperliquid, Synfutures, Drift, etc.), and old projects are also generally similar to similar transaction mining incentives (such asDydx, Vertex, RabbitX), making the data of the transaction volume does not have much representativeness.We will choose TVL, PS and profit indicators to compare the data of GMX and competitors horizontally.

In terms of TVL, GMX is currently the first place, but the old derivative protocol DYDX, the Jupiter Perp with a large amount of traffic in Solana, and the Hyperliquid TVL that has not yet been released is also the same level.

>

Data Source: DEFILLAMA

From the perspective of the PS indicator, in projects that have issued coin -issued, using perpetual contract transactions, and average daily transaction volume of more than $ 30 million, the GMX PS indicator is low, which is only higher than the current high.Vertex of trading mining incentive.

>

From the perspective of profit indicators, GMX’s profit in the past year is $ 6.5 million, and the data is lower than DYDX, GNS, and SNX.However, it is worth pointing out that this is largely due to the STIP event of ARBITRUM in March of this year in March of this year, GMX will get 12 million ARBs (at the price of ARB during the period, about $ 18 million), all).Released, resulting in a significant decrease in profits.From the slope of profit accumulation, we can see that GMX’s strong profit manufacturing ability.

>

4.2 Sucker River

Compared with the other DEFI projects mentioned above, GMX’s moat is relatively weak. New projects that have frequently emerged in recent years have also greatly impacted the transaction volume of GMX. The track is still crowded.The main advantages include:

ARBITRUM’s strong support.As the native project of the Arbitrum network, the GMX peak period contributed the nearly half of the ARBITRUM network. At that time, almost all the new DEFI projects on Arbitrum were “developed for GLP”. In addition to being able to obtain the official exposure of Arbitrum, it was also in the previous ARB.In the incentive activity, a large number of ARB tokens (8 million initial airdrops, 12 million STIP) were obtained, which enriched the GMX’s treasury, and also increased the valuable marketing budget.

The positive image brought by the leading position of the long -term industry.GMX led the narrative of “Real Evented DEFI” in the second half of 2022 to the first half of 23. It is the rare highlight of the market for the bear time in the market. GMX has taken this opportunity to accumulate a good brand image and accumulate a lotLoyal users.

A certain degree of scale effect.Trading platforms such as GMX have a scale effect, because only the LP scale is large enough can a larger amount of transaction orders and a higher liquidation contract volume, and the higher scale transaction volume can be given to LP higher in turn to higher LP higher.Increase.As the leading derivative trading platform on the chain, GMX has become the beneficiary of this scale effect.For example, the well -known trader Andrew Kang once opened a long and short position of up to tens of millions of dollars in GMX. At that time, GMX was almost the only choice for him to open such a large order on the chain.

4.3 Valuation level

GMX is currently circulating.We have performed the horizontal comparison of the same industry above. The GMX is currently the mainstream derivative exchanges with the lowest valuation.

Comparison with historical data, the revenue of GMX is relatively stable, and the PS indicator is in a low position from a historical perspective.

>

4.4 Risk and Challenge

Powerful competitors.GMX’s competitors include not only the old -fashioned but also frequent Defi protocol Synthetix and DYDX, but also each emerging agreement: AEVO and Hyperliquid who have not issued coins have obtained considerable transaction volume and exposure in the last year.The Jupiter Perp, which has a large amount of traffic entrance to Solana, only uses a mechanism that is almost completely similar to GMX, and has obtained a TVL close to GMX and the transaction volume exceeding GMX.GMX is also preparing to extend their V2 version to Solana, but the track is generally fierce in terms of competition, and it does not generally have a relatively certain pattern like other DEFI tracks.The common trading mining incentives in the industry reduces the cost of switching users, and the loyalty of users is generally low.

The price of GMX adopts the price of prophecy as the price basis for transactions and liquidation, and there is the possibility of being attacked by the prophet.In September 2022, GMX lost $ 560,000 due to the attack on Avax’s prophet attack on Avax.Of course, for most GMX’s assets that allow transactions, the cost of attack (manipulating the CEX corresponding token price) is much greater than its income.The V2 version of the GMX has also been targeted to the isolation pool and the trading slip point to respond to this risk.

5. Other Defi project worthy of attention

In addition to the DEFI project mentioned above, we have also investigated other attention DEFI projects, such as the old stabilized currency project MakerDao, Ethena, and the leader chainlink.But on the one hand, it is limited and cannot be presented in this article. On the other hand, these projects also face more problems, such as:

Although MakerDao is still a decentralized stable coin leader and has a large number of “natural currency”, these currency holders are holding DAIs like USDC and USDT, but the scale of stable currency has always stagnated, the market valueOnly about half of the previous round.Its mortgage uses a large number of US dollar assets outside the chain, and is gradually damaging the decentralized credit of its token.

In contrast to MakerDao’s DAI, Ethena’s stable currency USDE has made a high progress in scale, from about half a year to $ 3.6 billion from 0.However, Ethena’s business model (a public fund that focuses on perpetual contract arbitrage) still has obvious ceiling. Behind its large -scale expansion of stablecoins is to use the secondary market users to take over its token ENA to provide USDE to provide USDEThe premise of high income subsidies.This slightly Ponzi design can easily usher in negative spirals of business and currency when the market is poor.The key point of Ethena’s business turning point is that the USDE can one day can really become a decentralized stable currency with a large number of “natural currency”. At this point, its business model has also completed the transformation from a public offering fund to stable currency operator, but butConsidering that the underlying assets of USDE are mostly storage of arbitrage positions stored on the centralized exchange, USDE does not rely on both ends of the “decentralized anti -review” and “strong credit institution endors”.Essence

After the DEFI era, ChainLink is preparing to usher in a wave of hidden wave -level narratives, that is, represented by Berlaide, in recent years, and gradually actively embracing Web3’s financial giants, RWA narratives.In addition to promoting the listing of BTC and ETH ETFs, the most noteworthy actions of Bellaide this year are the US dollar Treasury fund that issued code on Ethereum for BUILD. The fund size exceeded 380 million US dollars within 6 weeks.The financial product experiments of subsequent traditional financial giants on the chain will continue, and they will inevitably face the problem of passing assets under the chain, as well as communication and interoperability under the chain chain.ChainLink’s exploration in this area has gone forward. For example, in May this year, Chainlink and the United States Starting Trust and Clearance Company (DTCC) and many major US financial institutions completed the “Smart Nav” pilot project.The project aims to establish a standardized process and use Chainlink’s interoperable protocol CCIP to gather and disseminate net asset value (NAV) data on private or public blockchains.In addition, in February this year, asset management company ARK Invest and 21Shares announced that it verified the positioning data by integrating the reserve of the Chainlink.However, ChainLink still faces the problem of business value and tokens. Link token lacks value capture and rigid application scenarios, making it worried that the holder is difficult to benefit from the business growth of his parent company.

Summarize

Just as many revolutionary products are developing, Defi also experienced narrative fermentation in the first 2020 after the appearance, the rapid foaming of asset prices in 21 years, and the stage of disillusionment after the cracked by the bear market in 22 years. Currently, with the productsThe full verification of PMF is coming out of the low valley of the narrative dismissal, using actual business data to build its inherent value.

>

The author believes that as a rare mature business model in the encryption field and the market space is still growing, Defi still has long -term attention and investment value.